SOLUTION

(30 min.) Fixed manufacturing overhead variance analysis (continuation of 8-23).

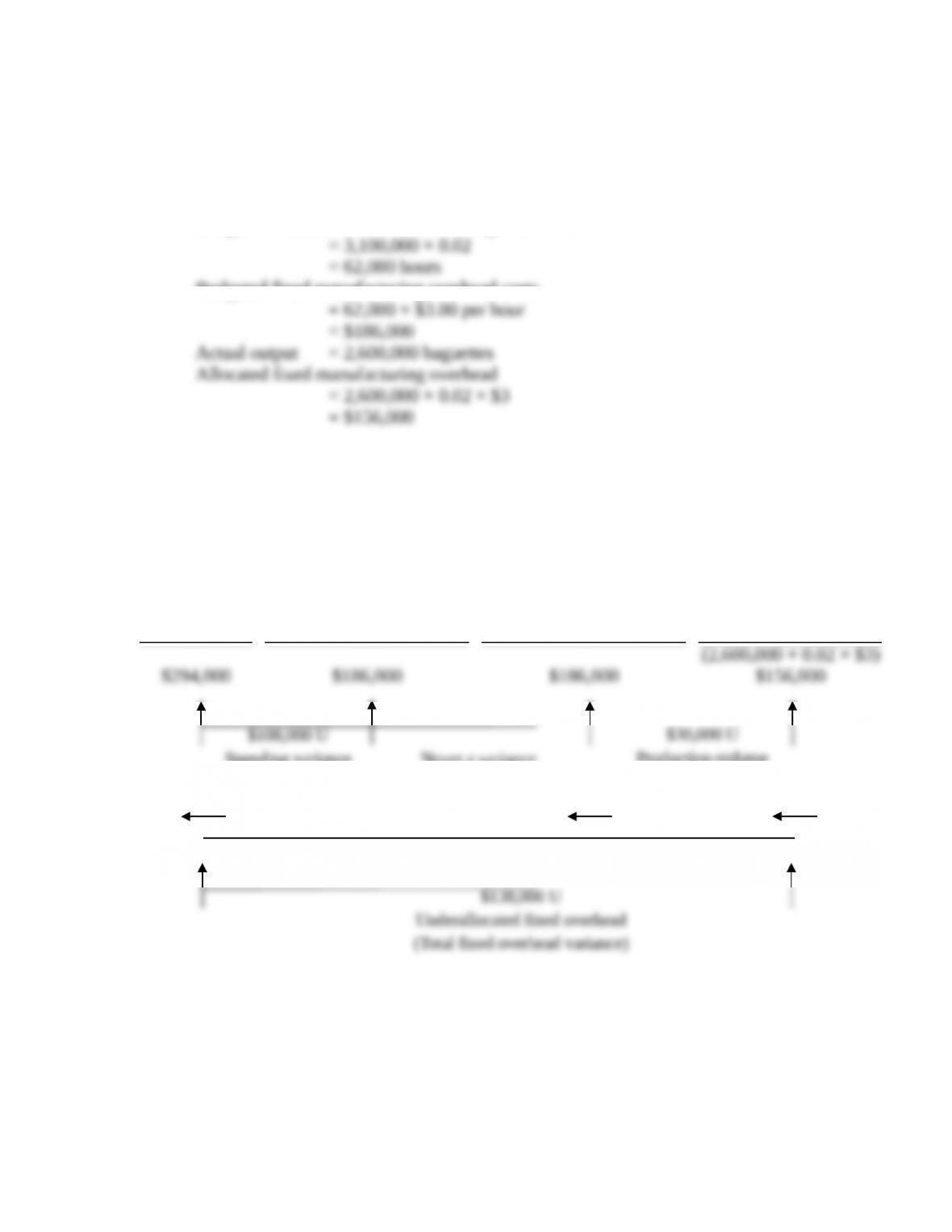

1. Budgeted standard direct manufacturing labor used = 0.02 per baguette

Budgeted output = 3,100,000 baguettes

Budgeted standard direct manufacturing labor-hours

Budgeted fixed manufacturing overhead costs

Fixed Manufacturing Overhead Variance Analysis for Sourdough Bread Company for 2017

Actual Costs

Incurred

(1)

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(2)

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

(2,600,000 × 0.02 × $3)

2. The fixed manufacturing overhead is underallocated by $138,000.

3. The production-volume variance of $30,000 U captures the difference between the budgeted

3,100,0000 baguettes and the lower actual 2,600,000 baguettes produced—the fixed cost

capacity not used. The spending variance of $108,000 unfavorable means that the actual

aggregate spending on fixed costs ($294,000) exceeds the budgeted amount ($186,000).

8-5

Spending variance Never a variance

Production-volume

variance

$108,000 U

Flexible-budget variance

$30,000 U

Production-volume

variance

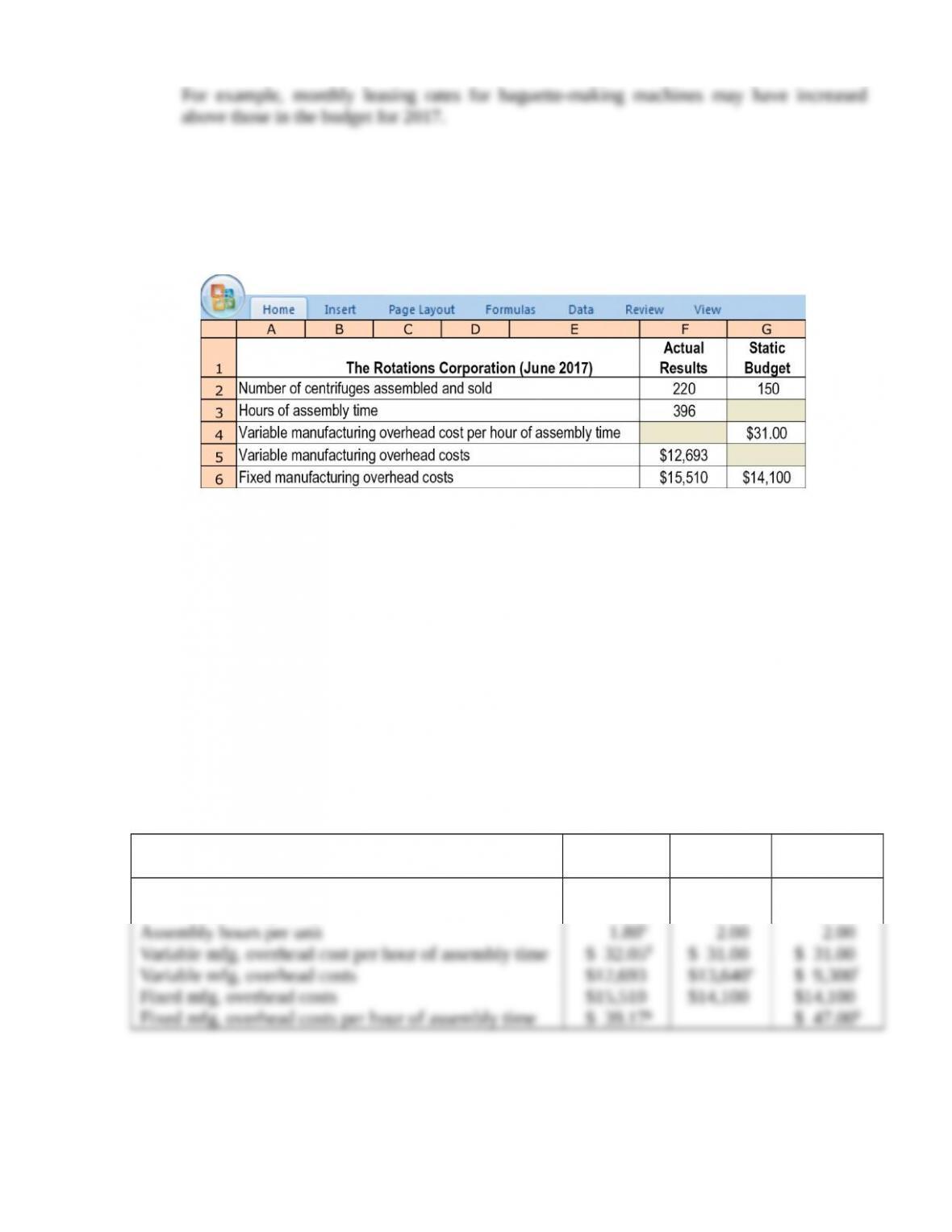

8-25 Manufacturing overhead, variance analysis. The Rotations Corporation is a

manufacturer of centrifuges. Fixed and variable manufacturing overheads are allocated to each

centrifuge using budgeted assembly-hours. Budgeted assembly time is 2 hours per unit. The

following table shows the budgeted amounts and actual results related to overhead for June 2017.

Required:

1. Prepare an analysis of all variable manufacturing overhead and fixed manufacturing

overhead variances using the columnar approach in Exhibit 8-4 (page 304).

2. Prepare journal entries for Rotations’ June 2017 variable and fixed manufacturing overhead

costs and variances; write off these variances to Cost of Goods Sold for the quarter ending

June 30, 2017.

3. How does the planning and control of variable manufacturing overhead costs differ from the

planning and control of fixed manufacturing overhead costs?

SOLUTION

(30–40 min.) Manufacturing overhead, variance analysis.

1. The summary information is:

The Rotations Corporation (June 2017) Actual

Flexible

Budget

Static

Budget

Outputs units (number of assembled units) 220 220 150

Hours of assembly time 396 440c 300a

a 150 units

´

2 assembly hours per unit = 300 hours

8-5

b 396 hours

¸

220 units = 1.80 assembly hours per unit

c 220 units

´

2 assembly hours per unit = 440 hours

´

¸

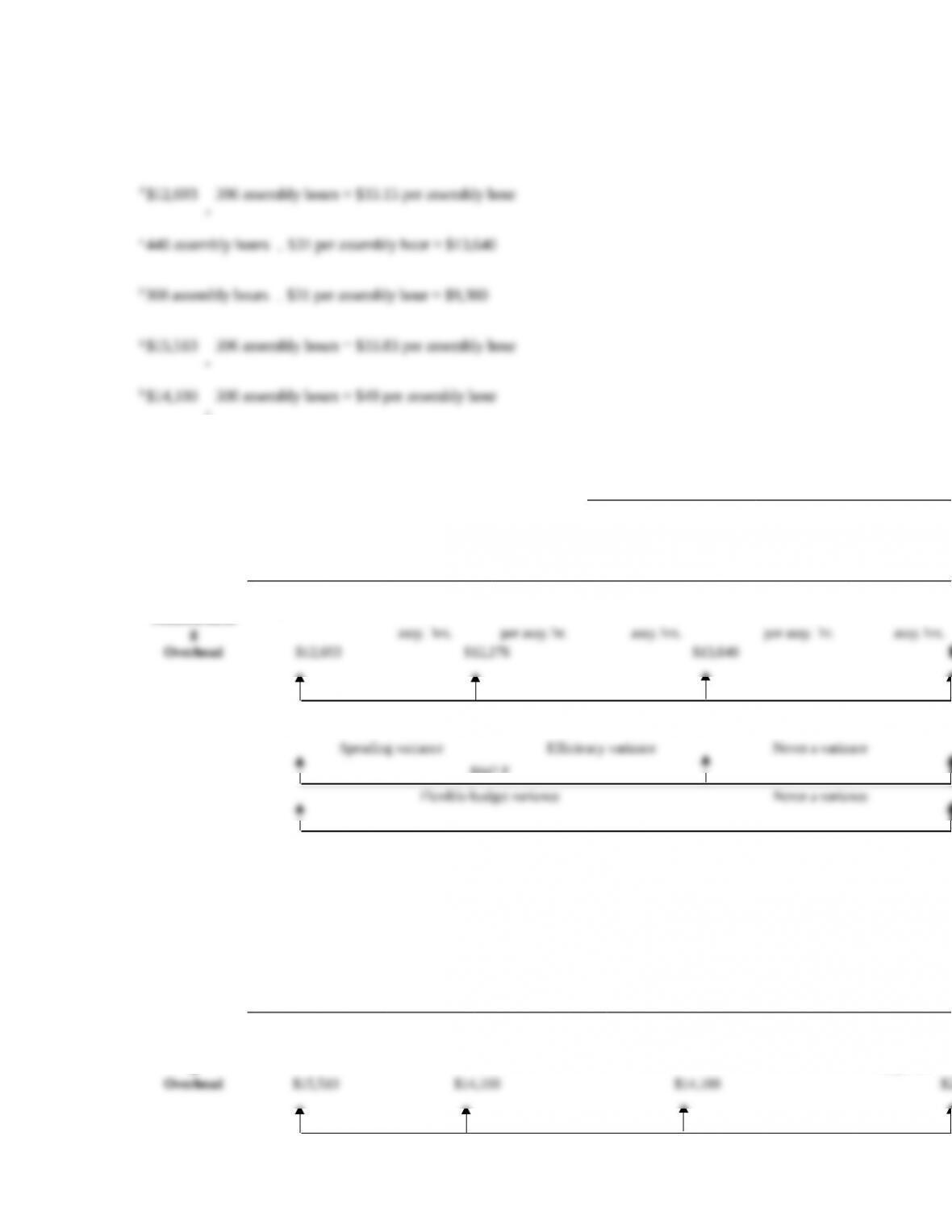

Flexible Budget: Allocated:

Actual Costs

Actual Input Qty.

´

Budgeted Input

Qty. Allowed Budgeted

Budgeted Input

Qty. Allowed

Incurred Budgeted Rate

for Actual Output

´

Rate for Actual Output

Variable 396

´

$31.00 440

´

$31.00 440

Manufacturin

$417 U $1,364 F

$947 F

$947 F

Overallocated variable overhead

Flexible Budget: Allocated:

Actual Costs Static Budget Lump Sum Static Budget Lump Sum

Budgeted Input

Allowed

Incurred Regardless of Output Level Regardless of Output Level

for Actual Output

Fixed 440

Manufacturin

gassy. hrs.

8-5

$5,170 F

Overallocated fixed overhead

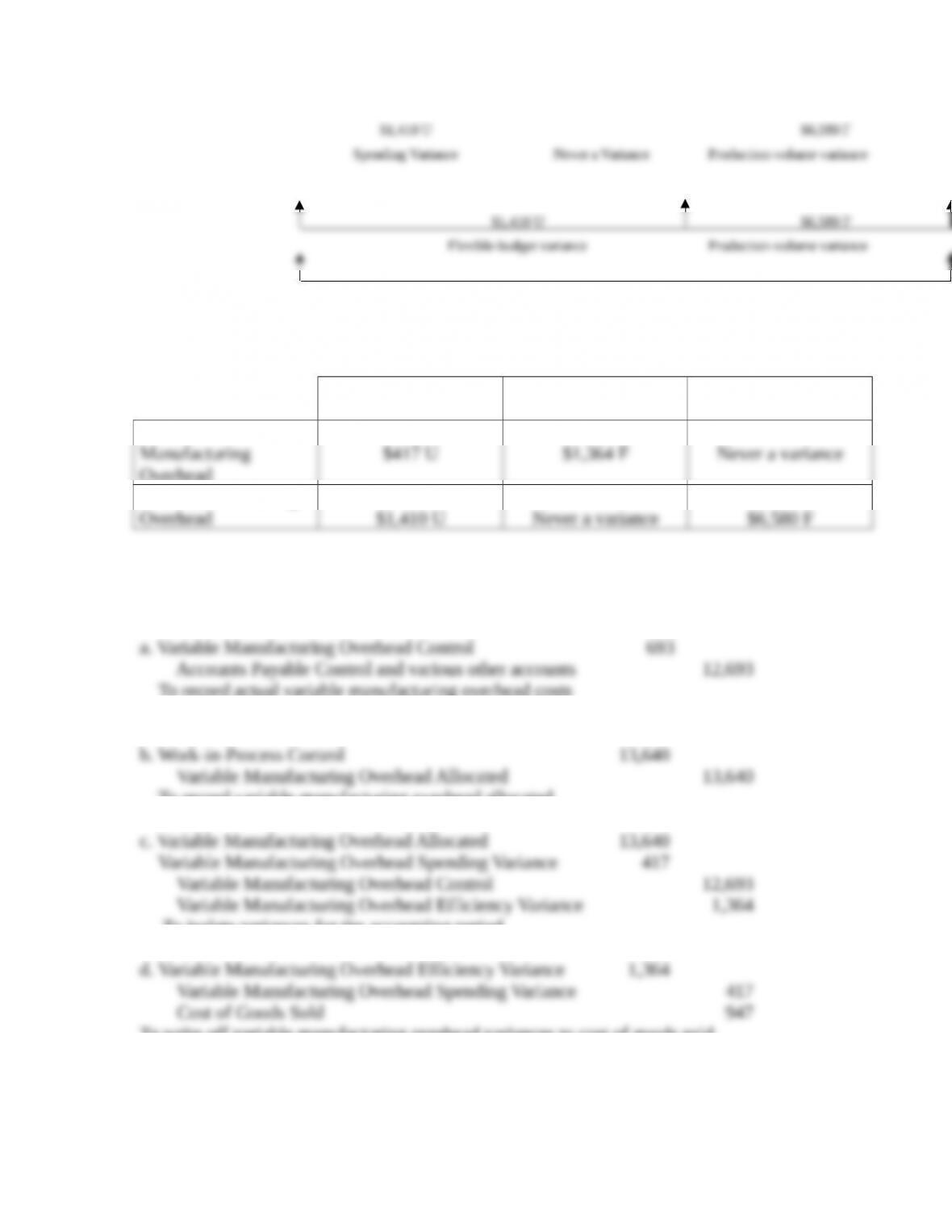

The summary analysis is:

Spending

Variance

Efficiency

Variance

Production-Volume

Variance

Variable

Overhead

Fixed Manufacturing

2. Variable Manufacturing Costs and Variances

12,

To record actual variable manufacturing overhead costs

incurred.

To record variable manufacturing overhead allocated.

To isolate variances for the accounting period.

To write off variable manufacturing overhead variances to cost of goods sold.

Fixed Manufacturing Costs and Variances

8-5

To record actual fixed manufacturing overhead costs incurred.

To record fixed manufacturing overhead allocated.

c. Fixed Manufacturing Overhead Allocated 20,680

To isolate variances for the accounting period.

d. Fixed Manufacturing Overhead Production-Volume Variance 6,580

To write off fixed manufacturing overhead variances to cost of goods sold.

3. Planning and control of variable manufacturing overhead costs has both a long-run and a

short-run focus. It involves Rotations planning to undertake only value-added overhead activities

(a long-run view) and then managing the cost drivers of those activities in the most efficient way

(a short-run view). Planning and control of fixed manufacturing overhead costs at Rotations have

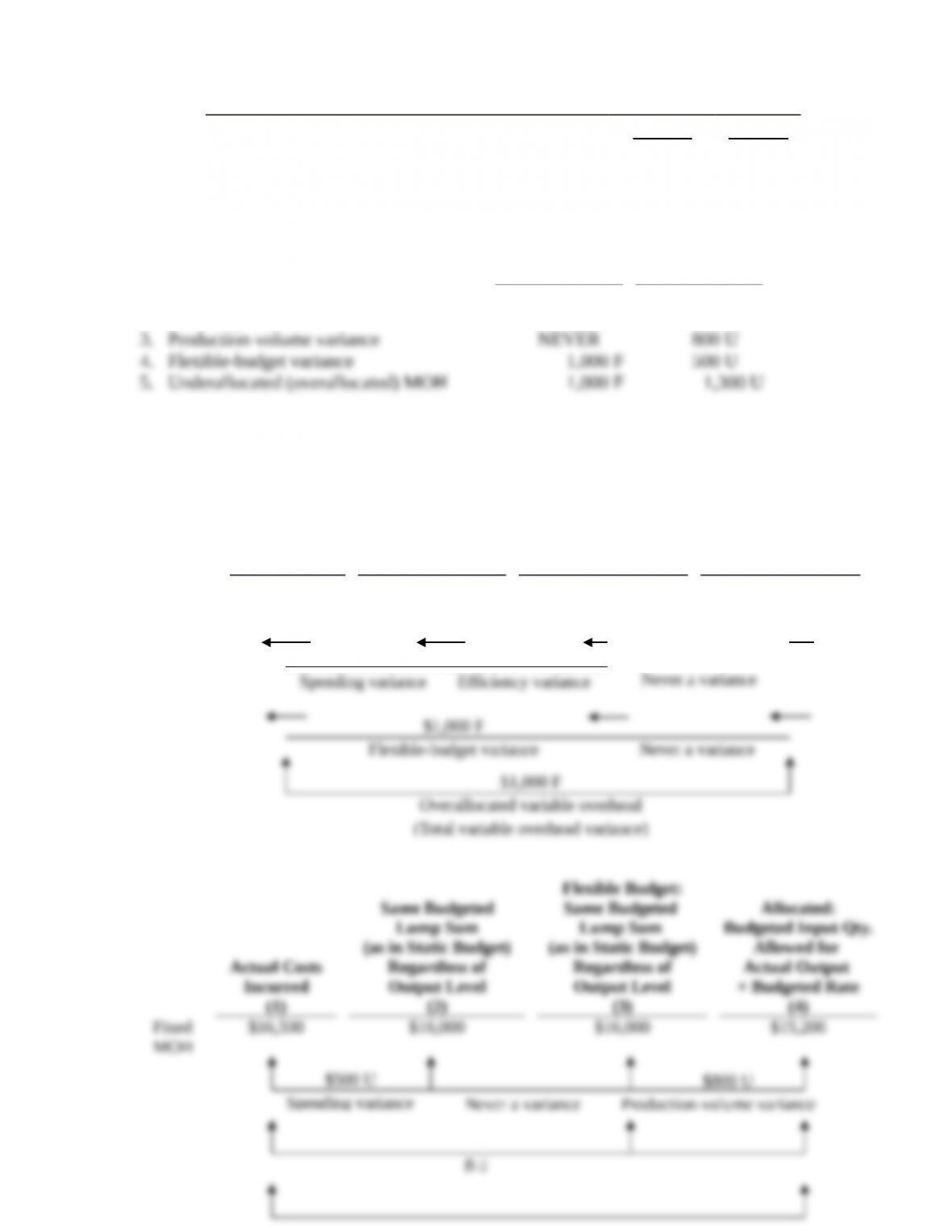

8-26 4-variance analysis, fill in the blanks. ProChem, Inc., produces chemicals for large

biotech companies. It has the following data for manufacturing overhead costs during August

2017:

Variable Fixed

Actual costs incurred $35,000 $16,500

Costs allocated to products 36,000 15,200

Flexible budget –––––– 16,000

Actual input × budgeted rate 31,500 ––––––

Fill in the blanks. Use F for favorable and U for unfavorable:

Variable Fixed

(1) Spending variance $ $

(2) Efficiency variance

(3) Production-volume variance

(4) Flexible-budget variance

8-5

Variable Fixed

(5) Underallocated (overallocated) manufacturing

overhead

SOLUTION

(1015 min.) 4-variance analysis, fill in the blanks.

Variable Fixed

1. Spending variance

2. Efficiency variance

$3,500 U

4,500 F

$ 500 U

NEVER

These relationships could be presented in the same way as in Exhibit 8-4.

Actual Costs

Incurred

(1)

Actual Input Qty.

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

Variable

MOH

$35,000 $31,500 $36,000 $36,000

$3,500 U

$4,500 F

An overview of the 4 overhead variances is:

4-Variance

Analysis

Spending

Variance

Efficiency

Variance

Production-Volume

Variance

Variable

8-27 Straightforward 4-variance overhead analysis. The Lopez Company uses standard

costing in its manufacturing plant for auto parts. The standard cost of a particular auto part, based

on a denominator level of 4,000 output units per year, included 6 machine-hours of variable

manufacturing overhead at $8 per hour and 6 machine-hours of fixed manufacturing overhead at

$15 per hour. Actual output produced was 4,400 units. Variable manufacturing overhead incurred

was $245,000. Fixed manufacturing overhead incurred was $373,000. Actual machine-hours

were 28,400.

Required:

1. Prepare an analysis of all variable manufacturing overhead and fixed manufacturing

overhead variances, using the 4-variance analysis in Exhibit 8-4 (page 304).

2. Prepare journal entries using the 4-variance analysis.

3. Describe how individual fixed manufacturing overhead items are controlled from day to day.

4. Discuss possible causes of the fixed manufacturing overhead variances.

SOLUTION

(20–30 min.) Straightforward 4-variance overhead analysis.

1. The budget for fixed manufacturing overhead is 4,000 units × 6 machine-hours × $15

machine-hours/unit = $360,000.

An overview of the 4-variance analysis is:

4-Variance

Analysis

Spending

Variance

Efficiency

Variance

Production-

Volume Variance

Variable

Manufacturing

Overhead

$17,800 U $16,000 U Never a Variance

8-5

$500 U

Flexible-budget variance

$800 U

Production-volume variance

$1,300 U

Underallocated fixed overhead

(Total fixed overhead variance)

Fixed

Overhead

Solution Exhibit 8-27 has details of these variances.

A detailed comparison of actual and flexible budgeted amounts is:

Actual Flexible Budget

Output units (auto parts) 4,400 4,400

Allocation base (machine-hours) 28,400 26,400a

a 4,400 units × 6.00 machine-hours/unit = 26,400 machine-hours

b 28,400 ÷ 4,400 = 6.45 machine-hours per unit

c 4,400 units × 6.00 machine-hours per unit × $8.00 per machine-hour = $211,200

d $245,000 ÷ 28,400 = $8.63

e 4,000 units × 6.00 machine-hours per unit × $15 per machine-hour = $360,000

f $373,000 ÷ 28,400 = $13.13

2. Variable Manufacturing Overhead Control 245,000

Accounts Payable Control and other accounts 245,000

Fixed Manufacturing Overhead Allocated 396,000

Fixed Manufacturing Overhead Spending Variance 13,000

8-5

3. Individual fixed manufacturing overhead items are not usually affected very much by

day-to-day control. Instead, they are controlled periodically through planning decisions and

4. The fixed overhead spending variance is caused by the actual realization of fixed costs

differing from the budgeted amounts. Some fixed costs are known because they are

contractually specified, such as rent or insurance, although if the rental or insurance contract

expires during the year, the fixed amount can change. Other fixed costs are estimated, such as

the cost of managerial salaries which may depend on bonuses and other payments not known at

the beginning of the period. In this example, the spending variance is unfavorable, so actual

FOH is greater than the budgeted amount of FOH.

SOLUTION EXHIBIT 8-27

Actual Costs

Incurred

(1)

Actual Input

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input

Allowed for

Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input

Allowed for

Actual Output

× Budgeted Rate

(4)

Variable

MOH $245,000

(28,400 × $8)

$227,200

(4,400 × 6 × $8)

$211,200

(4,400 × 6 × $8)

$211,200

Actual Costs

Incurred

(1)

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(2)

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(3)

Allocated:

Budgeted Input

Allowed for

Actual Output

× Budgeted Rate

(4)

8-5

$17,800 U

Spending variance

$16,000 U

Efficiency variance Never a variance

$33,800 U

Flexible-budget variance

Never a variance

$33,800 U

Underallocated variable overhead

(Total variable overhead variance)

Fixed

(4,000 × 6 × $15)

(4,000 × 6 × $15)

(4,400 × 6 × $15)

8-28 Straightforward coverage of manufacturing overhead, standard-costing system. The

Brazil division of an American telecommunications company uses standard costing for its

machine-paced production of telephone equipment. Data regarding production during June are as

follows:

Variable manufacturing overhead costs incurred $537,470

Variable manufacturing overhead cost rate $7 per standard machine-hour

Fixed manufacturing overhead costs incurred $146,101

Fixed manufacturing overhead costs budgeted $136,000

Denominator level in machine-hours 68,000

Standard machine-hour allowed per unit of output 1.2

Units of output 66,500

Actual machine-hours used 75,700

Ending work-in-process inventory 0

Required:

1. Prepare an analysis of all manufacturing overhead variances. Use the 4-variance analysis

framework illustrated in Exhibit 8-4 (page 304).

2. Prepare journal entries for manufacturing overhead costs and their variances.

3. Describe how individual variable manufacturing overhead items are controlled from day to

day.

4. Discuss possible causes of the variable manufacturing overhead variances.

8-5

Spending variance

Never a variance

variance

Flexible-budget variance

Production-volume

variance