SOLUTION

(20 min.) Operation costing.

1. Calculate the conversion cost rates for each department:

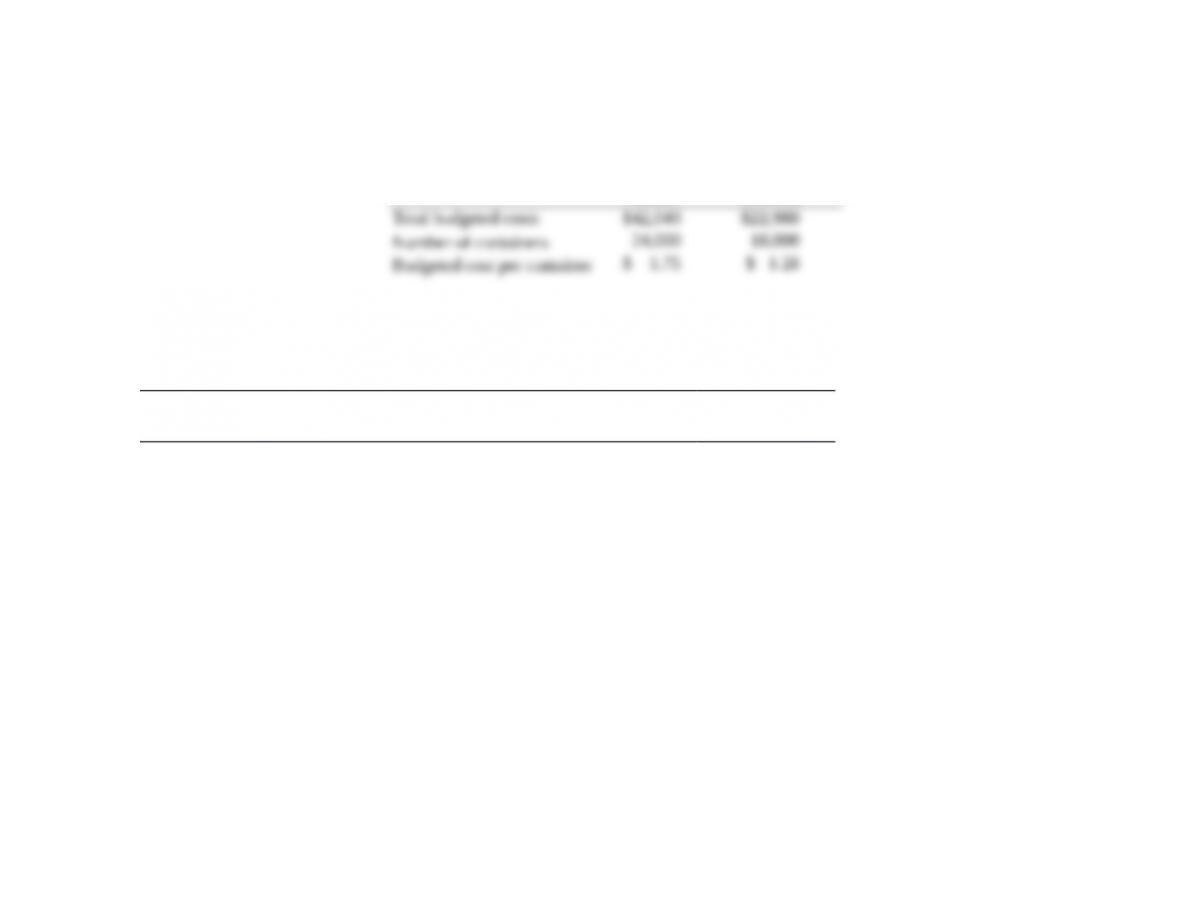

Relax Refresh Total

Budgeted

Conversion

Cost

Cost Driver

Budgeted

Quantity

of Cost

Driver Conversion Cost Rate

2. Budgeted cost of goods manufactured:

Relax Refresh

d $9.80 per labor-hour (1,200; 0 labor hours)

e $0.48 per container (24,000; 18,000 containers)

f $8.00 per machine-hour (200; 150 machine hours)

3. Budgeted cost per container

Relax Refresh

17-34 Standard-costing with beginning and ending work in process. Lawrence Company is a manufacturer of contemporary door

handles. The vice president of Design attends home shows twice a year so the company can keep current with home trends. Because of

its volume, Lawrence uses process costing to account for production. Costs and output figures for August are as follows:

Lawrence Company’s Process Costing for the Month Ended August 31, 2017

Units

Direct

Materials

Conversion

Costs

Standard cost per unit $ 5.75 $ 12.25

Work in process, beginning inventory (Aug. 1) 15,000 $ 86,250 $ 55,125

Degree of completion of beginning work in

process

100% 30%

Started in August 100,000

Completed and transferred out 95,000

Work in process, ending inventory (Aug. 31) 20,000

Degree of completion of ending work in

process

100% 80%

Total costs added during August $569,000 $1,307,240

Required:

1. Compute equivalent units for direct materials and conversion costs. Show physical units in the first column of your schedule.

2Compute the total standard costs of handles transferred out in August and the total standard costs of the August 31 inventory of

work in process.

3. Compute the total August variances for direct materials and conversion costs.

4. Prepare summarized journal entries to record both the actual costs and standard costs for direct materials and conversion costs,

including the variances for both production costs.

SOLUTION

(30-35 min.) Standard-costing with beginning and ending work in process.

1. Solution Exhibit 17-34A computes the equivalent units of work done in November 2017 by Lawrence Company for direct

materials and conversion costs.

2. and 3. Solution Exhibit 17-34B summarizes total costs of the Lawrence Company for August 31, 2017 and, using the standard

cost per equivalent unit for direct materials and conversion costs, assigns these costs to units completed and transferred out and to

units in ending work in process. The exhibit also summarizes the cost variances for direct materials and conversion costs for August

2017.

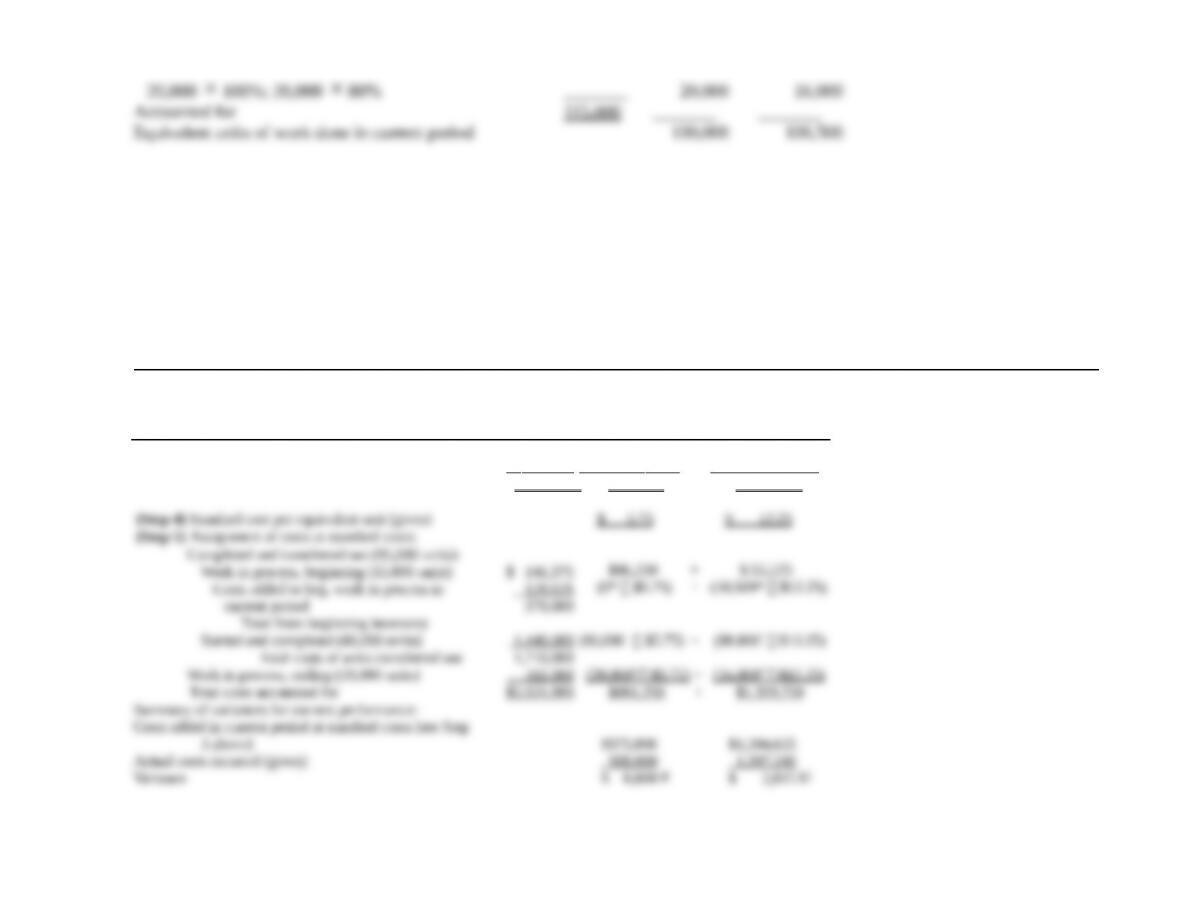

SOLUTION EXHIBIT 17-34A

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

Standard Costing Method of Process Costing,

Lawrence Company for the month ended August 31, 2017.

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

§Degree of completion in this department: direct materials, 100%; conversion costs, 30%.

†95,000 physical units completed and transferred out minus 15,000 physical units completed and transferred out from beginning work-in-process inventory.

*Degree of completion in this department: direct materials, 100%; conversion costs, 80%.

SOLUTION EXHIBIT 17-34B

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign Costs to the Units Completed and Units

in Ending Work-in-Process Inventory;

Standard-Costing Method of Process Costing,

Lawrence Company for the month ended August 31, 2017.

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given) $ 141,375 $ 86,250 + $ 55,125

Costs added in current period at standard costs 1 ,879,625 ( 100,000 5.75) + ( 10,500 $12.25)

Total costs to account for $ 2 ,021,000 $661 ,250 + $1,359,750

*Equivalent units to complete beginning work in process from Solution Exhibit 17-34A, Step 2.

†Equivalent units started and completed from Solution Exhibit 17-34A, Step 2.

#Equivalent units in ending work in process from Solution Exhibit 17-34A, Step 2.

4.

Direct Materials

17-35 Equivalent units, comprehensive. Louisville Sports manufactures baseball bats for use by players in the major leagues. A

critical requirement for elite players is that each bat they use have an identical look and feel. As a result, Louisville uses a dedicated

process to produce bats to each player’s specifications.

One of Louisville’s key clients is Ryan Brown of the Green Bay Brewers. Producing his bat involves the use of three materials—

ash, cork, and ink—and a sequence of 20 standardized steps. Materials are added as follows:

Ash: This is the basic wood used in bats. Eighty percent of the ash content is added at the start of the process; the rest is added at

the start of the 16th step of the process.

Cork: This is inserted into the bat in order to increase Ryan’s bat speed. Half of the cork is introduced at the beginning of the

seventh step of the process; the rest is added at the beginning of the 14th step.

Ink: This is used to stamp Ryan’s name on the finished bat and is added at the end of the process.

Of the total conversion costs, 6% are added during each of the first 10 steps of the process, and 4% are added at each of the remaining

10 steps.

On May 1, 2017, Louisville had 100 bats in inventory. These bats had completed the ninth step of the process as of April 30, 2017.

During May, Louisville put another 60 bats into production. At the end of May, Louisville was left with 40 bats that had completed the

12th step of the production process.

Required:

1. Under the weighted-average method of process costing, compute equivalent units of work done for each relevant input for the

month of May.

2. Under the FIFO method of process costing, compute equivalent units of work done for each relevant input for the month of May.

SOLUTION

(30 min.) Equivalent units, comprehensive.

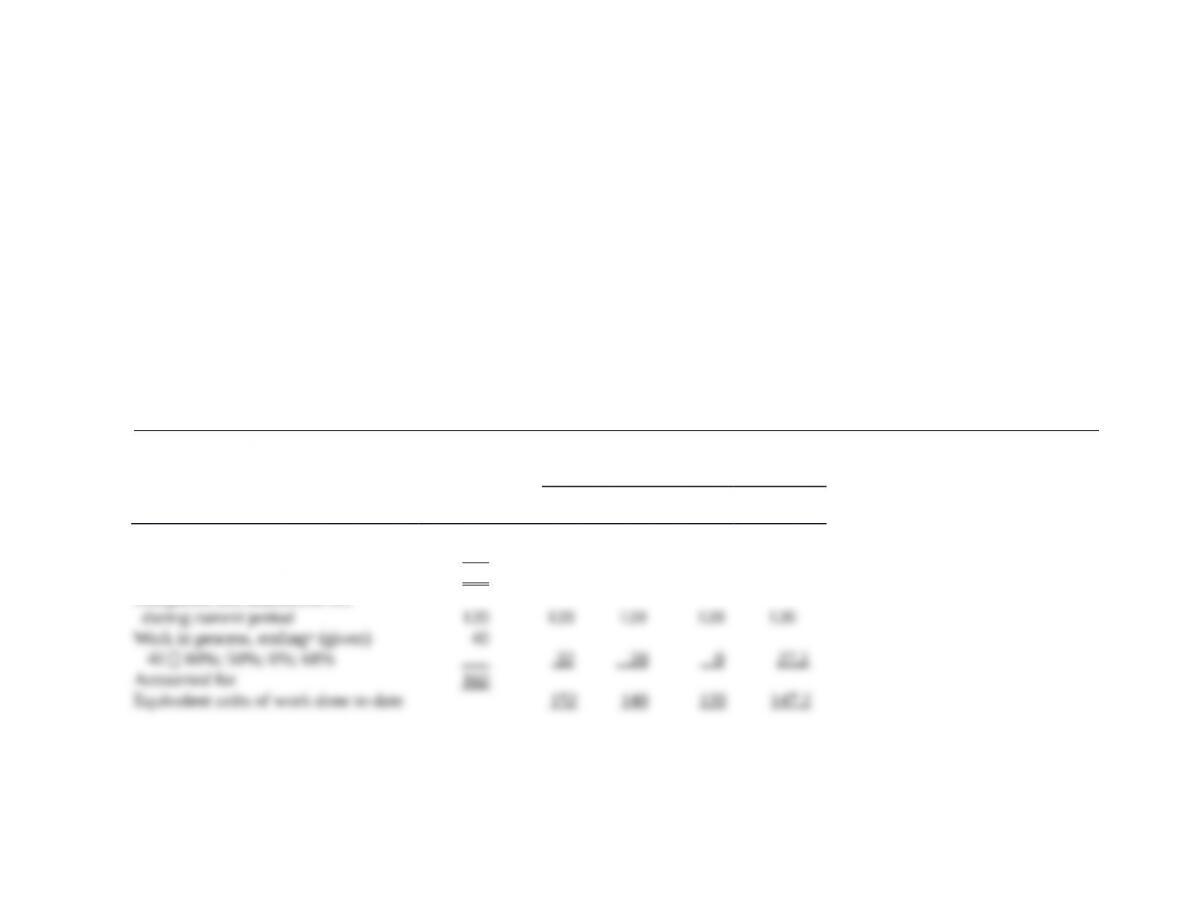

1.

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

Weighted-Average Method of Process Costing,

Louisville Sports for May 2017.

(Step 1) (Step 2)

Equivalent Units

Flow of Production

Physical

Units

Ash Cork Ink Conversion

Costs

Work in process, beginning (given) 100

Started during current period (given) 60

To account for 160

Completed and transferred out

*Degree of completion in this department: Step 12 of production process: Ash, 80%; Cork, 50%; Ink, 0%; Conversion costs, (6% × 10 steps) + (4% × 2 steps) =

68%.

2.

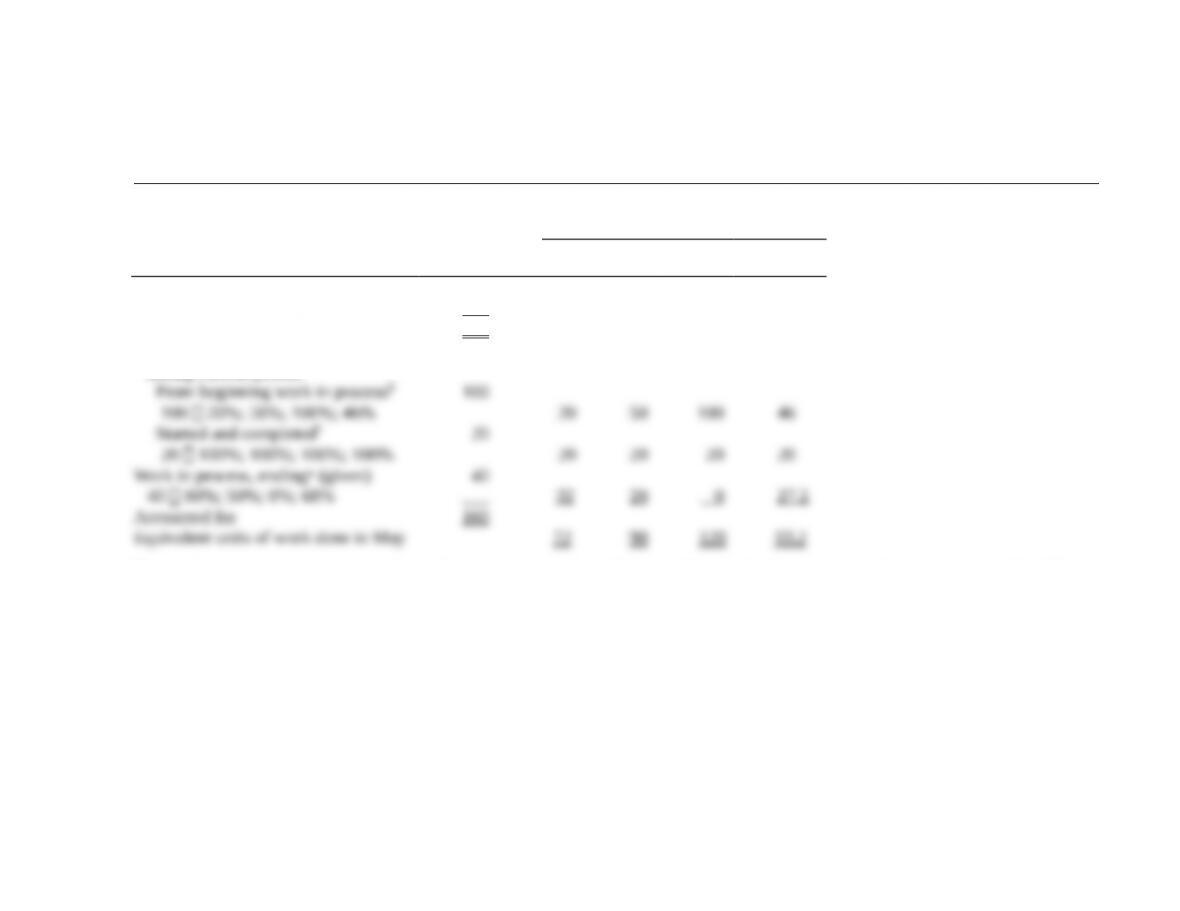

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

FIFO Method of Process Costing,

Louisville Sports for May 2017.

(Step 1) (Step 2)

Equivalent Units

Flow of Production

Physical

Units

Ash Cork Ink Conversion

Costs

Work in process, beginning (given) 100

Started during current period (given) 60

To account for 160

Completed and transferred out

during current period:

§Degree of completion in this department: Step 9 of production process: Ash, 80%; Cork, 50%; Ink, 0%; Conversion costs, 6% × 9 steps = 54%. The difference

between 100% and these numbers represents the amount of work done to complete the beginning work in process in this period.

†120 bats completed and transferred out minus 100 bats completed and transferred out from beginning work-in-process inventory.

*Degree of completion in this department: Step 12 of production process: Ash, 80%; Cork, 50%; Ink, 0%; Conversion costs, (6% × 10 steps) + (4% × 2 steps) =

68%.

17-36 Weighted-average method. Hoffman Company manufactures car seats in its Boise plant. Each car seat passes through the

assembly department and the testing department. This problem focuses on the assembly department. The process-costing system at

Hoffman Company has a single direct-cost category (direct materials) and a single indirect-cost category (conversion materials are

added at the costs). Direct beginning of the process. Conversion costs are added evenly during the process. When the assembly

department finishes work on each car seat, it is immediately transferred to testing.

Hoffman Company uses the weighted-average method of process costing. Data for the assembly department for October 2017 are

as follows:

Physical Units

(Car Seats)

Direct

Materials

Conversion

Costs

Work in process, October 1a4,000 $1,248,000 $ 241,650

Started during October 2017 22,500

Completed during October 2017 26,000

Work in process, October 31b500

Total costs added during October

2017

$4,635,000 $2,575,125

aDegree of completion: direct materials,?%; conversion costs, 45%.

bDegree of completion: direct materials,?%; conversion costs, 65%.

Required:

1. For each cost category, compute equivalent units in the assembly department. Show physical units in the first column of your

schedule.

2. What issues should the manager focus on when reviewing the equivalent-unit calculations?

3. For each cost category, summarize total assembly department costs for October 2017 and calculate the cost per equivalent unit.

4. Assign costs to units completed and transferred out and to units in ending work in process.

SOLUTION

(25 min.) Weighted-average method.

1. Since direct materials are added at the beginning of the assembly process, the units in this department must be 100% complete

with respect to direct materials. Solution Exhibit 17-36A shows equivalent units of work done to date:

SOLUTION EXHIBIT 17-36A

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

Weighted-Average Method of Process Costing,

Assembly Department of Hoffman Company for October 2017.

(Step 1) (Step 2)

Equivalent Units

Physical Direct Conversion

Flow of Production Units Materials Costs

*Degree of completion in this department: direct materials, 100% (since they are added at the start of the process); conversion costs, 65%.

2. To show better performance, a department supervisor might report a higher degree of completion resulting in

understated cost per equivalent unit and overstated operating income. If performance for the period is very good, the department

To guard against the possibility of bias, managers should ask supervisors specific questions about the process they

3. & 4. Solution Exhibit 17-36B summarizes the total Assembly Department costs for October 2017, calculates cost per equivalent unit

of work done to date, and assigns these costs to units completed (and transferred out) and to units in ending work in process using the

weighted-average method.

SOLUTION EXHIBIT 17-36B

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign Costs to the Units Completed and Units

in Ending Work in Process Inventory;

Weighted-Average Method of Process Costing,

Assembly Department of Hoffman Company for October 2017.

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given) $1,489,650 $1,248,000 $ 241,650

Costs added in current period (given) 7 ,210,125 4 ,635 ,000 2 ,575,125

*Equivalent units completed and transferred out from Solution Exhibit 17-36A, Step 2.

†Equivalent units in work in process, ending from Solution Exhibit 17-36A, Step 2.

17-37 Journal entries (continuation of 17-36).

Required:

Prepare a set of summarized journal entries for all October 2017 transactions affecting Work in Process—Assembly. Set up a

T-account for Work in Process—Assembly and post your entries to it.