SOLUTION EXHIBIT 8-36

Variable Manufacturing Overhead

Actual Costs

Incurred

(1)

Actual Input Qty.

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

(1,632 $44)

$71,808

(1,632 $42)

$68,544

(1,920 $42)

$80,640

(1,920 $42)

$80,640

Fixed Manufacturing Overhead

Actual Costs

Incurred

(1)

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless Of

Output Level

(2)

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

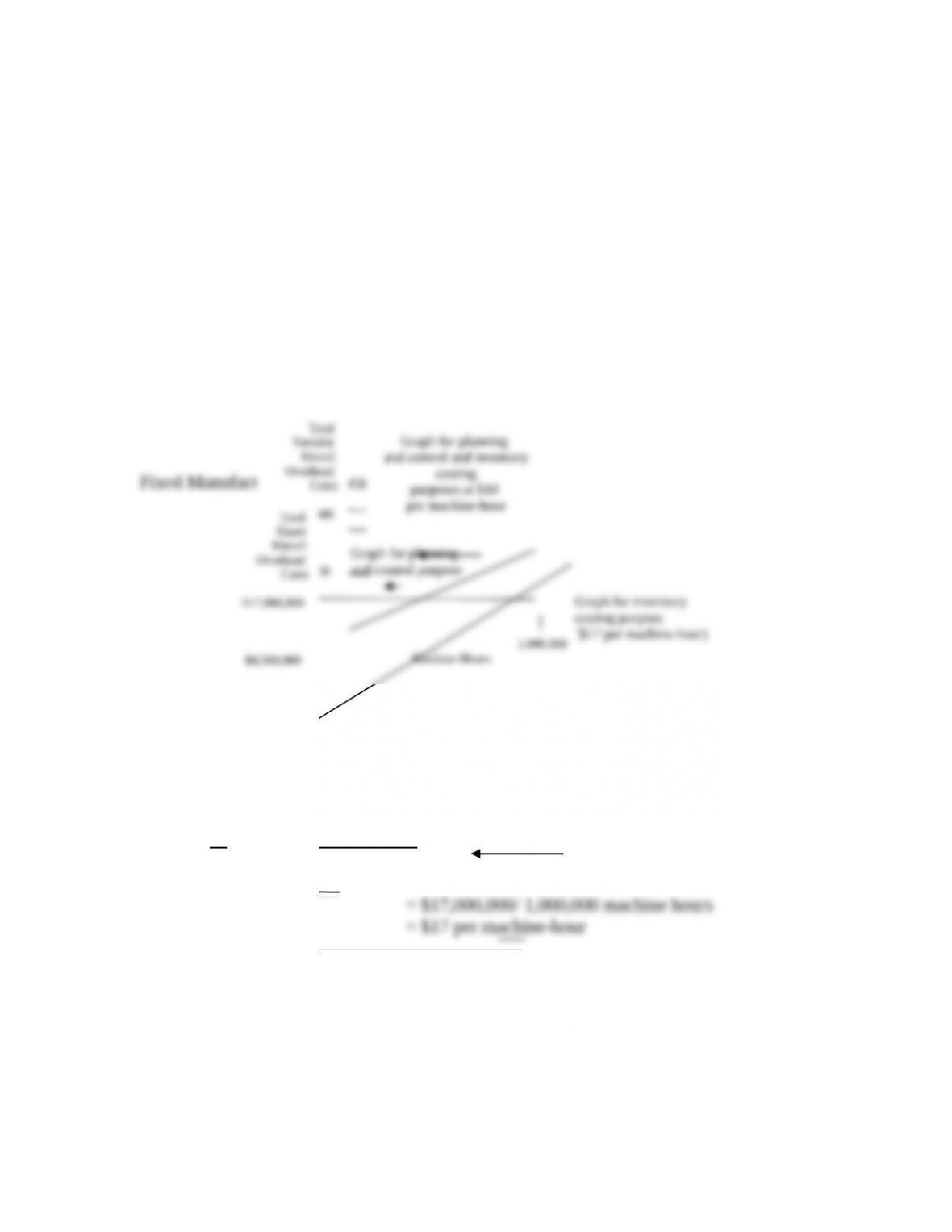

8-37 Graphs and overhead variances. Best Around, Inc., is a manufacturer of vacuums and

uses standard costing. Manufacturing overhead (both variable and fixed) is allocated to products on

the basis of budgeted machine-hours. In 2017, budgeted fixed manufacturing overhead cost was

$17,000,000. Budgeted variable manufacturing overhead was $10 per machine-hour. The

denominator level was 1,000,000 machine-hours.

Required:

1. Prepare a graph for fixed manufacturing overhead. The graph should display how Best

Around, Inc.’s fixed manufacturing overhead costs will be depicted for the purposes of (a)

planning and control and (b) inventory costing.

2. Suppose that 1,125,000 machine-hours were allowed for actual output produced in 2017, but

1,200,000 actual machine-hours were used. Actual manufacturing overhead was

$12,075,000, variable, and $17,100,000, fixed. Compute (a) the variable manufacturing

overhead spending and efficiency variances and (b) the fixed manufacturing overhead

$3,264 U

Spending variance

$12,096 F

Efficiency variance

Never a variance

spending and production-volume variances. Use the columnar presentation illustrated in

Exhibit 8-4 (page 304).

3. What is the amount of the under- or overallocated variable manufacturing overhead and the

under- or overallocated fixed manufacturing overhead? Why are the flexible-budget variance

and the under- or overallocated overhead amount always the same for variable manufacturing

overhead but rarely the same for fixed manufacturing overhead?

4. Suppose the denominator level was 1,700,000 rather than 1,000,000 machine-hours. What

variances in requirement 2 would be affected? Recompute them.

SOLUTION

(3040 min.) Graphs and overhead variances.

1. Variable Manufacturing Overhead Costs

=

2. (a) Variable Manufacturing Overhead Variance Analysis for Best Around, Inc. for 2017

1,000,000

1,000,000

Machine-Hours

Actual Costs

Incurred

(1)

Actual Input Qty.

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

(1,200,000 $10)

(1,125,000 $10)

(1,125,000 $10)

(b) Fixed Manufacturing Overhead Variance Analysis for Best Around, Inc. for 2017

Actual Costs

Incurred

(1)

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(2)

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

(1,125,000 × $17)

*Alternative computation: 1,125,000 budgeted hrs. allowed – 1,000,000 denominator hrs. = 125,000 hrs.

125,000 $17 = $2,125,000 F

$,825,000 U

Flexible-budget variance

Never a variance

Underallocated variable overhead

(Total variable overhead variance)

$100,000 U

$2,125,000 F*

3. The underallocated variable manufacturing overhead was $825,000 and overallocated

fixed overhead was $2,025,000. The flexible-budget variance and underallocated overhead are

4. The choice of the denominator level will affect inventory costs. The new fixed

manufacturing overhead rate would be $17,000,000 ÷ 1,700,000 = $10.00 per machine-hour. In

turn, the allocated amount of fixed manufacturing overhead and the production-volume variance

would change as seen below:

Actual Budget Allocated

1,125,000 × $10.00 =

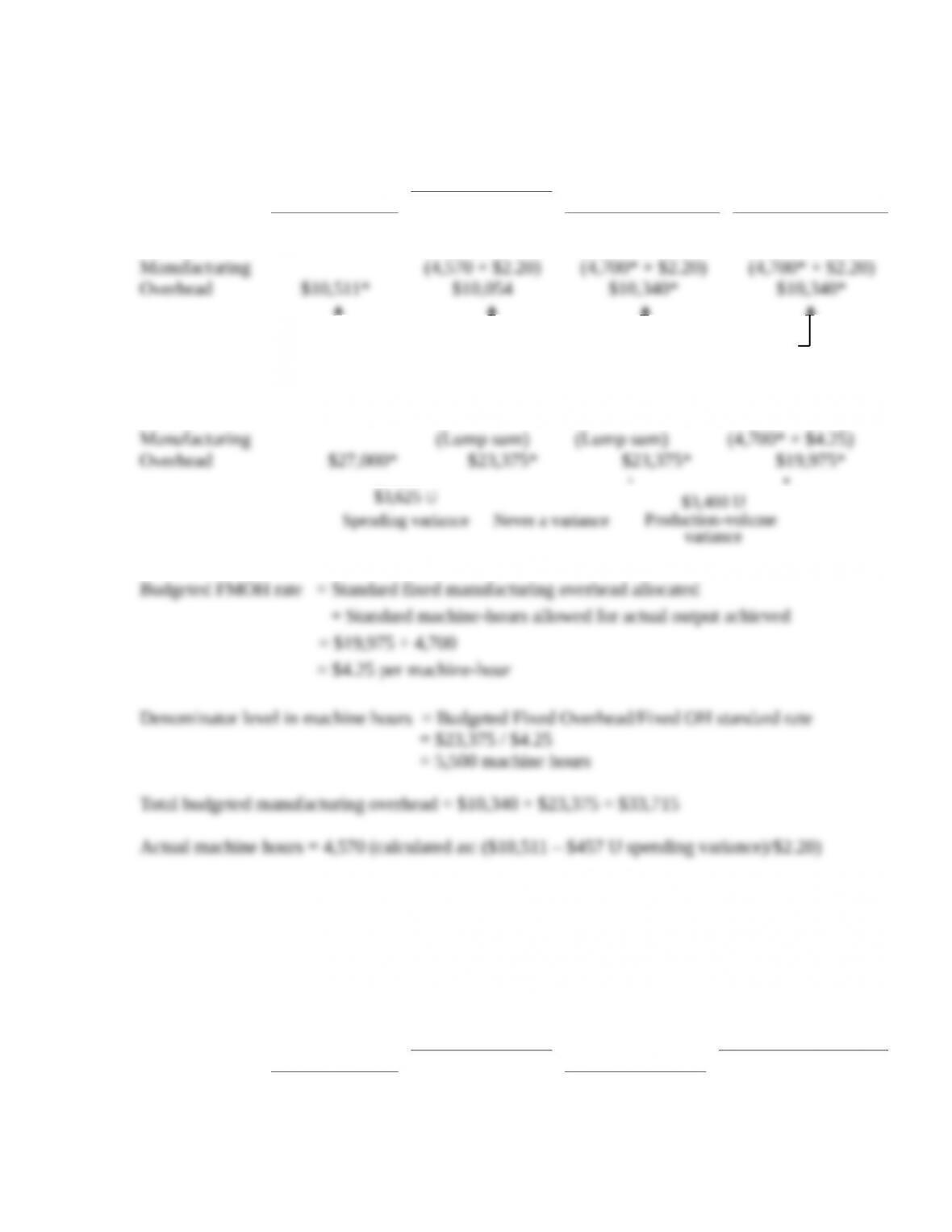

8-38 Overhead variance, missing information. Consider the following two situations—cases

A and B—independently. Data refer to operations for April 2017. For each situation, assume

standard costing. Also assume the use of a flexible budget for control of variable and fixed

manufacturing overhead based on machine-hours.

Cases

A B

(1) Fixed manufacturing overhead incurred $27,000 $132,900

(2) Variable manufacturing overhead incurred $10,511 —

(3) Denominator level in machine-hours — 45,000

(4) Standard machine-hours allowed for actual

output achieved

4,700 —

(5) Fixed manufacturing overhead (per standard

machine-hour)

— —

Flexible-Budget Data:

(6) Variable manufacturing overhead (per standard — $ 2.10

Cases

A B

machine-hour)

(7) Budgeted fixed manufacturing overhead $23,375 $130,500

(8) Budgeted variable manufacturing overheada— —

(9) Total budgeted manufacturing overheada— —

Additional Data:

(10) Standard variable manufacturing overhead

allocated

$10,340 —

(11) Standard fixed manufacturing overhead

allocated

$19,975 —

(12) Production-volume variance — $ 580 F

(13) Variable manufacturing overhead spending

variance

$ 457 U $ 1,490 F

(14) Variable manufacturing overhead efficiency

variance

— $ 1,680 F

(15) Fixed manufacturing overhead spending

variance

— —

(16) Actual machine-hours used — —

aFor standard machine-hours allowed for actual output produced.

Required:

Fill in the blanks under each case. [Hint: Prepare a worksheet similar to that in Exhibit 8-4 (page

304). Fill in the knowns and then solve for the unknowns.]

SOLUTION

(30 min.) Overhead variance, missing information.

Known figures denoted by an *

Case A:

Actual Costs

Incurred

Actual Input Qty.

× Budgeted Rate

Flexible Budget:

Budgeted Input

Qty.

Allowed for

Actual Output

× Budgeted Rate

Allocated:

Budgeted Input

Qty.

Allowed for

Actual Output

× Budgeted Rate

Variable

Manufacturing

(4,570 × $2.20)

(4,700* × $2.20)

(4,700* × $2.20)

Fixed

Manufacturing

(Lump sum)

(Lump sum)

(4,700* × $4.25)

Case B:

Actual Costs

Incurred

Actual Input Qty.

× Budgeted Rate

Flexible Budget:

Budgeted Input

Qty.

Allowed for

Actual Output

× Budgeted Rate

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

Never a variance

$286 F

Efficiency variance

$457 U*

Spending variance

Variable

Manufacturing

Overhead $91,750

(44,400 $2.10*)

$93,240

(45,200 $2.10*)

$94,920

(45,200 $2.10*)

$94,920

Fixed

Manufacturing

Overhead $132,900*

(Lump sum)

$130,500*

(Lump sum)

$130,500*

45,200 x $2.90

$131,080

Budgeted FMOH rate = Budgeted fixed manufacturing overhead

÷ Denominator level in machine-hours

Standard machine-hours allowed for actual output

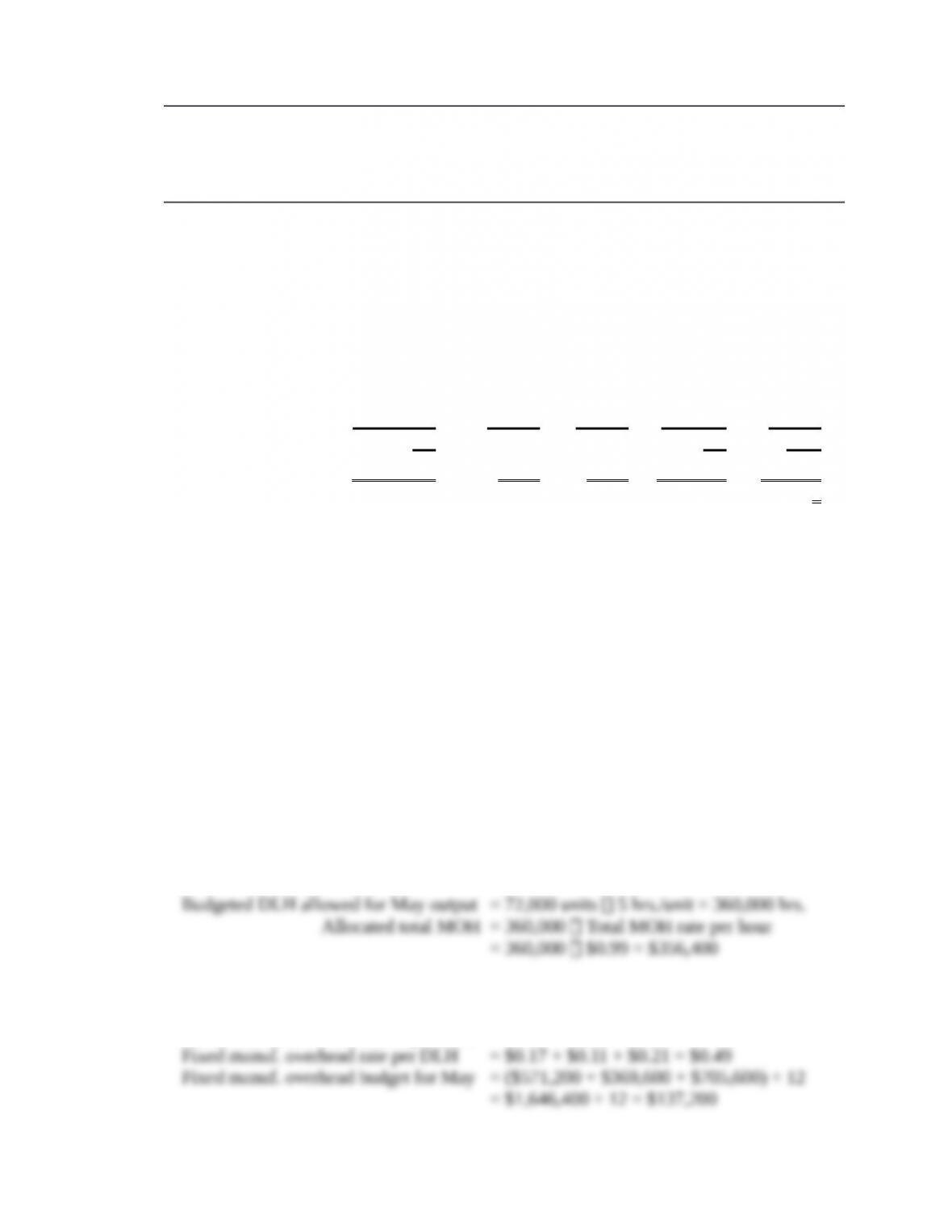

8-39 Flexible budgets, 4-variance analysis. (CMA, adapted) Wilson Products uses standard

costing. It allocates manufacturing overhead (both variable and fixed) to products on the basis of

standard direct manufacturing labor-hours (DLH). Wilson Products develops its manufacturing

overhead rate from the current annual budget. The manufacturing overhead budget for 2017 is

based on budgeted output of 672,000 units, requiring 3,360,000 DLH. The company is able to

schedule production uniformly throughout the year.

A total of 72,000 output units requiring 321,000 DLH was produced during May 2017.

Manufacturing overhead (MOH) costs incurred for May amounted to $355,800. The actual costs,

compared with the annual budget and 1/12 of the annual budget, are as follows:

Never a variance

$1,680 F*

Efficiency variance

$1,490 F*

Spending variance

$580 F*

Production-volume

variance

Never a variance

$2,400 U

Spending variance

Annual Manufacturing Overhead Budget 2017

Total

Amount

Per

Output

Unit

Per DLH

Input

Unit

Monthly

MOH

Budget

May 2017

Actual

MOH

Costs for

May 2017

Variable MOH

Indirect

manufacturing labor

$1,008,000 $1.50 $0.30 $ 84,000 $

84,000

Supplies 672,000 1.00 0.20 56,000 117,000

Fixed MOH

Supervision 571,200 0.85 0.17 47,600 41,000

Utilities 369,600 0.55 0.11 30,800 55,000

Depreciation 705,6

00

1.05 0.21 58,8

00

88,

800

Total $3,326,400 $4.95 $0.99 $277,200 $355,80

0

Calculate the following amounts for Wilson Products for May 2017:

Required:

1. Total manufacturing overhead costs allocated

2. Variable manufacturing overhead spending variance

3. Fixed manufacturing overhead spending variance

4. Variable manufacturing overhead efficiency variance

5. Production-volume variance

Be sure to identify each variance as favorable (F) or unfavorable (U).

SOLUTION

(1525 min.) Flexible budgets, 4-variance analysis.

1. =

= = 3,360,000/672,000 = 5 hours per unit

2, 3, 4, 5. See Solution Exhibit 8-39

Variable manuf. overhead rate per DLH = $0.30 + $0.20 = $0.50

or,

An overview of the 4-variance analysis using the block format of the text is:

4-Variance

Analysis

Spending

Variance

Efficiency

Variance

Production-

Volume

Variance

Variable

Overhead

Fixed

Overhead

SOLUTION EXHIBIT 8-39

Variable Manufacturing Overhead

Actual Costs

Incurred

(1)

Actual Input Qty.

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

$201,000

(321,000 $0.50)

$160,500

(360,000 $0.50)

$180,000

(360,000 $0.50)

$180,000

$40,500 U

Spending variance

$19,500 F

Efficiency variance

Never a variance

Fixed Manufacturing Overhead

Actual Costs

Incurred

(1)

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(2)

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(3)

Allocated:

Budgeted Input

Allowed for

Actual Output

× Budgeted Rate

(4)

(360,000 $0.49)