SOLUTION

(60 min.) Comprehensive variance analysis review

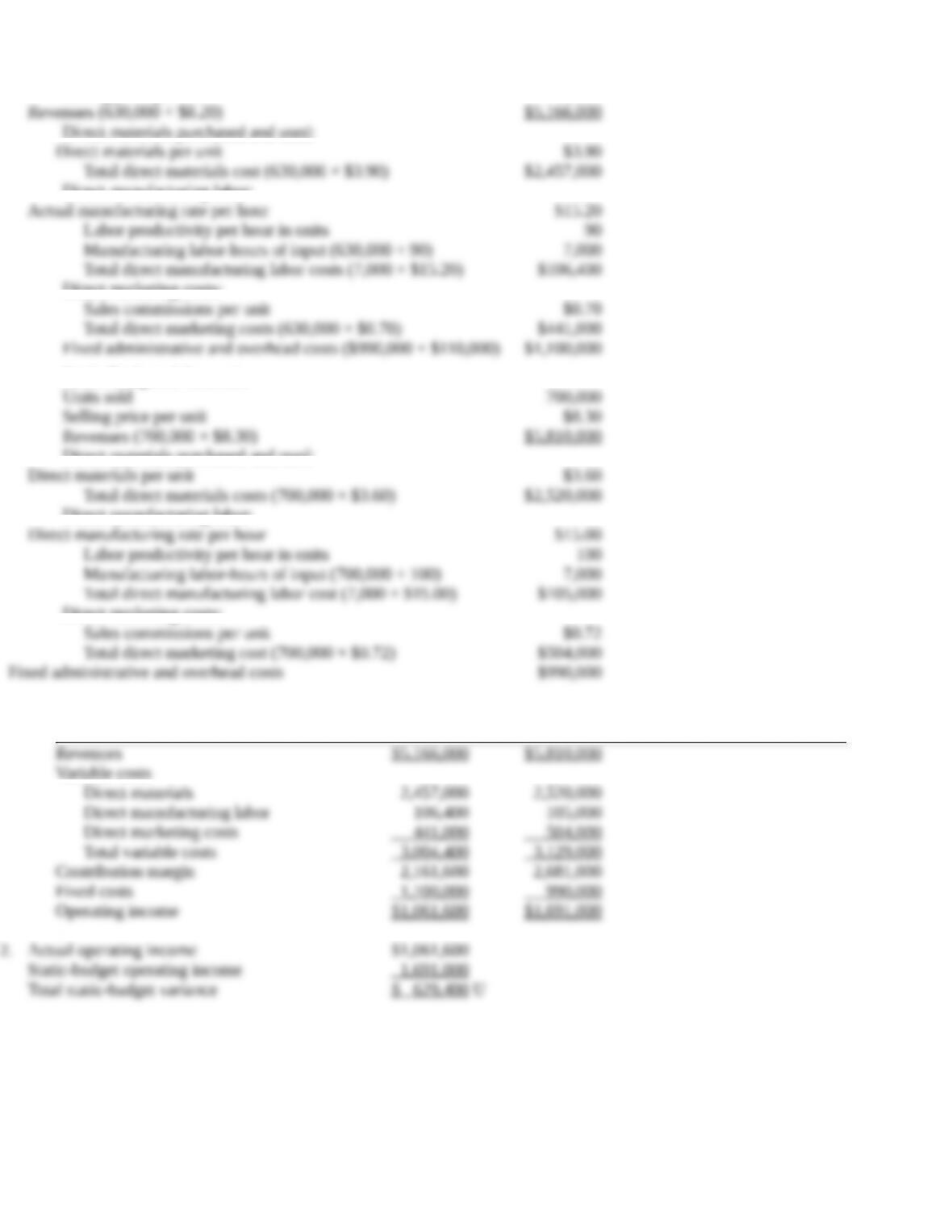

Actual Results

Units sold (90% × 700,000) 630,000

Selling price per unit $8.20

Direct materials purchased and used:

Direct manufacturing labor:

Direct marketing costs:

Static Budgeted Amounts

Direct materials purchased and used:

Direct manufacturing labor:

Direct marketing costs:

1. Actual Static-Budget

Results Amounts

Variable costs

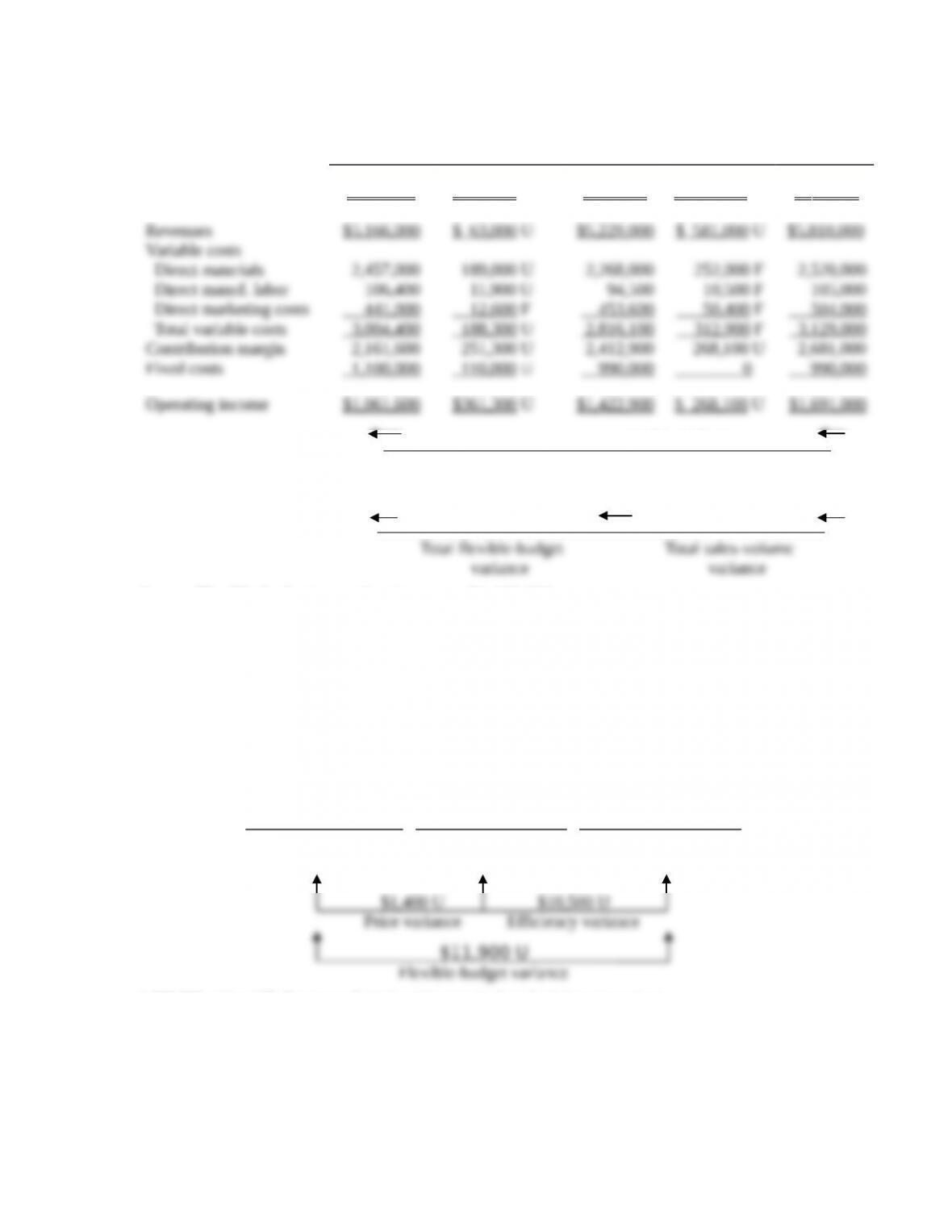

Flexible-budget-based variance analysis for Ellis Animal Health, Inc. for April 2017:

Actual

Results

Flexible-Budget

Variances

Flexible

Budget

Sales-Volume

Variances

Static

Budget

Units (vials) sold 630,000 0 630,000 70,000 7 00,000

3. Flexible-budget operating income = $1,422,900.

4. Flexible-budget variance for operating income = $361,300 U.

5. Sales-volume variance for operating income = $268,100 U.

6.

Analysis of direct mfg. labor flexible-budget variance for Ellis Animal Health, Inc. for April 2017:

Actual Costs

Incurred

(Actual Input Qty.

× Actual Price)

Actual Input Qty.

× Budgeted Price

Flexible Budget

(Budgeted Input

Qty. Allowed for

Actual Output

× Budgeted Price)

Direct.

Mfg. Labor

(7,000 × $15.20)

$106,400

(7,000 × $15.00)

$105,000

(*6,300 × $15.00)

$94,500

* 630,000 units ÷ 100 direct manufacturing labor standard productivity rate per hour.

DML price variance = $1,400 U; DML efficiency variance = $10,500 U

7. DML flexible-budget variance = $11,900 U

7-37 Possible causes for price and efficiency variances. You have been

invited to interview for an internship with an international food manufacturing

company. When you arrive for the interview, you are given the following

information related to a ‘ctitious Belgian chocolatier for the month of June. The

chocolatier manufactures tru*es in 12-piece boxes. The production is labor

intensive, and the delicate nature of the chocolate requires a high degree of

skill.

Actual

Boxes produced 10,000

Direct materials used in production 2,150,000 g

Actual direct material cost 60,200 euro

Actual direct manufacturing labor-hours 1,100

Actual direct manufacturing labor cost 12,650 euro

Standards

Purchase price of direct materials 0.03 euro/g

Materials per box 200 g

Wage rate 12 euro/hour

Boxes per hour 10

Please respond to the following questions as if you were in an interview situation:

Required:

1. Calculate the materials efficiency and price variance and the wage and labor efficiency vari–

ances for the month of June.

2. Discuss some possible causes of the variances you have calculated. Can you make any possible

connection between the material and labor variances? What recommendations do you have for

future improvement?

SOLUTION

(20 min.) Possible causes for price and efficiency variances

1.

Actual Costs

Incurred

(Actual Input Qty.

× Actual Price)

(1)

Actual Input Qty.

× Budgeted Price

(2)

Flexible Budget

(Budgeted Input

Qty. Allowed for

Actual Output

× Budgeted Price)

(3)

Direct

(2,150,000 × € 0.03)

(10,000 × 200 × € .03)

Direct

(1,100 × € 12)

(10,000 × (1/10) × € 12)

2. The favorable materials price variance, paired with the unfavorable materials efficiency

variance could be an indication that the company purchased less expensive ingredients,

The favorable labor price variance suggests that less experienced workers may have

The company should look at the number of rejected units, and if they are indeed

7-38 Material-cost variances, use of variances for performance evaluation. Katharine John-

son is the owner of Best Bikes, a company that produces high-quality cross-country bicycles. Best

Bikes participates in a supply chain that consists of suppliers, manufacturers, distributors, and elite

bicycle shops. For several years Best Bikes has purchased titanium from suppliers in the supply

chain. Best Bikes uses titanium for the bicycle frames because it is stronger and lighter than other

metals and therefore increases the quality of the bicycle. Earlier this year, Best Bikes hired Michael

Bentfield, a recent graduate from State University, as purchasing manager. Michael believed that he

could reduce costs if he purchased titanium from an online marketplace at a lower price.

Best Bikes established the following standards based upon the company’s experience with

previous suppliers. The standards are as follows:

Cost of titanium $18 per pound

Titanium used per bicycle 8 lbs.

Actual results for the first month using the online supplier of titanium are as follows:

Bicycles produced 400

Titanium purchased 5,200 lb. for $88,400

Titanium used in production 4,700 lb.

Required:

1. Compute the direct materials price and efficiency variances.

2. What factors can explain the variances identified in requirement 1? Could any other variances

be affected?

3. Was switching suppliers a good idea for Best Bikes? Explain why or why not.

4. the production manager’s evaluation be based solely on efficiency variances? Why is it im-

portant for Katharine Johnson to understand the causes of a variance before she evaluates

performance?

5. Other than performance evaluation, what reasons are there for calculating variances?

6. What future problems could result from Best Bikes’ decision to buy a lower quality of titani-

um from the online marketplace?

SOLUTION

(35 min.) Material cost variances, use of variances for performance evaluation

1. Materials Variances

Actual Costs

Incurred

(Actual Input Qty.

× Actual Price)

Actual Input Qty.

× Budgeted Price

Flexible Budget

(Budgeted Input Qty. Allowed

for Actual Output

× Budgeted Price)

Purchases Usage

2. The favorable price variance is due to the $1 difference ($18 – $17) between the standard

price based on the previous suppliers and the actual price paid through the on-line

3. Switching suppliers was not a good idea. The $5,200 savings in the cost of titanium was

outweighed by the $27,000 extra material usage. In addition, the $27,000 U efficiency

4. The purchasing manager’s performance evaluation should not be based solely on the

price variance. The short-run reduction in purchase costs was more than offset by higher

usage rates. His evaluation should be based on the total costs of the company as a whole.

5. Variances should be used to help Best Bikes understand what led to the current set of

6. Future problems can arise in the supply chain. Bentfield may need to go back to the

previous suppliers. But Best Bikes’ relationship with them may have been damaged and

7-39 Direct manufacturing labor and direct materials variances,

missing data. (CMA, heavily adapted) Oyster Bay Surfboards manufactures fiberglass

surfboards. The standard cost of direct materials and direct manufacturing labor is $248 per

board. This includes 35 pounds of direct materials, at the budgeted price of $3 per pound, and 11

hours of direct manufacturing labor, at the budgeted rate of $13 per hour. Following are addition–

al data for the month of July:

Units completed 5,600 units

Direct material purchases 230,000 pounds

Cost of direct material purchases $759,000

Actual direct manufacturing labor-hours 43,000 hours

Actual direct manufacturing labor cost $623,500

Direct materials efficiency variance $ 1,200 F

There were no beginning inventories.

Required:

1. Compute direct manufacturing labor variances for July.

2. Compute the actual pounds of direct materials used in production in July.

3. Calculate the actual price per pound of direct materials purchased.

4. Calculate the direct materials price variance.

SOLUTION

(30 min.) Direct manufacturing labor and direct materials variances, missing data.

1.

Flexible Budget

(Budgeted Input

Actual Costs Qty. Allowed for

Incurred (Actual Actual Input Qty. Actual Output

Input Qty.× Actual Price) × Budgeted Price × Budgeted Price)

Direct mfg. labor $623,500a $559,000b$800,800c

2. The favorable direct materials efficiency variance of $241,800 indicates that fewer

pounds of direct materials were actually used than the budgeted quantity allowed for actual

output.

=

$1,200 efficiency variance

$3 per pound budgeted price

3. Actual price paid per pound = $759,000/230,000

4. Actual Costs Incurred Actual Input ×

(Actual Input × Actual Price) Budgeted Price

$759,000a$690,000b

a Given

7-40 Direct materials efficiency, mix, and yield variances. Sandy’s Snacks produces snack

mixes for the gourmet and natural foods market. Its most popular product is Tempting Trail Mix, a

mixture of peanuts, dried cranberries, and chocolate pieces. For each batch, the budgeted quantities

and budgeted prices are as follows:

Quantity per Batch Price per Cup

Peanuts 60 cups $1

Dried cranberries 30 cups $2

Chocolate pieces 10 cups $3

Small changes to the standard mix of direct materials reflected in the above quantities do not signifi–

cantly affect the overall end product. In addition, not all ingredients added to production end up in

the finished product, as some are rejected during inspection.

In the current period, Sandy’s Snacks made 100 batches of Tempting Trail Mix with the follow-

ing actual quantity, cost, and mix of inputs:

Actual Quantity Actual Cost Actual Mix

Peanuts 6,720 cups $ 5,712 64%

Dried cranberries 2,625 cups 5,775 25%

Chocolate pieces 1,155 cups 3,350 11%

Total actual 10,500 cups $14,837 100%

Required:

1. What is the budgeted cost of direct materials for the 100 batches?

2. Calculate the total direct materials efficiency variance.

3. Calculate the total direct materials mix and yield variances.

4. How do the variances calculated in requirement 3 relate to those calculated in requirement 2?

What do the variances calculated in requirement 3 tell you about the 100 batches produced

this period? Are the variances large enough to investigate?

SOLUTION

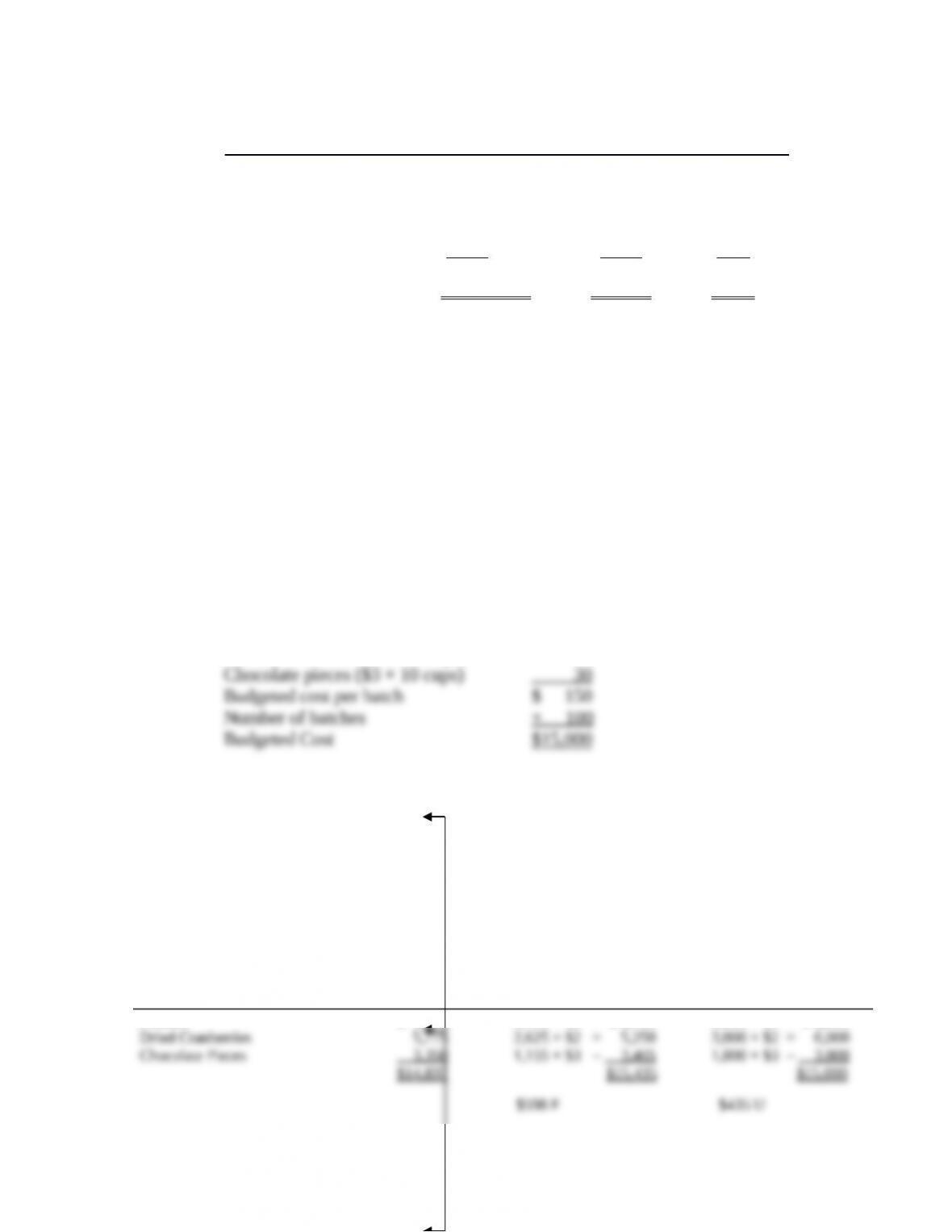

(35 min.) Direct materials efficiency, mix, and yield variances

1. Peanuts ($1 × 60 cups) $ 60

Dried cranberries ($2 × 30 cups) 60

2. Solution Exhibit 7-40A presents the total price variance ($598 F), the total efficiency

variance ($435 U), and the total flexible-budget variance ($163 F).

SOLUTION EXHIBIT 7-40A

Columnar Presentation of Direct Materials Price and Efficiency Variances for Sandy’s Snacks

Company.

Actual Costs

Incurred

(Actual Input Quantity

× Actual Price)

(1)

Actual Input Quantity

× Budgeted Price

(2)

Flexible Budget

(Budgeted Input Quantity

Allowed for Actual Output

× Budgeted Price)

(3)

Peanuts

$ 5,712

6,720 × $1 = $ 6,720

6,000 × $1 = $ 6,000

Total price variance

3. Solution Exhibit 7-40B presents the total direct materials yield ($750 U) and mix ($315

F) variances.

SOLUTION EXHIBIT 7-40B

Columnar Presentation of Direct Materials Yield and Mix Variances for Sandy’s Snacks Compa-

ny.

Actual Total Quantity

of All Inputs Used

× Actual Input Mix

× Budgeted Price

(1)

Actual Total Quantity

of All Inputs Used

× Budgeted Input Mix

× Budgeted Price

(2)

Flexible Budget:

Budgeted Total Quantity of

All Inputs Allowed for

Actual Output ×

Budgeted Input Mix

× Budgeted Price

(3)

4. The total mix variance combines with the total yield variance to equal the total efficiency vari-

ance calculated in part 2. The direct materials mix variance of $315 F indicates that the actual product

mix uses relatively more of less-expensive ingredients than planned. In this case, the actual mix con-

tains more peanuts while using fewer dried cranberries, and only slightly more chocolate pieces.

7-41 Direct materials and manufacturing labor variances, solving unknowns. (CPA, adapt-

ed) On May 1, 2017, Bovar Company began the manufacture of a new paging machine known as

Dandy. The company installed a standard costing system to account for manufacturing costs. The

standard costs for a unit of Dandy follow:

Direct materials (3 lb. at $4 per lb.) $12.00

Direct manufacturing labor (1/2 hour at $20 per hour) 10.00

Manufacturing overhead (75% of direct manufacturing la- 7.50

bor costs)

$29.50

The following data were obtained from Bovar’s records for the month of May:

Debit Credit

Revenues $125,000

Accounts payable control (for May’s purchases of direct materials) 55,000

Direct materials price variance $3,500

Direct materials efficiency variance 2,400

Direct manufacturing labor price variance 1,890

Direct manufacturing labor efficiency variance 2,200

Actual production in May was 4,000 units of Dandy, and actual sales in May were 2,500 units.

The amount shown for direct materials price variance applies to materials purchased during May.

There was no beginning inventory of materials on May 1, 2017.

Compute each of the following items for Bovar for the month of May. Show your computa-

tions.

Required:

1. Standard direct manufacturing labor-hours allowed for actual output produced

2. Actual direct manufacturing labor-hours worked

3. Actual direct manufacturing labor wage rate

4. Standard quantity of direct materials allowed (in pounds)

5. Actual quantity of direct materials used (in pounds)

6. Actual quantity of direct materials purchased (in pounds)

7. Actual direct materials price per pound