SOLUTION

(60 min.) Variable and absorption costing and breakeven points

1.

2017 Variable-Costing Based Operating Income Statement

Revenues (1,300 boards

´

$800 per board)

Variable costs:

Beginning inventory (240 boards

´

$375 per board)

Variable manufacturing costs (1,200 boards

´

$375 per board)

Deduct: Ending inventory (140 boards

´

$375 per board)

Variable shipping costs (1,300 boards

´

$20 per board)

26 ,000

Fixed costs

2.

2017 Absorption-Costing Based Operating Income Statement

Revenues (1,300 boards

´

$800 per board)

Cost of goods sold:

Beginning inventory (240 boards

´

$665a per board)

Variable manufacturing costs (1,200 boards

´

$375 per board)

Allocated fixed manufacturing costs (1,200 boards

´

$290 per board)

´

´

26,000

3. Breakeven point in units:

a. Variable Costing:

Q=

Total Fixed Costs Target Operating Income

Contribution Margin Per Unit

+

Q=

($319,000 $150,000) $0

$800 ($375 $20)

+ +

– +

Q=

$469,000

$405

Q= 1,159 hoverboards (rounding up)

b. Absorption costing:

Fixed manufacturing cost rate = $319,000 ÷ 1,100 = $290 per hoverboard

Total Target Fixed Breakeven Units

fixed operating manufacturing sales produced

costs income cost rate in units

Contribution margin per unit

Q

é ù

æ ö

ê ú

ç ÷

+ + ´ –

ê ú

ç ÷

ç ÷

ê ú

è ø

ë û

=

Q=

[ ]

($319,000 $150,000) $0 $290 (Q 1, 200)

$405

+ + + –

$405Q= $469,000 + $290Q – $348,000

$392,000+$280 Q−$252,000

4. Proof of breakeven point:

a. Variable Costing:

b. Absorption costing:

Revenues, $800

´

1,053 units $842,400

*This is not zero due to rounding up to 1,159 and 1,053 whole units sold.

5. If $44,000 of fixed administrative costs were reclassified as production costs, there would

be no change in breakeven sales using variable costing. This is because all fixed costs,

regardless of whether they are for production or administrative activities, are treated the same

6. The additional $20 per unit variable production cost will cause unit contribution margin

to decrease from $405 to $385. This decrease will cause the breakeven point to increase.

In the case of variable costing:

9-41 Downward demand spiral. Market.com is about to enter the highly

competitive personal electronics market with a new type of tablet. In anticipation of future

growth, the company has leased a large manufacturing facility and has purchased several

expensive pieces of equipment. In 2017, the company’s first year, Market.com budgets for

production and sales of 50,000 units, compared with its practical capacity of 78,000. The

company’s cost data are as follows:

Required:

1. Assume that Market.com uses absorption costing and uses budgeted units produced as the

denominator for calculating its fixed manufacturing overhead rate. Selling price is set at

140% of manufacturing cost. Compute Market.com’s selling price.

2. Market.com enters the market with the selling price computed previously. However, despite

growth in the overall market, sales are not as robust as the company had expected, and a

competitor has priced its product at $102.00. Mr. Samuel Buttons, the company’s president,

insists that the competitor must be pricing its product at a loss and that the competitor will be

unable to sustain that. In response, Market.com makes no price adjustments but budgets

production and sales for 2018 at 43,800 tablets. Variable and fixed costs are not expected to

change. Compute Market.com’s new selling price. Comment on how Market.com’s choice of

budgeted production affected its selling price and competitive position.

3. Recompute the selling price using practical capacity as the denominator level of activity.

How would this choice have affected Market.com’s position in the marketplace? Generally,

how would this choice affect the production-volume variance?

SOLUTION

(20 min.) Downward demand spiral.

1. Fixed manufacturing overhead rate =

¿

$650,000/50,000 units = $13 per unit

Manufacturing cost per unit:

$22 direct materials + $30 direct mfg. labor + $12 var. mfg. OH + $13 fixed mfg. OH = $77

2. Fixed manufacturing overhead rate =

¿

$650,000/43,800 units = $14.84 per unit

By using budgeted units produced, and not practical capacity, as the denominator level,

Market.com is burdening its products with the cost of unused capacity. Apparently, the

3. Fixed manufacturing overhead rate =

¿

$650,000/78,000 units = $8.33 per unit

Manufacturing cost per unit:

If Market.com had used practical capacity as its denominator level of activity, its initial selling

price of $101.26 would have been virtually in line with the $102 selling price of its competitor,

9-42 Absorption costing and production-volume variance—

alternative capacity bases. Planet Light First (PLF), a producer of energy-efficient

light bulbs, expects that demand will increase markedly over the next decade. Due to the high

fixed costs involved in the business, PLF has decided to evaluate its financial performance using

absorption costing income. The production-volume variance is written off to cost of goods sold.

The variable cost of production is $2.40 per bulb. Fixed manufacturing costs are $1,170,000 per

year. Variable and fixed selling and administrative expenses are $0.20 per bulb sold and

$220,000, respectively. Because its light bulbs are currently popular with environmentally

conscious customers, PLF can sell the bulbs for $9.80 each.

PLF is deciding among various concepts of capacity for calculating the cost of each unit

produced. Its choices are as follows:

Theoretical capacity 900,000 bulbs

Practical capacity 520,000 bulbs

Normal capacity 260,000 bulbs (average expected output for the next three years)

Master-budget capacity 225,000 bulbs expected production this year

Required:

1. Calculate the inventoriable cost per unit using each level of capacity to compute fixed

manufacturing cost per unit.

2. Suppose PLF actually produces 300,000 bulbs. Calculate the production-volume variance

using each level of capacity to compute the fixed manufacturing overhead allocation rate.

3. Assume PLF has no beginning inventory. If this year’s actual sales are 225,000 bulbs,

calculate operating income for PLF using each type of capacity to compute fixed

manufacturing cost per unit.

SOLUTION

(35 min.) Absorption costing and production volume variance — alternative capacity

bases

1. Inventoriable cost per unit = Variable production cost + Fixed manufacturing

overhead/Capacity

Capacity Type

Capacity

Level

Fixed Mfg.

Overhead

Fixed Mfg.

Overhead

Rate

Variable

Production

Cost

Inventoriable

Cost Per Unit

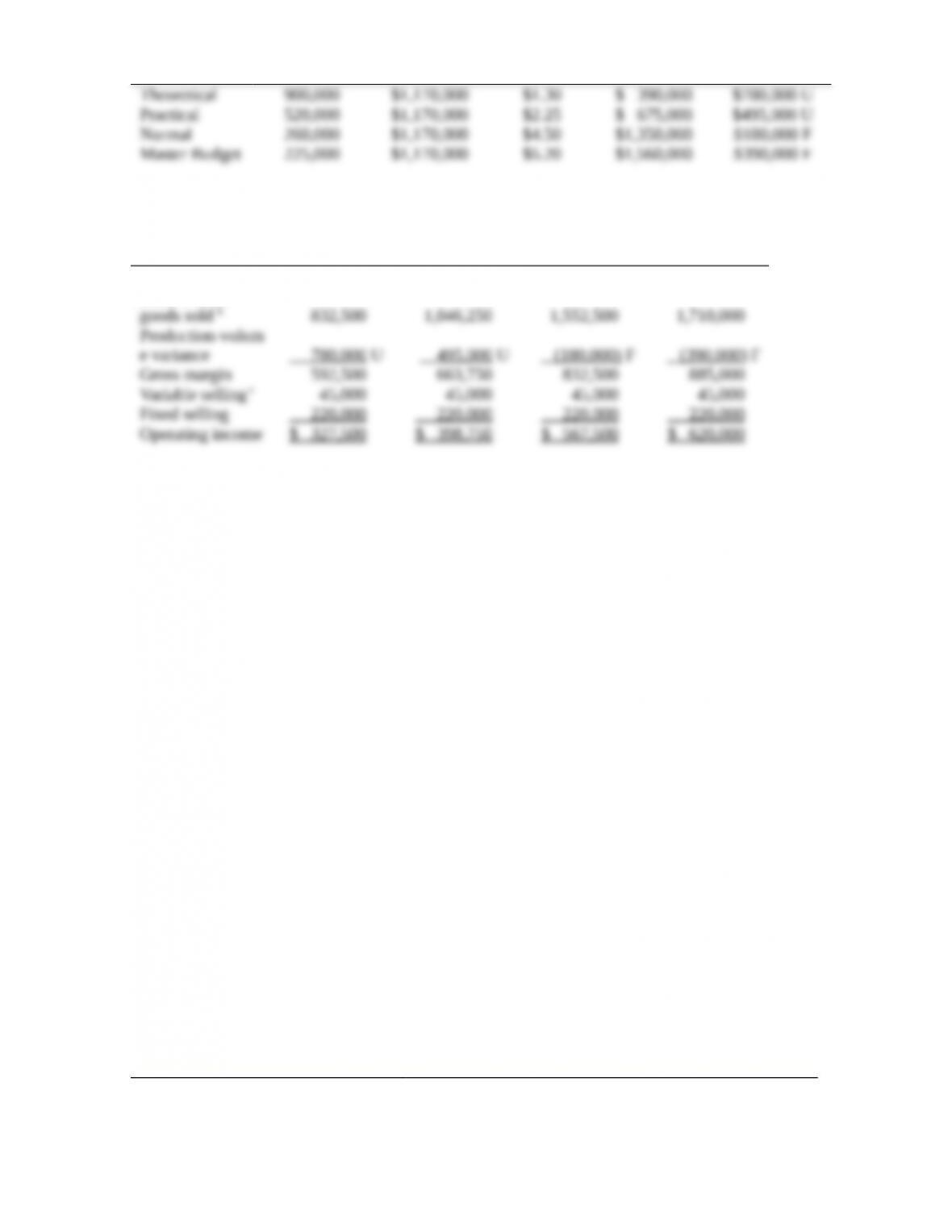

Theoretical 900,000 $1,170,000 $1.30 $2.40 $3.70

2. PLF’s actual production level is 300,000 bulbs. We can compute the production-volume

variance as:

Production Volume Variance = Budgeted Fixed Mfg. Overhead

Capacity Type

Capacity

Level

Fixed Mfg.

Overhead

Fixed Mfg.

Overhead

Rate

Fixed Mfg.

Overhead

Rate × Actual

Production

Production

Volume

Variance

3. Operating Income for PLF given production of 300,000 bulbs and sales of 225,000 bulbs @

$9.80 apiece:

Theoretical Practical Normal Master Budget

Revenue a$2,205,000 $2,205,000 $2,205,000 $2,205,000

Less: Cost of

a225,000 × 9.80

b225,000 × 3.70, × 4.65, × 6.90, × 7.60

c225,000 × 0.20

9-43 Operating income effects of denominator-level choice and

disposal of production-volume variance (continuation of 9-42).

Required:

1. If PLF sells all 300,000 bulbs produced, what would be the effect on operating income of

using each type of capacity as a basis for calculating manufacturing cost per unit?

2. Compare the results of operating income at different capacity levels when 225,000 bulbs are

sold and when 300,000 bulbs are sold. What conclusion can you draw from the comparison?

3. Using the original data (that is, 300,000 units produced and 225,000 units sold) if PLF had

used the proration approach to allocate the production-volume variance, what would

operating income have been under each level of capacity? (Assume that there is no ending

work in process.)

SOLUTION

(35 min.) Operating income effects of denominator-level choice and disposal of

production-volume variance (continuation of 9-42)

1. Since no beginning inventories exist, if PLF sells all 300,000 bulbs manufactured, its

operating income will be the same under all four capacity options. Calculations are provided

below:

Theoretical Practical Normal Master Budget

Revenue a$2,940,000 $2,940,000 $2,940,000 $2,940,000

Less: Cost of 1,110,000 1,395,000 2,070,000 2,280,000

goods sold b

Less: Production

2. If the manager of PLF produces and sells 300,000 bulbs, then all capacity levels will result in

the same operating income of $770,000 (see requirement 1 above). If the manager of PLF is able

to sell only 225,000 of the bulbs produced and if the production-volume variance is closed to

cost of goods sold, then the operating income is given as in requirement 3 of 9-42. Both sets of

numbers are reproduced below.

Theoretical Practical Normal Master Budget

3. In this scenario, the manager of PLF produces 300,000 bulbs and sells 225,000 of them, and

the production volume variance is prorated. Given the absence of ending work in process

inventory or beginning inventory of any kind, the fraction of the production volume variance that

is absorbed into the cost of goods sold is given by 225,000/300,000 or 75%. The operating

income under various denominator levels is then given by the following modification of the

solution to requirement 3 of 9-42:

Theoretical Practical Normal Master Budget

Revenue $2,205,000 $2,205,000 $2,205,000 $2,205,000

Less: Cost of goods

9-44 Variable and absorption costing, actual costing. The Iron City

Company started business on January 1, 2017. Iron City manufactures a specialty honey beer,

which it sells directly to state-owned distributors in Pennsylvania. Honey beer is produced and

sold in six-packs, and in 2017, Iron City produced more six-packs than it was able to sell. In

addition to variable and fixed manufacturing overhead, Iron City incurred direct materials costs

of $880,000, direct manufacturing labor costs of $400,000, and fixed marketing and

administrative costs of $295,000. For the year, Iron City sold a total of 180,000 six-packs for a

sales revenue of $2,250,000.

Iron City’s CFO is convinced that the firm should use an actual costing system but is debating –

whether to follow variable or absorption costing. The controller notes that Iron City’s operating

income for the year would be $438,000 under variable costing and $461,000 under absorption

costing. Moreover, the ending finished-goods inventory would be valued at $7.15 under variable

costing and $8.30 under absorption costing.

Iron City incurs no variable nonmanufacturing expenses.

Required:

1. What is Iron City’s total contribution margin for 2017?

2. Iron City incurs fixed manufacturing costs in addition to its fixed marketing and

administrative costs. How much did Iron City incur in fixed manufacturing costs in 2017?

3. How many six-packs did Iron City produce in 2017?

4. How much in variable manufacturing overhead did Iron City incur in 2017?

5. For 2017, how much in total manufacturing overhead is expensed under variable costing,

either through cost of goods sold or as a period expense?

SOLUTION

(30 min.) Variable and absorption costing, actual costing.

1. Since no beginning inventories exist, the cost of the ending inventory must be the same as the

cost of goods sold for the period. So, the unit cost of goods sold under variable costing is $7.15.

2. The profit under variable costing is given as $438,000. We just calculated the contribution

margin of Iron City as $963,000. The difference, $525,000 ($963,000 – $438,000) must

represent the total fixed costs incurred by Iron City in 2017.

In requirement 2, we calculated that the total fixed manufacturing costs are $230,000.

So, Units produced = Total manufacturing costs/Unit fixed manufacturing cost of production

4. In 2017, Iron City incurred a total of 200,000 × $7.15 = $1,430,000 in variable manufacturing

costs. This includes $880,000 in direct materials costs (given), $400,000 in direct manufacturing

labor costs (given), and the rest in variable manufacturing overhead.

5. Under variable costing, the proportion of variable manufacturing overhead corresponding to

the units sold, relative to units produced, is expensed as variable cost of goods sold. This equals:

9-45 Cost allocation, downward demand spiral. Meals To Go operates a

chain of 10 hospitals in the Los Angeles area. Its central food-catering facility, Mealman,

prepares and delivers meals to the hospitals. It has the capacity to deliver up to 1,460,000 meals a

year. In 2017, based on estimates from each hospital controller, Mealman budgeted for 1,050,000

meals a year. Budgeted fixed costs in 2017 were $1,533,000. Each hospital was charged $6.16

per meal—$4.70 variable costs plus $1.46 allocated budgeted fixed cost.

Recently, the hospitals have been complaining about the quality of Mealman’s meals and their

rising costs. In mid-2017, Meals To Go’s president announces that all Meals To Go hospitals and

support facilities will be run as profit centers. Hospitals will be free to purchase quality-certified

services from outside the system. Dean Wright, Mealman’s controller, is preparing the 2018

budget. He hears that three hospitals have decided to use outside suppliers for their meals, which

will reduce the 2018 estimated demand to 912,500 meals. No change in variable cost per meal or

total fixed costs is expected in 2018.

Required:

1. How did Wright calculate the budgeted fixed cost per meal of $1.46 in 2017?

2. Using the same approach to calculating budgeted fixed cost per meal and pricing as in 2017,

how much would hospitals be charged for each Mealman meal in 2018? What would the

reaction of the hospital controllers be to the price?

3. Suggest an alternative cost-based price per meal that Wright might propose and that might

be more acceptable to the hospitals. What can Mealman and Wright do to make this price

profitable in the long run?