Decisions regarding sources of long-term financing are best made at subunit level as the

subunit has local knowledge and can leverage it in negotiations.

Managers track the costs incurred in each value-chain category is to reduce costs and to

improve efficiency.

An actual cost is the cost incurred–a historical or past cost.

Each cost pool will have one cost-allocation base.

Fixed costs automatically increase or decrease with the level of activity within a

relevant range of activity.

When using transfer prices based on costs rather than market prices, management can

better determine profitability of the investment made in the intermediate producing

division.

When a company has no opening or ending inventory during the month, the cost per

unit is calculated by dividing the total costs incurred in the period by the total units

produced during the period.

The financial cost of quality measures serves as a common denominator for evaluating

trade-offs among prevention costs and failure costs.

Computer-based systems, such as ERP systems, cannot perform calculations for

financial planning models.

The classification of costs as variable and fixed depends on the relevant range, the

length of the time horizon, and the specific decision situation.

In an EVA calculation, the appropriate measure of a division’s profit would be that

division’s pre-tax operating income.

Throughput costing considers only direct materials and direct manufacturing labor to be

truly variable costs.

Two different approaches to pricing decisions are market based and cost-plus.

Goal congruence exists when individuals work toward achieving one goal, and groups

work toward achieving a different goal.

The net present value (NPV) method calculates the expected monetary gain or loss from

a project by discounting all expected future cash inflows and outflows back to the

present point in time using the required rate of return.

Product-mix decisions usually have only a short-run focus because they typically arise

in the context of capacity constraints that can be relaxed in the long run.

Whether the firm uses the market-based approach or the cost-based approach for

pricing decisions, the market forces must be considered.

Percentage of reworked products is an example of a nonfinancial measure of internal

business-process quality.

Many common performance measures, such as customer satisfaction, rely on internal

financial accounting information.

Value engineering cannot decrease value-added costs.

When budgeted fixed costs are allocated based on actual usage, user departments will

not know their fixed-cost allocations until the end of the budget period.

Integrity is to abstain from engaging in or supporting any activity that might discredit

the profession.

The principal difference between process costing and job costing is that in job costing

an averaging process is used to compute the unit costs of products or services.

A customer cost hierarchy may include distribution-channel costs.

The implication of controlling a process at a Six Sigma level is that the process

produces only 3.4 defects per million products produced.

Because the cost driver is the same for the fringe benefits of life insurance and pension

benefits cost is the same, those costs can be aggregated into one homogeneous cost

pool.

An example of why a manager would perform cost allocations for economic decisions

would be to cost inventories for reporting to the tax authorities.

Simple regression analysis estimates the relationship between the dependent variable

and one independent variable.

Gross Margin will always be greater than contribution margin.

The accounting for 3-variance analysis is simpler than the 4-variance analysis, but some

information is lost because the variable and fixed overhead spending variances are

combined

into a single tosstal overhead spending variance.

Accountants define a cost as the amount of money spent on a resource.

The issue of “allowable costs” is applicable in government cost-plus contracts.

The balanced scorecard uses financial and nonfinancial performance measures to

evaluate short-run and long-run performance in a single report.

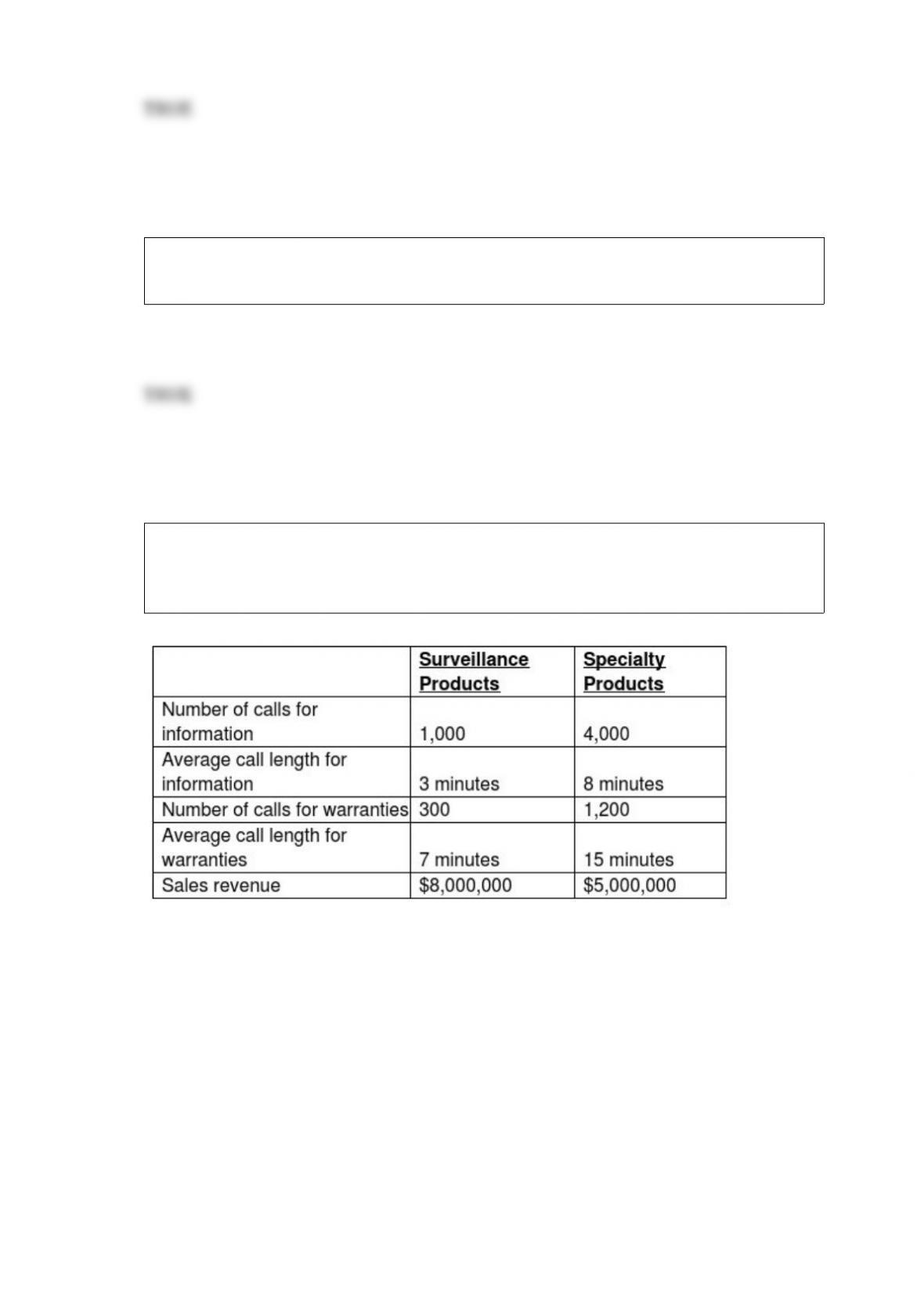

At New England Goods Inc., product lines are charged for call center support costs

based on sales revenue. Last year’s summary of call center operations revealed the

following:

New England Goods Inc. currently allocates call center support costs using a rate of 0.6%

of sales revenue.

Required:

a. Compute the amount of call center support costs allocated to each product line under the

current system.

b. Assume New England decides to use the average call length for information to assign

last year’s support costs. Does this allocation method seem more appropriate than

percentage of sales? Why or why not?

c. Assume New England decides to use the numbers of calls for information and for

warranties to assign last year’s support costs of $65,000. Compute the amount of call

center support costs assigned to each product line under this revised ABC system.

d. New England Goods assigns bonuses based on departmental profits. How might the

Specialty Products manager try to obtain higher profits for next year if support costs are

assigned based on the average call length for information?

e. Discuss the barriers for implementing ABC for this call center.

Tony placed an order for a customized watch. The customer response time is 43 hours,

its receipt time is 9 hours, and manufacturing cycle time is 25 hours. Calculate the

delivery time of the product.

A) 18 hours

B) 9 hours

C) 16 hours

D) 4.5 hours

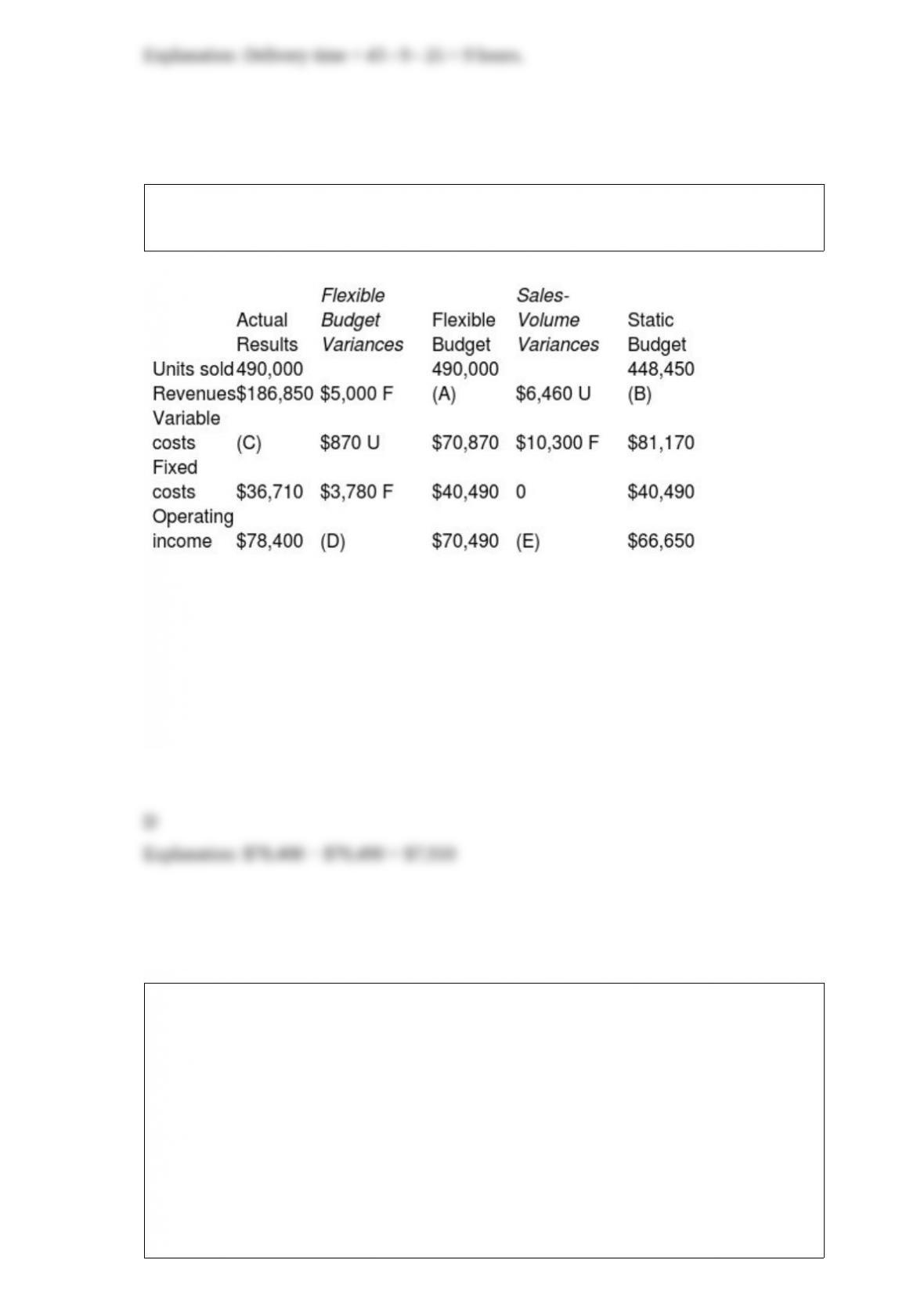

Classic Products Company manufactures colonial style desks. Some of the company’s

data was misplaced. Use the following information to replace the lost data:

What is the total flexible-budget variance (D)?

A) $11,750 favorable

B) $0

C) $3,840 favorable

D) $7,910 favorable

Orion Company sells several products. Information of average revenue and costs is as

follows:

Selling price per unit $23

Variable costs per unit:

Direct material $4

Direct manufacturing labor $1.70

Manufacturing overhead $0.40

Selling costs $2

Annual fixed costs $100,000

The company sells 12,000 units at the end of the year.

If direct labor and direct material costs increase by $1 each, contribution margin

________.

A) increases by $24,000

B) increases by $12,000

C) decreases by $24,000

D) decreases by $12,000

John’s 8-year-old Chevrolet Trail Blazer requires repairs estimated at $10,000 to make it

road worthy again. His wife, Sherry, suggested that he should buy a 5-year-old used

Jeep Grand Cherokee instead for $10,000 cash. Sherry estimated the following costs for

the two cars:

Trail Blazer Grand Cherokee

Acquisition cost $25,000 $10,000

Repairs $10,000 —

Annual operating costs

(Gas, maintenance, insurance) $2,780 $1,800

The cost NOT relevant for this decision is the ________.

A) acquisition cost of the Trail Blazer

B) acquisition cost of the Grand Cherokee

C) repairs to the Trail Blazer

D) annual operating costs of the Grand Cherokee

Which of the following is true of historical costs?

A) They are useful for making future predictions.

B) They are relevant for decision making.

C) They are always accounted as opportunity costs.

D) They cannot be fixed costs.

The net present value method focuses on ________.

A) cash flows and required rate of return

B) inventory cost and cost of capital

C) working capital and cost of capital

D) operating income and required rate of return

Which of the following is true of an executive compensation plan?

A) The compensation paid to the executives should be linked only to the financial

performance of the company.

B) Most compensation plans are two parts: salary and health plan

C) It does not help balancing risk with short-run and long-run incentives.

D) It includes salary, annual incentive compensation, and benefits such as medical

benefits, pension plans, and life insurance.

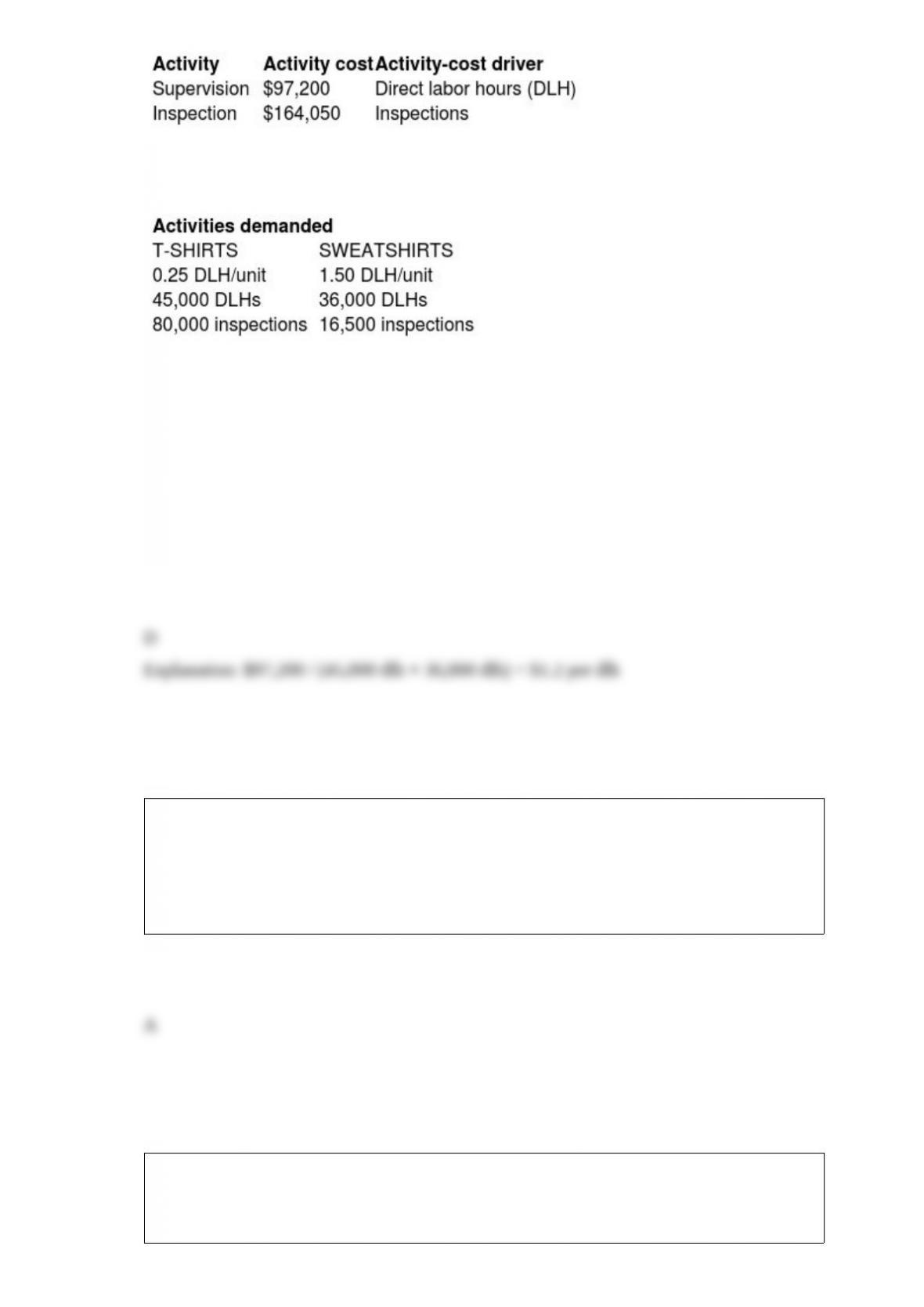

Tiger Pride produces two product lines: T-shirts and Sweatshirts. Product profitability is

analyzed as follows:

T-SHIRTS SWEATSHIRTS

Production and sales volume 180,000 units 24,000 units

Selling price $20.00 $29.00

Direct material $1.80 $ 5.00

Direct labor $4.70 $ 7.20

Manufacturing overhead $6.00 $ 3.00

Gross profit $ 7.50 $13.80

Selling and administrative $4.30 $ 7.00

Operating profit $3.20 $ 6.80

Tiger Pride’s managers have decided to revise their current assignment of overhead

costs to reflect the following ABC cost information:

Under the revised ABC system, the activity-cost driver rate for the supervision activity is

________.

A) $1.70

B) $2.70

C) $2.16

D) $1.2

One-time-only special orders should only be accepted if ________.

A) incremental revenues exceed incremental costs

B) differential revenues exceed variable costs

C) incremental revenues exceed fixed costs

D) total revenues exceed total costs

A transfer price based on the full cost plus a markup may lead to suboptimal decisions

because ________.

A) it leads the buying division to regard the fixed costs and the markup of the selling

division as a variable cost

B) it leads the buying division to regard the variable costs and the markup of the selling

division as a fixed cost

C) it leads the buying division to regard the fixed costs and the markup of the selling

division as total costs

D) it leads the buying division to regard the variable costs and the markup of the selling

division as total costs

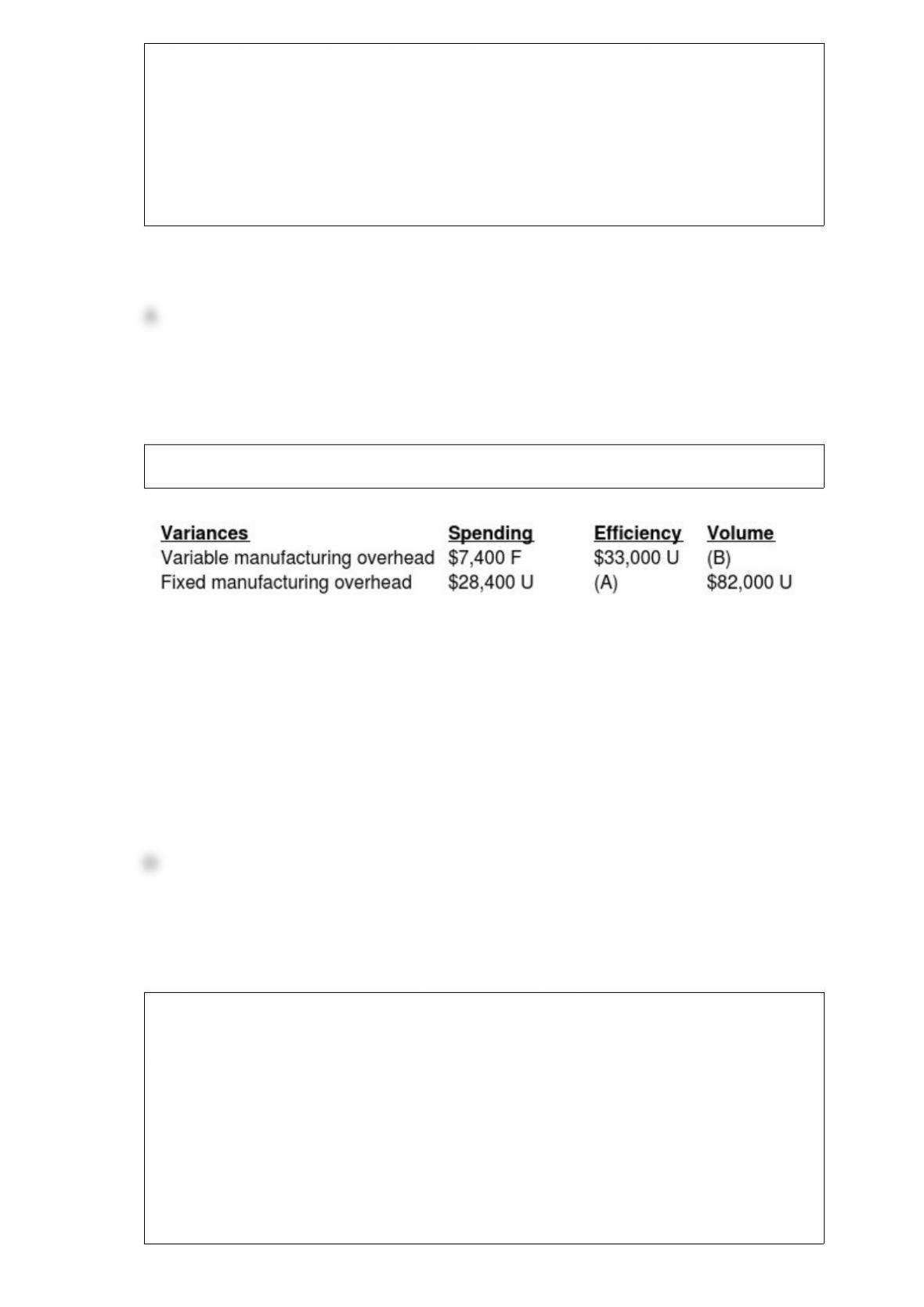

In the above table, the amounts for (A) and (B), respectively, are ________.

A) $25,600 U; $115,000 U

B) $25,600 U; Zero

C) Zero; $115,000 U

D) Zero; Zero

Place the following steps in order for estimating a cost function using quantitative

analysis.

A = Plot the data

B = Collect data on the dependent variable and the cost driver.

C = Choose the dependent variable

D = Identify the independent variable, or cost driver

E = Estimate the cost function

A) D C E A B

B) C D B A E

C) A D C E B

D) E D C B A

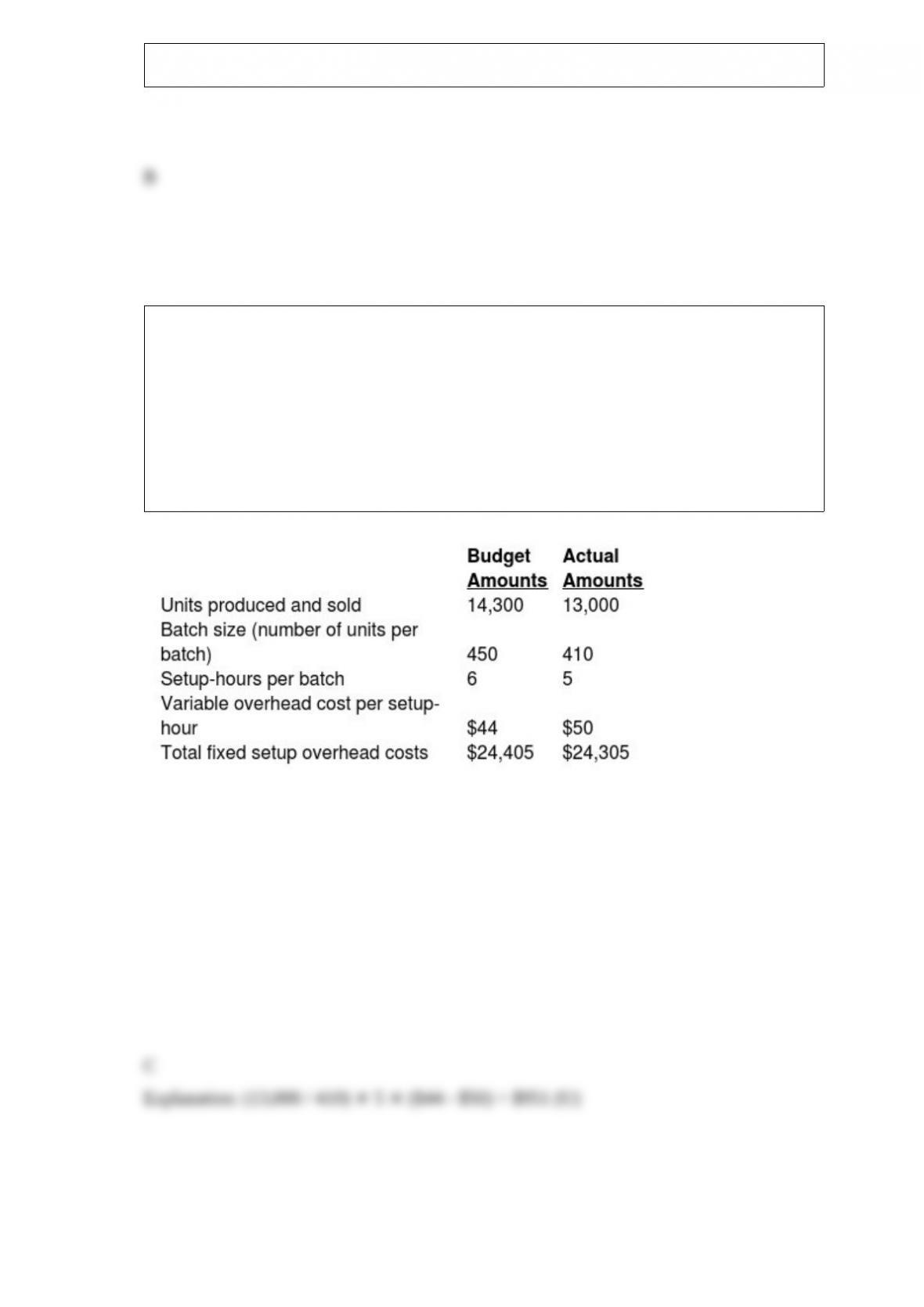

Bristol Fabricators, Inc., produces air purifiers in batches. To manufacture a batch of the

purifiers, Bristol Fabricator, Inc., must set up the machines and assembly line tooling.

Setup costs are batch-level costs because they are associated with batches rather than

individual units of products. A separate Setup Department is responsible for setting up

machines and tooling for different models of the air purifiers.

Setup overhead costs consist of some costs that are variable and some costs that are

fixed with respect to the number of setup-hours. The following information pertains to

June 2015:

Calculate the spending variance for variable overhead setup costs. (Round all intermediary

calculations two decimal places and your final answer to the nearest whole number.)

A) $651 unfavorable

B) $651 favorable

C) $951 unfavorable

D) $951 favorable

Which of the following statements is true about the factors that affect pricing decisions?

A) Information about competitors’ technologies is not useful for pricing decisions.

B) Information about a competitor in a perfect market affects pricing decisions.

C) Increase in price of a substitute product does not affect pricing decisions.

D) Managers must always be aware of the competition when pricing their products

Assembly department of Zahra Technologies had 200 units as work in process at the

beginning of the month. These units were 45% complete. It has 300 units which are

25% complete at the end of the month. During the month, it completed and transferred

600 units. Direct materials are added at the beginning of production. Conversion costs

are allocated evenly throughout production. Zahra uses weighted-average

process-costing method. What is the number of equivalent units of work done during

the month with regards to direct materials?

A) 700 units

B) 1100 units

C) 900 units

D) 600 units

A favorable variance indicates that ________.

A) budgeted costs are less than actual costs

B) actual revenues exceed budgeted revenues

C) actual operating income is less than the budgeted amount

D) budgeted contribution margin is more than the actual amount

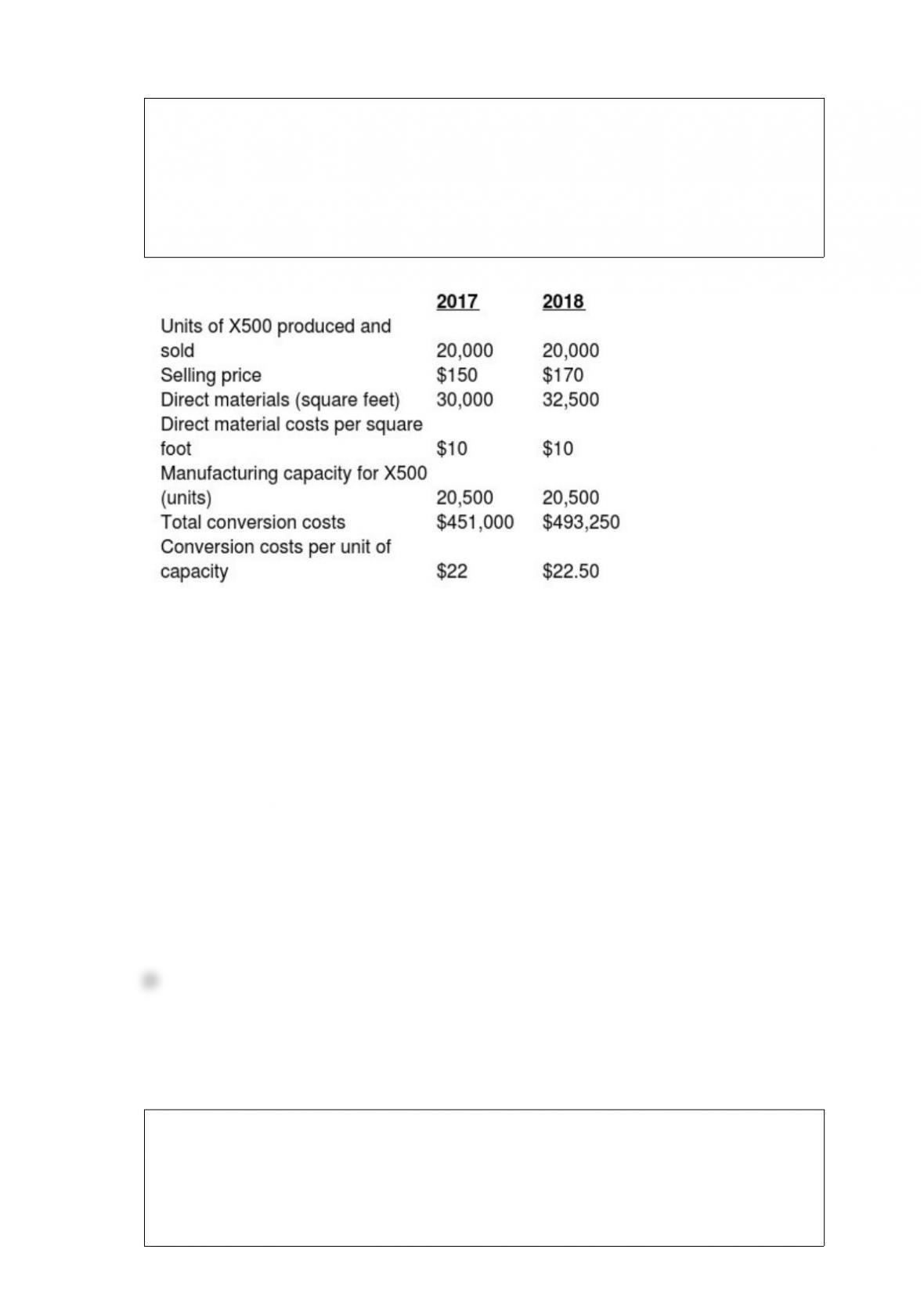

Cobalt Company makes a household appliance with model number X500. The goal for

2018 is to improve product design and outlook. No defective units are currently

produced. Manufacturing conversion costs depend on production capacity defined in

terms of X500 units that can be produced. The industry market size for appliances

increased 10% from 2017 to 2018. The following additional data are available for 2017

and 2018:

Out of the two basic strategies, Cobalt’s strategy is ________.

A) product differentiation because Cobalt is able to produce a given quantity of output

with a lower cost of inputs

B) cost leadership because Cobalt is able to produce a given quantity of output with a

lower cost of inputs

C) cost leadership because Cobalt is able to increase its output price faster than the

increase in its input prices

D) product differentiation because Cobalt is able to increase its output price faster than the

increase in its input prices

Family Furniture sells a table for $950. Its fixed costs are $2,500, while its variable

costs are $500 per table. It currently plans to sell 180 tables this month.

What is the budgeted operating income for the month assuming that Family Furniture

sells 180 tables?

A) $168,500

B) $81,000

C) $78,500

D) $171,000

In ________, fixed manufacturing costs are included as inventoriable costs.

A) variable costing

B) absorption costing

C) throughput costing

D) activity-based costing

Which of the following differentiates job costing from process costing?

A) Job costing is used when each unit of output is identical, and process costing deals

with unique products.

B) Job costing is used when each unit of output is identical and not produced in batches,

and process costing deals with unique products produced on large scale.

C) Process costing is used when each unit of output is identical, and job costing deals

with unique products not produced in batches.

D) Job costing is used by manufacturing industries, and process costing is used by

service industries.

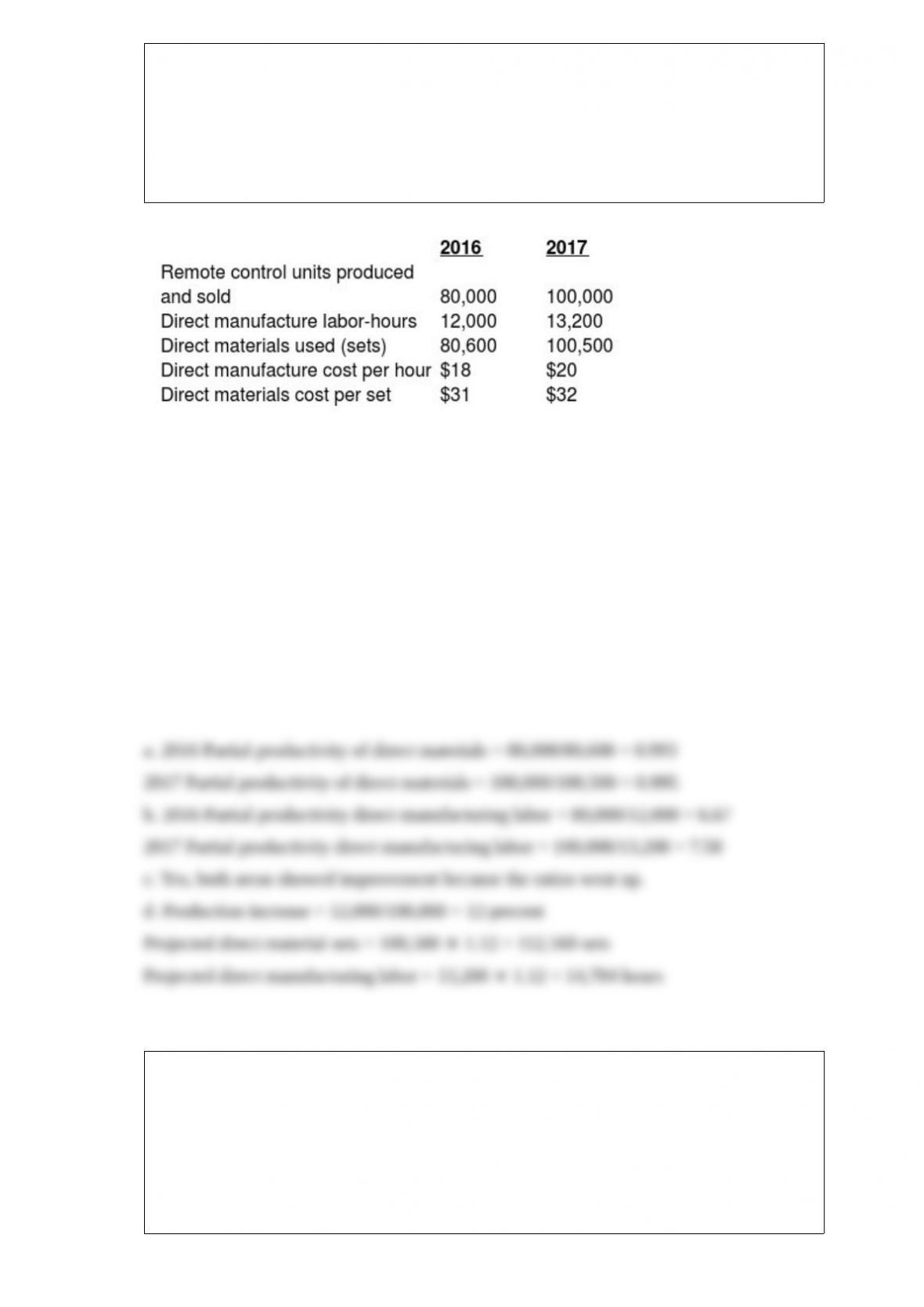

Power Company has been unhappy with the financial accounting variances that its cost

accounting system has been producing, because its managers believe that there is more

to evaluating an operation than just examining accounting numbers. Therefore, it has

started gathering data to assist in the examination of nonfinancial results of operations.

The following information relates to the manufacture of remote control units for

televisions, radios, and stereo components:

Required:

a. What is the partial productivity of direct materials for each year?

b. What is the partial productivity of direct manufacturing labor for each year?

c. Did each area improve between 2016 and 2017? Explain.

d. What will be the projected direct material and labor needs for 2013 if remote control

units increase by 12,000 units, assuming Power Company applies the constant returns to

scale technology?

Which of the following is a stage of the capital budgeting process that determines

which investment

yields the greatest benefit and the least cost to an organization?

A) make decisions by choosing among alternatives stage

B) make predictions stage

C) identify projects stage

D) implement the decision, evaluate performance, and learn stage

When using the direct allocation method, a cost accountant would ________.

A) not allocate support department costs to other support departments

B) use information about reciprocal services provided among support departments and

therefore could generate inaccurate estimates of the cost of operating departments

C) allocate complete reciprocated costs

D) allocate support department costs to other support departments

Which of the following is the basic formula of the direct materials usage budget?

A) Ending inventory of direct materials + direct materials purchased and used during

the period = direct materials to be used this period

B) Beginning inventory of direct materials + direct materials purchased and used during

the period = direct materials to be used this period

C) units used in production + target ending inventory – beginning inventory = purchases

to be made for the budget period

D) units used in production + target beginning inventory – ending inventory = purchases

to be made for the budget period

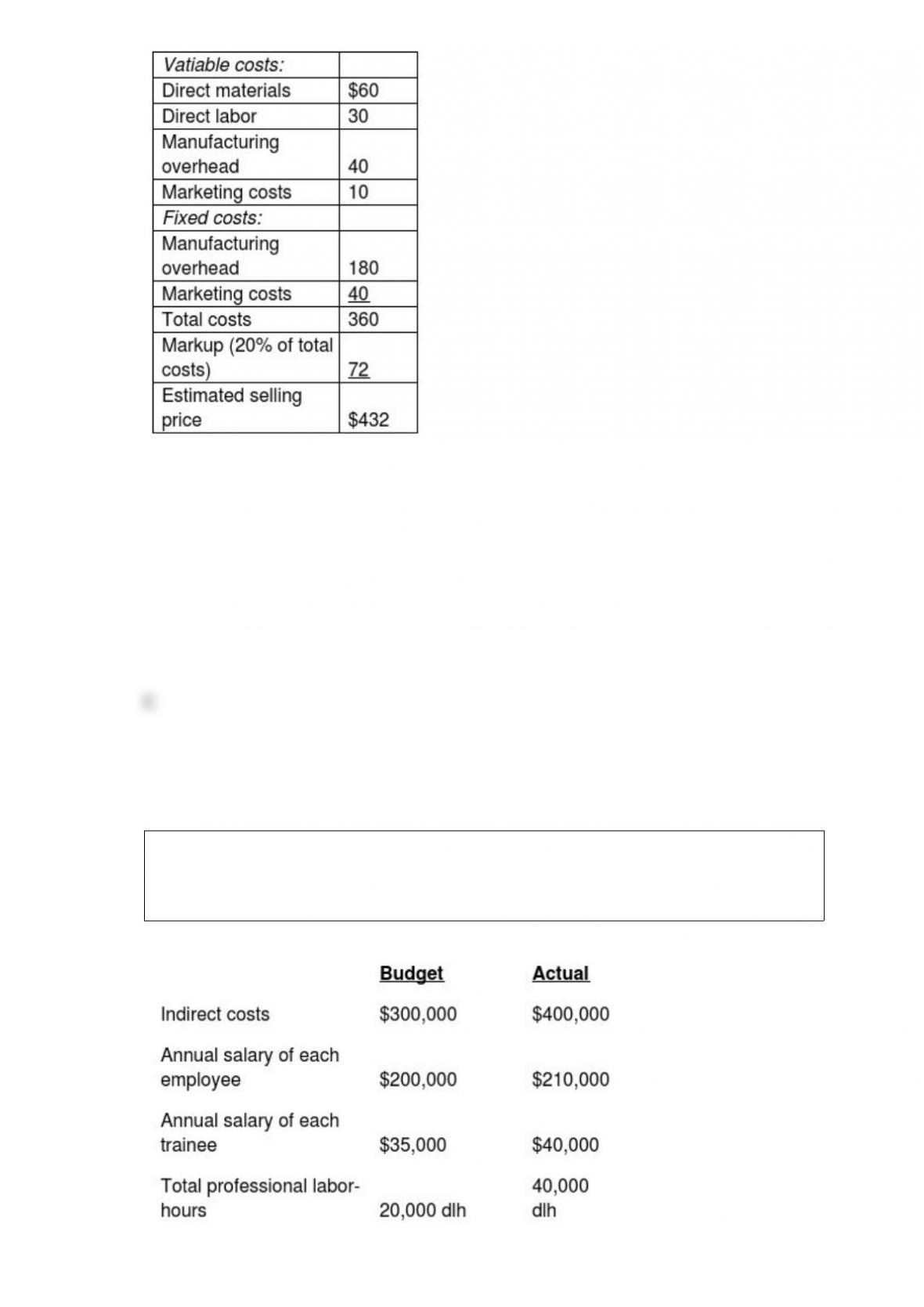

Gracius Manufacturing is approached by a European customer to fulfill a one-time-only

special order for a product similar to one offered to domestic customers. Gracius

Manufacturing has a policy of adding a 20% markup to full costs and currently has

excess capacity. The following per unit data apply for sales to regular customers:

What is the full cost of the product per unit for Gracius Manufacturing?

A) $90

B) $140

C) $360

D) $432

Elite Stationary Inc. employs 20 full-time employees and 10 trainees. Direct and

indirect costs are applied on a professional labor-hour basis that includes both employee

and trainee hours. Following is information for 2018:

What are the budgeted direct-cost rate and the budgeted indirect-cost rate, respectively, per

professional labor-hour? (Round the final answers to the nearest cent.)

A) $200.00; $16.75

B) $217.50; $15.00

C) $115.00; $10.00

D) $135.00; $10.00

The sales-quantity variance will be unfavorable when which of the following occurs?

A) the composite unit for the actual mix is less than for the budgeted mix

B) the actual unit sales are less than the budgeted unit sales

C) the actual contribution margin per unit is less than the static-budget contribution

margin

D) the actual sales mix shifts toward the less profitable units

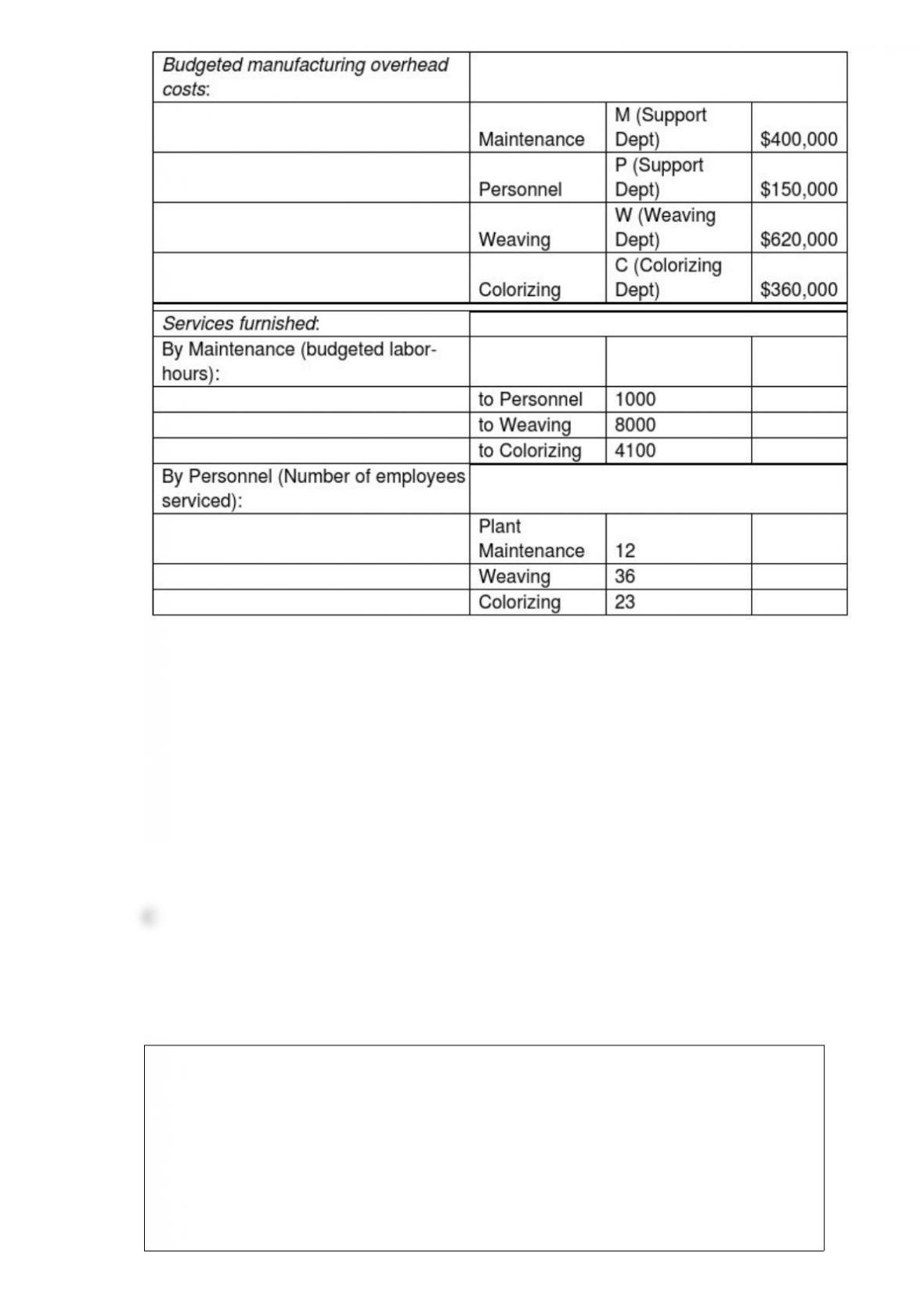

Hugo, owner of Automated Fabric, Inc., is interested in using the reciprocal allocation

method. The following data from operations were collected for analysis:

Which of the following linear equations represents the complete reciprocated cost of the

Personnel Department?

A) P = $400,000 – $150,000 (1000 / 13,100) M

B) P = (1000 / 13,100) M

C) P = $150,000 + (1000 / 13,100) M

D) P = $150,000

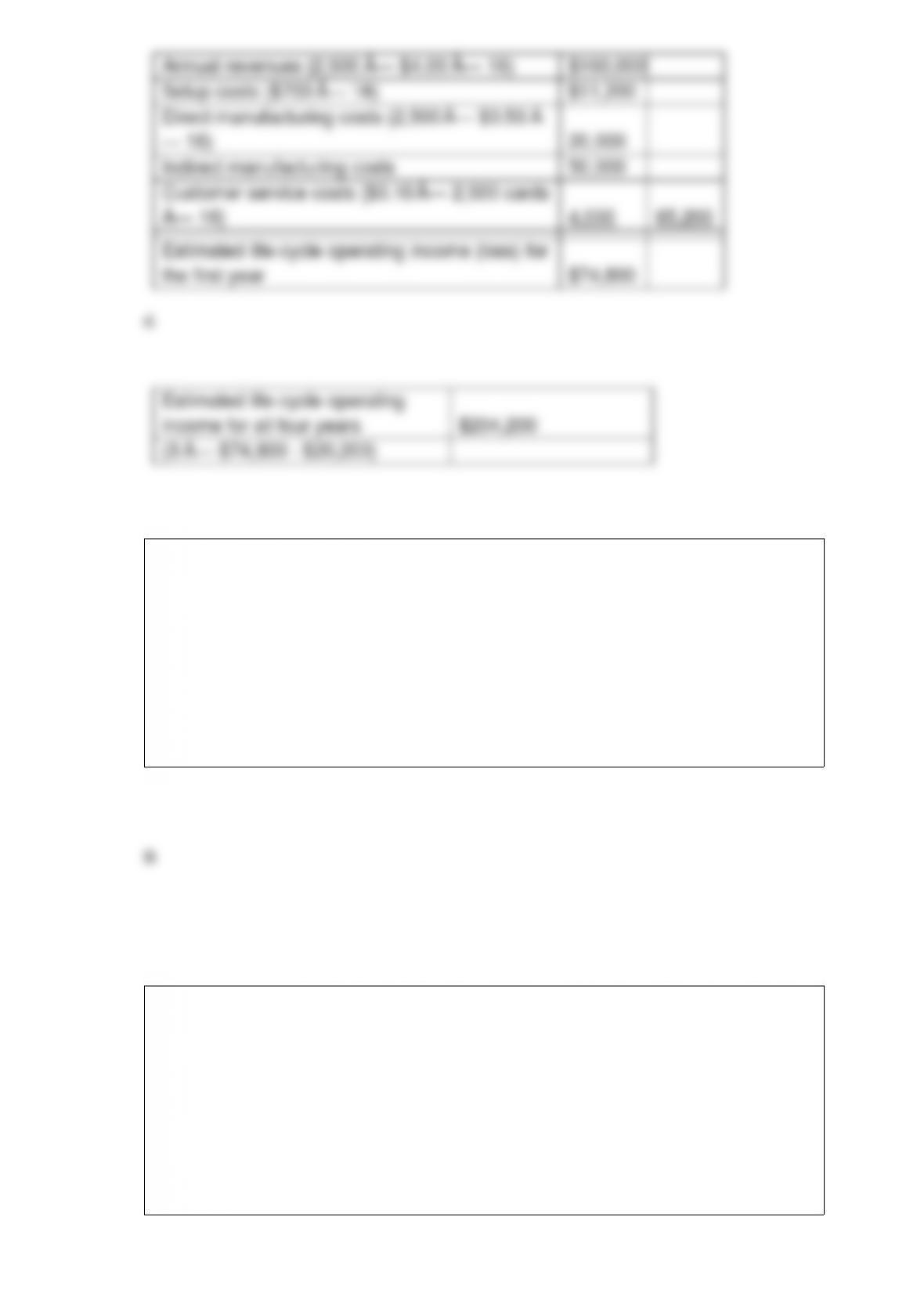

Grace Greeting Cards Incorporated is starting a new business venture and are in the

process of evaluating its product lines. Information for one new product, traditional

parchment grade cards, is as follows:

∙ Sixteen times each year, a new card design will be put into production. Each new

design will require $700 in setup costs.

∙ The parchment grade card product line incurred $75,000 in development costs and

is expected to be produced over the next four years.

∙ Direct costs of producing the designs average $0.50 each.

∙ Indirect manufacturing costs are estimated at $50,000 per year.

∙ Customer service expenses average $0.10 per card.

∙ Current sales are expected to be 2,500 units of each card design. Each card sells for

$4.00.

∙ Sales units equal production units each year.

Required:

a. What are the estimated life-cycle revenues?

b. What is the estimated life-cycle operating income for the first year?

c. What is the estimated life-cycle operating income per year for the years after the first

year?

d. What is the total estimated life-cycle operating income?

Advanced Technology Products produces 10 different fastners. Each time a type of

fastener is produced, the equipment must be stopped and items such as filters and drill

bits must be changed, oil must be added to the equipment and some parts need

lubrication. This work must be done before the products can be produced, the costs

related to this activity would be part of which cost pool?

A) Output-level costs

B) Batch-level costs

C) Product-sustaining costs

D) Service-sustaining costs

While-You-Train is a not-for-profit organization that aids the unemployed by

supplementing their incomes by $7,000 annually, while they seek new employment

skills. The organization has fixed costs of $200,000 and the budgeted appropriation for

the year totals $750,000. How many individuals can receive financial assistance this

year?

A) 29 people

B) 108 people

C) 79 people

D) 136 people

LaCrosse Products has a budget of $904,000 in 2017 for prevention costs. If it decides

to automate a portion of its prevention activities, it will save $80,500 in variable costs.

The new method will require $40,900 in training costs and $109,000 in annual

equipment costs. Management is willing to adjust the budget for an amount up to the

cost of the new equipment. The budgeted production level is 154,000 units.

Appraisal costs for the year are budgeted at $610,000. The new prevention procedures

will save appraisal costs of $50,100. Internal failure costs average $16 per failed unit of

finished goods. The internal failure rate is expected to be 4% of all completed items.

The proposed changes will cut the internal failure rate by one-third. Internal failure

units are destroyed. External failure costs average $56 per failed unit. The company’s

average external failures average 4% of units sold. The new proposal will reduce this

rate by 45%. Assume all units produced are sold and there are no ending inventories.

How much will appraisal costs change assuming the new prevention methods reduce

material failures by 40% in the appraisal phase?

A) $149,900 decrease

B) $69,400 increase

C) $50,100 decrease

D) $32,853 decrease

Which of the following is a problem related to cost analysis?

A) fixed costs are allocated as if they are variable costs

B) extreme observations are adjusted or removed

C) a company keeps accounting records on the accrual basis

D) inflationary effects are removed

The gross margin percentage is an example of the ________ measure of a

balanced-scorecard.

A) internal business process perspective

B) customer perspective

C) learning and growth perspective

D) financial perspective

Acme Janitor Service has always taken pride in the fact that it had one of the highest

customer response times in the home cleaning service industry. However, as the

products manufactured for this industry have become more complex, the company’s

customer response time has declined.

Required:

Why do you think that response time declined if all other quality factors have remained

the same?

What are the implications of JIT and backflush costing systems for activity-based

costing (ABC) systems?

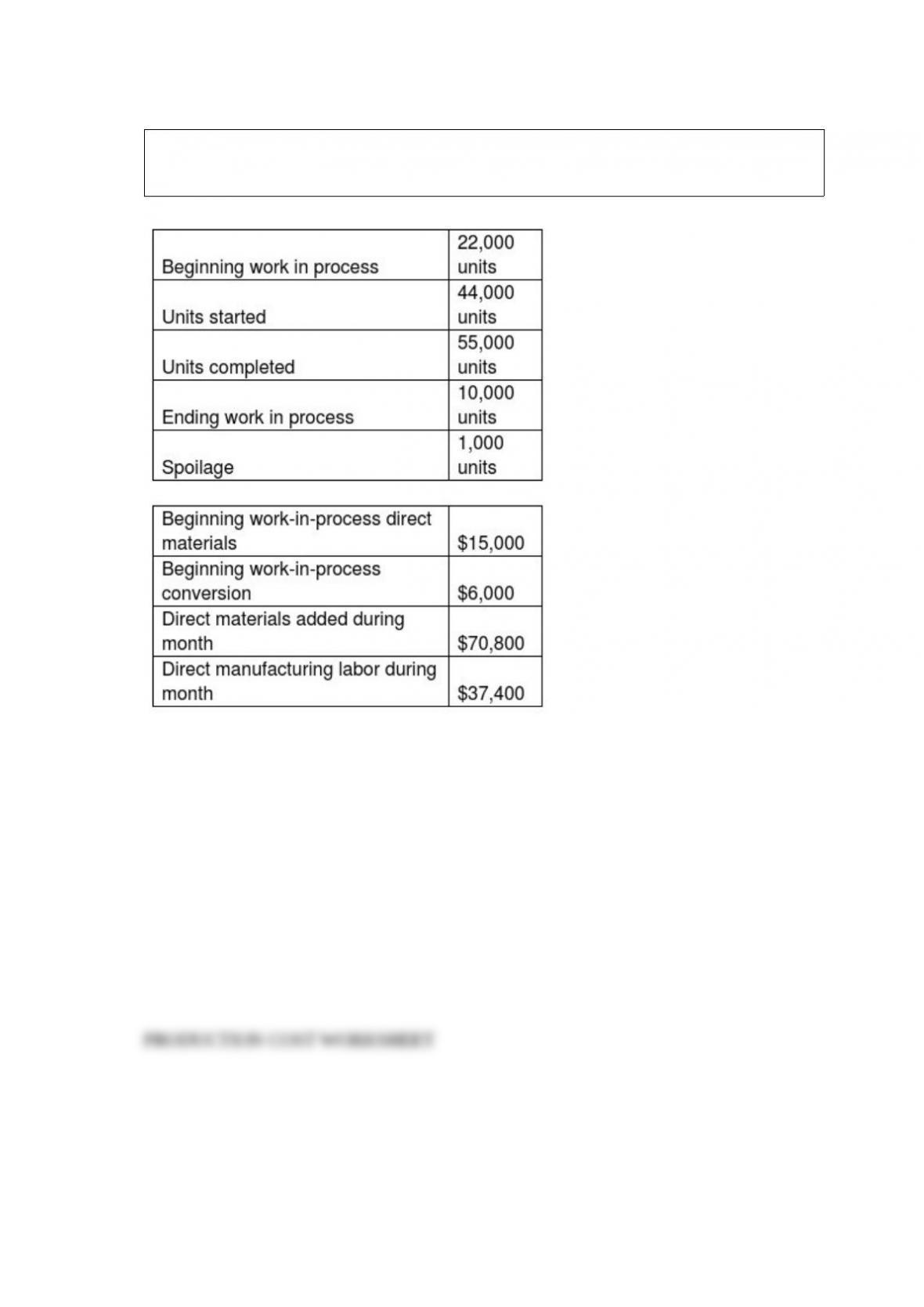

Venosis Sports is a manufacturer of sportswear. It produces all of its products in one

department. The information for the current month is as follows:

Beginning work in process was half complete as to conversion. Direct materials are added

at the beginning of the process. Factory overhead is applied at a rate equal to 50% of direct

manufacturing labor. Ending work in process was 60% complete. All spoilage is normal

and is detected at end of the process.

Required:

Prepare a production cost worksheet if spoilage is recognized and the weighted-average

method is used.

Define variable overhead spending variance. Briefly explain why a favorable variable

overhead spending variance may not always be desirable.

Cost accounting provides information for both management accounting and financial

accounting professionals. Explain.

The Laramie Factory produces expensive boots. It has two departments that process all

the items. During January, the beginning work in process in the tanning department was

40% complete as to conversion and 100% complete as to direct materials. The

beginning inventory included $6,000 for materials and $18,000 for conversion costs.

Ending work-in-process inventory in the tanning department was 40% complete. Direct

materials are added at the beginning of the process.

Beginning work in process in the finishing department was 60% complete as to

conversion. Beginning inventories included $7,000 for transferred-in costs and $10,000

for conversion costs. Ending inventory was 30% complete.

Additional information about the two departments follows:

Required:

Prepare a production cost worksheet using weighted-average costing for the finishing

department.

The following data for the telephone company pertain to the production of 450 rolls of

telephone wire during June. Selected items are omitted because the costing records

were lost in a windstorm.

Direct Materials (All materials purchased were used.)

Standard cost per roll: a pounds at $4.00 per pound.

Total actual cost: b pounds costing $9,600.

Standard cost allowed for units produced was $9,000.

Materials price variance: c .

Materials efficiency variance was $80 unfavorable.

Direct Manufacturing Labor

Standard cost is 3 hours per roll at $8.00 per hour.

Actual cost per hour was $8.25.

Total actual cost: d .

Labor price variance: e .

Labor efficiency variance was $400 unfavorable.

Required:

Compute the missing elements in the report represented by the lettered items.

Explain two concerns when interpreting the production-volume variance as a measure

of the economic cost of unused capacity.

What are the arguments for prorating a production-volume variance that has been

deemed to be material among work-in-process, finished goods, cost and cost of goods

sold as opposed to writing it all off to cost of goods sold?

Benny Industries allocates manufacturing overhead at a predetermined rate of 160% of

direct labor cost. Any overallocated or underallocated overhead is closed to the cost of

goods sold at the end of the month. Below is information on job 205 that was in process

at the end of the month of October

Direct materials $4,000

Direct labor $3,000

Allocated manufacturing overhead $4,800

Jobs 206, 207, and 208 were started in November. Direct materials that were used in

November were $26,000 and direct labor costs were $21,000. For the month of

November, actual manufacturing overhead was $32,000. The only job still in process on

the last day of November was job 104 with the following costs: $3,000 for direct

materials and $1,500 for direct labor.

Required:

Calculate the cost of goods manufacturered for November.

What is sales mix? How do companies choose their sales mix?

Describe both variable and fixed costs. Explain why the distinction between variable

and fixed costs is important in cost accounting.

Describe operating and financial budgets and give at least two examples of each

discussed in the textbook.

What are the four key perspectives in the balanced scorecard?

The successful management accountant possesses several skills and characteristics that

reach well beyond

basic analytical abilities. Discuss.

Cast Iron Stove Company wants to buy a molding machine that can be integrated into

its computerized manufacturing process. It has received three bids for the machine and

related manufacturer’s specifications. The bids range from $3,500,000 to $3,550,000.

The estimated annual savings of the machines range from $260,000 to $270,000. The

payback periods are almost identical and the net present values are all within $8,000 of

each other. The president just doesn’t know what to do about which vendor to choose

since all of the selection criteria are so close together.

Required:

What suggestions do you have for the president?