Which of the following statements is true of sell-or-process-further decisions in joint

costing?

A) Joint costs incurred before the split-off point are relevant in deciding whether to

process the product further.

B) All separable costs in joint-cost allocations are incremental costs.

C) Separable costs incurred before the split-off point are irrelevant in deciding whether

to process the product further.

D) Costs that differ between the alternatives of selling products or processing further

are relevant.

Captain Carl’s Seascapes produces sea pictures for sale through catalogs. The company

has two workstations, photo production and framing. The photo production station is

limited by the speed of operating the photo development machine. Framing is limited

by the speed of the employees. Framing normally waits for work from photo

production. Each department works an eight-hour day. If Captain Carl’s Seascapes adds

an earlier half shift so that photo production begins work four hours earlier than

framing each day, the two departments generally finish their work at about the same

time. Not only does this eliminate the bottleneck, but it also increases finished units

produced each day by 200 units. All units produced can be sold. The cost of operating

the photo production department four more hours each day is $1310. The contribution

margin of the finished products is $20 each.

What is the change in the daily contribution margin if the change is made?

A) $250

B) $2690

C) $4000

D) $200

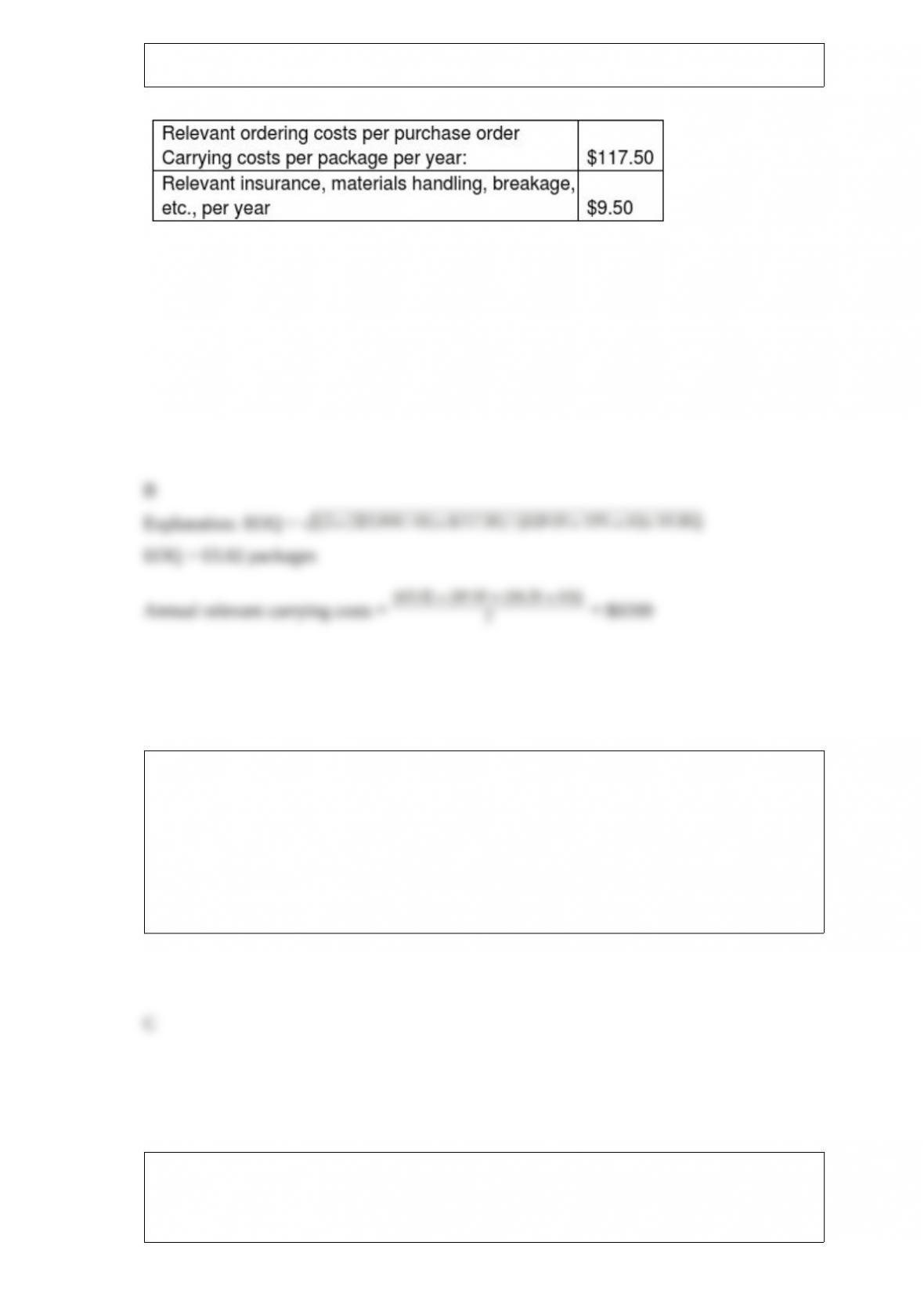

Globe Inc. is a distributor of DVDs. DVD Mart is a local retail outlet which sells blank

and recorded DVDs. DVD Mart purchases DVDs from Globe at $29.00 per DVD;

DVDs are shipped in packages of 65. Globe pays all incoming freight, and DVD Mart

does not inspect the DVDs due to Globe’s reputation for high quality. Annual demand is

321,000 DVDs at a rate of 6800 DVDs per week. DVD Mart earns 15% on its cash

investments. The purchase-order lead time is one week. The following cost data are

available:

What are the annual relevant carrying costs?

A) $9362

B) $9209

C) $849

D) $6511

When analyzing the change in operating income, the strategy component of

productivity ________.

A) calculations are similar to the sales-volume variance calculations

B) compares the change in output price with the changes in input prices

C) will report a large positive amount when a company has successfully pursued the

cost leadership strategy

D) isolates the change attributed solely to an increase in the quantity of units sold

To minimize the chances of violating pricing laws, a company should ________.

A) keep detailed records of variable costs for all value-chain business functions

B) use a variable cost-plus markup method of pricing

C) underprice products on a consistent basis, rather than sporadically

D) use dumping only when a product is at the end of its life cycle

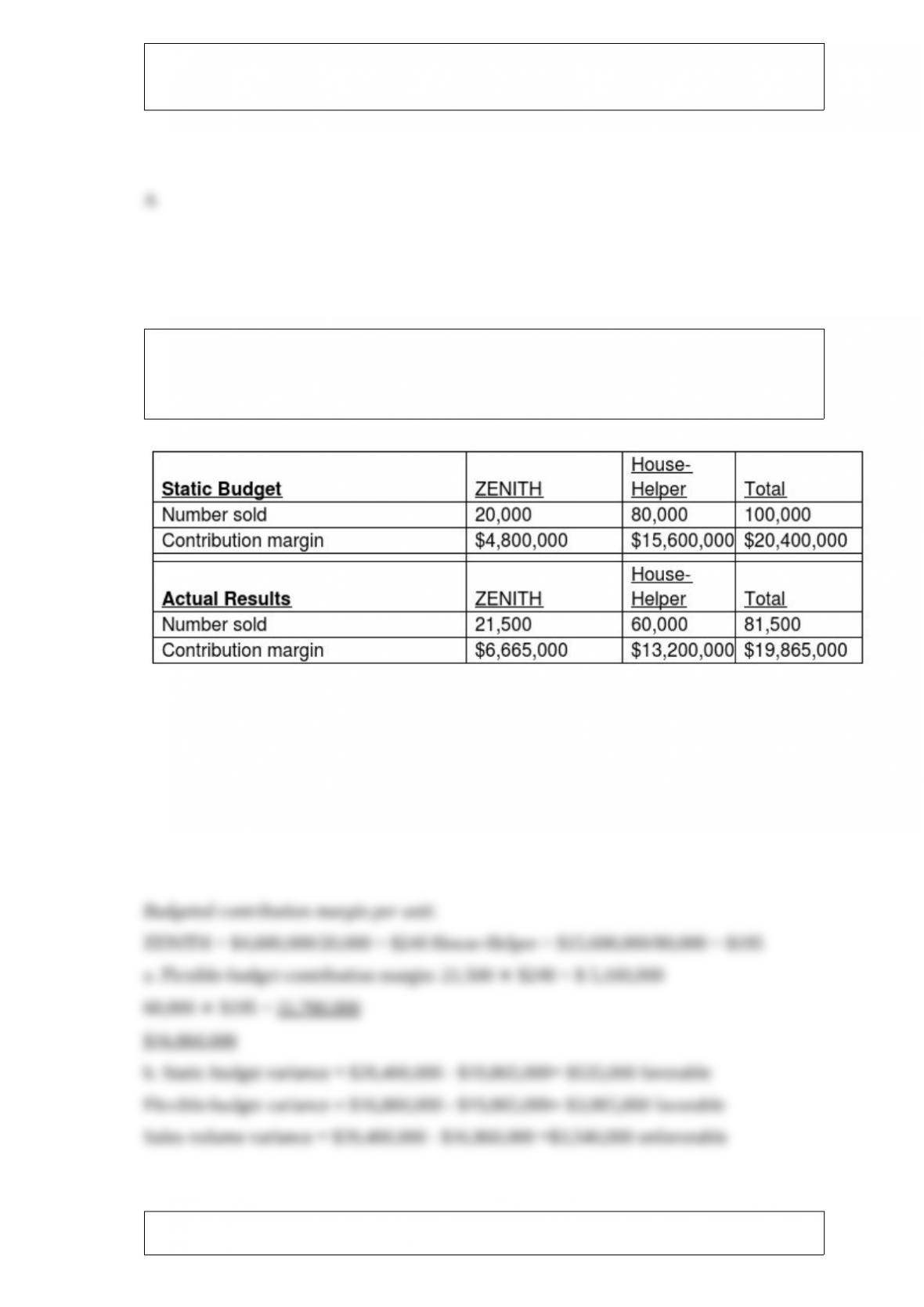

The Octova Corporation manufactures two types of vacuum cleaners: the ZENITH for

commercial building use and the House-Helper for residences. Budgeted and actual

operating data for the year 2017 are as follows:

Required:

a. Calculate the contribution margin for the flexible budget.

b. Determine the total static-budget variance, the total flexible-budget variance, and the

total sales-volume variance in terms of the contribution margin.

During 2018, Get There Corporation incurred manufacturing expenses of $200,000 to

produce 40,000 finished units. It was determined that 35,000 units were sold by the end

of November while 5,000 units remained in ending inventory. The storage cost for

December is $0.5 per unit.

Required:

a. What is the cost of producing one unit?

b. What is the amount that will be reported on the income statement for cost of goods

sold?

c. What is the cost incurred for storing the inventory?

________ is the continuing reduction in the demand for a company’s products that

occurs when competitor prices are not met.

A) Downward demand spiral

B) Competitor pricing pressure

C) Continuous step down demand

D) Super-demand cutback

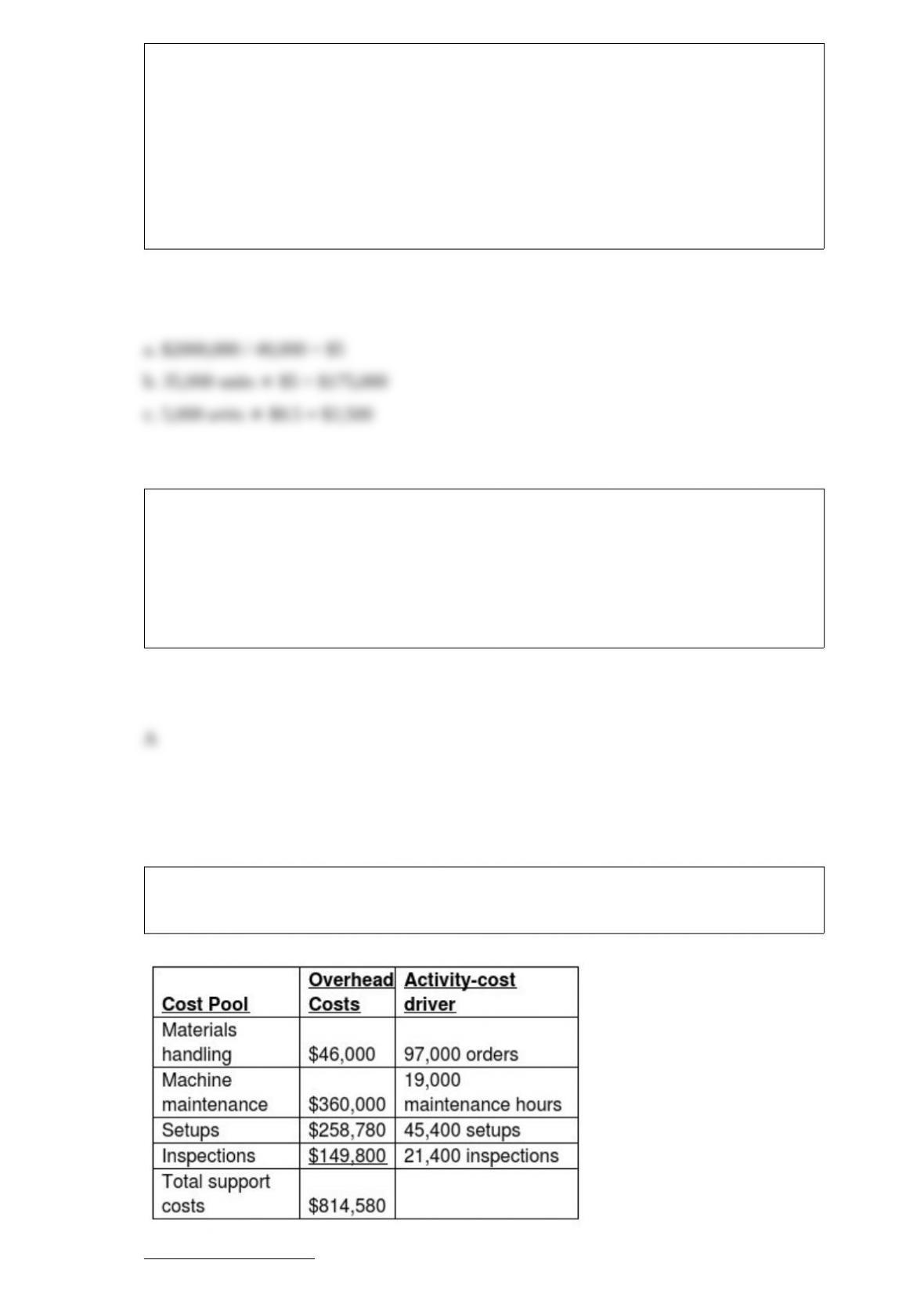

Canton Corp. manufactures two sizes of ceramic paperweights, regular and jumbo. The

following information applies to their expectations for the planning period:

Production Estimates

Production units:

Regular = 12,000,000 units

Jumbo = 24,000,000 units

Machine-hours = 400,000 mh

Labor-hours = 800,000 dlh

Expected direct costs amounts to $927,000 for the period. Support cost requirements of

both products are substantially different from one another. Zitriks uses an ABC costing

system.

Which of the following is true of Canton’s overhead costing?

A) Multiple cost pools are appropriate for Canton’s because of high direct costs.

B) Single cost pool is appropriate for Canton’s because of high direct costs.

C) Multiple cost pools are appropriate for Canton’s because of diverse support costs.

D) Single cost pool is appropriate for Canton’s because of diverse support costs.

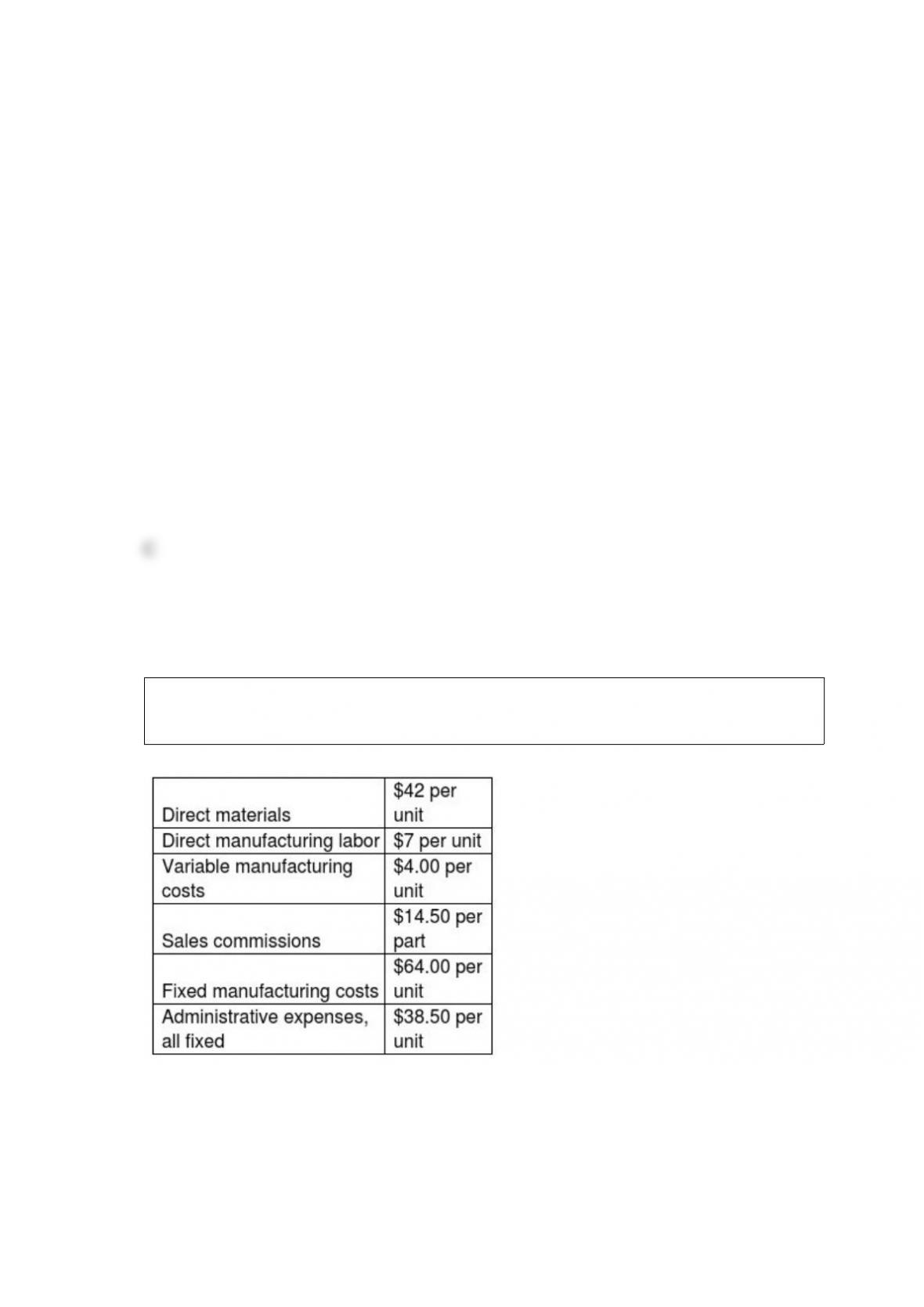

Time Again LLC produces and sells a mantel clock for $100 per unit. In 2017, 41,000

clocks were produced and 37,000 were sold. Other information for the year includes:

What is the inventoriable cost per unit using absorption costing?

A) $49.00

B) $53.00

C) $117.00

D) $106.00

The major objectives of a budgeting process should include all of the following

EXCEPT:

A) providing coordination among the subunits

B) providing communication among the subunits

C) providing unyielding commitment to targets as a means to achieve a target profit

D) providing a framework for judging performance and facilitating learning

When using the five-step decision process, which one of the following steps should be

done first?

A) obtain information

B) choose an alternative

C) evaluation and feedback

D) implementing the decision

Time and Again Company makes clocks. The fixed overhead costs for 2017 total

$900,000. The company uses direct labor-hours for fixed overhead allocation and

anticipates 200,000 hours during the year for 330,000 units. An equal number of units

are budgeted for each month.

During June, 32,000 clocks were produced and $72,000 was spent on fixed overhead.

Required:

a. Determine the fixed overhead rate for 2017 based on units of input.

b. Determine the fixed overhead static-budget variance for June.

c. Determine the production-volume overhead variance for June.

In planning and control of capacity costs, managers must consider possible capacity

measures. Which of the following measures the available supply of capacity in a

factory?

A) Theoretical capacity

B) Practical capacity

C) Normal capacity

D) Master-budget capacity

Forge Company wants to purchase a new cutting machine for its sewing plant. The

investment is expected to generate annual cash inflows of $140,000. The required rate

of return is 10% and the current machine is expected to last for seven years. Of the

following choices, which is the dollar amount the company would be willing to spend

for the machine, assuming its life is also seven years? Income taxes are not considered.

A) $1,328,180

B) $882,000

C) $702,660

D) $681,520

Division A sells ground veal internally to Division B, which in turn, produces veal

burgers that sell for $19 per pound. Division A incurs costs of $1.25 per pound while

Division B incurs additional costs of $6.50 per pound.

Which of the following formulas correctly reflects the company’s operating income per

pound?

A) $19 – ($1.25 + $6.50) = $11.25

B) $19 – ($3.25 + $6.50) = $9.25

C) $19 – ($1.25 + $9.75) = $8.00

D) $19 – ($0.75 + $3.25 + $3.25) = $5.50

Striker 44 Corporation produces a part that is used in the manufacture of one of its

products. The costs associated with the production of 12,000 units of this part are as

follows:

Direct materials $86,000

Direct labor 130,000

Variable factory overhead 57,000

Fixed factory overhead 135,000

Total costs $408,000

Of the fixed factory overhead costs, $58,000 is avoidable.

Assuming no other use of their facilities, the highest price that McMurphy should be

willing to pay for 12,000 units of the part is ________.

A) $408,000

B) $273,000

C) $331,000

D) $351,000

Answer the following question using the information below:

Jason Novelty Company produces a specialty item. Management has provided the

following information:

What is the total throughput contribution?

A) $3,432,000

B) $3,360,000

C) $4,620,000

D) $2,520,000

Which of the following statements is true of benchmarking?

A) It is a systematic approach of optimizing business processes.

B) It fails to help to improve organizational performance as benchmarking data does not

provide insight into why costs or revenues differ across companies.

C) It is difficult to ensure that the benchmark numbers are comparable due to the

existence of differences across companies.

D) It considers four major business aspects such as financial, customer, internal

business processes, and learning and growth.

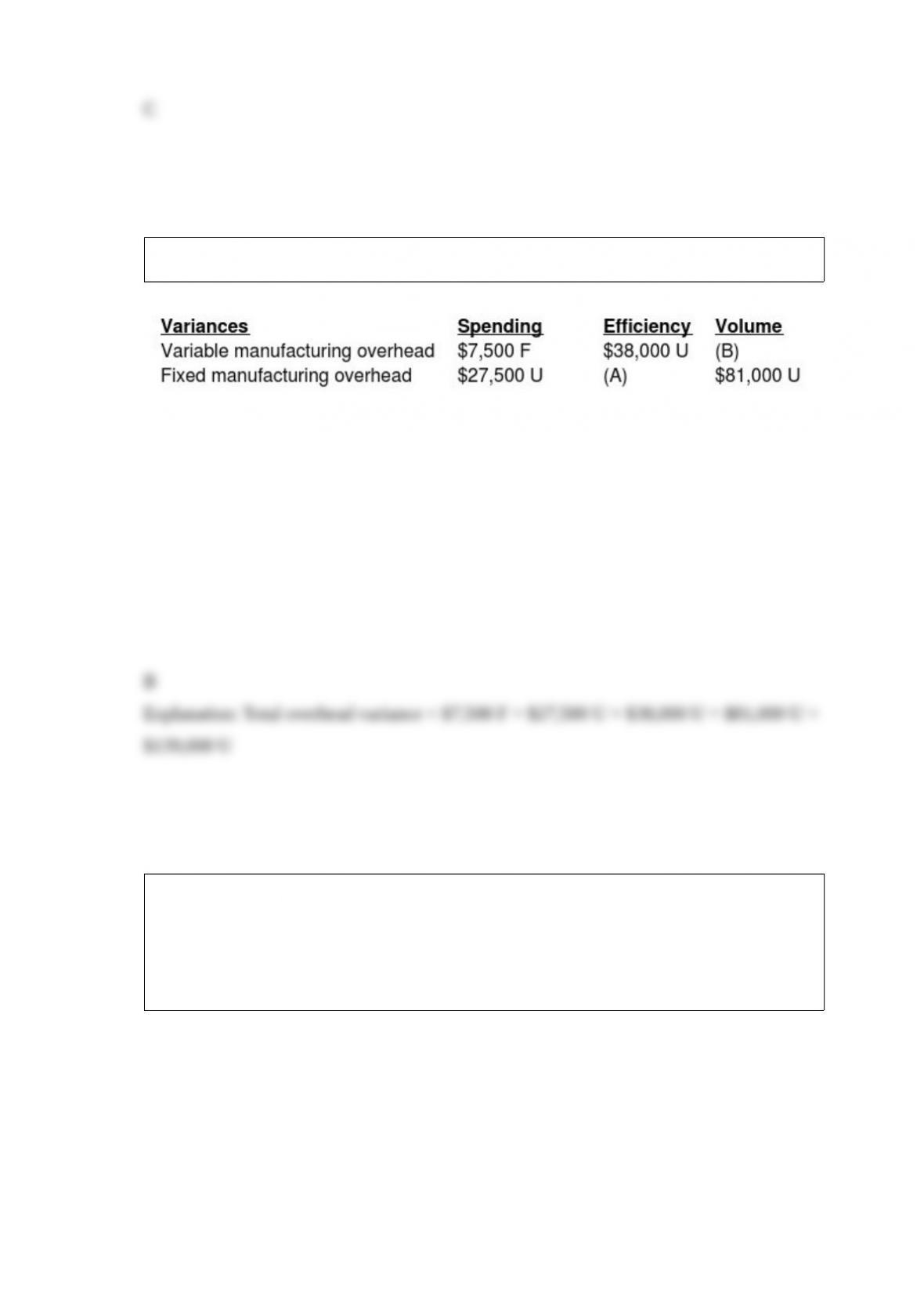

The total overhead variance should be ________.

A) $154,000 F

B) $139,000 U

C) $154,000 U

D) $139,000 F

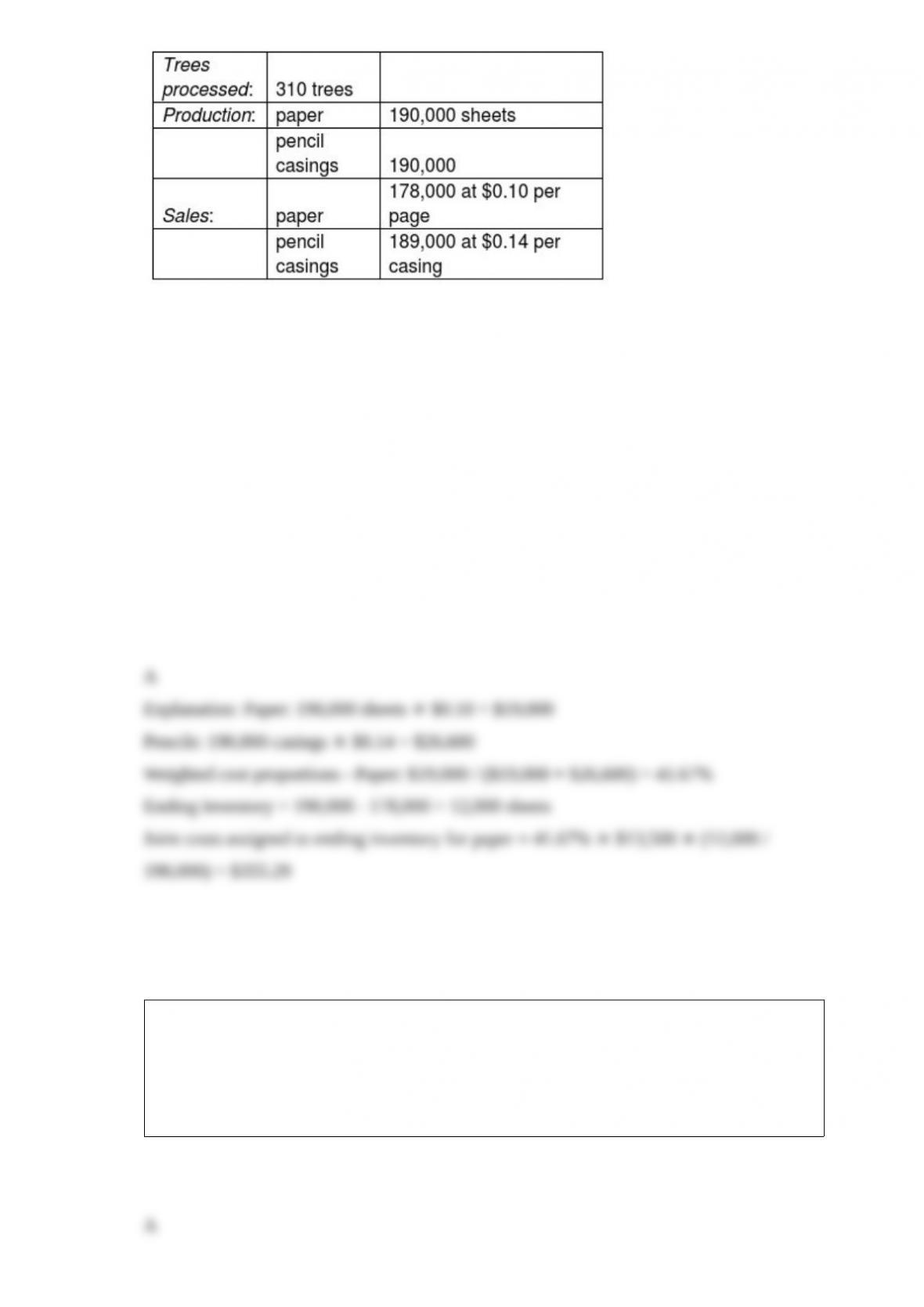

Bismite Corporation purchases trees from Cheney lumber and processes them up to the

split-off point where two products (paper and pencil casings) emerge from the process.

The products are then sold to an independent company that markets and distributes

them to retail outlets. The following information was collected for the month of

October:

The cost of purchasing 310 trees and processing them up to the split-off point to yield

190,000 sheets of paper and 190,000 pencil casings is $13,500.

Bismite’s accounting department reported no beginning inventory.

If the sales value at split-off method is used, what are the approximate joint costs assigned

to ending inventory for paper? (Round intermediary percentages to the nearest hundredth.)

A) $355.29

B) $29.61

C) $497.34

D) $379.24

Under GAAP, only ________ can be assigned to inventories in the financial statements.

A) manufacturing costs

B) period costs

C) cost of goods sold

D) historical costs

The use of activity-based budgeting is growing because of ________.

A) the increased use of activity-based costing

B) the increased use of kaizen costing

C) increases in work-in-process inventory

D) increases in direct materials inventory

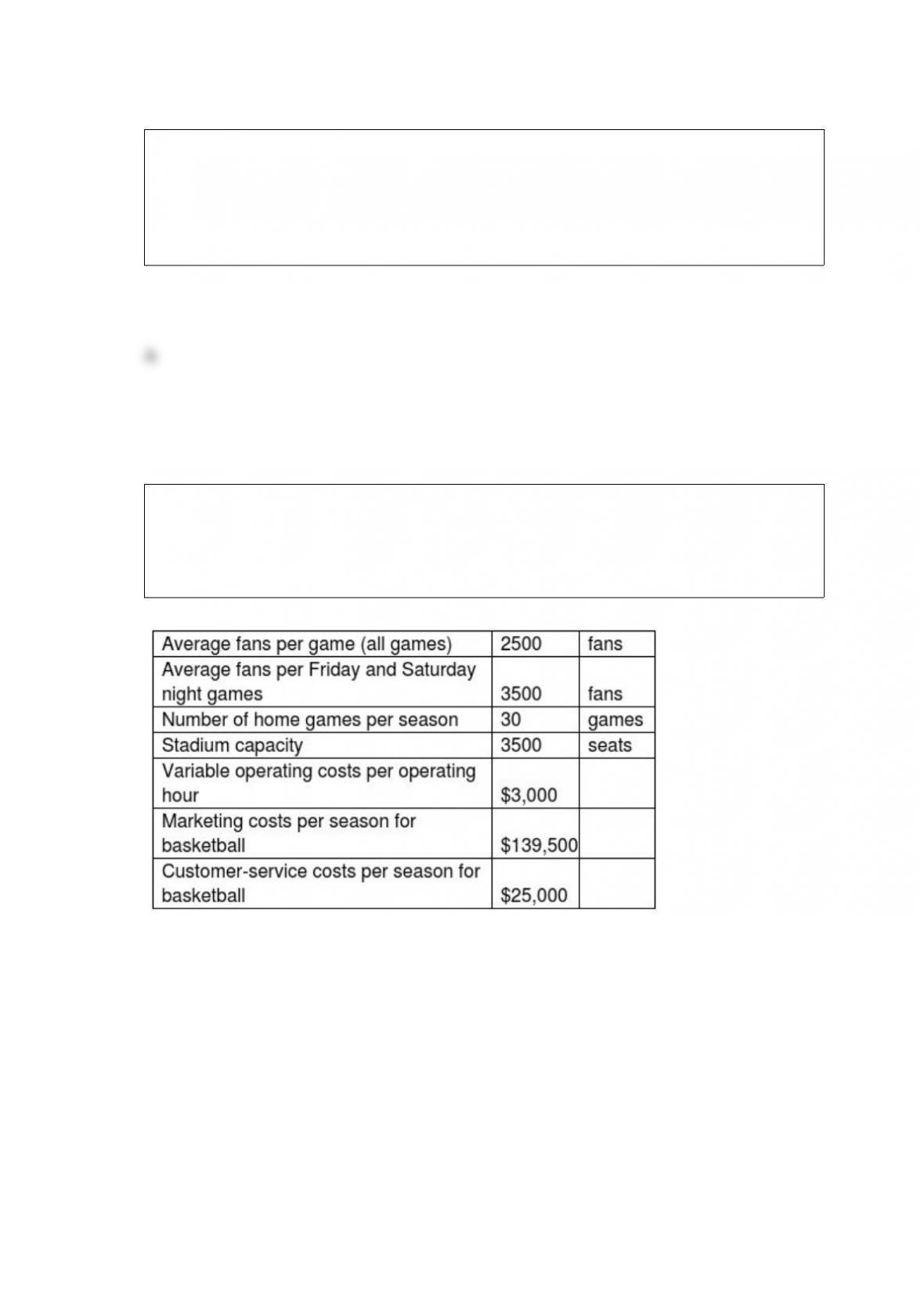

The Maize Eagles are evaluating ticket prices for its basketball games. Studies show

that Friday and Saturday night games average more than twice the number of fans

compared to other days. The following information pertains to the stadium’s normal

operations per season:

The stadium is open for 4 operating hours on each day a game is played. All employees

work by the hour except for the administrators. A maximum of one game is played per day

and each fan has only one ticket per game.

The stadium authority wants to charge more for games on Friday and Saturday. What is the

minimum price that should be charged for peak attendance nights?

A) $4.99

B) $4.80

C) $6.99

D) $209.80

The Zeron Corporation wants to purchase a new machine for its factory operations at a

cost of $380,000. The investment is expected to generate $225,000 in annual cash flows

for a period of four years. The required rate of return is 10%. The old machine can be

sold for $30,000. The machine is expected to have zero value at the end of the four-year

period. What is the net present value of the investment? Would the company want to

purchase the new machine? Income taxes are not considered.

A) $363,025; yes

B) $22,500; no

C) $350,000; yes

D) $375,650; no

Crandle Manufacturers Inc. is approached by a potential new customer to fulfill a

one-time-only special order for a product similar to one offered to domestic customers.

The company has excess capacity. The following per unit data apply for sales to regular

customers:

Variable costs:

Direct materials $170

Direct labor 90

Manufacturing support 135

Marketing costs 85

Fixed costs:

Manufacturing support 145

Marketing costs 75

Total costs 700

Markup (40%) 280

Targeted selling price $980

What is the contribution margin per unit?

A) $220

B) $280

C) $500

D) $700

When companies do not want to use market prices or find it too costly, they typically

use ________ prices, even though suboptimal decisions may occur.

A) average-cost

B) full-cost

C) long-run cost

D) short-run average cost

Which of the following is true of a budget?

A) Budgets are used to express only the operational plans and not the strategic plans of

a company.

B) Budgets do not account for nonfinancial aspects of the upcoming period.

C) Budgets are most useful when they are planned independent of the company’s

strategic plans.

D) Budgets help managers to revise their plans and strategies.

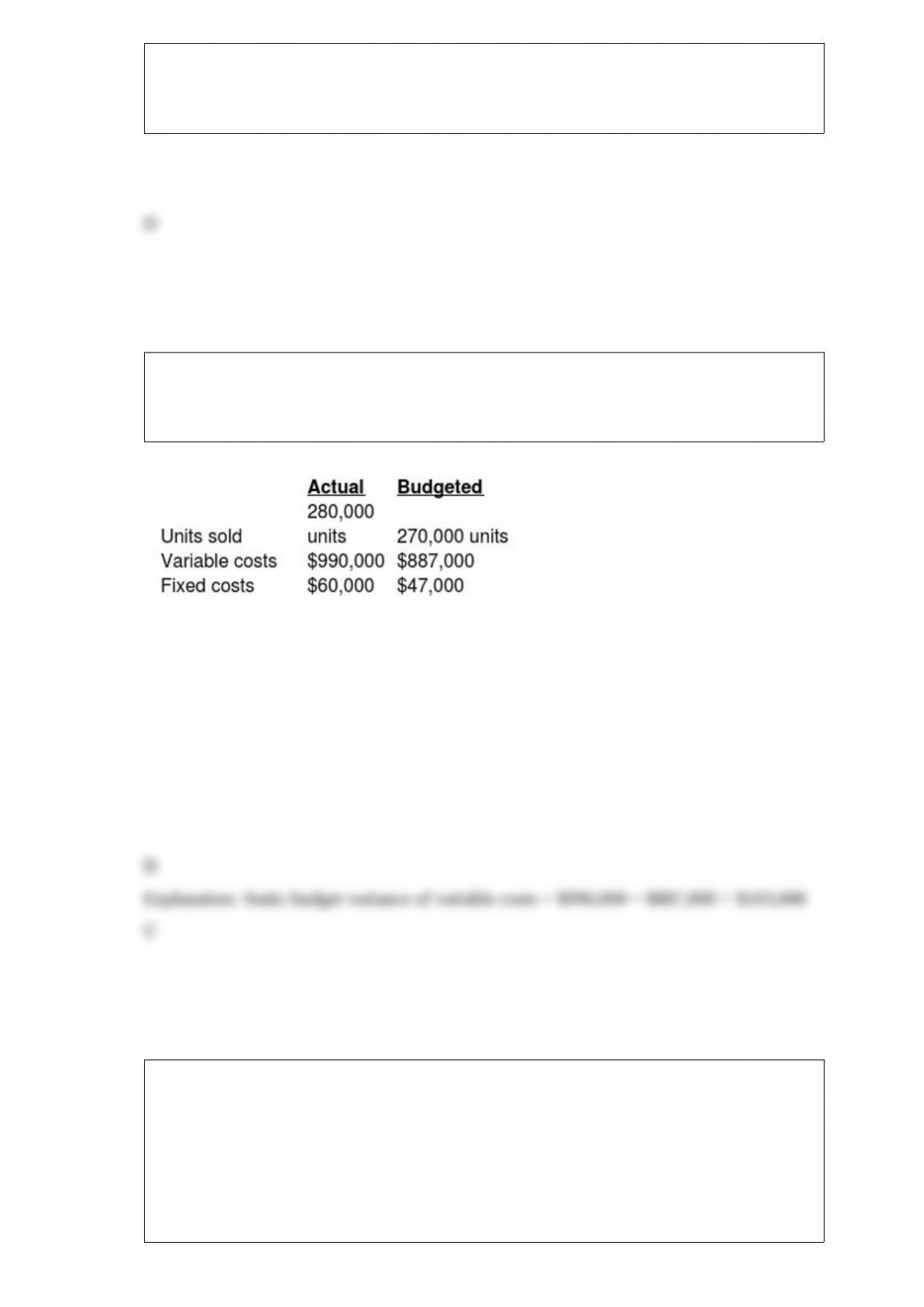

Daniels Corporation used the following data to evaluate their current operating system.

The company sells items for $19 each and had used a budgeted selling price of $20 per

unit.

What is the static-budget variance of variable costs?

A) $116,000 favorable

B) $116,000 unfavorable

C) $103,000 favorable

D) $103,000 unfavorable

Stephanie’s Bridal Shoppe sells wedding dresses. The average selling price of each

dress is $1,200, variable costs are $700, and fixed costs are $100,000. How many

dresses must the Bridal Shoppe sell to yield after-tax net income of $20,000, assuming

the tax rate is 40%?

A) 267 dresses

B) 240 dresses

C) 200 dresses

D) 400 dresses

Which of the following is a stage of the capital budgeting process that indicates

potential capital investments that agree with an organization’s strategy?

A) identify projects stage

B) make predictions stage

C) obtain information stage

D) implement the decision, evaluate performance, and learn stage

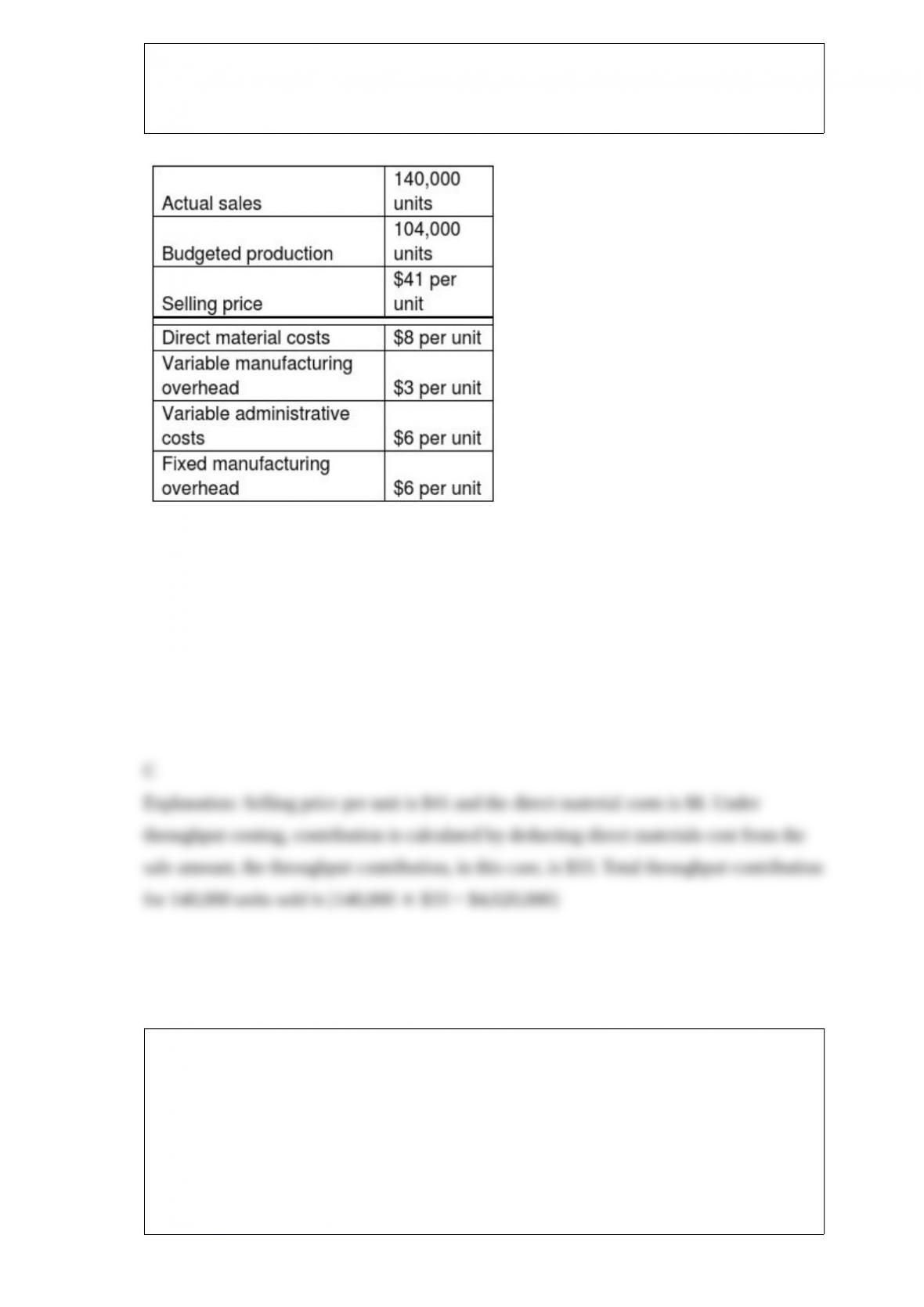

Swan Textiles Inc. produces and sells a decorative pillow for $98.00 per unit. In the first

month of operation, 2,300 units were produced and 1,800 units were sold. Actual fixed

costs are the same as the amount budgeted for the month. Other information for the

month includes:

What is the contribution margin using variable costing?

A) $135,000

B) $124,200

C) $165,600

D) $123,500