SOLUTION

(35 min.) Weighted-average method, Shipping Department (continuation of 18-36).

For the Shipping Department, Solution Exhibit 18-37 summarizes total costs to account for,

calculates the equivalent units of work done to date for each cost category, and assigns costs to

units completed (including normal spoilage), to abnormal spoilage, and to units in ending work

in process using the weighted-average method.

SOLUTION EXHIBIT 18-37

Weighted-Average Method of Process Costing with Spoilage,

Shipping Department of World Class Steaks for May

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units

(Step 1) (Step 2)

Equivalent Units

Flow of Production

Physical

Units

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

To account for

Good units completed and transferred out

during current period:

Accounted for

Equivalent units of work done to date

25,200

49 ,2 00

74 ,4 00

52,800

52,800

52,800

52,800

* Normal spoilage is 7% of good units transferred out: 7% 52,800 = 3,696 units. Degree of completion of normal spoilage in

this department: transferred-in costs, 100%; direct materials, 100%; conversion costs, 100%.

PANEL B: Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit,

and Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process

Inventory

Total

Production

Costs

Transferred-in

costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given) $ 114,347 $ 67,397 $ 0 $46,950

18-F

Costs added in current period (given)

Total costs to account for

275 ,053

$ 389 ,400

181 ,843*

$249 ,240

11 ,520

$11 ,520

81 ,690

$128 ,640

* Total costs of good units completed and transferred out in Panel B (Step 5) of Solution Exhibit 18-35.

# Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A above.

18-38 FIFO method, shipping department (continuation of 18-36). Refer to the

information in Problem 18-37 except that the transferred-in costs of beginning work in

process on May 1 are $66,180 (instead of $67,397). Transferred-in costs for May equal the

total cost of good units completed and transferred out in May from the prep department, as

calculated in Problem 18-36 using the FIFO method of process costing.

Required:

For the shipping department, use the FIFO method to summarize the total costs to account for

and assign those costs to units completed and transferred out (including normal spoilage), to

abnormal spoilage, and to units in ending work in process.

SOLUTION

(25 min.) FIFO method, Shipping Department (continuation of 18-37).

Solution Exhibit 18-38 summarizes the total Shipping Department costs for May, shows the

equivalent units of work done in the Shipping Department in the current period for transferred-in

costs, direct materials, and conversion costs, and assigns total costs to units completed and

transferred out (including normal spoilage), to abnormal spoilage, and to units in ending

work-in-process under the FIFO method.

SOLUTION EXHIBIT 18-38

First-in, First-out (FIFO) Method of Process Costing with Spoilage,

Shipping Department of World Class Steaks for May

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units

18-F

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

To account for

Good units completed and transferred out during

current period:

From beginning work in process||

25,200 (100% 100%); 25,200

(100% 0%); 25,200 (100% 70%)

Equivalent units of work done in current period

25,200

49 ,2 00

74 ,4 00

25,200

0

25,200

7,560

|| Degree of completion in this department: transferred-in costs, 100%; direct materials, 0%; conversion costs, 70%.

# 52,800 physical units completed and transferred out minus 25,200 physical units completed and transferred out

from beginning work-in-process inventory.

PANEL B: Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit,

and Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process

Inventory

Total

Production

Costs

Transferred-

in Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

Cost per equivalent unit

$113,130

274 ,254

$ 387 ,384

$ 66,180

181,044*

$247,224

$ 0

11,520

$11,520

$ 46,950

81,690

$128,640

18-F

(Step 5) Assignment of costs:

Good units completed and transferred out

(52,800 units)

(A)+(B)+(C) Total costs accounted for

$387 ,396 +

* Total costs of good units completed and transferred out in Step 5, Panel B of Solution Exhibit 18-36.

§ Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A.

18-39 Physical units, inspection at various levels of completion, weighted-average process

costing. SunEnergy produces solar panels. A key step in the conversion of raw silicon to a

completed solar panel occurs in the assembly department, where lightweight photovoltaic cells

are assembled into modules and connected on a frame. In this department, materials are added at

the beginning of the process and conversion takes place uniformly.

At the start of November 2017, SunEnergy’s assembly department had 2,400 panels in

beginning work in process, which were 100% complete for materials and 40% complete for

conversion costs. An additional 12,000 units were started in the department in November, and

3,600 units remain in work in process at the end of the month. These unfinished units are 100%

complete for materials and 70% complete for conversion costs.

The assembly department had 1,800 spoiled units in November. Because of the difficulty

of keeping moisture out of the modules and sealing the photovoltaic cells between layers of

glass, normal spoilage is approximately 12% of good units. The department’s costs for the

month of November are as follows:

Beginning WIP Costs Incurred During Period

Direct materials costs $ 76,800 $ 240,000

Conversion costs 123,000 1,200,000

Required:

1. Using the format on page 728, compute the normal and abnormal spoilage in units for

November, assuming the inspection point is at (a) the 30% stage of completion, (b) the 60%

stage of completion, and (c) the 100% stage of completion.

2. Refer to your answer in requirement 1. Why are there different amounts of normal and

18-F

abnormal spoilage at different inspection points?

3. Now assume that the assembly department inspects at the 60% stage of completion. Using

the weighted-average method, calculate the cost of units transferred out, the cost of abnormal

spoilage, and the cost of ending inventory for the assembly department in November.

SOLUTION

(30 min.) Physical units, inspection at various levels of completion, weighted-average

process costing.

1.

Inspection Inspection Inspection

at 30% at 60% at 100%

Work in process, beginning (40%)*

Started during November

To account for

2,400

12 ,000

14 ,400

2,400

12 ,000

14 ,400

2,400

12 ,000

14 ,400

*Degree of completion for conversion costs at the dates of the work-in-process inventories

a2,400 beginning inventory + 12,000 started – 1,800 spoiled – 3,600 ending inventory = 9,000.

2. There are different amounts of normal and abnormal spoilage because the spoilage is detected

at different points in the process. At the 30% inspection point, the beginning work in process

inventory has already passed inspection and consists entirely of good units. At the 60%

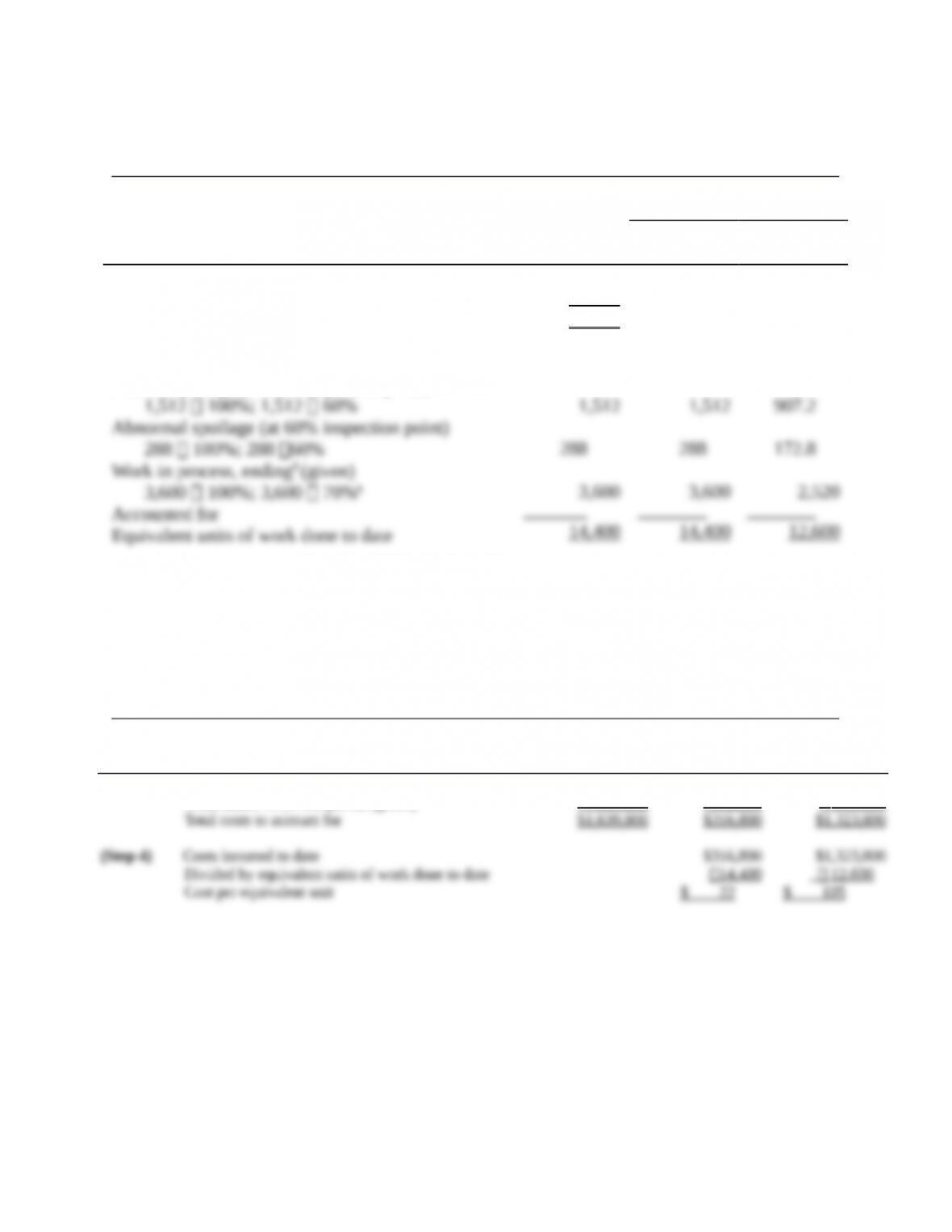

3. Solution Exhibit 18-39 summarizes total costs to account for, calculates the equivalent units of

SOLUTION EXHIBIT 18-39

Weighted-Average Method of Process Costing with Spoilage,

Assembly Department of SunEnergy for November 2017

18-F

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units

(Step 1) (Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

To account for

Good units completed and transferred out

during current period:

Normal spoilage (at 60% inspection point)

Equivalent units of work done to date

2,400

12 ,000

14 ,4 00

9,000

9,000

9,000

aDegree of completion in this department: direct materials, 100%; conversion costs, 70%.

PANEL B: Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit,

and Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process

Inventory

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

(Step 5) Assignment of costs

Good units completed and transferred out (9,000 units)

$ 199,800

1 ,444,000

$ 76,800

240 ,000

$ 123,000

1 ,200,000

18-F

(A)+(B)+(C) Total costs accounted for

$ 1 ,639,800

(288 22)

+

( 3,600 22)

+

$316 ,800 +

$1,323,000

#Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A above.

18-40 Spoilage in job costing. Jellyfish Machine Shop is a manufacturer of motorized carts for

vacation resorts.

Patrick Cullin, the plant manager of Jellyfish, obtains the following information for Job #10

in August 2017. A total of 46 units were started, and 6 spoiled units were detected and rejected at

final inspection, yielding 40 good units. The spoiled units were considered to be normal spoilage.

Costs assigned prior to the inspection point are $1,100 per unit. The current disposal price of the

spoiled units is $235 per unit. When the spoilage is detected, the spoiled goods are inventoried at

$235 per unit.

Required:

1. What is the normal spoilage rate?

2. Prepare the journal entries to record the normal spoilage, assuming the following:

a. The spoilage is related to a specific job.

b. The spoilage is common to all jobs.

c. The spoilage is considered to be abnormal spoilage.

SOLUTION

(15 min.) Spoilage in job costing

1. Normal spoilage rate= Units of normal spoilage ÷ Total good units completed

2.

a) Journal entry for spoilage related to a specific job:

b) Journal entry for spoilage common to all jobs:

18-F

Note: In developing the predetermined O/H rate, the budgeted manufacturing overhead would

include expected normal spoilage costs.

c) Journal entry for abnormal spoilage:

Note: If the spoilage is abnormal, the net loss is highlighted and always charged to an abnormal

loss account.

18-41 Rework in job costing, journal entry (continuation of 18-40). Assume that the 6

spoiled units of Jellyfish Machine Shop’s Job #10 can be reworked for a total cost of $1,800. A

total cost of $6,600 associated with these units has already been assigned to Job #10 before the

rework.

Required:

Prepare the journal entries for the rework, assuming the following:

a. The rework is related to a specific job.

b. The rework is common to all jobs.

c. The rework is considered to be abnormal.

SOLUTION

(10 min.) Rework in job costing, journal entry (continuation of 18-40)

a) Journal entry for rework related to a specific job:

b) Journal entry for rework common to all jobs:

c) Journal entry for abnormal rework:

18-42 Scrap at time of sale or at time of production, journal entries (continuation of

18-40). Assume that Job #10 of Jellyfish Machine Shop generates normal scrap with a total sales

value of $700 (it is assumed that the scrap returned to the storeroom is sold quickly).

18-F

Required:

Prepare the journal entries for the recognition of scrap, assuming the following:

a. The value of scrap is immaterial and scrap is recognized at the time of sale.

b. The value of scrap is material, is related to a specific job, and is recognized at the time of

sale.

c. The value of scrap is material, is common to all jobs, and is recognized at the time of sale.

d. The value of scrap is material, and scrap is recognized as inventory at the time of production

and is recorded at its net realizable value.

SOLUTION

(10 min.) Scrap at time of sale or at time of production, journal entries (continuation of

18-41)

a) Journal entry for recognizing immaterial scrap at time of sale:

(To record other revenue sale of scrap)

b) Journal entry for recognizing material scrap related to a specific job at time of sale:

c) Journal entry for recognizing material scrap common to all jobs at time of sale:

d) Journal entry for recognizing material scrap as inventory at time of production and recording

at net realizable value:

(When later sold)

18-43 Physical units, inspection at various stages of completion. Chemet manufactures

chemicals in a continuous process. The company combines various materials in a specially

configured machine at the beginning of the process, and conversion is considered uniform

through the period. Occasionally, the chemical reactions among the materials do not work as

expected and the output is then considered spoiled. Normal spoilage is 4% of the good units that

pass inspection. The following information pertains to March 2017:

18-F

Required:

Using the format on page 728, compute the normal and abnormal spoilage in units, assuming the

inspection point is at (a) the 20% stage of completion, (b) the 45% stage of completion, and (c)

the 100% stage of completion.

18-F