Differential revenue is the difference in total revenue between two alternatives.

Costs in beginning inventory are pooled with costs in the current period when

determining the costs of good units under the weighted-average method of process

costing.

If the incremental users are newly formed companies or subunits, the incremental

method may decrease their chances for short-run survival by assigning them a high

allocation of the common costs.

Sunk costs are irrelevant to decision making.

Developing a product that satisfies the need of the potential customers is the first step in

implementing target pricing and target costing.

Direct costs of a cost object are costs related to a particular cost object that can be

allocated to that cost object in an economically feasible (cost-effective) way.

To convert the operating income for an overseas branch into US dollars, the historical

rate of exchange is used for its conversion into US dollars.

In a period of rising prices, the weighted-average method will result in higher tax

payments.

Variable cost per unit is the best product cost to use for one-time-only special order

decisions.

Customer life-cycle costs focus on the total costs incurred by a customer to acquire,

use, maintain, and dispose of a product or service.

The human resources systems is a part of the formal management control systems of an

organization.

A fixed cost remains unchanged in total for a given time period, despite wide changes

in the related level

of total activity or volume of output produced.

All other things being equal, the longer the time horizon the more likely a cost will be

fixed.

The level 3 components for the fixed overhead variance are the fixed overhead

spending variance and the fixed overhead production volume variance.

A full-cost formula for pricing does not require the management accountant to perform

a detailed analysis of cost-behavior patterns.

Control comprises taking actions that implement the planning decisions, evaluating past

performance, and providing feedback and learning to help future decision making.

From the perspective of control, the direct materials price variance should be isolated at

the time of sales.

In a decision as to whether or not to drop a product, fixed costs that have been allocated

to that product are generally not relevant unless there is a savings of fixed costs as a

result of dropping the product.

All costs are locked in at the design stage itself.

The ending balance in Work-in-Process Control represents the total costs of all jobs that

have NOT yet been completed.

The weighted-average cost is the total of all costs entering the Work-in-Process account

(whether they are from beginning work-in-process or from work started during the

current period) divided by total equivalent units of work done to date.

The sales value at split-off method presupposes the exact number of subsequent steps

undertaken for further processing.

Before the split-off point, decisions relating to the sale or further processing of each

identifiable product cannot be made independently of decisions about the other

products.

A fixed cost is fixed only in relation to a given wide range of total activity or volume

and only for a given

time span, usually a particular budget period.

Transferred-in costs are costs incurred in previous departments that are carried forward

as the product’s cost when it moves to a subsequent process in the production cycle.

Outsourcing is risk free to the manufacturer because the supplier now has the

responsibility of producing the part.

Transferred-in costs are treated as if they are 100 percent complete at the beginning of

the process in the new department.

The proponents of using net book value as an investment base maintain that it is less

confusing because it is consistent with the amount of total assets shown in the

conventional balance sheet.

Environmental costs that are incurred over several years of the product’s life cycle are

often locked in at the product- and process-design stage.

Managers who utilize customer profitability charts should drop customers that generate

a negative customer operating income, since dropping an unprofitable customer will

automatically cause overall income to increase.

Full costs of a product include variable and fixed costs in a particular business function

in the value

chain.

Selling prices computed under cost-plus pricing are prospective prices that may or may

not actually be charged to customers.

All manufacturing costs are period costs.

If one of five distribution channels is discontinued, corporate-sustaining costs such as

general administration costs will most likely be reduced by 20%.

To simplify calculations under FIFO, spoiled units are accounted for as if they were

started in the current period.

An effective plan for variable overhead costs will eliminate activities that do not add

value.

One of the most direct financial measures of quality is the costs of quality.

The IBP Grocery orders most of its items in lot sizes of 10 units. Average annual

demand per side of beef is 720 units per year. Ordering costs are $25 per order with an

average purchasing price of $100. Annual inventory carrying costs are estimated to be

40% of the unit cost.

Required:

a. Determine the economic order quantity.

b. Determine the annual cost savings if the shop changes from an order size of 10 units

to the economic order quantity.

c. Since the shelf life is limited, the IBP Grocery must keep the inventory moving.

Assuming a 360-day year, determine the optimal lot size under each of the following:

(1) a 20-day shelf life and (2) a 10-day shelf life.

Producing on schedule, quality of supplier products or services, reliability, along with

costs are all important considerations when____

A) when deciding to insource

B) making outsourcing decisions

C) when executing right-shoring

D) making decisions based on quantitative factors

Jupiter Corporation incurred fixed manufacturing costs of $16,000 during 2017. Other

information for 2017 includes:

The budgeted denominator level is 2,300 units.

Units produced total 2,600 units.

Units sold total 1,600 units.

Variable cost per unit is $4

Beginning inventory is zero.

The fixed manufacturing cost rate is based on the budgeted denominator level.

Under variable costing, the fixed manufacturing costs expensed on the income

statement (excluding adjustments for variances) total ________.

A) $16,000

B) $11,130

C) $21,530

D) $0

Dropping an unprofitable customer will ________.

A) eliminate long-run costs assigned to that customer

B) eliminate most short-run costs assigned to that customer

C) decrease long-run profitability

D) increase the potential to cross-sell other products that are more desirable

The spreading of underallocated or overallocated overhead among ending

work-in-process, finished goods, and cost of goods sold is called ________.

A) the adjusted allocation rate approach

B) the proration approach

C) the write-off of cost of goods sold approach

D) the weighted-average cost approach

AAA Manufacturing Inc, makes a product with the following costs per unit:

Direct materials $180

Direct labor $20

Manufacturing overhead (variable) $30

Manufacturing overhead (fixed) $130

Marketing costs $75

What would be the inventoriable cost per unit under variable costing and what would it

be under absorption costing?

A) $180 for variable costing and $305 under absorption costing

B) $230 for variable costing and $305 under absorption costing

C) $230 for variable costing and $360 under absorption costing

D) $200 for variable costing and $305 under absorption costing

If a company would like to increase its degree of operating leverage it should

________.

A) increase its sales relative to its fixed costs

B) increase its sales relative to its variable costs

C) increase its variable costs relative to its fixed costs

D) increase its fixed costs relative to its variable costs

Job costing ________.

A) cannot be used by the service industry

B) records the flow of costs for each product or service

C) allocates an equal amount of cost to each unit made during a time period

D) is used when each unit of output is identical

Successful implementation of a product differentiation strategy will result in ________.

A) a large favorable growth and price-recovery components

B) a large favorable price-recovery and productivity components

C) a large favorable productivity and growth components

D) only a large favorable growth component

The flexible-budget variance for materials is $2,000 (U). The sales-volume variance is

$18,000 (U). The price variance for material is $38,000 (F). The efficiency variance for

direct manufacturing labor is $12,000 (F). Calculate the efficiency variance for

materials.

A) $40,000 favorable

B) $18,000 unfavorable

C) $6,000 favorable

D) $40,000 unfavorable

Which of the following is an assumption under FIFO process-costing method?

A) It assumes some of the higher-cost units are placed in ending work in process.

B) It assumes that all the lower-cost units from the previous period in beginning work

in process are the first to be completed and transferred out of the process.

C) It assumes that unit inputs costs are constant and do not fluctuate in the short run.

D) It assumes that the ending work in process consists of only the lower-cost

current-period units.

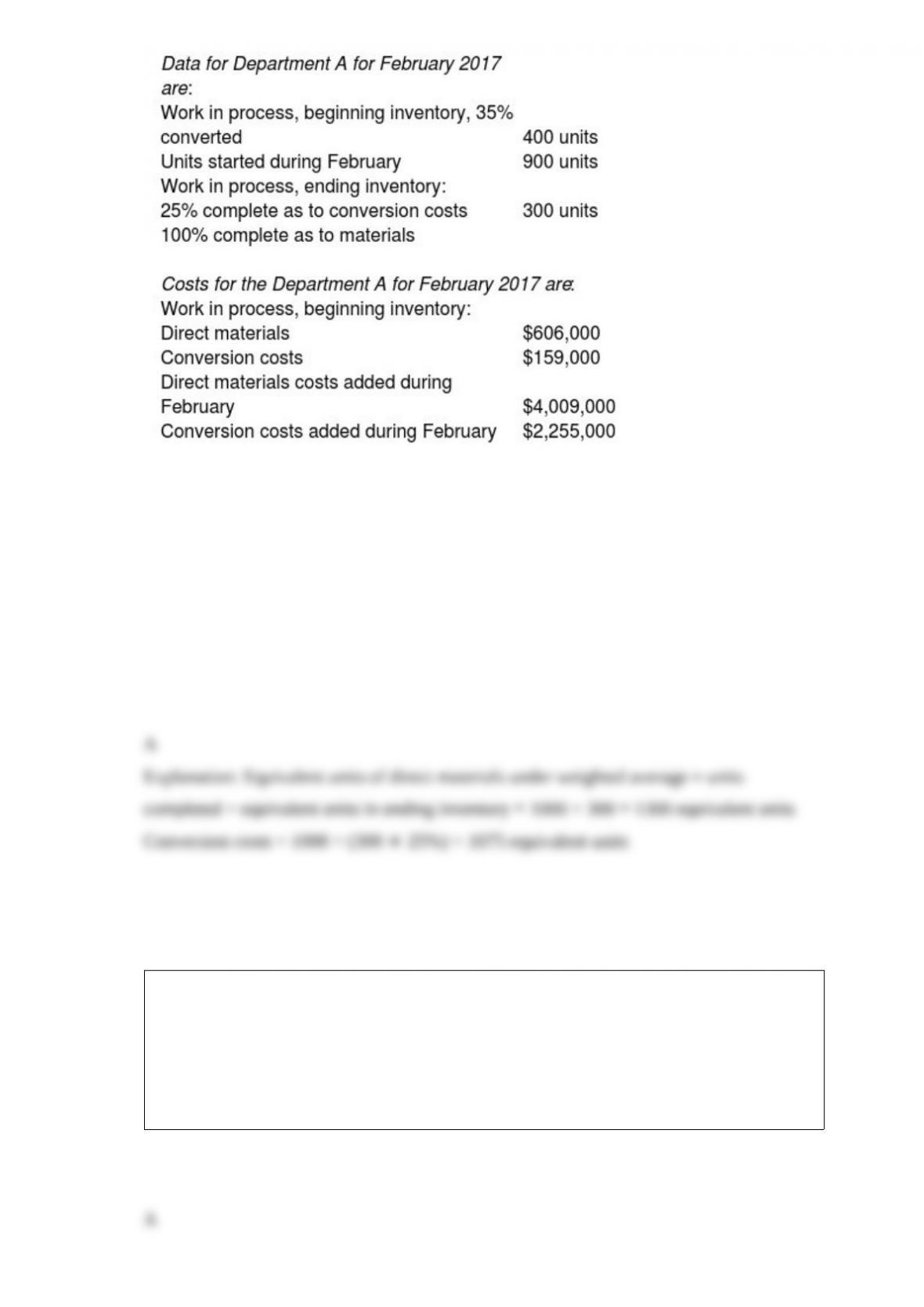

Audrey Auto Accessories manufactures plastic moldings for car seats. Its costing

system uses two cost categories, direct materials and conversion costs. Each product

must pass through Department A and Department B. Direct materials are added at the

beginning of production. Conversion costs are allocated evenly throughout production.

What were the equivalent units of direct materials and conversion costs, respectively, at the

end of February? Assume Audrey uses the weighted-average process costing method.

A) 1300; 1075

B) 1300; 1300

C) 1300; 1000

D) 900; 600

________ occurs when a decision’s benefits for one subunit is more than offset by the

costs to the organization as a whole.

A) Suboptimal decision making

B) Independent decision making

C) Congruent decision making

D) Departmental decision making

The operating budget process generally concludes with the preparation of the

________.

A) production budget

B) cash flow statement

C) balance sheet

D) budgeted income statement

The reason to have a post-investment audit is ________.

A) they encourage mid-level managers to make overly optimistic estimates during the

early stages of the capital budgeting process

B) they help alert senior management to problems in the implementation of projects

C) they analyze by calculating contribution-margin

D) they help in calculating present value

If a company has a degree of operating leverage of 5 and sales increase by 30%, then

________.

A) total fixed costs will increase by 150%

B) total costs will increase by 150%

C) profit will increase by 120%

D) profit will increase by 150%

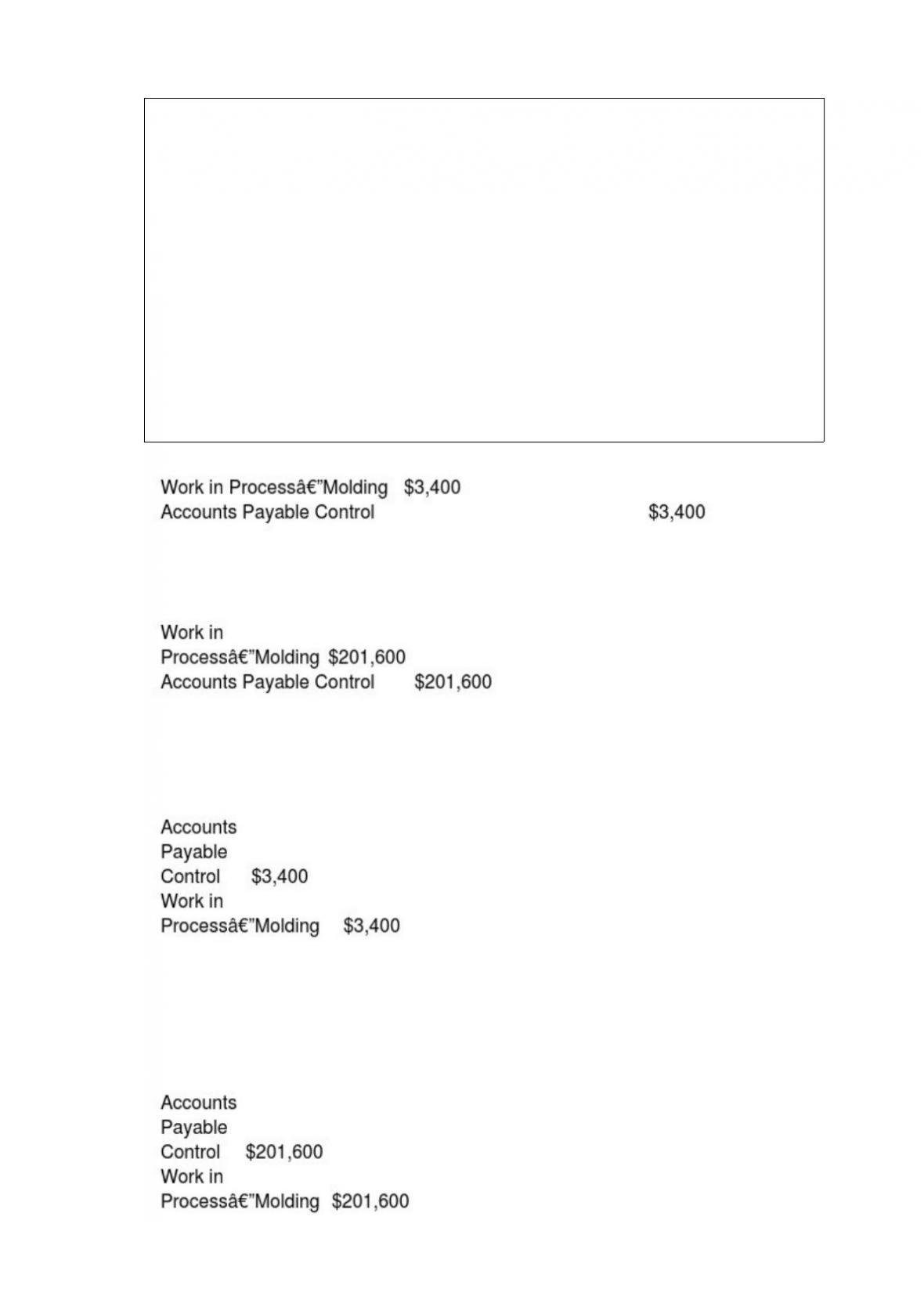

Stefan Ceramics is in the business of selling ceramic vases. It has two departments –

molding and finishing. Molding department purchases tungsten carbide and produces

ceramic vases out of it. Ceramic Vases are then transferred to finishing department,

which designs it as per the requirement of the customers.

During the month of July, molding department purchased 720 kgs of tungsten carbide at

$280 per kg. It started manufacture of 4200 vases and completed and transferred 3800

vases during the month. It has 400 vases in the process at the end of the month. It

incurred direct labor charges of $1500 and other manufacturing costs of $1300, which

included electricity costs of $300. Stefan had no inventory of tungsten carbide at the

end of the month. It also had no beginning inventory of vases. The ending inventory

was 50% complete in respect of conversion costs.

Which of the following journal entry would record the tungsten carbide purchased and

used in production during July?

A)

B)

C)

D) Accounts Payable Control $201,600

Work in Process—Molding $201,600

Sales of Blistre Autos are 380,000, variable cost is 230,000, fixed cost is 90,000 tax rate

is 40%. Calculate the operating leverage of the company.

A) 1.50 times

B) 4.17 times

C) 1.53 times

D) 2.50 times

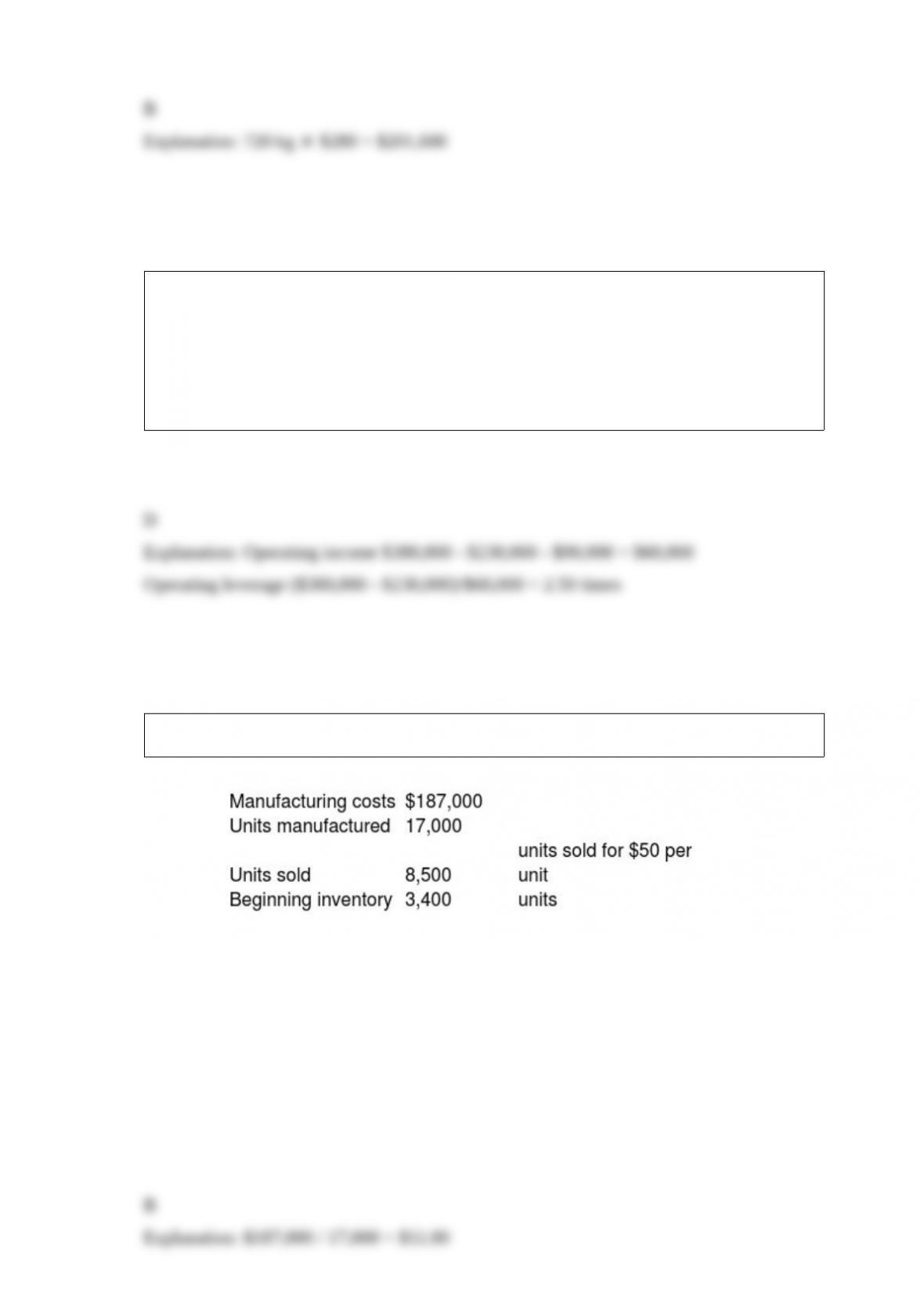

Pederson Company reported the following:

What is the average manufacturing cost per unit?

A) $11.20

B) $11.00

C) $22.00

D) $22.40

Segmenting customers as a result of customer profitability analysis would be done by

which of the following groupings?

A) geography such as state or by zip code

B) operating income

C) gross margin

D) total direct costs

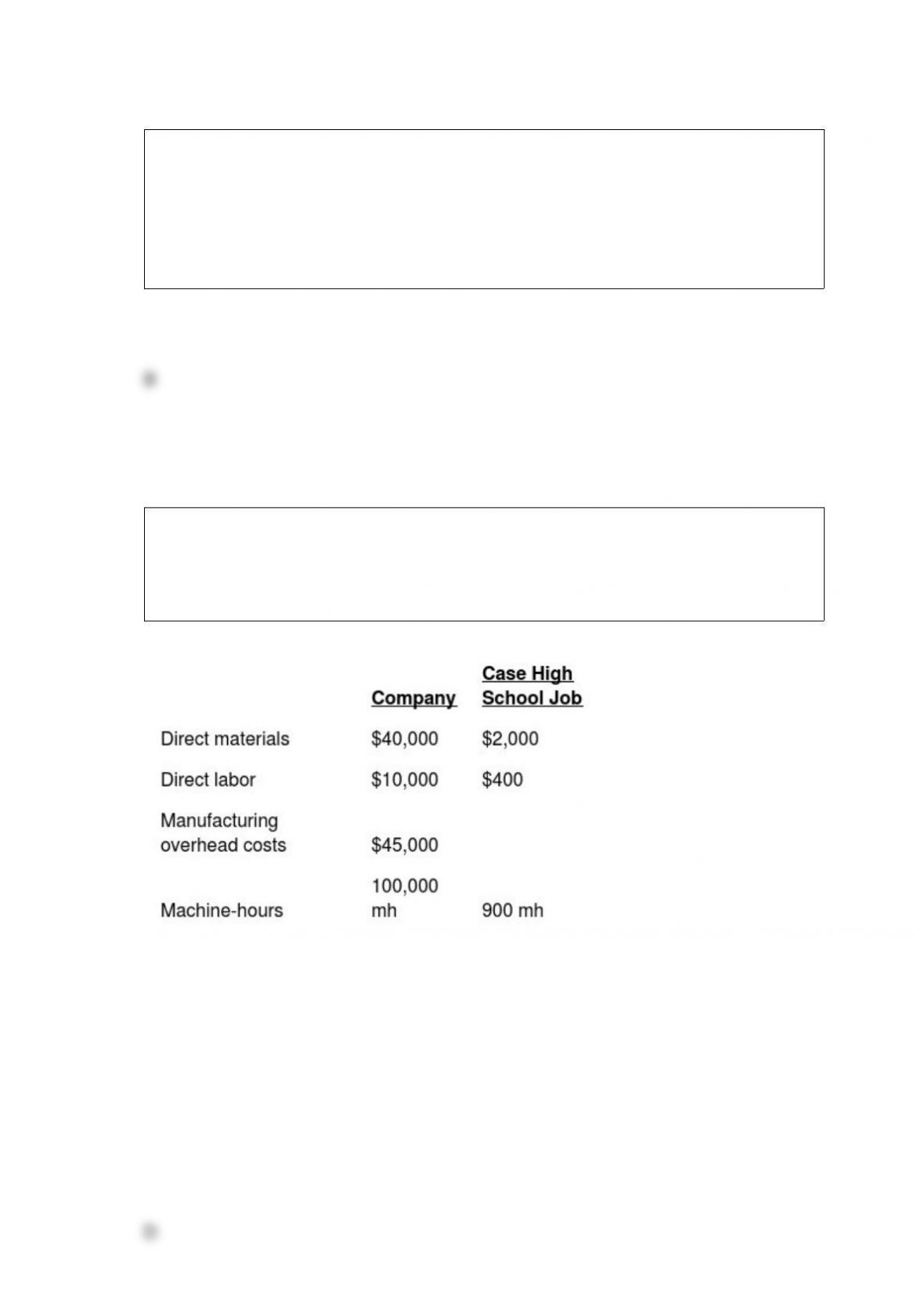

Lancelot Manufacturing is a small textile manufacturer using machine-hours as the

single indirect-cost rate to allocate manufacturing overhead costs to the various jobs

contracted during the year. The following estimates are provided for the coming year

for the company and for the Case High School band jacket job.

What is the bid price for the Case High School job if the company uses a 40% markup of

total manufacturing costs?

A) $3,360

B) $1,122

C) $960

D) $3,927

Which of the following steps in designing an accounting-based performance measure

includes decisions such as defining assets as total assets or net assets in the calculation

of return on assets?

A) choosing performance measures that align with top management’s financial goals

B) choosing the time horizon of each performance measure

C) choosing the details for each performance measure

D) choosing a target level of performance

The Standards of Ethical Conduct for management accountants include concepts related

to ________.

A) competence, performance, diligence, and reporting

B) competence, confidentiality, integrity, and credibility

C) experience, diligence, reporting, and objectivity

D) diligence, objectivity, conflicts of interest, and credibility

In the service sector ________.

A) direct labor costs are always easy to trace to jobs

B) a budgeted direct-labor cost rate may be used to apply direct labor to jobs

C) normal costing may not be used

D) overhead is generally applied using an actual cost-allocation rate

Diemia Hospital has been considering the purchase of a new x-ray machine. The

existing machine is operable for three more years and will have a zero disposal price. If

the machine is disposed now, it may be sold for $170,000. The new machine will cost

$700,000 and an additional cash investment in working capital of $115,000 will be

required. The new machine will reduce the average amount of time required to take the

x-rays and will allow an additional amount of business to be done at the hospital. The

investment is expected to net $150,000 in additional cash inflows during the year of

acquisition and $180,000 each additional year of use. The new machine has a three-year

life, and zero disposal value. These cash flows will generally occur throughout the year

and are recognized at the end of each year. Income taxes are not considered in this

problem. The working capital investment will not be recovered at the end of the asset’s

life.

What is the net present value of the investment, assuming the required rate of return is

9%? Would the hospital want to purchase the new machine?

A) $(27,510); no

B) $117,000 no

C) $27,510; yes

D) $117,000; yes

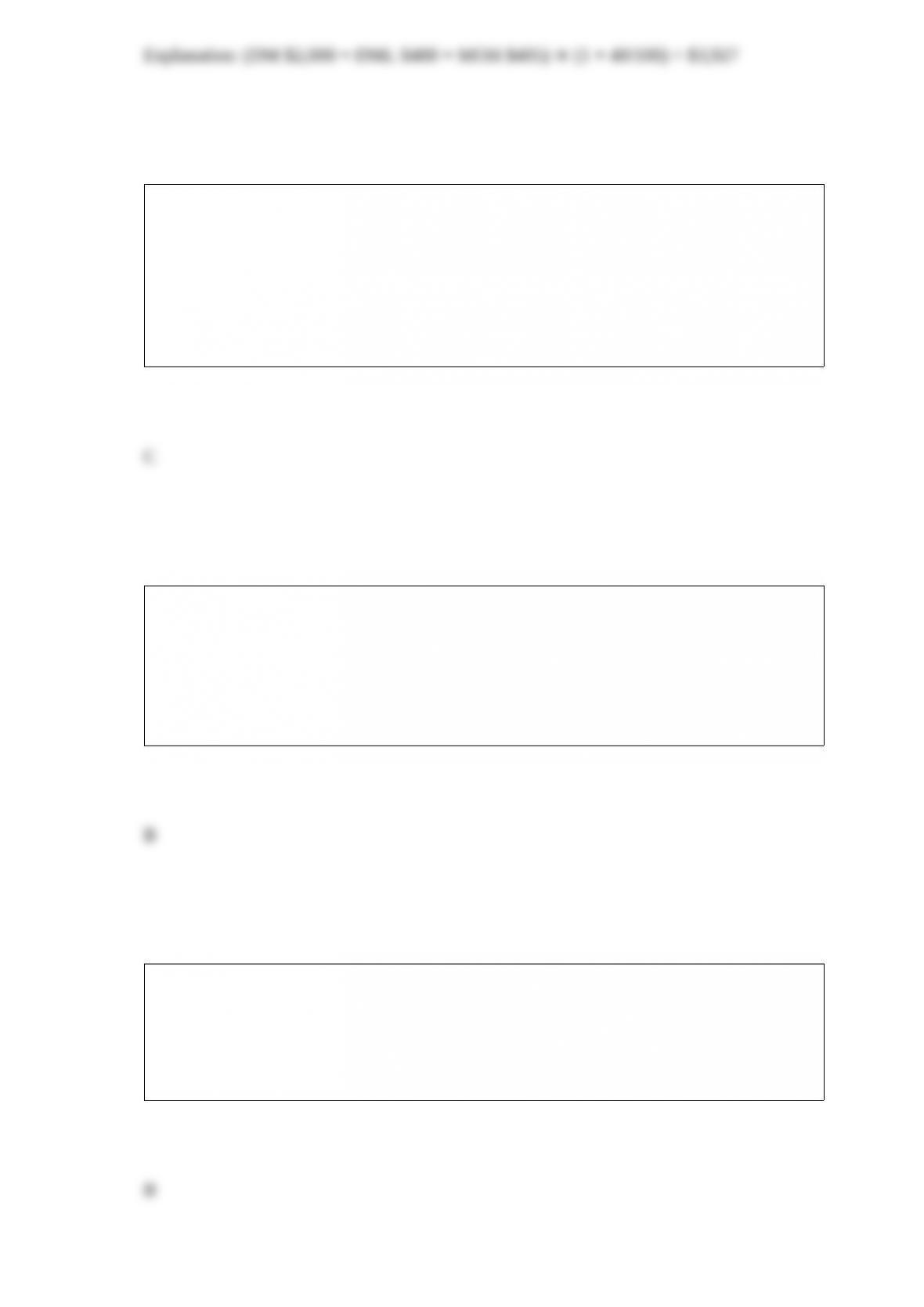

Bristol Fabricators, Inc., produces air purifiers in batches. To manufacture a batch of the

purifiers, Bristol Fabricators, Inc., must set up the machines and assembly line tooling.

Setup costs are batch-level costs because they are associated with batches rather than

individual units of products. A separate Setup Department is responsible for setting up

machines and tooling for different models of the air purifiers.

Setup overhead costs consist of some costs that are variable and some costs that are

fixed with respect to the number of setup-hours. The following information pertains to

June 2015:

Calculate the production-volume variance for fixed overhead setup costs. (Round all

intermediary calculations to two decimal places and your final answer to the nearest whole

number.)

A) $2,832 favorable

B) $2,832 unfavorable

C) $363 unfavorable

D) $363 favorable

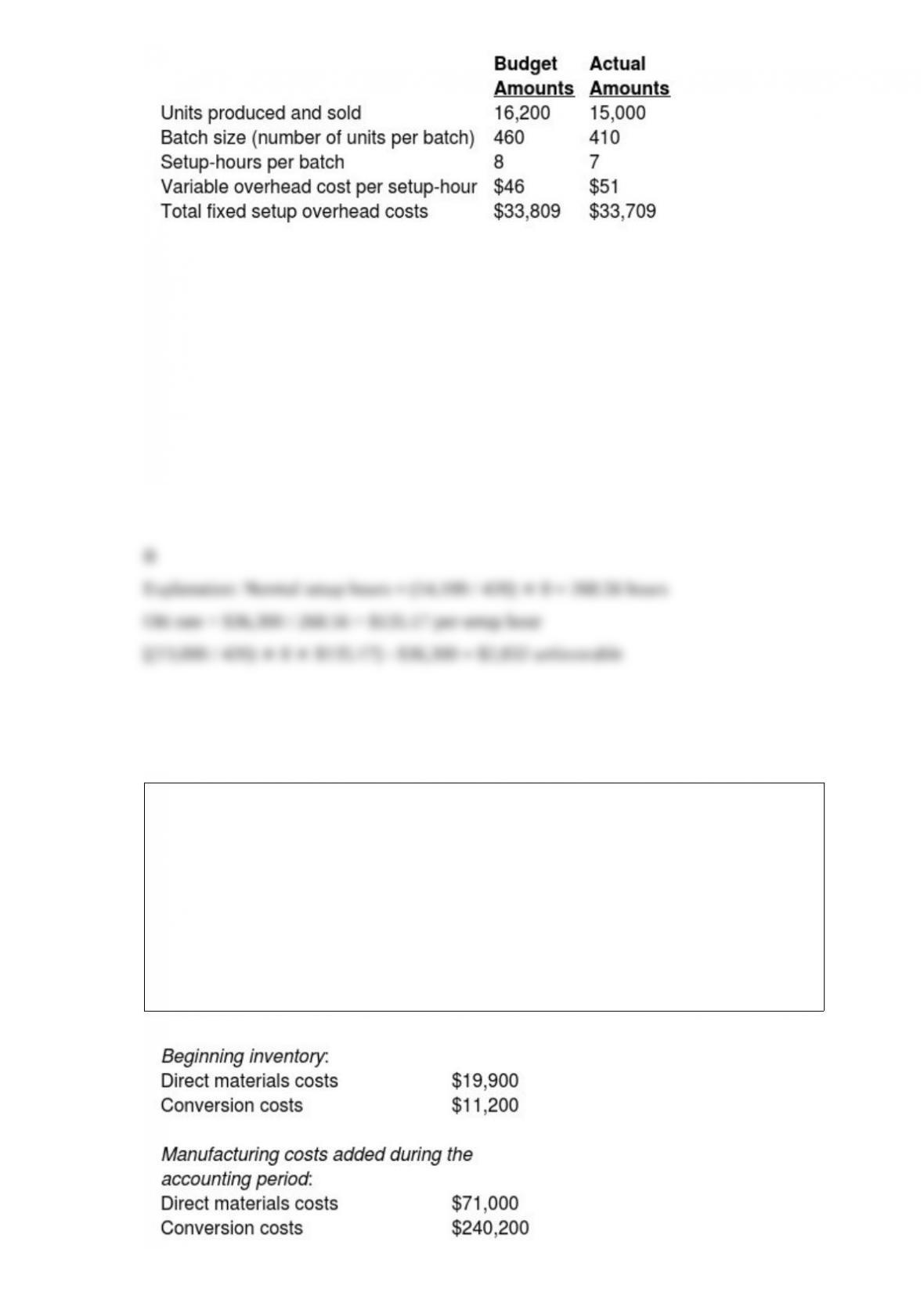

Jane Industries manufactures plastic toys. During October, Jane’s Fabrication

Department started work on 10,000 models. During the month, the company completed

11,300 models, and transferred them to the Distribution Department. The company

ended the month with 2000 models in ending inventory. There were 3300 models in

beginning inventory. All direct materials costs are added at the beginning of the

production cycle and conversion costs are added uniformly throughout the production

process. The FIFO method of process costing is being followed. Beginning work in

process was 30% complete as to conversion costs, while ending work in process was

55% complete as to conversion costs.

What were the equivalent units for conversion costs during October?

A) 10,400

B) 11,900

C) 11,410

D) 9000

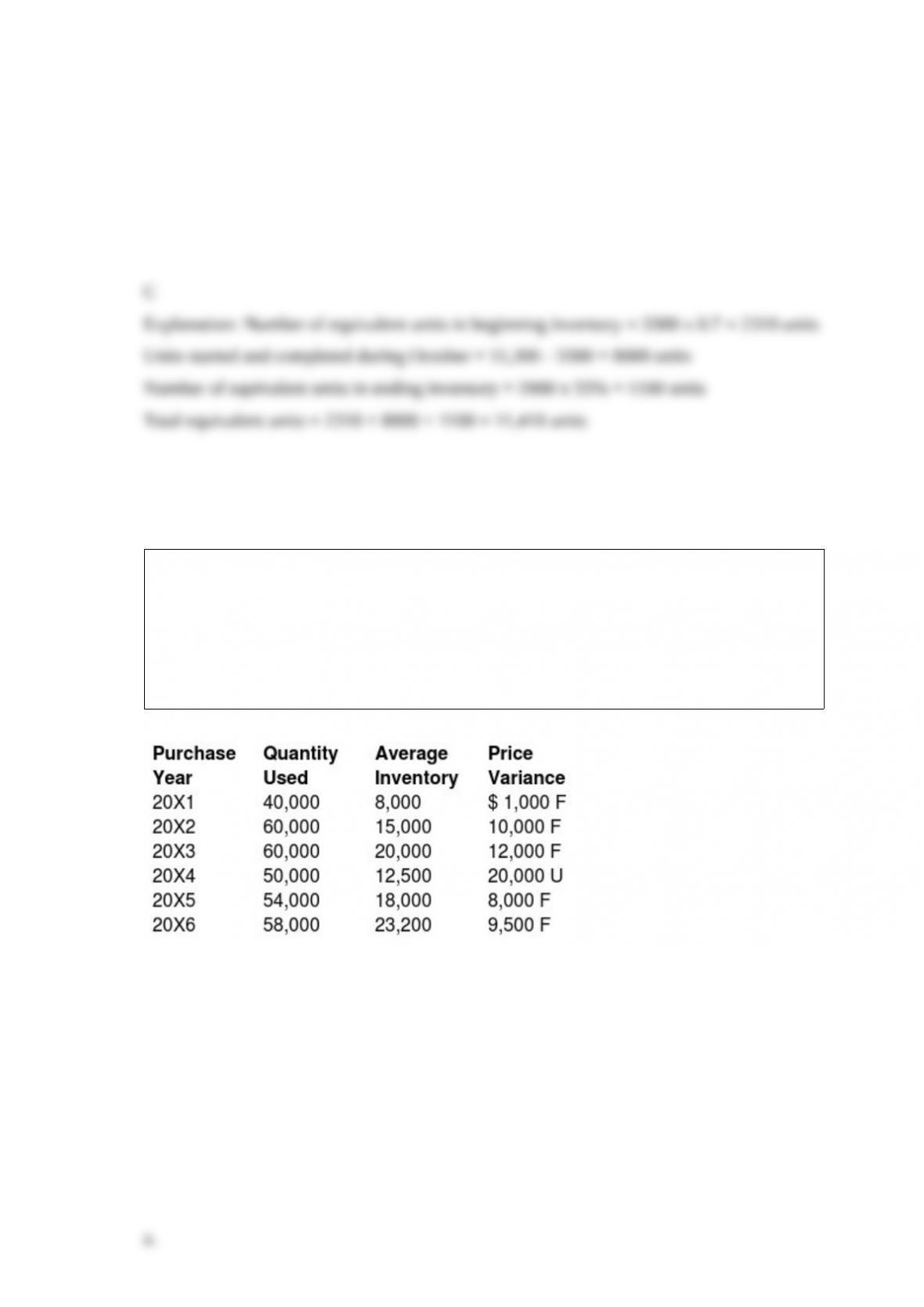

Kretzinger Company makes extensive use of financial performance reports for each of

its departments. Although most departments have been reporting favorable cost

variances with the company’s current inventory system, management is concerned about

the overall performance of the purchasing department. For example, the following

information is for the purchasing of materials for a product the company has been

manufacturing for several years:

Required:

a. Compute the inventory turnover for each year. Can any conclusions be drawn for a

yearly comparison of the purchase price variance and the inventory turnover?

b. Identify problems likely to be caused by evaluating purchasing only on the basis of the

purchase price variance.

c. What recommendations will improve the evaluation process?

In 2017, Commodity Inc., processor of whole grain flour, had the capacity to produce

10,000,000 pounds of product at a conversion cost per pound of $0.20. The conversion

cost per pound was $0.15 in 2016 (the previous year). The direct material cost per

pound for both years was $0.07 per pound and in 2017, Commodity Inc. produced

9,300,000 pounds while actual production for the previous year was 8,600,000 pounds.

What was the cost of unused capacity in 2017?

A) $280,000

B) $140,000

C) $105,000

D) $210,000

For each of the following activities, characteristics, and applications, identify whether

they can be found in a centralized organization, a decentralized organization, or both

types of organizations.

________ a. Freedom for managers at lower organizational levels to make decisions

________ b. Gathering information may be very expensive

________ c. Greater responsiveness to user needs

________ d. Have few interdependencies among divisions

________ e. Maximum constraints and minimum freedom for managers at lowest levels

________ f. Maximization of benefits over costs

________ g. Minimization of duplicate functions

________ h. Minimum of suboptimization

________ i. Multiple responsibility centers with various reporting units

________ j. Profit centers

Customers expect to pay a price that includes ________.

A) the cost of unused capacity

B) only the cost of actual capacity used

C) variable costs but not capacity costs

D) the cost of direct materials, direct labor, and fixed overhead

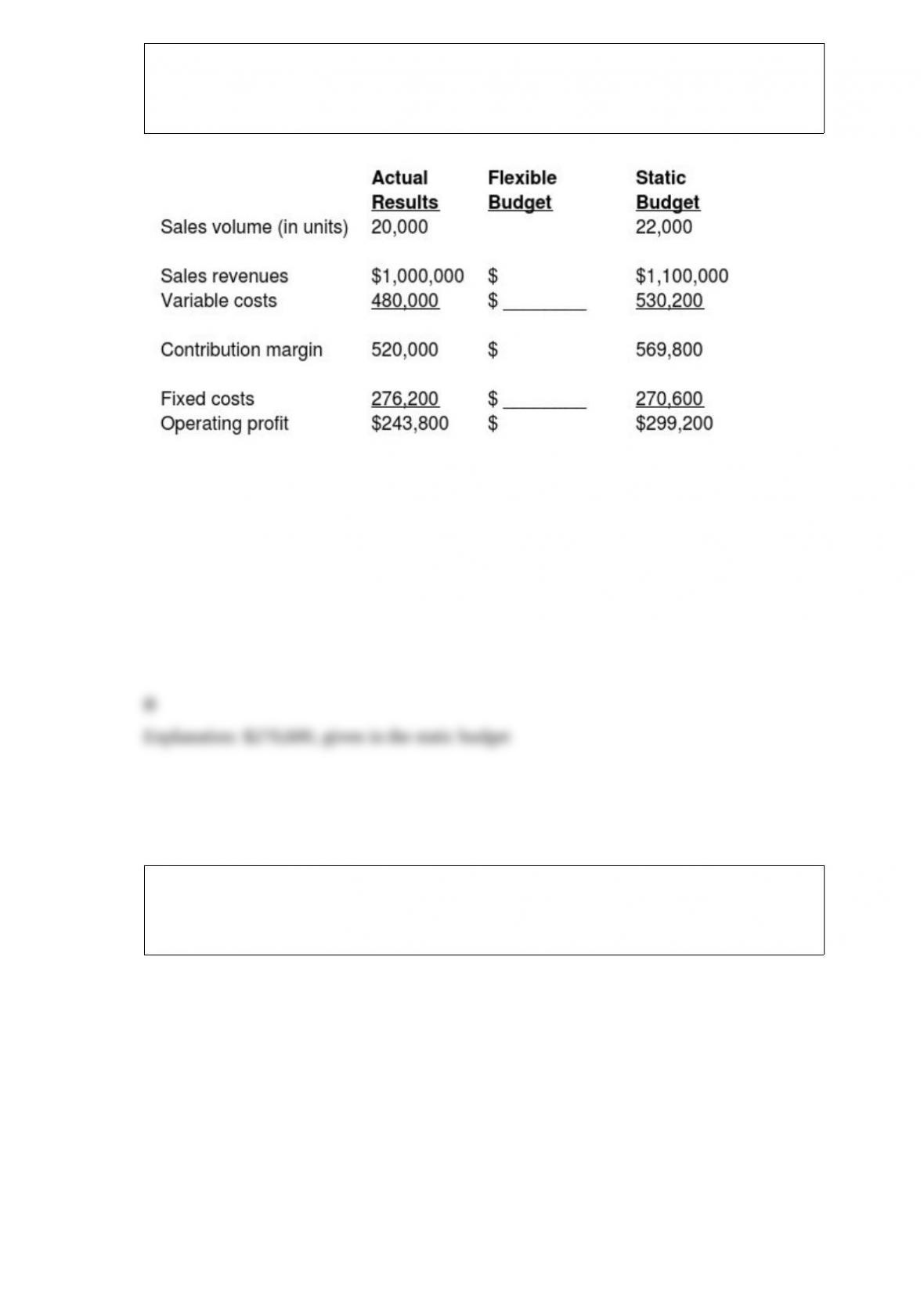

The actual information pertains to the month of June. As a part of the budgeting

process, Great Cabinets Company developed the following static budget for June. Great

Cabinets is in the process of preparing the flexible budget and understanding the results.

The flexible budget will report ________ for the fixed costs.

A) $303,820

B) $270,600

C) $530,200

D) $246,000

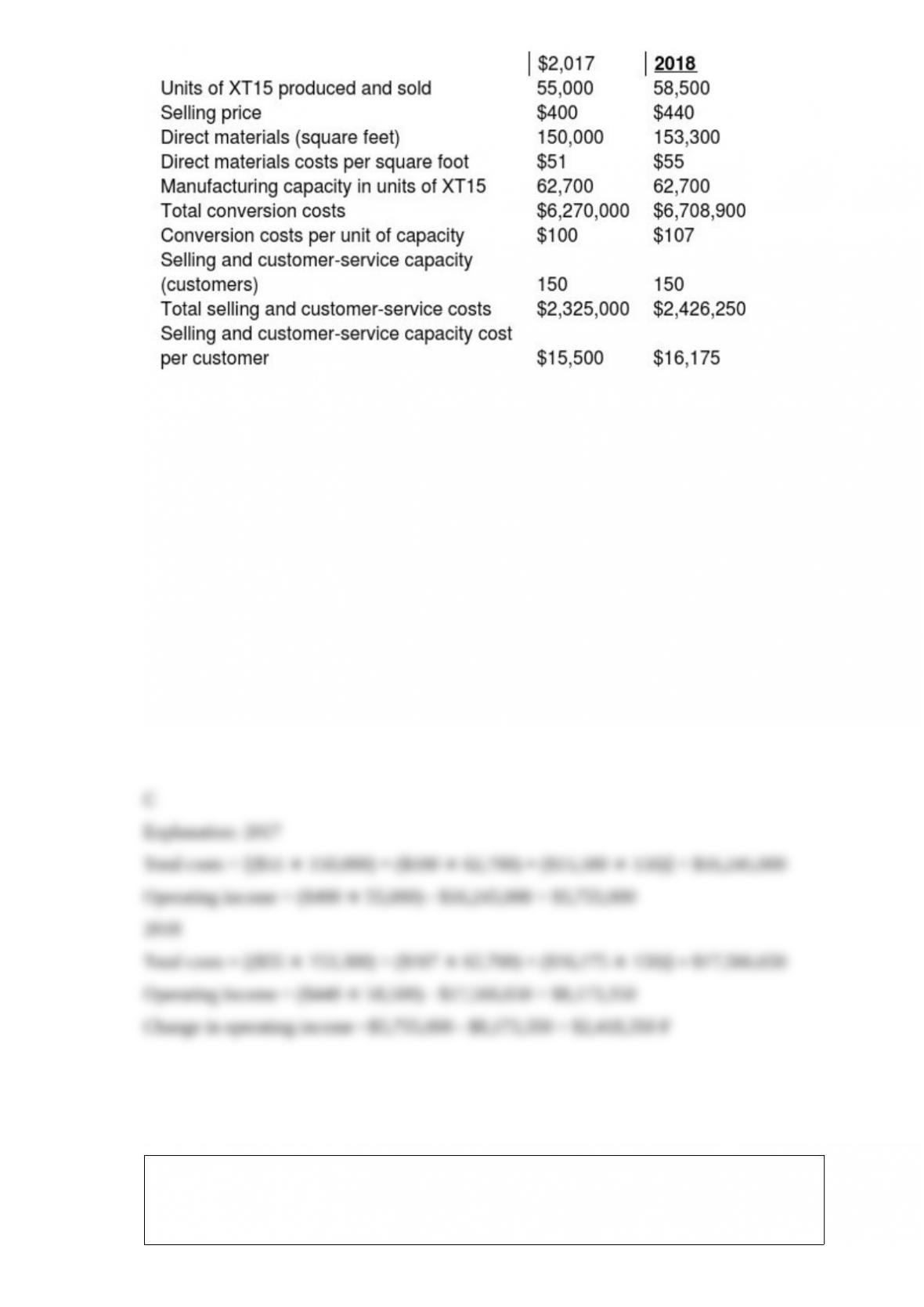

Following a strategy of product differentiation, Izzy’s Limited Company makes a

high-end Appliance, XT15. Izzy’s Limited presents the following data for the years

2017 and 2018:

Izzy’s Limited produces no defective units but it wants to reduce direct materials usage per

unit of XT15. Manufacturing conversion costs in each year depend on production capacity

defined in terms of XT15 units that can be produced. Selling and customer-service costs

depend on the number of customers that the customer and service functions are designed to

support. Izzy’s Limited had 135 customers in 2017 and 140 customers in 2018.

What is the change in operating income from 2017 to 2018?

A) $2,418,350 U

B) $3,740,000 F

C) $2,418,350 F

D) $3,740,000 U

The last step of the five-step decision making process is implementing the decision,

evaluating performance, and learning. How can a balanced scorecard play a role in

helping to assure this final step will be successful?

Rally Company manufactures garage storage systems for homeowners. It uses a normal

costing system with two direct cost categories – direct materials and direct labor – an

one indirect-cost pool, manufacturing overhead costs.

For 2018:

Budgeted manufacturing overhead costs $1,000,000

Budgeted manufacturing labor-hours 20,000 hours

Actual manufacturing overhead costs $1,100,000

Actual direct manufacturing labor-hours 22,000

Actual direct material costs $10,000

Actual direct manufacturing labor hours 200

Actual direct manufacturing labor rate $20 per hour

Required:

Calculate the total manufacturing costs using normal costing.

Local Steel Construction Company produces two products, steel and wood beams. Steel

beams have a unit contribution margin of $200, and wood beams have a unit

contribution margin of $150. The demand for steel beams exceeds Local Steel

Construction Company’s production capacity, which is limited by available direct labor

and machine-hours. The maximum demand for wood beams is 90 per week.

Management desires that the product mix should maximize the weekly contribution

toward fixed costs and profits.

Direct manufacturing labor is limited to 3,000 hours a week and 1,000 hours is all that

the company’s outdated machines can run a week. The steel beams require 120 hours of

labor and 60 machine-hours. Wood beams require 150 labor hours and 120

machine-hours.

Required:

Formulate the objective function and constraints necessary to determine the optimal

product mix.

What are three possible ways to dispose of underallocated or overallocated overhead

costs at the end of a fiscal year? Briefly comment on the theoretical correctness or

incorrectness of each method.

Describe job-costing and process-costing systems. Explain when it would be

appropriate to use each.

Explain the difference between an inventoriable cost and a period cost. What potential

problems does an inaccurate classification of product and period costs cause?

Briefly explain why many companies use absorption costing for external reporting as

well as internal accounting.

For each of the following measures, identify which perspective of the balanced

scorecard it represents: financial, customer, internal-business-process, or learning-and

growth.

1. service response time

2. market share

3. gross margin percentage

4. defect rates

5. customer satisfaction

6. information system availability

7. new-product development time

8. revenue growth

9. employee turnover rates

10. setup time

Patrick Ross, the president of M & M Materials Company, has asked for information

about the cost behavior of manufacturing overhead costs. Specifically, he wants to

know how much overhead cost is fixed and how much is variable. The following data

are the only records available:

Month Machine-hours Overhead Costs

February 1,870 $22,500

March 3,080 24,475

April 1,100 24,321

May 2,750 23,650

June 3,850 31,196

Required:

Using the high-low method, determine the overhead cost equation. Use machine-hours

as your cost driver.

What is the distinction between normal and abnormal spoilage?

What is a standard costing system?

Compare and contrast the theory of constraints and activity based costing. Which is

more useful in short-run and long-run management of costs?

What actions might be taken with an unprofitable customer?

What conflicts can arise between using discounted cash flow methods for capital

budgeting decisions and accrual accounting for performance evaluation? How can these

conflicts be reduced?

What is goal congruence?

Picture Company has one particular product that has an annual demand of 5,000 units.

Total manufacturing costs per unit total $50. Ordering costs for the product total $60

per purchase order. Currently, the carrying costs per unit are 25% of manufacturing

costs.

Required:

Determine the economic manufacturing order quantity.