SOLUTION

(30 min.) Make versus buy, activity-based costing, opportunity costs.

1. Relevant costs under buy alternative:

Relevant costs under make alternative:

The allocated fixed plant administration, taxes, and insurance will not change if

Lexington makes or buys the burners. Hence, these costs are irrelevant to the make-or-buy

decision. The analysis indicates that it is less costly for Lexington to make rather than buy the

burners from the outside supplier.

2. Relevant costs under the make alternative:

Relevant costs under the buy alternative:

Additional contribution margin from using the space

where the burners were made to upgrade the grills by

Lexington should buy the side burners from an outside vendor and use its own capacity to

upgrade its grills.

3. In this requirement, the decision on making the rotisserie attachments is irrelevant to the

analysis because the rotisserie attachments increase operating income and they will be

made whether the burners are purchased or made.

Relevant cost of manufacturing burners:

11-

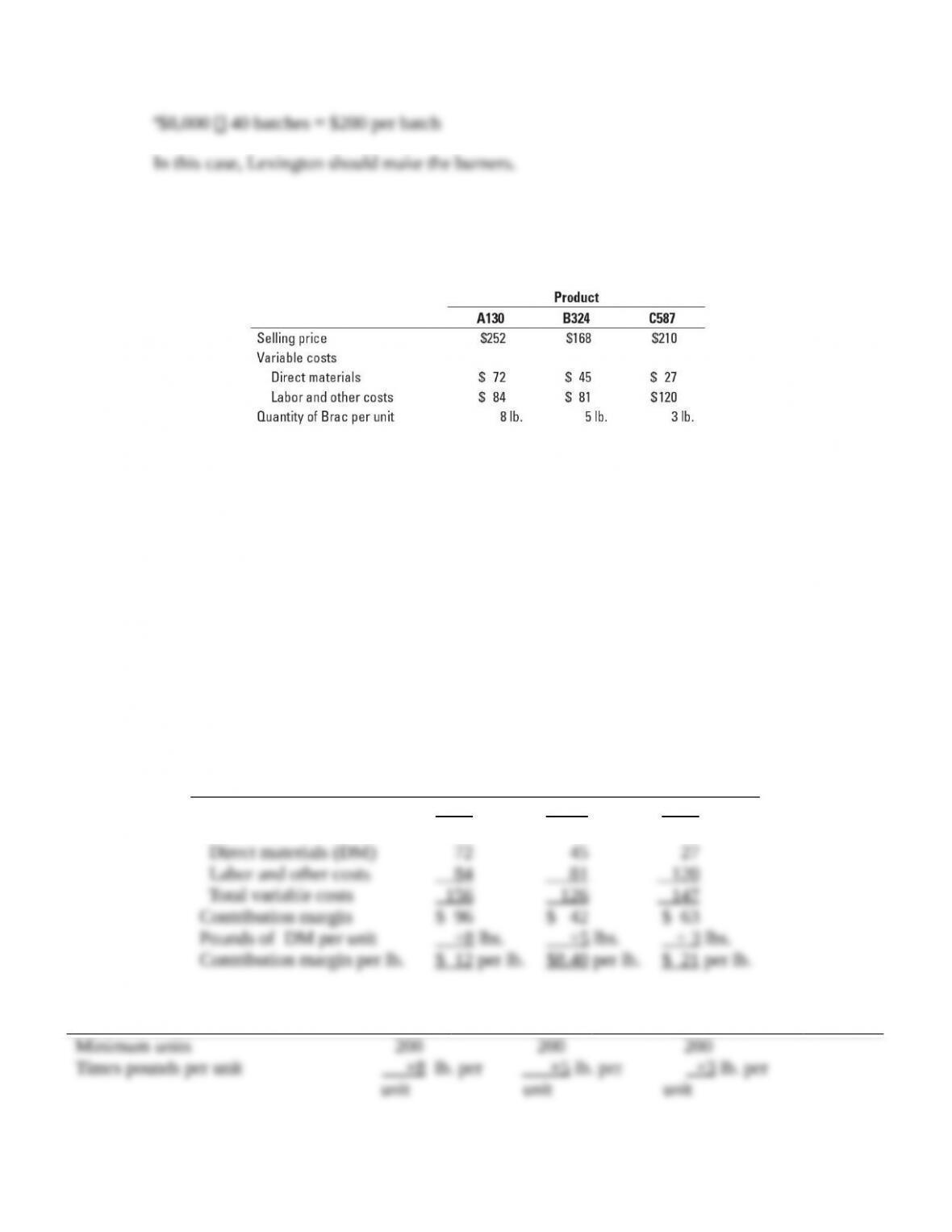

11-42 Product mix, constrained resource. Wechsler Company produces three products: A130,

B324, and C587. All three products use the same direct material, Brac. Unit data for the three

products are:

The demand for the products far exceeds the direct materials available to produce the products.

Brac costs $9 per pound, and a maximum of 5,000 pounds is available each month. Wechsler

must produce a minimum of 200 units of each product.

Required:

1. How many units of product A130, B324, and C587 should Wechsler produce?

2. What is the maximum amount Wechsler would be willing to pay for another 1,200 pounds of

Brac?

SOLUTION

(25 min.) Product mix, constrained resource.

1.

A130 B324 C587

Selling price $252 $ 168 $210

Variable costs:

First, satisfy minimum requirements.

A130 B324 C587 Total

11-

The remaining 1,800 pounds (5,000 – 3,200) should be devoted to C587 because it has the

highest contribution margin per pound of direct material. Because each unit of C587 requires 3

pounds of Brac, the remaining 1,800 pounds can be used to produce another 600 units of C587.

The following combination yields the highest contribution margin given the 5,000 pounds

constraint on availability of Brac.

2. The demand for Wechsler’s products exceeds the materials available. Assuming that fixed

costs are covered by the original product mix, Wechsler would be willing to pay up to an

additional $21 per pound (the contribution margin per pound of C587) for another 1,200 pounds

of Brac. That is, Wechsler would be willing to pay $9 + $21 = $30 per pound of Brac for the

pounds of Brac that will be used to produce C587.1 If sufficient demand does not exist for 400

units (1,200 pounds ÷ 3 pounds per unit) of C587, then the maximum price Wechsler would be

willing to pay is an additional $12 per pound (the contribution margin per pound of A130) for the

pounds of Wechsler that will be used to produce A130. In this case Wechsler would be willing to

pay $9 + $12 = $21 pound. If all the 1,200 pounds of Brac are not used to satisfy the demand for

C587 and A130, then the maximum price Wechsler would be willing to pay is an additional

$8.40 per pound (the contribution margin per pound of B324) for the pounds of Brac that will be

used to produce B324. Wechsler would be willing to pay $8.40 + $9 = $17.40 per pound of

Brac.

1An alternative calculation focuses on column 3 for C587 of the table in requirement 1.

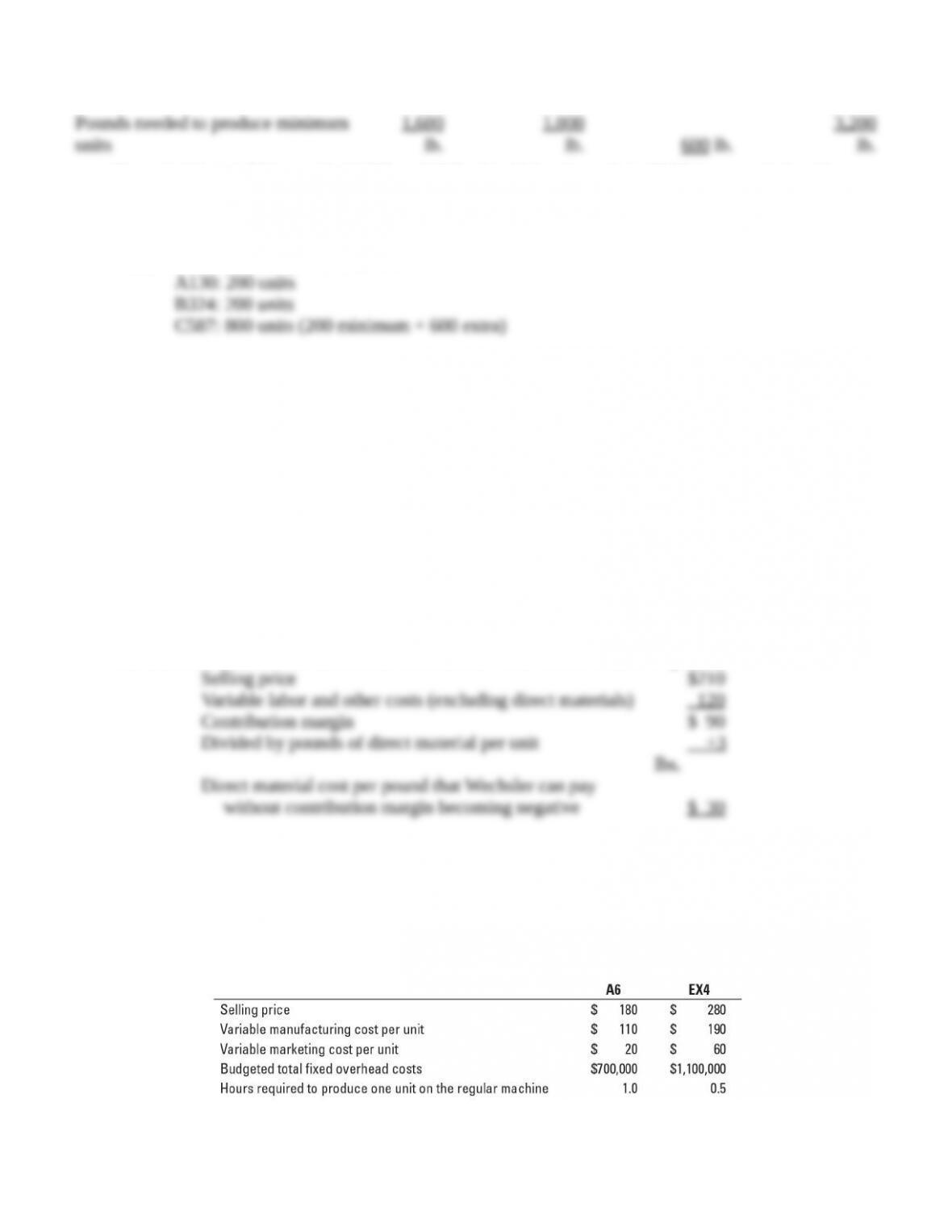

11-43 Product mix, special order. (N. Melumad, adapted) Gormley Precision Tools makes

cutting tools for metalworking operations. It makes two types of tools: A6, a regular cutting tool,

and EX4, a high-precision cutting tool. A6 is manufactured on a regular machine, but EX4 must

be manufactured on both the regular machine and a high-precision machine. The following

information is available:

11-

Additional information includes the following:

a. Gormley faces a capacity constraint on the regular machine of 50,000 hours per year.

b. The capacity of the high-precision machine is not a constraint.

c. Of the $1,100,000 budgeted fixed overhead costs of EX4, $600,000 are lease payments for

the high-precision machine. This cost is charged entirely to EX4 because Gormley uses the

machine exclusively to produce EX4. The company can cancel the lease agreement for the

high-precision machine at any time without penalties.

d. All other overhead costs are fixed and cannot be changed.

Required:

1. What product mix—that is, how many units of A6 and EX4—will maximize Gormley’s

operating income? Show your calculations.

2. Suppose Gormley can increase the annual capacity of its regular machines by 15,000

machine-hours at a cost of $300,000. Should Gormley increase the capacity of the regular

machines by 15,000 machine-hours? By how much will Gormley’s operating income

increase or decrease? Show your calculations.

3. Suppose that the capacity of the regular machines has been increased to 65,000 hours.

Gormley has been approached by Clark Corporation to supply 20,000 units of another cutting

tool, V2, for $240 per unit. Gormley must either accept the order for all 20,000 units or reject

it totally. V2 is exactly like A6 except that its variable manufacturing cost is $130 per unit. (It

takes 1 hour to produce one unit of V2 on the regular machine, and variable marketing cost

equals $20 per unit.) What product mix should Gormley choose to maximize operating

income? Show your calculations.

SOLUTION

(30–40 min.) Product mix, relevant costs.

1.

A6 EX4

Selling price $ 180 $ 280

Even though EX4 has the higher contribution margin per unit of the constrained resource, the

fact that Gormley must incur additional costs of $600,000 to achieve this higher contribution

margin means that Gormley is better off using its entire 50,000-hour capacity on the regular

2. If capacity of the regular machines is increased by 15,000 machine-hours to 65,000

machine-hours (50,000 originally + 15,000 new), the net relevant benefit from producing A6 and

EX4 is as follows:

A6 EX4

Total contribution margin from selling only

A6 or only EX4

Adding 15,000 machine-hours of capacity for regular machines and using all the capacity to

produce EX4 increases operating income by $3,000,000.

Investing in the additional capacity increases Gormley’s operating income by $500,000

3.

A6 EX4 V2

11-

Selling price $180 $280 $240

Contribution margin per unit of the constrained resource

$50

1

= $50;

$30

0.5

$30

0.5

= $60;

$70

1

$90

1

= $90

The first step is to compare the operating profits that Gormley could earn if it accepted the

Clark Corporation offer for 20,000 units with the operating profits Gormley is currently

earning. V2 has the highest contribution margin per hour on the regular machine and

A6 EX4

Total contribution margin from selling only

Gormley should use all the 45,000 hours of available capacity to produce 45,000 units of A6.

Thus, the product mix that maximizes operating income is 20,000 units of V2, 45,000 units of

11-44 Theory of constraints, throughput margin, and relevant costs. Washington Industries

manufactures electronic testing equipment. Washington also installs the equipment at

customers’ sites and ensures that it functions smoothly. Additional information on the

manufacturing and installation departments is as follows (capacities are expressed in terms of

the number of units of electronic testing equipment):

11-

Washington manufactures only 250 units per year because the installation department has only

enough capacity to install 250 units. The equipment sells for $55,000 per unit (installed) and has

direct material costs of $30,000. All costs other than direct material costs are fixed. The

following requirements refer only to the preceding data. There is no connection between the

requirements.

Required:

1. Washington’s engineers have found a way to reduce equipment manufacturing time. The new

method would cost an additional $500 per unit and would allow Washington to manufacture

30 additional units a year. Should Washington implement the new method? Show your

calculations.

2. Washington’s designers have proposed a change in direct materials that would increase direct

material costs by $2,000 per unit. This change would enable Washington to install 285 units

of equipment each year. If Washington makes the change, it will implement the new design

on all equipment sold. Should Washington use the new design? Show your calculations.

3. A new installation technique has been developed that will enable Washington’s engineers to

install 7 additional units of equipment a year. The new method will increase installation costs

by $145,000 each year. Should Washington implement the new technique? Show your

calculations.

4. Washington is considering how to motivate workers to improve their productivity (output

per hour). One proposal is to evaluate and compensate workers in the manufacturing and

installation departments on the basis of their productivities. Do you think the new proposal

is a good idea? Explain briefly.

SOLUTION

(20 min.) Theory of constraints, throughput contribution, relevant costs.

1. It will cost Washington $500 per unit to reduce manufacturing time. But manufacturing is

2. Increase in throughput margin, $25,000 5 units, $ 875,000

Alternatively, compare throughput margin under each alternative.

11-

3. Increase in throughput margin, $25,000 units $ 175,000

4. Motivating installation workers to increase productivity is worthwhile because

installation is a bottleneck operation, and any increase in productivity at the bottleneck will

increase throughput margin. On the other hand, motivating workers in the manufacturing

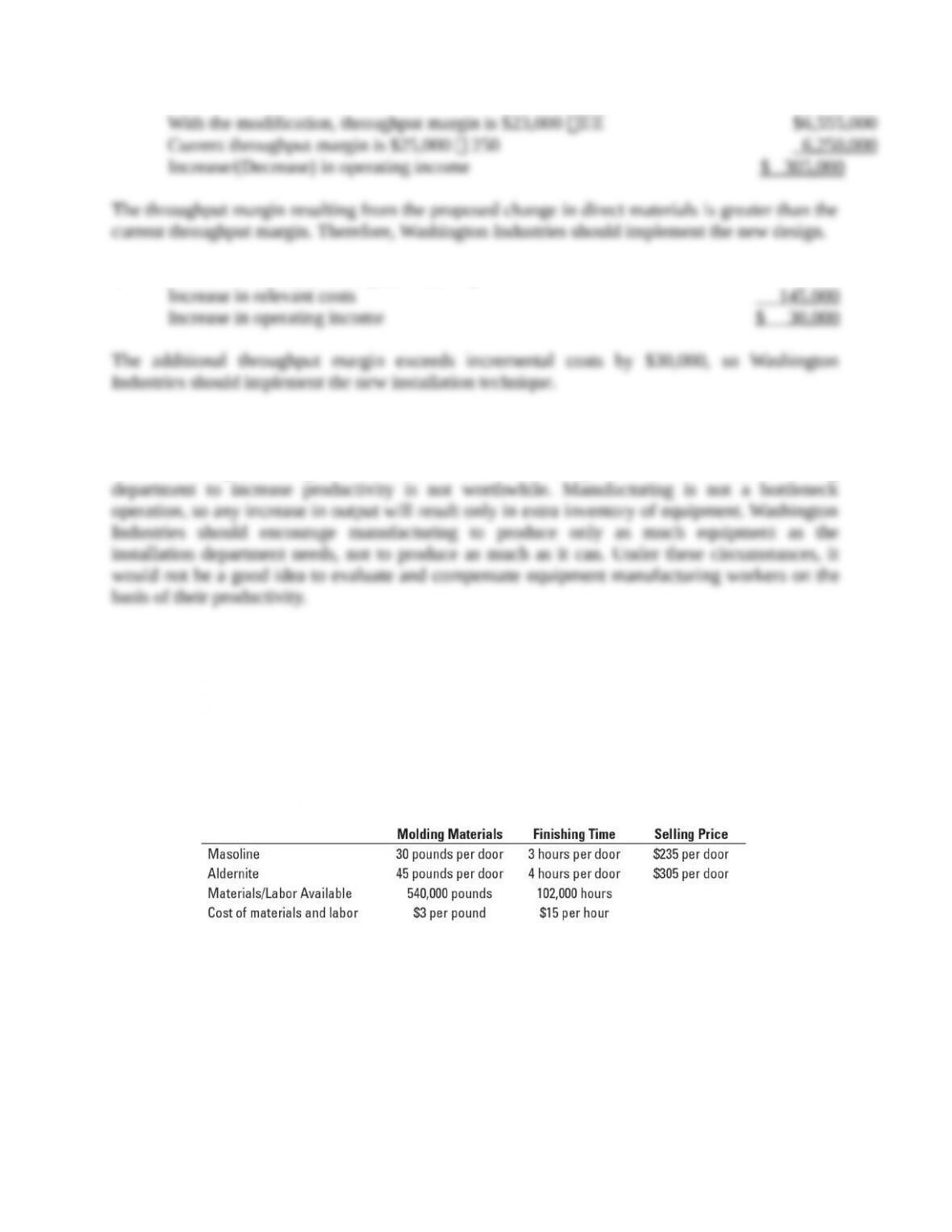

11-45 Theory of constraints, contribution margin, sensitivity analysis. Damon Furniture

(DF) produces fiberglass doors in two processes: molding and finishing. DF is currently

producing two models: Masoline and Aldernite. Production in the molding department is limited

by the amount of materials available. Production in the finishing department is limited by the

amount of trained labor available. The only variable costs are materials in the molding

department and labor in the finishing department. Following are the requirements and limitations

by model and department:

The following requirements refer only to the preceding data. There is no connection between the

requirements.

Required:

1. If there were enough demand for either door, which door would DF produce? How many of

these doors would it make and sell?

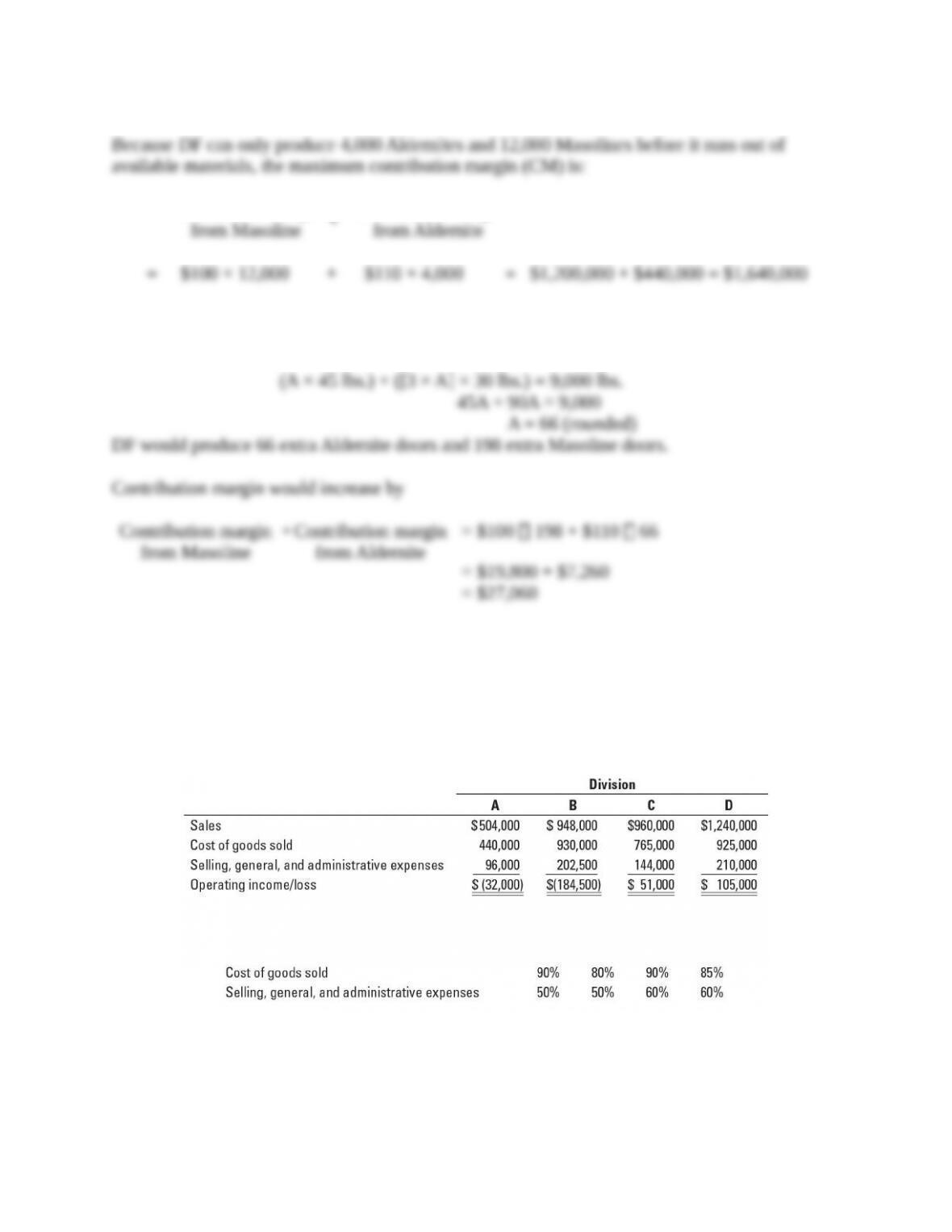

2. If DF sells three Masoline for each Aldernite, how many doors of each type would it produce

and sell? What would be the total contribution margin?

11-

3. If DF sells three Masoline for each Aldernite, how much would production and contribution

margin increase if the molding department could buy 9,000 more pounds of materials for $3

per pound?

4. If DF sells three Masoline for each Aldernite, how much would production and contribution

margin increase if the assembly department could get 780 more labor hours at $15 per hour?

SOLUTION

11-45 (30-35 min.) Theory of constraints, contribution margin, sensitivity analysis.

1. Assuming only one type of door is produced, the maximum production in each

department given their resource constraints is:

Molding

Department

Finishing Department Contribution Margin

Masoline

540,000 lbs = 18,000

30 lbs

102,000 hours = 34,000

3 hours

$235 − 30 × $3 – 3 × $15

= $100

Aldernite

540,000 lbs = 12,000

45 lbs

102,000 hours = 25,500

4 hours

$305 − 45 × $3 – 4 × $15

= $110

For both types of doors, the constraining resource is the availability of material because this

constraint causes the lowest maximum production.

2. As shown in Requirement 1, available material in the Molding department is the limiting

constraint.

If DF sells three Masolines for each Aldernite, then the maximum number of Aldernite doors the

Molding Department can produce (where the number of Aldernite doors is denoted as A) is:

11-

Contribution margin

3. With 9,000 more pounds of materials, DF would produce more doors. Using the same

technique as in Requirement 2, the increase in production is:

4. With 780 more labor hours, production would not change. The limiting constraint is

pounds of material, not labor hours. DF already has more labor hours available than it needs.

11-46 Closing down divisions. Ainsley Corporation has four operating divisions. The budgeted

revenues and expenses for each division for 2017 follows:

Further analysis of costs reveals the following percentages of variable costs in each division:

Closing down any division would result in savings of 40% of the fixed costs of that division.

Top management is very concerned about the unprofitable divisions (A and B) and is

considering closing them for the year.

11-

Required:

1. Calculate the increase or decrease in operating income if Ainsley closes division A.

2. Calculate the increase or decrease in operating income if Ainsley closes division B.

3. What other factors should the top management of Ainsley consider before making a

decision?

11-