2. The cost per equivalent unit of beginning inventory and of work done in the current

period differ substantially:

Beginning

Inventory

Work Done in

Current Period

Direct

Materials

Conversion

Costs

* from Solution Exhibit 18-29, Panel B

**from Solution Exhibit 18-30, Panel B

The cost per equivalent unit differs between the two methods because each method uses different

costs as the numerator of the calculation. FIFO uses only the costs added during the current

period whereas weighted-average uses the costs from the beginning work-in-process as well as

costs added during the current period. Both methods also use different equivalent units in the

denominator.

The following table summarizes the costs assigned to units completed and those still in

process under the weighted-average and FIFO process-costing methods for our example.

FIFO

(Solution

Exhibit 18-30B)

Wtd.-Avg.

(Solution

Exhibit 18-29B) Difference

Total costs accounted for

$1 ,008,882

$1 ,008,882

The FIFO ending inventory is higher than the weighted-average ending inventory by $10,486.

This is because FIFO assumes that all the lower-cost prior-period units in work in process are the

LogicCo’s managers should consider the weighted-average method because it leads to a

higher cost of goods completed and transferred (and sold), thereby lowering taxes. The managers

may have an incentive, however, to use the FIFO method and show a higher level of current

18-<

18-31 Standard-costing method, spoilage. Refer to the information in Exercise 18-29.

Suppose LogicCo determines standard costs of $215 per equivalent unit for direct materials and

$92 per equivalent unit for conversion costs for both beginning work in process and work done

in the current period.

Required:

1. Do Exercise 18-29 using the standard-costing method.

2. What issues should the manager focus on when reviewing the equivalent units calculation?

SOLUTION

(30 min.) Standard-costing method, spoilage.

1. Solution Exhibit 18-30, Panel A, shows the computation of the equivalent units of work

done in September 2017 for direct materials (2,754 units) and conversion costs (2,943 units).

(This computation is the same for FIFO and standard-costing.)

SOLUTION EXHIBIT 18-31

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign

Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process Inventory;

Standard Costing Method of Process Costing with Spoilage,

LogicCo for September 2017

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 5) Assignment of costs at standard costs:

Good units completed and transferred out

(2,500 units)

18-<

(A)+(B)+(C) Total costs accounted for

*Work in process, beginning has 900 equivalent units (900 physical units 100%) of direct materials and 270

equivalent units (900 physical units 30%) of conversion costs.

§Equivalent units of direct materials and conversion costs calculated in Step 2 in Solution Exhibit 18-30, Panel A.

2. To show better performance, a department supervisor might report a higher degree of

completion resulting in understated cost per equivalent unit and overstated operating income. If

performance for the period is very good, the department supervisor may be tempted to report a

To guard against the possibility of bias, managers should ask supervisors specific

18-32 Spoilage and job costing. (L. Bamber) Barrett Kitchens produces a variety of items in

accordance with special job orders from hospitals, plant cafeterias, and university dormitories.

An order for 2,100 cases of mixed vegetables costs $9 per case: direct materials, $4; direct

manufacturing labor, $3; and manufacturing overhead allocated, $2. The manufacturing overhead

rate includes a provision for normal spoilage. Consider each requirement independently.

Required:

1. Assume that a laborer dropped 420 cases. Suppose part of the 420 cases could be sold to a

nearby prison for $420 cash. Prepare a journal entry to record this event. Calculate and

explain briefly the unit cost of the remaining 1,680 cases.

2. Refer to the original data. Tasters at the company reject 420 of the 2,100 cases. The 420 cases

are disposed of for $840. Assume that this rejection rate is considered normal. Prepare a

journal entry to record this event, and do the following:

a. Calculate the unit cost if the rejection is attributable to exacting specifications of this

particular job.

b. Calculate the unit cost if the rejection is characteristic of the production process and is

not attributable to this specific job.

c. Are unit costs the same in requirements 2a and 2b? Explain your reasoning briefly.

3. Refer to the original data. Tasters rejected 420 cases that had insufficient salt. The product

18-<

can be placed in a vat, salt can be added, and the product can be reprocessed into jars. This

operation, which is considered normal, will cost $420. Prepare a journal entry to record this

event and do the following:

a. Calculate the unit cost of all the cases if this additional cost was incurred because of the

exacting specifications of this particular job.

b. Calculate the unit cost of all the cases if this additional cost occurs regularly because of

difficulty in seasoning.

c. Are unit costs the same in requirements 3a and 3b? Explain your reasoning briefly.

SOLUTION

(20–30 min.) Spoilage and job costing.

1. Cash 420

from abnormal spoilage.

2. a. Cash 840

Work-in-Process Control 840

b. Cash 840

The unit cost of a good case remains at $9.00.

c. The unit costs in 2a and 2b are different because in 2a the normal spoilage cost is

charged as a cost of the job which has exacting job specifications. In 2b however,

18-<

b. Manufacturing Department Overhead Control 420

c. The unit costs in 3a and 3b are different because in 3a the normal rework cost is

charged as a cost of the job which has exacting job specifications. In 3b however,

18-33 Reworked units, costs of rework. Heyer Appliances assembles dishwashers at its plant

in Tuscaloosa, Alabama. In February 2017, 60 circulation motors that cost $110 each (from a

new supplier who subsequently went bankrupt) were defective and had to be disposed of at zero

net disposal value. Heyer Appliances was able to rework all 60 dishwashers by substituting new

circulation motors purchased from one of its existing suppliers. Each replacement motor cost

$125.

Required:

1. What alternative approaches are there to account for the materials cost of reworked units?

2. Should Heyer Appliances use the $110 circulation motor or the $125 motor to calculate the

cost of materials reworked? Explain.

3. What other costs might Heyer Appliances include in its analysis of the total costs of rework

due to the circulation motors purchased from the (now) bankrupt supplier?

SOLUTION

(15 min.) Reworked units, costs of rework.

1. The two alternative approaches to account for the materials costs of reworked units are:

a. To charge the costs of rework to the current period as a separate expense item as

b. To charge the costs of the rework to manufacturing overhead as normal rework.

2. The $125 circulation motor cost is the cost of the actual motors included in the

3. The total costs of rework due to the defective circulation motors include the following:

a. the labor and other conversion costs spent on substituting the new circulation motors;

18-<

18-34 Scrap, job costing. The Russell Company has an extensive job-costing facility that uses

a variety of metals. Consider each requirement independently.

Required:

1. Job 372 uses a particular metal alloy that is not used for any other job. Assume that scrap is

material in amount and sold for $480 quickly after it is produced. Prepare the journal entry.

2. The scrap from Job 372 consists of a metal used by many other jobs. No record is maintained

of the scrap generated by individual jobs. Assume that scrap is accounted for at the time of its

sale. Scrap totaling $4,500 is sold. Prepare two alternative journal entries that could be used

to account for the sale of scrap.

3. Suppose the scrap generated in requirement 2 is returned to the storeroom for future use, and

a journal entry is made to record the scrap. A month later, the scrap is reused as direct

material on a subsequent job. Prepare the journal entries to record these transactions.

SOLUTION

(25 min.) Scrap, job costing.

1. Journal entry to record scrap generated by a specific job and accounted for at the time

scrap is sold is:

To recognize asset from sale of scrap.

A memo posting is also made to the specific job record.

2. Scrap common to various jobs and accounted for at the time of its sale can be accounted

for in two ways:

a. Regard scrap sales as a separate line item of revenues (the method generally used when

the dollar amount of scrap is immaterial):

To recognize revenue from sale of scrap.

b. Regard scrap sales as offsets against manufacturing overhead (the method generally used

when the dollar amount of scrap is material):

To record cash raised from sale of scrap.

3. Journal entry to record scrap common to various jobs at the time scrap is returned to

storeroom:

18-<

To record value of scrap returned to storeroom.

When the scrap is reused as direct material on a subsequent job, the journal entry is:

To record reuse of scrap on a job.

Explanations of journal entries are provided here but are not required.

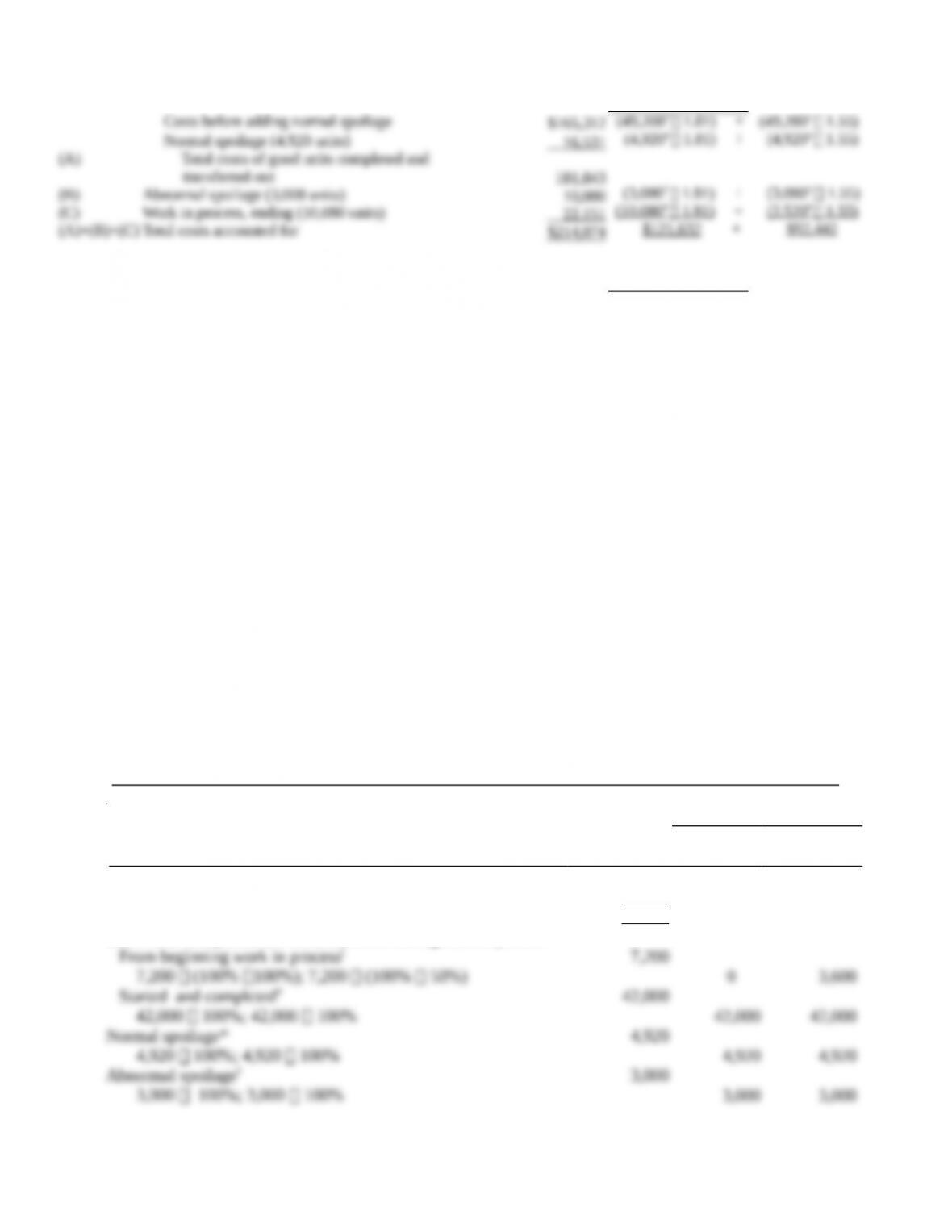

18-35 Weighted-average method, spoilage. World Class Steaks is a meat-processing

firm based in Texas. It operates under the weighted-average method of process costing and has

two departments: preparation (prep) and shipping. For the prep department, conversion costs are

added evenly during the process, and direct materials are added at the beginning of the process.

Spoiled units are detected upon inspection at the end of the prep process and are disposed of at

zero net disposal value. All completed work is transferred to the shipping department. Summary

data for May follow:

Required:

For the prep department, summarize the total costs to account for and assign those costs to units

completed and transferred out (including normal spoilage), to abnormal spoilage, and to units in

ending work in process. (Problem 18-37 explores additional facets of this problem.)

SOLUTION

(30 min.) Weighted-average method, spoilage.

Solution Exhibit 18-35 summarizes total costs to account for, calculates the equivalent units of

work done to date for each cost category, and assigns total costs to units completed (including

normal spoilage), to abnormal spoilage, and to units in ending work in process using the

weighted-average method.

18-<

SOLUTION EXHIBIT 18-35

Weighted-Average Method of Process Costing with Spoilage,

Prep Department for World Class Steaks for May

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

(Step 1) (Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

To account for

Good units completed and transferred out

Equivalent units of work done to date

7,200

60 ,000

67 ,2 00

*Normal spoilage is 10% of good units transferred out: 10% 49,200 = 4,920 units. Degree of completion of

normal spoilage in this department: direct materials, 100%; conversion costs, 100%.

†Total spoilage = 7,200 + 60,000 – 49,200 – 10,080 = 7,920 units; Abnormal spoilage = 7,920 – 4,920 = 3,000 units.

Degree of completion of abnormal spoilage in this department: direct materials, 100%; conversion costs, 100%.

‡Degree of completion in this department: direct materials, 100%; conversion costs, 25%.

PANEL B: Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit,

and Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process

Inventory

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

(Step 5) Assignment of costs

Good units completed and transferred out (49,200 units)

$ 13,410

200 ,664

$ 214 ,074

$ 10,632

111 ,000

$121 ,632

$ 2,778

89 ,664

$92 ,442

18-<

#Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A above.

18-36 FIFO method, spoilage. Refer to the information in Problem 18-35.

Required:

Do Problem 18-35 using the FIFO method of process costing. (Problem 18-38 explores

additional facets of this problem.)

SOLUTION

(25 min.) FIFO method, spoilage.

For the Prep Department, Solution Exhibit 18-36 summarizes the total costs for May, calculates

the equivalent units of work done in the current period for direct materials and conversion costs,

and assigns total costs to units completed and transferred out (including normal spoilage), to

abnormal spoilage, and to units in ending work in process under the FIFO method.

SOLUTION EXHIBIT 18-36

First-in, First-out (FIFO) Method of Process Costing with Spoilage,

Prep Department for World Class Steaks for May

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given) 7,200

Started during current period (given) 60 ,000

To account for 67 ,200

Good units completed and transferred out during current period:

18-<

|| Degree of completion in this department: direct materials, 100%; conversion costs, 50%.

#49,200 physical units completed and transferred out minus 7,200 physical units completed and transferred out from

beginning work-in-process inventory.

*Normal spoilage is 10% of good units transferred out: 10% 49,200 = 4,920 units. Degree of completion of

normal spoilage in this department: direct materials, 100%; conversion costs, 100%.

†Total spoilage = 7,200 + 60,000 – 49,200 – 10,080 = 7,920 units; Abnormal spoilage = 7,920 – 4,920 = 3,000 units.

Degree of completion of abnormal spoilage in this department: direct materials, 100%; conversion costs, 100%.

‡Degree of completion in this department: direct materials, 100%; conversion costs, 25%.

PANEL B: Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit,

and Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process

Inventory

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

$ 13,410

200 ,664

$ 214 ,074

$ 10,632

111 ,000

$121 ,632

$ 2,778

89 ,664

$92 ,442

§Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A.

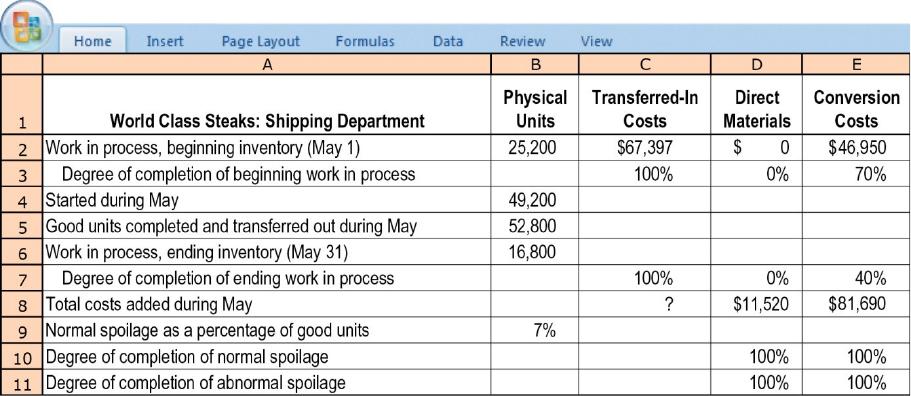

18-37 Weighted-average method, shipping department (continuation of 18-35). In the

shipping department of World Class Steaks, conversion costs are added evenly during the

process, and direct materials are added at the end of the process. Spoiled units are detected upon

inspection at the end of the process and are disposed of at zero net disposal value. All completed

work is transferred to the next department. The transferred-in costs for May equal the total cost

of good units completed and transferred out in May from the prep department, which were

calculated in Problem 18-35 using the weighted-average method of process costing. Summary

data for May follow.

18-<

Required:

For the shipping department, use the weighted-average method to summarize the total costs to

account for and assign those costs to units completed and transferred out (including normal

spoilage), to abnormal spoilage, and to units in ending work in process.

18-<