Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 18

SPOILAGE, REWORK, AND SCRAP

18-1 Why is there an unmistakable trend in manufacturing to improve quality?

18-2 Distinguish among spoilage, rework, and scrap.

18-3 “Normal spoilage is planned spoilage.” Discuss.

Yes. Normal spoilage is spoilage inherent in a particular production process that arises even

18-4 “Costs of abnormal spoilage are losses.” Explain.

Abnormal spoilage is spoilage that is not inherent in a particular production process and would

18-5 “What has been regarded as normal spoilage in the past is not necessarily acceptable as

normal spoilage in the present or future.” Explain.

18-6 “Units of abnormal spoilage are inferred rather than identified.” Explain.

Normal spoilage typically is expressed as a percentage of good units passing the inspection

18-7 “In accounting for spoiled units, we are dealing with cost assignment rather than cost

incurrence.” Explain.

18-3

Accounting for spoiled goods deals with cost assignment, rather than with cost incurrence,

18-8 “Total input includes abnormal as well as normal spoilage and is, therefore, inappropriate

as a basis for computing normal spoilage.” Do you agree? Explain.

Yes. Normal spoilage rates should be computed from the good output or from the normal input,

not the total input. Normal spoilage is a given percentage of a certain output base. This base

18-9 “The inspection point is the key to the allocation of spoilage costs.” Do you agree?

Explain.

Yes, the point of inspection is the key to the assignment of spoilage costs. Normal spoilage costs

18-10 “The unit cost of normal spoilage is the same as the unit cost of abnormal spoilage.” Do

you agree? Explain.

No. If abnormal spoilage is detected at a different point in the production cycle than normal

18-11 “In job costing, the costs of normal spoilage that occur while a specific job is being done

are charged to the specific job.” Do you agree? Explain.

No. Spoilage may be considered a normal characteristic of a given production cycle. The costs of

18-12 “The costs of rework are always charged to the specific jobs in which the defects were

originally discovered.” Do you agree? Explain.

No. Unless there are special reasons for charging normal rework to jobs that contained the bad

18-13 “Abnormal rework costs should be charged to a loss account, not to manufacturing

overhead.” Do you agree? Explain.

18-3

Yes. Abnormal rework is a loss just like abnormal spoilage. By charging it to manufacturing

18-14 When is a company justified in inventorying scrap?

18-15 How do managers use information about scrap?

Companies measure scrap to measure efficiency and to also control a tempting source of theft.

18-16 All of the following are accurate regarding the treatment of normal or abnormal spoilage

by a firm with the exception of:

a. Abnormal spoilage is excluded in the standard cost of a manufactured product.

b. Normal spoilage is capitalized as part of inventory cost.

c. Abnormal spoilage has no financial statement impact.

d. Normal and abnormal spoilage units affect the equivalent units of production.

SOLUTION

Choice "c" is correct. This represents an inaccurate statement. Abnormal spoilage represents a

period expense that is reflected on the firm’s income statement.

18-17 Which of the following is a TRUE statement regarding the treatment of scrap by a firm?

a. Scrap is always allocated to a specific job.

18-3

b. Scrap is separated between normal and abnormal scrap.

c. Revenue received from the sale of scrap on a job lowers the total costs for that job.

d. There are costs assigned to scrap.

SOLUTION

Choice "c is correct. This is a TRUE statement. When there is scrap from a given job, and the

scrap is sold, the scrap revenues serve to reduce the total costs of the job.

18-18 Healthy Dinners Co. produces frozen dinners for the health conscious consumer. During

the quarter ended September 30, the company had the following cost data:

Dinner ingredients $3,550,000

Preparation labor 900,000

Sales and marketing costs 125,000

Plant production overhead 50,000

Normal food spoilage 60,000

Abnormal food spoilage 40,000

General and administrative expenses 75,000

Based on the above, what is the total amount of period expenses reflected in the company’s

income statement for the quarter ended September 30?

a. $200,000 b. $240,000

c. $290,000 d. $300,000

SOLUTION

Choice "b" is correct. Healthy Dinners Co. would recognize the following period expenses on the

income statemen:

Choice "a" is incorrect. This answer choice treated both normal spoilage and abnormal spoilage

as product costs. Only normal spoilage is classified as a product cost.

18-19 Fresh Products, Inc. incurred the following costs during December related to the

18-3

production of its 162,500 frozen ice cream cone specialty items:

Food product labor $175,000

Ice cream cone ingredients 325,000

Sales and marketing costs 10,000

Factory overhead 16,000

Normal food spoilage 4,000

Abnormal spoilage 3,000

What is the per unit inventory cost allocated to the company’s frozen ice cream cone specialty

items for December?

a. $3.18 b. $3.20

c. $3.22 d. $3.26

SOLUTION

Choice "b" is correct. The total inventory cost is determined as follows:

Choice "a" is incorrect. This answer choice treats normal spoilage as a period cost instead of a

product cost.

18-20 Normal and abnormal spoilage in units. The following data, in physical units, describe

a grinding process for January:

Work in process, beginning 19,300

Started during current period 145,400

To account for 164,700

Spoiled units 12,000

Good units completed and transferred out 128,000

18-3

Work in process, ending 24,700

Accounted for 164,700

Required:

Inspection occurs at the 100% completion stage. Normal spoilage is 5% of the good units passing

inspection.

1. Compute the normal and abnormal spoilage in units.

2. Assume that the equivalent-unit cost of a spoiled unit is $8. Compute the amount of potential

savings if all spoilage were eliminated, assuming that all other costs would be unaffected.

Comment on your answer.

SOLUTION

(5–10 min.) Normal and abnormal spoilage in units.

Regardless of the targeted normal spoilage, abnormal spoilage is non-recurring and

avoidable. The targeted normal spoilage rate is subject to change. Many companies have reduced

their spoilage to almost zero, which would realize all potential savings. Of course, zero spoilage

usually means higher-quality products, more customer satisfaction, more employee satisfaction,

and various beneficial effects on nonmanufacturing (for example, purchasing) costs of direct

materials.

18-21 Weighted-average method, spoilage, equivalent units. (CMA, adapted) Consider the

following data for November 2017 from MacLean Manufacturing Company, which makes silk

pennants and uses a process-costing system. All direct materials are added at the beginning of the

process, and conversion costs are added evenly during the process. Spoilage is detected upon

inspection at the completion of the process. Spoiled units are disposed of at zero net disposal

value. MacLean Manufacturing Company uses the weighted-average method of process costing.

Physical Units

(Pennants)

Direct

Materials

Conversion

Costs

Work in process, November 1a1,350 $ 966 $ 711

Started in November 2017 ?

Good units completed and transferred

out during November 2017

8,800

Normal spoilage 80

Abnormal spoilage 50

Work in process, November 30b1,700

Total costs added during November 2017 $10,302 $30,055

18-3

aDegree of completion: direct materials, 100%; conversion costs, 45%.

bDegree of completion: direct materials, 100%; conversion costs, 35%.

Required:

Compute equivalent units for direct materials and conversion costs. Show physical units in the

first column of your schedule.

SOLUTION

(20 min.) Weighted-average method, spoilage, equivalent units.

Solution Exhibit 18-21 calculates equivalent units of work done to date for direct materials and

conversion costs.

SOLUTION EXHIBIT 18-21

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

Weighted-Average Method of Process Costing with Spoilage,

MacLean Manufacturing Company for November 2017.

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

18-22 Weighted-average method, assigning costs (continuation of 18-21).

Required:

For the data in Exercise 18-21, summarize the total costs to account for; calculate the cost per

equivalent unit for direct materials and conversion costs; and assign costs to units completed and

transferred out (including normal spoilage), to abnormal spoilage, and to units in ending

work-in-process inventory.

SOLUTION

(2025 min.) Weighted-average method, assigning costs (continuation of 18-21).

18-3

Solution Exhibit 18-22 summarizes total costs to account for, calculates the costs per equivalent

unit for direct materials and conversion costs, and assigns total costs to units completed and

transferred out (including normal spoilage), to abnormal spoilage, and to ending work in process.

SOLUTION EXHIBIT 18-22

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign

Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process Inventory;

Weighted-Average Method of Process Costing,

MacLean Manufacturing Company, November 2017.

Total

Production

Costs

Direct

Materials

Conversion

Costs

#Equivalent units of direct materials and conversion costs calculated in Step 2 in Solution Exhibit 18-21.

18-23 FIFO method, spoilage, equivalent units. Refer to the information in Exercise 18-21.

Suppose MacLean Manufacturing Company uses the FIFO method of process costing instead of

the weighted-average method.

Required:

Compute equivalent units for direct materials and conversion costs. Show physical units in the

first column of your schedule.

SOLUTION

(15 min.) FIFO method, spoilage, equivalent units.

Solution Exhibit 18-23 calculates equivalent units of work done in the current period for direct

materials and conversion costs.

SOLUTION EXHIBIT 18-23

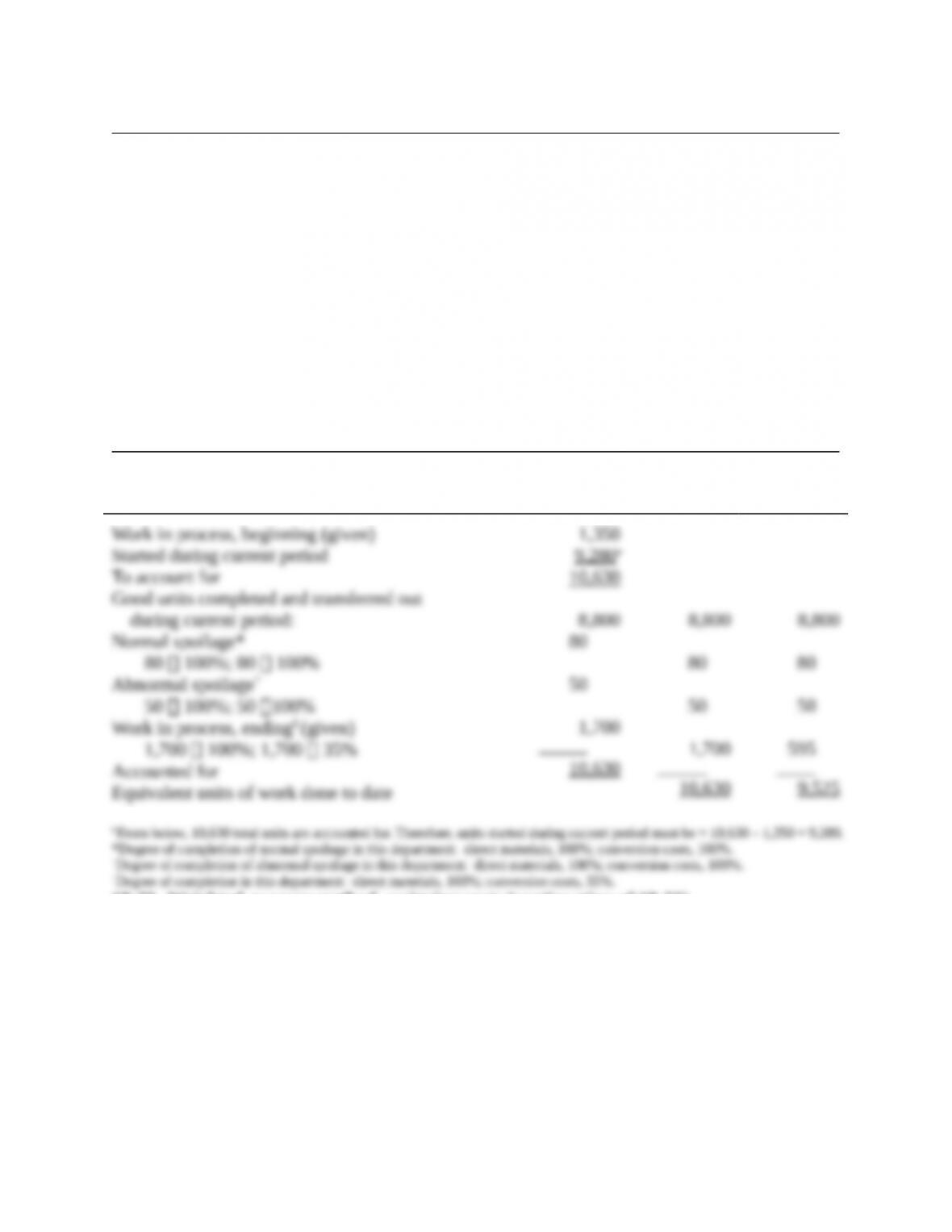

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

First-in, First-out (FIFO) Method of Process Costing with Spoilage,

MacLean Manufacturing Company for November 2017.

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given) 1,350

18-3

a From below, 10,630 total units are accounted for. Therefore, units started during current period must be 10,63 –

1,350 = 9,280.

||Degree of completion in this department: direct materials, 100%; conversion costs, 45%.

#8,800 physical units completed and transferred out minus 1,350 physical units completed and transferred out from

beginning work-in-process inventory.

18-24 FIFO method, assigning costs (continuation of 18-23).

Required:

For the data in Exercise 18-21, use the FIFO method to summarize the total costs to account for;

calculate the cost per equivalent unit for direct materials and conversion costs; and assign costs

to units completed and transferred out (including normal spoilage), to abnormal spoilage, and to

units in ending work in process.

SOLUTION

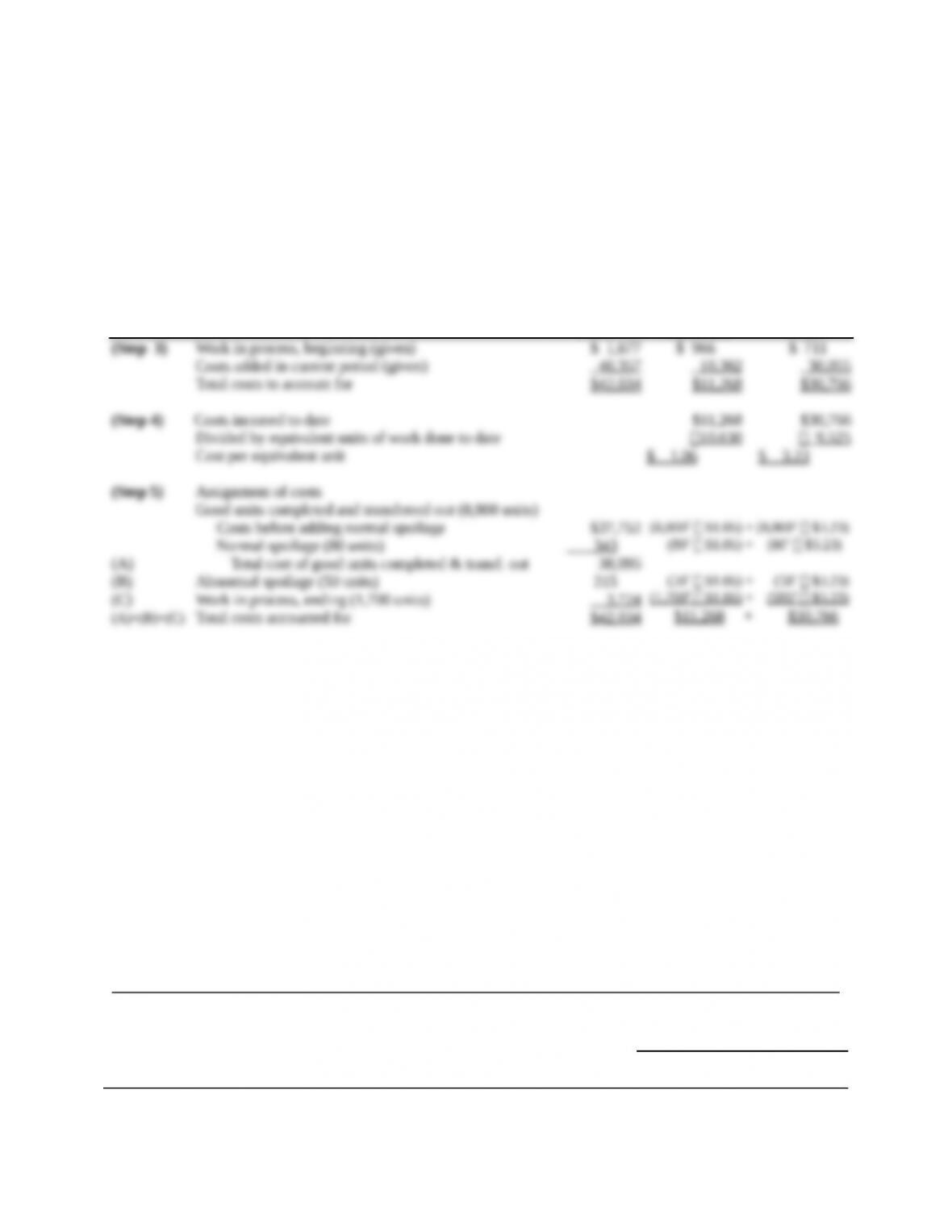

(2025 min.) FIFO method, assigning costs (continuation of 18-23).

Solution Exhibit 18-24 summarizes total costs to account for, calculates the costs per equivalent

unit for direct materials and conversion costs, and assigns total costs to units completed and

transferred out (including normal spoilage), to abnormal spoilage, and to ending work in process.

18-3