Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

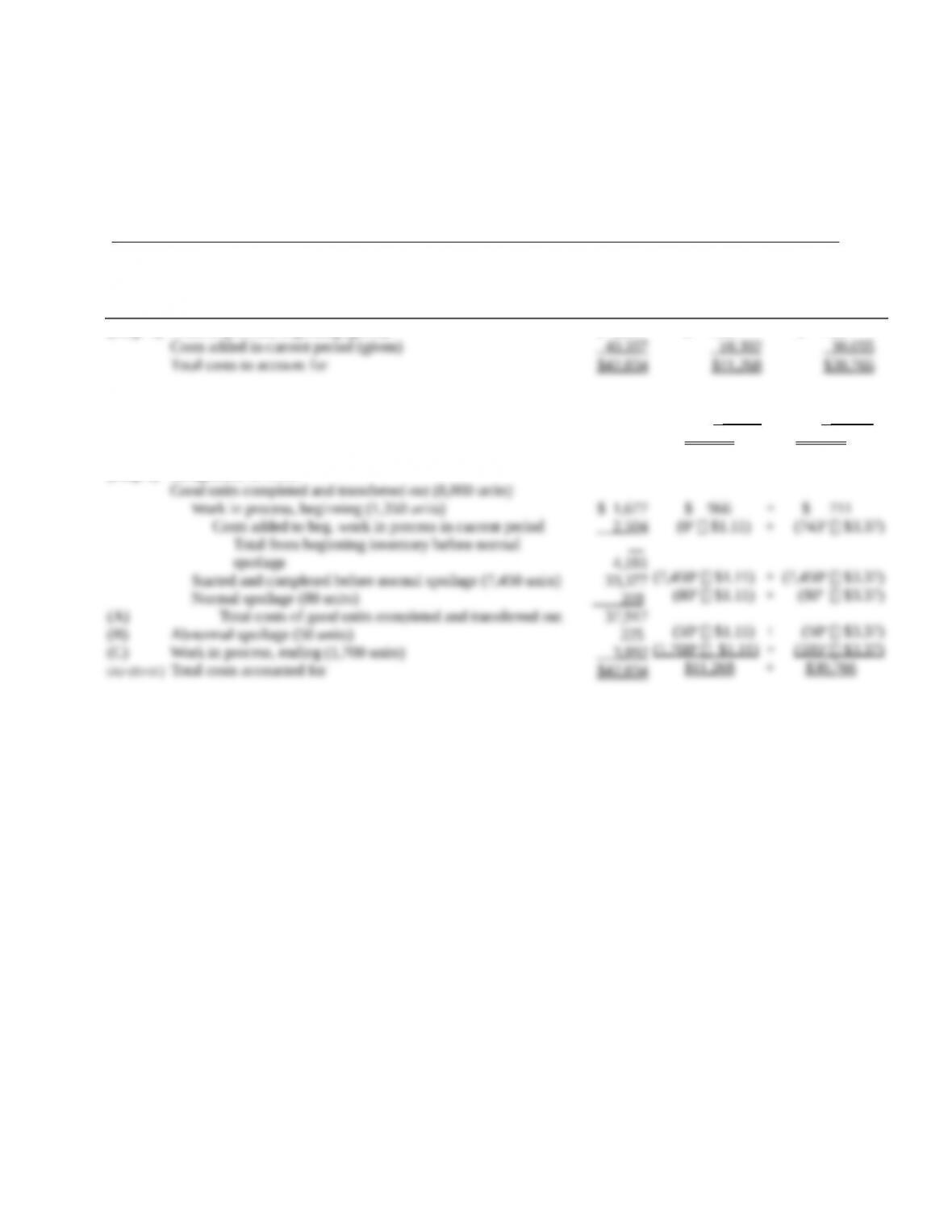

SOLUTION EXHIBIT 18-24

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign

Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process Inventory;

FIFO Method of Process Costing,

MacLean Manufacturing Company, November 2017.

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

(Step 4) Costs added in current period

Divided by equivalent units of work done in current period

Cost per equivalent unit

(Step 5) Assignment of costs:

Good units completed and transferred out (8,800 units)

$ 1,677

40 ,357

$42 ,034

$ 966

10 ,302

$11 ,268

$10,302

9 ,280

$ 1.11

$ 711

30 ,055

$30 ,766

$30,055

8 ,918

$ 3.37

Work in process, beginning (1,350 units)

Costs added to beg. work in process in current period

Total from beginning inventory before normal

spoilage

Started and completed before normal spoilage (7,450 units)

Normal spoilage (80 units)

(A) Total costs of good units completed and transferred out

(B) Abnormal spoilage (50 units)

(C) Work in process, ending (1,700 units)

$ 1,677

2 ,504

4,181

33,377

359

37,917

225

3 ,892

$ 966 + $ 711

(0a $1.11) + (743a $3.37)

(7,450a $1.11) + (7,450a $3.37)

(80a $1.11) + (80a $3.37)

(50a $1.11) + (50a $3.37)

(1,700 a

$1.11) + (595 a

$3.37)

a Equivalent units of direct materials and conversion costs calculated in Step 2 in Solution Exhibit 18-23.

18-25 Weighted-average method, spoilage. LaCroix Company produces handbags from

leather of moderate quality. It distributes the product through outlet stores and department store

chains. At LaCroix’s facility in northeast Ohio, direct materials (primarily leather hides) are

added at the beginning of the process, while conversion costs are added evenly during the

process. Given the importance of minimizing product returns, spoiled units are detected upon

inspection at the end of the process and are discarded at a net disposal value of zero.

LaCroix uses the weighted-average method of process costing. Summary data for April 2017

are as follows:

18-@

Required:

1. For each cost category, calculate equivalent units. Show physical units in the first column of

your schedule.

2. Summarize the total costs to account for; calculate the cost per equivalent unit for each cost

category; and assign costs to units completed and transferred out (including normal spoilage),

to abnormal spoilage, and to units in ending work in process.

SOLUTION

(35 min.) Weighted-average method, spoilage.

1. Solution Exhibit 18-25, Panel A calculates equivalent units of work done to date for

direct materials and conversion costs.

2. Solution Exhibit 18-25, Panel B summarizes total costs to account for, calculates the

costs per equivalent unit for direct materials and conversion costs, and assigns total costs to units

completed and transferred out (including normal spoilage), to abnormal spoilage, and to units in

ending work in process, using the weighted-average method.

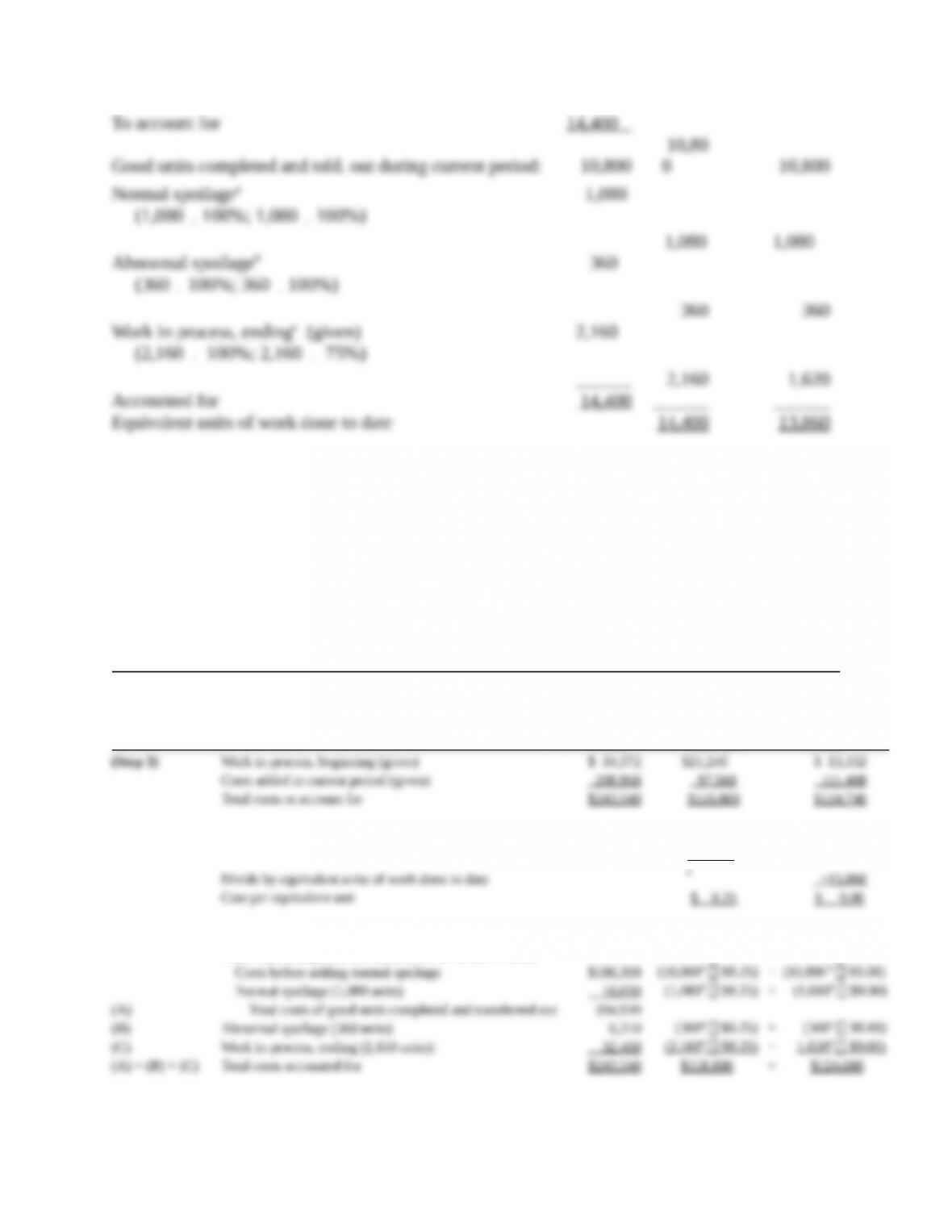

SOLUTION EXHIBIT 18-25

Weighted-Average Method of Process Costing with Spoilage,

La Croix Company for April 2017

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units

(Step 1) (Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given) 2,400

Started during current period (given) 12,000

18-@

aNormal spoilage is 10% of good units transferred out: 10% × 10,800 = 1,080 units. Degree of completion of normal spoilage

in this department: direct materials, 100%; conversion costs, 100%.

bTotal spoilage = Beg. units + Units started - Good units transferred out – Ending units = 2,400 + 12,000 - 10,800 - 2,160 = 1,440;

Abnormal spoilage = Total spoilage – Normal spoilage = 1,440 – 1,080 = 360 units. Degree of completion of abnormal spoilage

in this department: direct materials, 100%; conversion costs, 100%.

cDegree of completion in this department: direct materials, 100%; conversion costs, 75%.

PANEL B: Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit,

and Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process

Inventory

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 4) Costs incurred to date $118,800 $124,740

¸

14,400

(Step 5) Assignment of costs

Good units completed and transferred out (10,800 units)

dEquivalent units of direct materials and conversion costs calculated in step 2 of Solution Exhibit 18-21A.

18-@

18-26 FIFO method, spoilage.

Required:

1. Do Exercise 18-25 using the FIFO method.

2. What are the managerial issues involved in selecting or reviewing the percentage of spoilage

considered normal? How would your answer to requirement 1 differ if all spoilage were

viewed as normal?

SOLUTION

(35 min.) FIFO method, spoilage.

1. Solution Exhibit 18-26, Panel A calculates equivalent units of work done in the current

Solution Exhibit 18-26, Panel B summarizes total costs to account for, calculates the

SOLUTION EXHIBIT 18-26

First-in, first-out (FIFO) Method of Process Costing with Spoilage,

La Croix Company for April 2017

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

2,400

12 ,000

18-@

||Degree of completion in this department: direct materials, 100%; conversion costs, 50%.

#10,800 physical units completed and transferred out minus 2,400 physical units completed and transferred out from

beginning work-in-process inventory.

*Degree of completion of normal spoilage in this department: direct materials, 100%; conversion costs, 100%.

†Degree of completion of abnormal spoilage in this department: direct materials, 100%; conversion costs, 100%.

‡Degree of completion in this department: direct materials, 100%; conversion costs, 75%.

PANEL B: Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit,

and Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process

Inventory

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

$ 34,572

208 ,968

$21,240

97 ,560

$ 13,332

111 ,408

a Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A.

2. The issues related to the determination of the percentage of spoilage considered normal

are similar to the factors discussed in Chapter 17 regarding the importance of verifying the

In the above example, if all 1,440 units spoiled were considered normal spoilage, then

18-@

18-27 Spoilage, journal entries. Plastique produces parts for use in various industries.

Plastique uses a job-costing system. The nature of its process is such that management expects

normal spoilage at a rate of 2% of good parts. Data for last month is as follows:

Production (units) 10,000

Good parts produced 9,750

Direct material cost/unit $ 5.00

Required:

The spoiled parts were identified after 100% of the direct material cost was incurred. The

disposal value is $2/part.

1. Record the journal entries if the spoilage was (a) job specific or (b) common to all jobs.

2. Comment on the differences arising from the different treatment for these two scenarios.

SOLUTION

(10 min.) Spoilage, journal entries.

1. First, calculate normal and abnormal spoilage:

a) Journal entries if the spoilage was job specific

Normal Spoilage:

b) Journal entries if spoilage was common to all jobs

Normal Spoilage:

18-@

2. When the spoilage is specific to a certain job, the job absorbs the cost of those spoiled

parts less the disposal value. Therefore, the cost per good part of that job will be higher.

18-28 Recognition of loss from spoilage. Spheres Toys manufactures globes at its San

Fernando facility. The company provides you with the following information regarding

operations for April 2017:

Total globes manufactured 20,000

Globes rejected as spoiled units 750

Total manufacturing cost $800,000

Required:

Assume the spoiled units have no disposal value.

1. What is the unit cost of making the 20,000 globes?

2. What is the total cost of the 750 spoiled units?

3. If the spoilage is considered normal, what is the increase in the unit cost of good globes

manufactured as a result of the spoilage?

4. If the spoilage is considered abnormal, prepare the journal entries for the spoilage incurred.

SOLUTION

(15 min.) Recognition of loss from spoilage.

1. The unit cost of making the 20,000 globes is:

2. The total cost of the 750 spoiled units is:

3. The increase in the per-unit cost of goods sold as a result of the normal spoilage is:

4. The $30,000 cost for the 750 spoiled units is taken out of manufacturing costs and expensed in

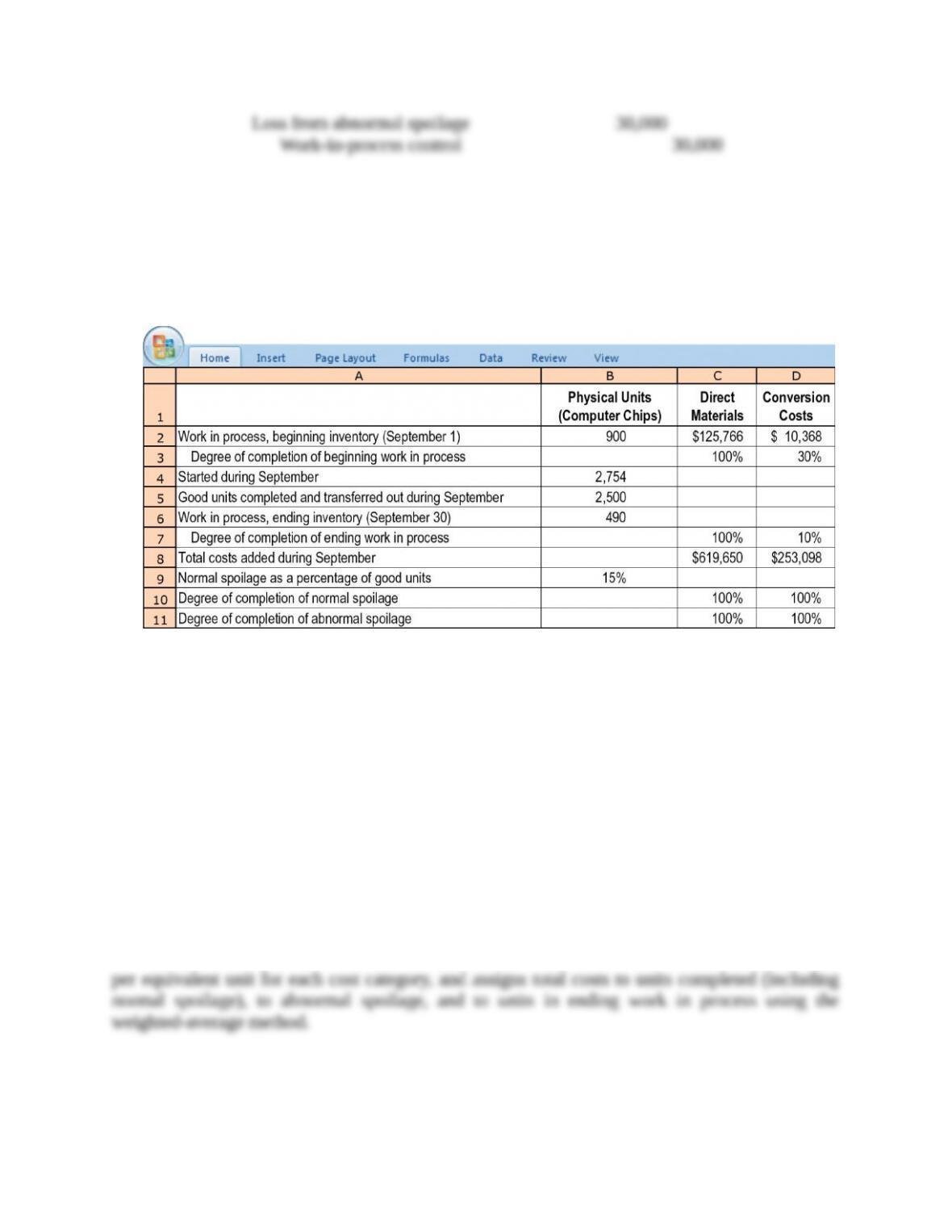

18-29 Weighted-average method, spoilage. LogicCo is a fast-growing manufacturer of

computer chips. Direct materials are added at the start of the production process. Conversion

costs are added evenly during the process. Some units of this product are spoiled as a result of

defects not detectable before inspection of finished goods. Spoiled units are disposed of at zero

net disposal value. LogicCo uses the weighted-average method of process costing.

Summary data for September 2017 are as follows:

Required:

1. For each cost category, compute equivalent units. Show physical units in the first column of

your schedule.

2. Summarize the total costs to account for; calculate the cost per equivalent unit for each cost

category; and assign costs to units completed and transferred out (including normal spoilage),

to abnormal spoilage, and to units in ending work in process.

SOLUTION

(25 min.) Weighted-average method, spoilage.

1. Solution Exhibit 18-29, Panel A, calculates the equivalent units of work done to date for each

cost category in September 2017.

2. Solution Exhibit 18-29, Panel B, summarizes total costs to account for, calculates the costs

SOLUTION EXHIBIT 18-29

Weighted-Average Method of Process Costing with Spoilage,

LogicCo for September 2017

18-@

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units

(Step 1) (Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

To account for

Good units completed and transferred out

900

2 ,754

3 ,654

*Normal spoilage is 15% of good units transferred out: 15% 2,500 = 375 units. Degree of completion of normal

spoilage in this department: direct materials, 100%; conversion costs, 100%.

†Total spoilage = 900 + 2,754 – 2,500 – 490 = 664 units; Abnormal spoilage = Total spoilage Normal spoilage =

664 375 = 289 units. Degree of completion of abnormal spoilage in this department: direct materials, 100%;

conversion costs, 100%.

‡Degree of completion in this department: direct materials, 100%; conversion costs, 20%.

PANEL B: Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit,

and Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process

Inventory

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

$ 136,134

872 ,748

$1 , 008,882

$125,766

619,650

$ 745,416

$ 10,368

253 ,098

$ 263 ,466

(A) Total cost of good units completed and

transferred out

822,250

18-@

# Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A.

18-30 FIFO method, spoilage. Refer to the information in Exercise 18-29.

Required:

1. Do Exercise 18-29 using the FIFO method of process costing.

2. Should LogicCo’s managers choose the weighted-average method or the FIFO method?

Explain briefly.

SOLUTION

(25 min.) FIFO method, spoilage.

1. Solution Exhibit 18-30, Panel A, calculates the equivalent units of work done in the

current period for each cost category in September 2017.

Solution Exhibit 18-30, Panel B, summarizes LogicCo’s production costs for September

SOLUTION EXHIBIT 18-30

First-in, First-out (FIFO) Method of Process Costing with Spoilage,

LogicCo for September 2017

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

To account for

Good units completed and transferred out

during current period:

Abnormal spoilage†

900

2 ,754

3 ,654

289

18-@

||Degree of completion in this department: direct materials, 100%; conversion costs, 30%.

#2,500 physical units completed and transferred out minus 900 physical units completed and transferred out from

beginning work in process inventory.

PANEL B: Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit,

and Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process

Inventory

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

$ 136,134

872,748

$ 1,008,882

$125,766

619,650

$745,416

$ 10,368

253,098

$263,466

2

§Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A.

18-@