SOLUTION

(30 min.) Special order, activity-based costing.

1. Direct materials cost per unit ($600,000 10,000 units) = $60 per unit

Reward One’s opera&ng income under the alterna&ves of accep&ng/rejec&ng the special

order are:

Without

One-Time

Only Special

Order

10,000 Units

With

One-Time

Only Special

Order

12,000 Units

difference

2,000 Units

Revenues $2 ,500,000 $2 ,950,000 $450 ,000

Variable costs:

1$600,000 + ($60 2,000 units) 2$700,000 + ($70 2,000 units) 3$150,000 + ($1,500 25

batches)

11-

Alterna&vely, we could calculate the incremental revenue and the incremental costs of the

addi&onal 2,000 units as follows:

Reward One should accept the one-&me-only special order if it has no long-term implica&ons

because accep&ng the order increases Reward One’s opera&ng income by $152,500.

2. Reward One has a capacity of 11,000 windows. Therefore, if it accepts the special

one-time order of 2,000 windows, it can sell only 9,000 windows instead of the 10,000 windows

that it currently sells to existing customers. That is, by accepting the special order, Reward One

must forgo sales of 1,000 windows to its regular customers. Alternatively, Reward One can reject

the special order and continue to sell 10,000 windows to its regular customers.

Reward One’ operating income from selling 9,000 windows to regular customers and

2,000 windows under one-time special order follow:

11-

1Reward One makes regular windows in batch sizes of 100. To produce 9,000 windows requires

90 (9,000 ÷ 100) batches.

Accep&ng the special order will result in an increase in opera&ng income of $47,500

($447,500 – $400,000). The special order should, therefore, be accepted.

A more direct approach would be to focus on the incremental effects––the benefit of

accep&ng the special order of 2,000 units versus the costs of selling 1,000 fewer units to regular

customers. Increase in opera&ng income from the 2,000-unit special order equals $152,500

(requirement 1). The loss in opera&ng income from selling 1,000 fewer units to regular

customers equals:

Accep&ng the special order will result in an increase in opera&ng income of $47,500 ($152,500 –

$105,000). The special order should, therefore, be accepted.

3. Reward One should not accept the special order.

Increase in opera&ng income by selling 2,000 units

The special order should, therefore, be rejected.

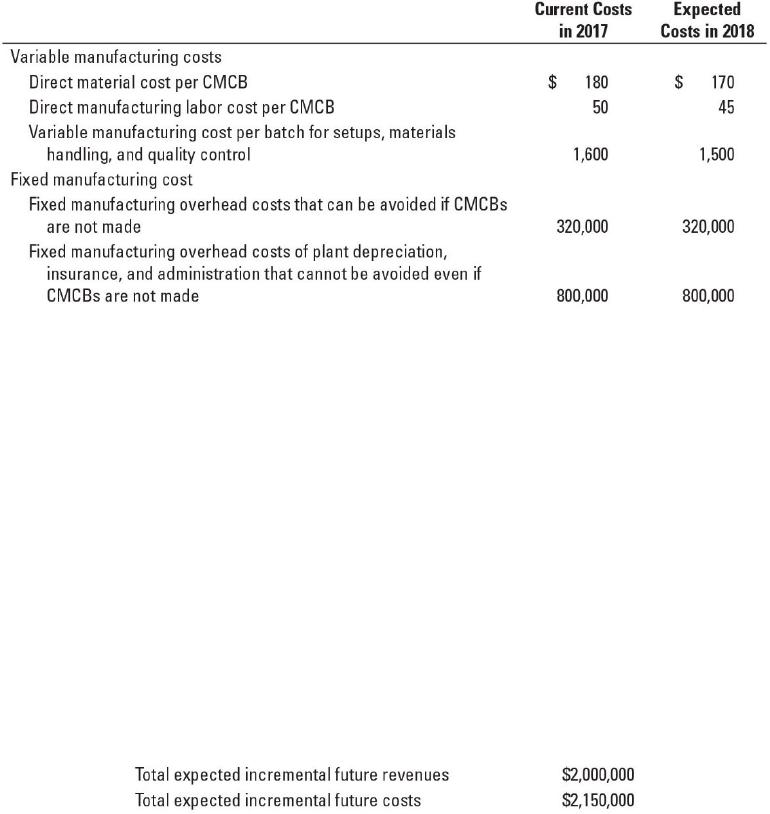

11-25 Make versus buy, activity-based costing. The Svenson Corporation manufactures

cellular modems. It manufactures its own cellular modem circuit boards (CMCB), an important

part of the cellular modem. It reports the following cost information about the costs of making

CMCBs in 2017 and the expected costs in 2018:

11-

Svenson manufactured 8,000 CMCBs in 2017 in 40 batches of 200 each. In 2018, Svenson

anticipates needing 10,000 CMCBs. The CMCBs would be produced in 80 batches of 125 each.

The Minton Corporation has approached Svenson about supplying CMCBs to Svenson in

2018 at $300 per CMCB on whatever delivery schedule Svenson wants.

Required:

1. Calculate the total expected manufacturing cost per unit of making CMCBs in 2018.

2. Suppose the capacity currently used to make CMCBs will become idle if Svenson purchases

CMCBs from Minton. On the basis of financial considerations alone, should Svenson make

CMCBs or buy them from Minton? Show your calculations.

3. Now suppose that if Svenson purchases CMCBs from Minton, its best alternative use of the

capacity currently used for CMCBs is to make and sell special circuit boards (CB3s) to the

Essex Corporation. Svenson estimates the following incremental revenues and costs from

CB3s:

On the basis of financial considerations alone, should Svenson make CMCBs or buy them

from Minton? Show your calculations.

SOLUTION

(30 min.) Make versus buy, activity-based costing.

1. The expected manufacturing cost per unit of CMCBs in 2018 is as follows:

11-

Total

Manufacturing

Costs of CMCB

(1)

Manufacturing

Cost per Unit

(2) = (1) ÷ 10,000

Direct materials, $170 10,000

$1,700,000

$170

2. The following table iden&:es the incremental costs in 2015 if Svenson (a) made CMCBs

and (b) purchased CMCBs from Minton.

Total

Incremental Costs

Per-Unit

Incremental Costs

Incremental Items Make Buy Make Buy

Cost of purchasing CMCBs from Minton

$3,000,000

$300

11-

Svenson should con&nue to manufacture the CMCBs internally because the incremental

costs to manufacture are $259 per unit compared to the $300 per unit that Minton has quoted.

3. Svenson should con&nue to make CMCBs. The simplest way to analyze this problem is to

recognize that Svenson would prefer to keep any excess capacity idle rather than use it to make

CB3s. Why? Because expected incremental future revenues from CB3s, $2,000,000, are less

than expected incremental future costs, $2,150,000. If Svenson keeps its capacity idle, we know

from requirement 2 that it should make CMCBs rather than buy them.

An important point to note is that, because Svenson forgoes no contribu&on by not

being able to make and sell CB3s, the opportunity cost of using its facili&es to make CMCBs is

zero. It is, therefore, not forgoing any profit by using the capacity to manufacture CMCBs. If it

does not manufacture CMCBs, rather than lose money on CB3s, Svenson will keep capacity idle.

Choices for Svenson

Relevant Items

Make CMCBs

and Do Not

Make CB3s

Buy CMCBs

and Make

CB3s, if profitable

TOTAL-ALTERNATIVES APPROACH TO MAKE-OR-BUY DECISIONS

11-

Total incremental costs of

making/buying CMCBs (from

requirement 2)

Because incremental future costs

exceed incremental future revenues

from CB3s, Svenson will make zero

CB3s even if it buys CMCBs from

Minton

Total relevant costs

0

0

Svenson will minimize manufacturing costs and maximize opera&ng income by making CMCBs.

OPPORTUNITY-COST APPROACH TO MAKE-OR-BUY DECISIONS

Total incremental costs of

making/buying CMCBs (from

requirement 2)

Opportunity cost: pro:t contribu&on

forgone because capacity will not

be used to make CB3s

0* 0

*Opportunity cost is zero because Svenson does not give up anything by not making CB3s.

Svenson is best off leaving the capacity idle (rather than manufacturing and selling CB3s).

11-26 Inventory decision, opportunity costs. Best Trim, a manufacturer of lawn mowers,

predicts that it will purchase 204,000 spark plugs next year. Best Trim estimates that 17,000

spark plugs will be required each month. A supplier quotes a price of $9 per spark plug. The

supplier also offers a special discount option: If all 204,000 spark plugs are purchased at the start

of the year, a discount of 2% off the $9 price will be given. Best Trim can invest its cash at 10%

per year. It costs Best Trim $260 to place each purchase order.

11-

Required:

1. What is the opportunity cost of interest forgone from purchasing all 204,000 units at the start

of the year instead of in 12 monthly purchases of 17,000 units per order?

2. Would this opportunity cost be recorded in the accounting system? Why?

3. Should Best Trim purchase 204,000 units at the start of the year or 17,000 units each month?

Show your calculations.

4. What other factors should Best Trim consider when making its decision?

SOLUTION

(10 min.) Inventory decision, opportunity costs.

1. Unit cost, orders of 17,000 $9.00

Opportunity cost of interest forgone from 204,000-unit purchase at start of year

= $823,140 0.10 = $82,314

2. No. The $82,314 is an opportunity cost rather than an incremental or outlay cost. No

3. The following table presents the two alternatives:

11-

Alternative A:

Purchase

204,000

spark plugs at

beginning of

year

(1)

Alternative B:

Purchase

17,000

spark plugs

at beginning

of each month

(2)

difference

(3) = (1) – (2)

Annual purchase-order costs

Column (3) indicates that purchasing 17,000 spark plugs at the beginning of each month is

4. If other incremental benefits of holding lower inventory such as lower insurance,

11-27 Relevant costs, contribution margin, product emphasis. The Beach Comber is a

take-out food store at a popular beach resort. Sara Miller, owner of the Beach Comber, is

deciding how much refrigerator space to devote to four different drinks. Pertinent data on these

four drinks are as follows:

11-

Miller has a maximum front shelf space of 12 feet to devote to the four drinks. She wants a

minimum of 1 foot and a maximum of 6 feet of front shelf space for each drink.

Required:

1. Calculate the contribution margin per case of each type of drink.

2. A coworker of Miller’s recommends that she maximize the shelf space devoted to those

drinks with the highest contribution margin per case. Do you agree with this

recommendation? Explain briefly.

3. What shelf-space allocation for the four drinks would you recommend for the Beach

Comber? Show your calculations.

11-