SOLUTION

(20 min.) Throughput costing (continuation of Exercise 9-21).

1. April 2017 May 2017

Direct material cost of goods sold

Beginning inventory

d ($3,300 × 500) + $2,000,000

2. Operating income under:

April May

In April, throughput costing has the lowest operating income, whereas in May throughput costing

3. Throughput costing puts a penalty on production without a corresponding sale in the

9-23 Variable and absorption costing, explaining operating-income

differences. EntertainMe Corporation manufactures and sells 50-inch television sets and uses

standard costing. Actual data relating to January, February, and March 2017 are as follows:

9-1

January February March

Unit data:

Beginning inventory 0 150 150

Production 1,500 1,400 1,520

Sales 1,350 1,400 1,530

Variable costs:

Manufacturing cost per unit produced $

1,000

$ 1,000 $

1,00

0

Operating (marketing) cost per unit

sold

$

800

$ 800 $

800

Fixed costs:

Manufacturing costs $525,00

0

$525,000 $525,0

00

Operating (marketing) costs $130,00

0

$130,000 $130,0

00

The selling price per unit is $3,300. The budgeted level of production used to calculate the

budgeted fixed manufacturing cost per unit is 1,500 units. There are no price, efficiency, or

spending variances. Any production-volume variance is written off to cost of goods sold in the

month in which it occurs.

1. Prepare income statements for EntertainMe in January, February, and March 2017 under (a)

variable costing and (b) absorption costing.

2. Explain the difference in operating income for January, February, and March under variable

costing and absorption costing.

SOLUTION

(40 min.) Variable and absorption costing, explaining operating-income differences.

1. Key inputs for income statement computations are:

January February March

Beginning inventory

0

150

150

The budgeted fixed manufacturing cost per unit and budgeted total manufacturing cost

9-2

per unit under absorption costing are:

January February March

9-3

(a) Variable Costing

January 2017 February 2017 March 2017

Revenuesa$4,455,000 $4,620,000 $5,049,000

Variable costs

Beginning inventoryb$ 0 $ 150,000 $ 150,000

9-4

(b) Absorption Costing

January 2017 February 2017 March 2017

Operating costs

9-5

2. – = –

The difference between absorption and variable costing is due solely to moving fixed

manufacturing costs into inventories as inventories increase (as in January) and out of

inventories as they decrease (as in March).

9-24 Throughput costing (continuation of 9-23). The variable manufacturing costs per unit

of EntertainMe Corporation are as follows:

January February March

Direct material cost per unit $ 525 $ 525 $ 525

Direct manufacturing labor cost per unit 200 200 200

Manufacturing overhead cost per unit 275 275 275

$1,000 $1,000 $1,000

Required:

1. Prepare income statements for EntertainMe in January, February, and March 2017 under

throughput costing.

2. Contrast the results in requirement 1 of this exercise with those in requirement 1 of Exercise

9-23.

3. Give one motivation for EntertainMe to adopt throughput costing.

SOLUTION

(20–30 min.) Throughput costing (continuation of Exercise 9-23).

1.

January February March

Revenuesa

Direct material cost of

goods sold:

Beginning inventoryb$ 0

$4,455,000

$78,750

$4,620,000

$ 78,750

$5,049,000

9-6

Direct materials in goods

Other costs

Manufacturinge

Operatingf

1,237,500

1 ,210,000

1,190,000

1 ,250,000

1,247,000

1 ,354,000

2. Operating income under:

January February March

Throughput costing

Throughput costing puts greater emphasis on sales as the source of operating income than does

3. Throughput costing puts a penalty on producing without a corresponding sale in the same

period. Costs other than direct materials that are variable with respect to production are expensed

9-25 Variable versus absorption costing. The Tomlinson Company manufactures trendy,

high-quality, moderately priced watches. As Tomlinson’s senior financial analyst, you are asked

to recommend a method of inventory costing. The CFO will use your recommendation to prepare

Tomlinson’s 2017 income statement. The following data are for the year ended December 31,

2017:

Beginning inventory, January 1, 2017 90,000 units

9-7

Ending inventory, December 31, 2017 34,000 units

2017 sales 433,000 units

Selling price (to distributor) $24.00 per unit

Variable manufacturing cost per unit, including

direct materials

$5.40 per unit

Variable operating (marketing) cost per unit sold $1.20 per unit sold

Fixed manufacturing costs $1,852,200

Denominator-level machine-hours 6,300

Standard production rate 60 units per machine-hour

Fixed operating (marketing) costs $1,130,000

Required:

Assume standard costs per unit are the same for units in beginning inventory and units produced

during the year. Also, assume no price, spending, or efficiency variances. Any

production-volume variance is written off to cost of goods sold.

1. Prepare income statements under variable and absorption costing for the year ended

December 31, 2017.

2. What is Tomlinson’s operating income as percentage of revenues under each costing method?

3. Explain the difference in operating income between the two methods.

4. Which costing method would you recommend to the CFO? Why?

SOLUTION

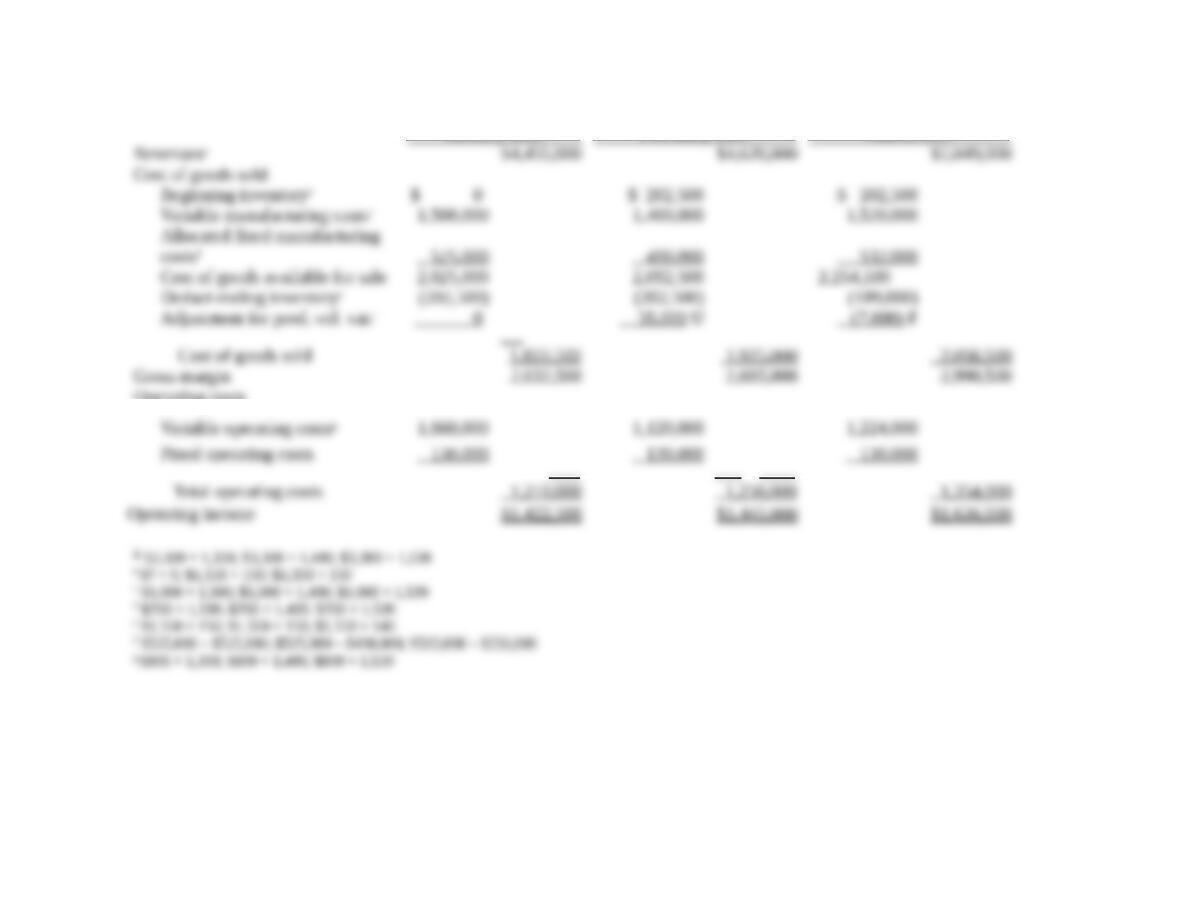

(40 min) Variable versus absorption costing.

1.

Beginning Inventory + 2017 Production = 2017 Sales + Ending Inventory

Income Statement for the Tomlinson Company, Variable Costing

for the Year Ended December 31, 2017

Revenues: $24 × 433,000 $10,392,000

Variable costs

9-8

Fixed costs

Absorption Costing Data

Fixed manufacturing overhead allocation rate =

¸

Fixed manufacturing overhead allocation rate per unit =

¸

Income Statement for the Tomlinson Company, Absorption Costing

for the Year Ended December 31, 2017

Revenues: $24 × 433,000 $10,392,000

Cost of goods sold

Beginning inventory ($5.40 + $4.90) × 90,000 $ 927,000

Variable manuf. costs: $5.40 × 377,000 2,035,800

Deduct ending inventory: ($5.40 + $4.90) × 34,000 (350,200)

Operating costs

Variable operating costs: $1.20 × 433,000 $ 519,600

Fixed operating costs 1 ,130,000

Total operating costs 1 ,649,600

2. Tomlinson’s operating margins as a percentage of revenues are

9-9

Under variable costing:

Under absorption costing:

3. Operating income using variable costing is 6.4% higher than operating income calculated

using absorption costing. The difference is entirely due to the way fixed manufacturing costs are

accounted for under the two costing systems.

4. The factors the CFO should consider include

(a) Effect on managerial behavior.

(b) Effect on external users of financial statements.

I would recommend absorption costing because it considers all the manufacturing resources

(whether variable or fixed) used to produce units of output. Absorption costing has many critics.

However, the dysfunctional aspects associated with absorption costing can be reduced by

9-26 Absorption and variable costing. (CMA) Miami, Inc., planned and actually

manufactured 250,000 units of its single product in 2017, its first year of operation. Variable

manufacturing cost was $19 per unit produced. Variable operating (nonmanufacturing) cost was

$13 per unit sold. Planned and actual fixed manufacturing costs were $750,000. Planned and

actual fixed operating (nonmanufacturing) costs totaled $420,000. Miami sold 170,000 units of

product at $41 per unit.

Required:

1. Miami’s 2017 operating income using absorption costing is (a) $600,000, (b) $360,000, (c)

$780,000, (d) $1,020,000, or (e) none of these. Show supporting calculations.

2. Miami’s 2017 operating income using variable costing is (a) $1,100,000, (b) $600,000, (c)

$360,000, (d) $780,000, or (e) none of these. Show supporting calculations.

9-10

9-11