In the banking industry, depositing a customer’s check into the wrong bank account is

an example of quality of design failure.

With disregard to all other factors, the use of high-quality raw materials is likely to

result in a favorable efficiency variance and an unfavorable price variance.

The nominal approach to incorporating inflation into the net present value method

predicts cash inflows in real monetary units and uses a real rate as the required rate of

return.

Contribution margin percentage equals the unit contribution margin divided by the

selling price.

A company with a higher degree of operating leverage is at greater risk during

economic downturns because of its higher fixed costs.

Jacob’s Manufacturing sales is equal to production.If Jacob’s Manufacturing presented a

Financial Accounting Income Statement emphasizing gross margin showing operating

income of $180,000. A Contribution Income Statement emphasizing contribution

margin would show a different operating income.

Management control systems utilize information gathered within a company and from

external sources so as to aid management with their planning and control decision

making.

The reorder point is the quantity level of inventory at which a new purchase order is

made.

An activity-based costing system may focus on customers rather than products.

Kaizen budgeting can be applied to activities such as setups with the goal of reducing

setup time and setup costs.

Indirect labor and distribution costs would most likely be in the same activity-cost pool.

While calculating terminal recovery of working capital there are no tax consequences as

there is no gain or loss on working capital.

Balanced scorecards show reveal as many measures as possible to connect objectives

with measures and initiatives to help assure the success of the enterprise.

Management accountants should have little or no role in deciding on a company’s

strategy.

There is no difference between scrap which can be sold for relatively small amount and

a byproduct.

ABC costing systems cannot be used in marketing decisions.

If fixed overhead cost variances are always written off to Cost of Goods Sold, operating

income can be manipulated for either financial reporting or income tax purposes.

An example of a financial measure of customer satisfaction would be the percentage of

defective products produced during a particular month.

Estimating the degree of completion for the calculation of equivalent units is usually

easier for conversion costs than it is for direct materials.

The DuPont method recognizes the two basic ingredients in profit making: increasing

the income per dollar of revenues and using assets to generate more revenues.

When the price of a product does not change as a result of changes in demand, the price

insensitivity to demand is called demand inelasticity.

Standard costing is NOT possible in a firm that uses process costing.

A decision model is an informal method for making a choice, using simpler methods

like surveying.

Cost of goods sold for a manufacturer is calculated as follows: beginning finished

goods + cost of goods manufacturered – ending finished goods.

A revenue driver is a variable, such as volume, that causally affects revenues.

The risk-return tradeoff across alternative cost structures can be measured as operating

leverage.

Studies show that variance analysis is no longer a popular tool of corporate managers as

they have adopted various other forms of performance evaluation.

In a make-or-buy decision when there are alternative uses for capacity, the opportunity

cost of idle capacity is relevant.

In hybrid-costing systems, managers use process costing to account for the conversion

costs and job costing for the material and customizable components.

Activity based costing (ABC) systems are less useful than the theory of constraints

(TOC) for long-run pricing, cost control, and capacity management.

Contribution Margin = Total revenues – Total variable costs

Technological innovation has led to shorter product-life cycles and increased the need

to bring new products to market more rapidly.

A cost may be direct for one cost object and indirect for another cost object.

The price variance is the difference between the actual price and the budgeted price of

the input, multiplied by the actual quantity of input.

If budgeted and actual machine hours are equal, spending variance will always be nil.

Spoilage and rework costs are thoroughly captured in the accounting system.

Capital budgeting is both a decision making and control tool. Which of the following is

an example of capital budgeting as a control tool?

A) A company uses capital budgeting techniques to evaluate a group of prospective

alternative projects.

B) A large manufacturer sets up a “capital relief” fund to help supplement sustainability

projects that would not meet targeted rates of returns without the capital relief fund

assistance.

C) When considering capital expenditures, a company looks at a minimum of six

potential (alternative) projects.

D) A company’s capital project is not meeting the level of profitability expected, will

not meet the targeted NPV, and is abandoned.

If Beta Corp’s net income is $230,000 and the tax rate is 40%, then the company’s

planned operating income is ________.

A) $322,000

B) $383,333

C) $193,200

D) $552,000

Market-share variance = $380,000 (U); Market-size variance = $250,000 (F); Sales-mix

variance = $640,000 (F); calculate the sales-quantity variance.

A) $380,000 (F)

B) $630,000 (F)

C) $10,000 (F)

D) $130,000 (U)

An example of allocating joint costs using physical measures is allocating joint costs

based on the ________.

A) sales value at split-off point

B) volume of the products produced

C) constant gross-margin percentage

D) net realizable value

Which of the following is true of long-run pricing?

A) It is fixed at a level that recovers the variable cost of the company and a

pre-determined profit markup.

B) It is generally a function of the market factors and the cost involved in production is

generally not a consideration.

C) It is a strategic decision designed to build long-run relationships with customers

based on stable and predictable prices.

D) It is based only on internal requirements like cost and estimated rate of return as in

the long run these requirements are the driving factors of any organization.

Which of the following is the most frequently used budget periods used in business?

A) a basic budget period of 1 year often subdivided into semi-annual periods

B) a basic budget period of 2 years often subdivided into quarters and semi-annual

periods

C) A basic budget period of 2 years subdivided into monthly periods

D) a basic budget period of 1 year often subdivided into quarters and months

Which of the following statements best defines a just-in-time production system?

A) a push-through system that manufactures finished goods for inventory on the basis

of demand forecasts

B) a push-through system in which each component in a production line is produced

immediately as needed by the next step in the production line

C) a demand-pull system that manufactures finished goods for inventory on the basis of

demand forecasts

D) a demand-pull system in which each component in a production line is produced

immediately as needed by the next step in the production line

When making pricing decisions managers should include fixed cost per unit in the cost

because ________.

A) it leads to reporting higher operating income for the period

B) it allows managers to report positive contribution as long as prices are above

variable costs

C) in the long run, the price of a product must exceed the full cost of the product

D) it requires the management accountant to perform a detailed analysis of

cost-behavior patterns to separate product costs into variable and fixed components

Put the following ABC implementation steps in order ________.

A Compute the allocation rates.

B Compute the total cost of the products.

C Identify the products that are the cost objects.

D Select the cost allocation bases.

A) DACB

B) DBCA

C) BADC

D) CDAB

Columbus Company provides the following ABC costing information:

The above activities used by their three departments are:

How much of the labor cost will be assigned to the Bush Department?

A) $127,400

B) $63,700

C) $200,900

D) $97,825

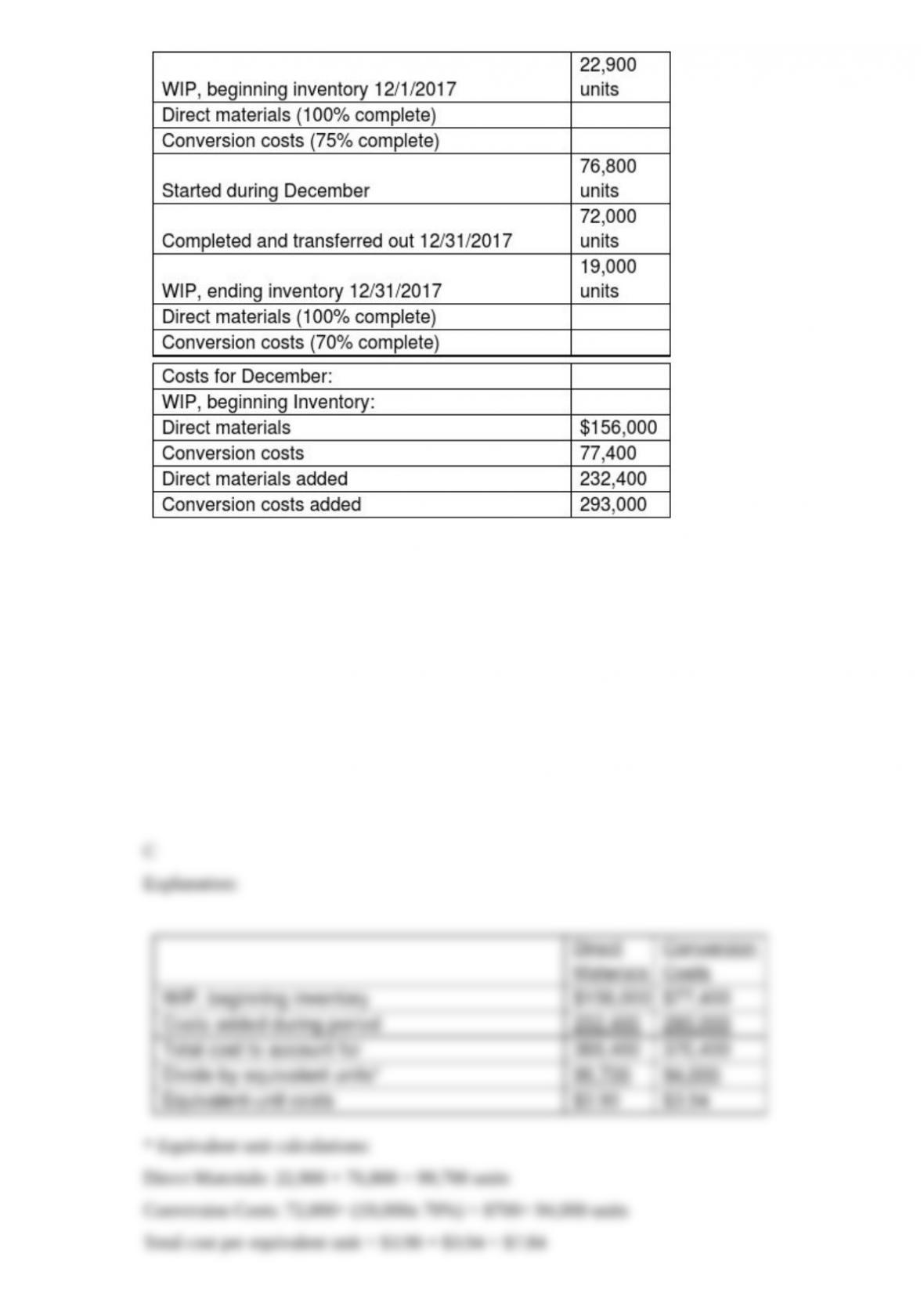

Outose Concept manufactures small tables in its Processing Department. Direct

materials are added at the initiation of the production cycle and must be bundled in

single kits for each unit. Conversion costs are incurred evenly throughout the

production cycle. Before inspection, some units are spoiled due to undetectable

materials defects. Inspection occurs when units are 55% converted. Spoiled units

generally constitute 5% of the good units. Data for December 2017 are as follows:

What is the amount of direct materials and conversion costs assigned to ending work in

process using the weighted-average process-costing method? (Round any cost per unit

calculations to the nearest cent.)

A) $40,484; $49,644

B) $74,860; $51,870

C) $74,100; $52,402

D) $156,293; $12,620

When fixed overhead spending variance is unfavorable, it can be safely assumed that

________.

A) flexible budget amount is higher than actual costs incurred

B) fixed overhead allocated for actual output is lower than actual costs incurred

C) flexible budget amount is lower than actual costs incurred

D) fixed overhead allocated for actual output is higher than actual costs incurred

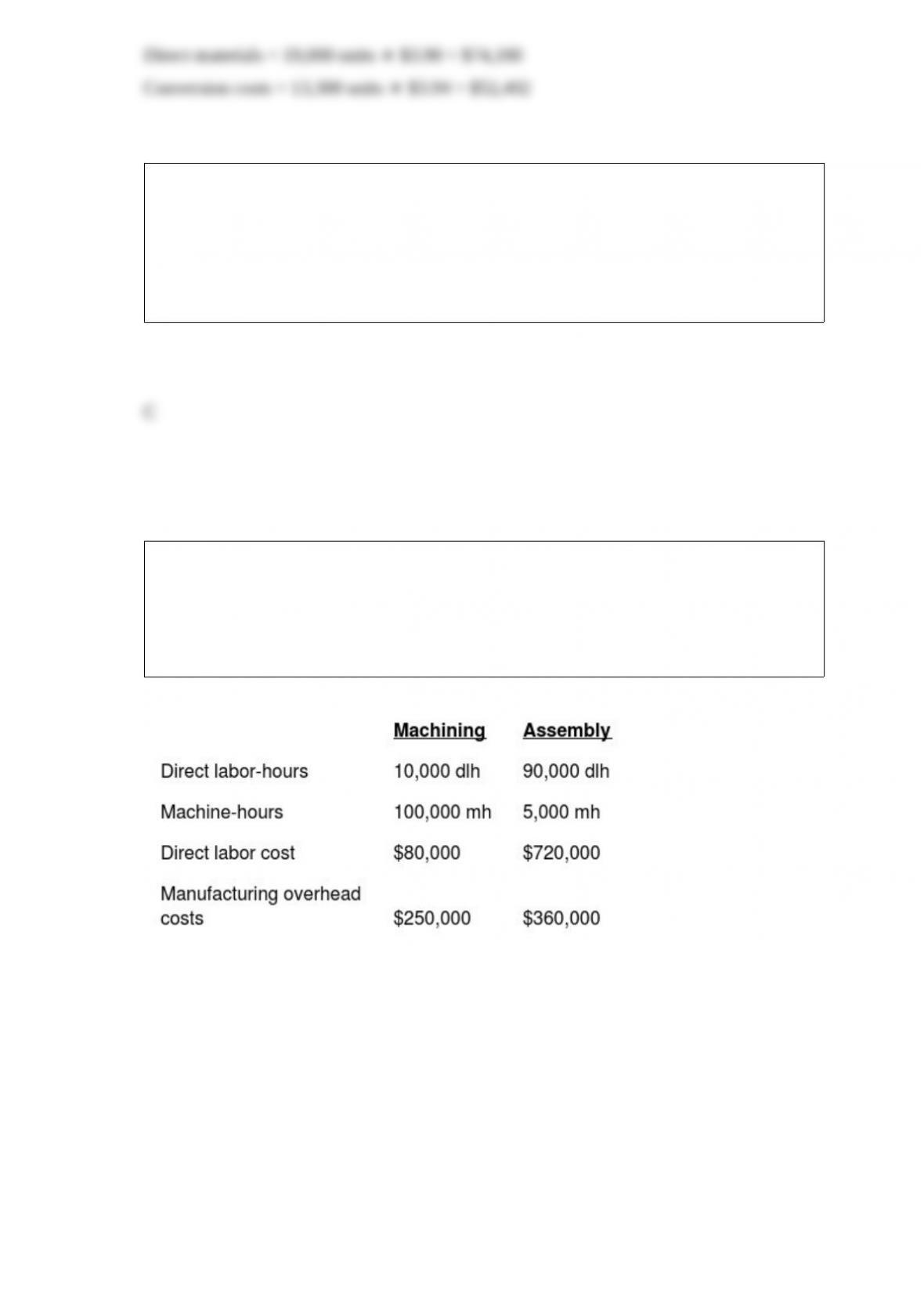

Hill Manufacturing uses departmental cost driver rates to apply manufacturing

overhead costs to products. Manufacturing overhead costs are applied on the basis of

machine-hours in the Machining Department and on the basis of direct labor-hours in

the Assembly Department. At the beginning of 2018, the following estimates were

provided for the coming year:

The accounting records of the company show the following data for Job #846:

Required:

a. Compute the manufacturing overhead allocation rate for each department.

b. Compute the total cost of Job #846.

c. Provide possible reasons why Hill Manufacturing uses two different cost allocation

rates.

For external reporting ________.

A) costs are classified as either inventoriable or period costs

B) costs reflect current values

C) there are no prescribed rules since no one is exactly sure how investors and creditors

will use these numbers

D) costs include amounts that reflect both current and future benefits

McMurphy Corporation produces a part that is used in the manufacture of one of its

products. The costs associated with the production of 12,000 units of this part are as

follows:

Direct materials $86,000

Direct labor 126,000

Variable factory overhead 58,000

Fixed factory overhead 138,000

Total costs $408,000

Of the fixed factory overhead costs, $55,000 is avoidable. Conners Company has

offered to sell 12,000 units of the same part to McMurphy Corporation for $41 per unit.

Assuming there is no other use for the facilities, Schmidt should ________.

A) make the part, as this would save $16 per unit

B) buy the part, as this would save $16 per unit

C) buy the part, as this would save the company $192,000

D) make the part, as this would save $14 per unit

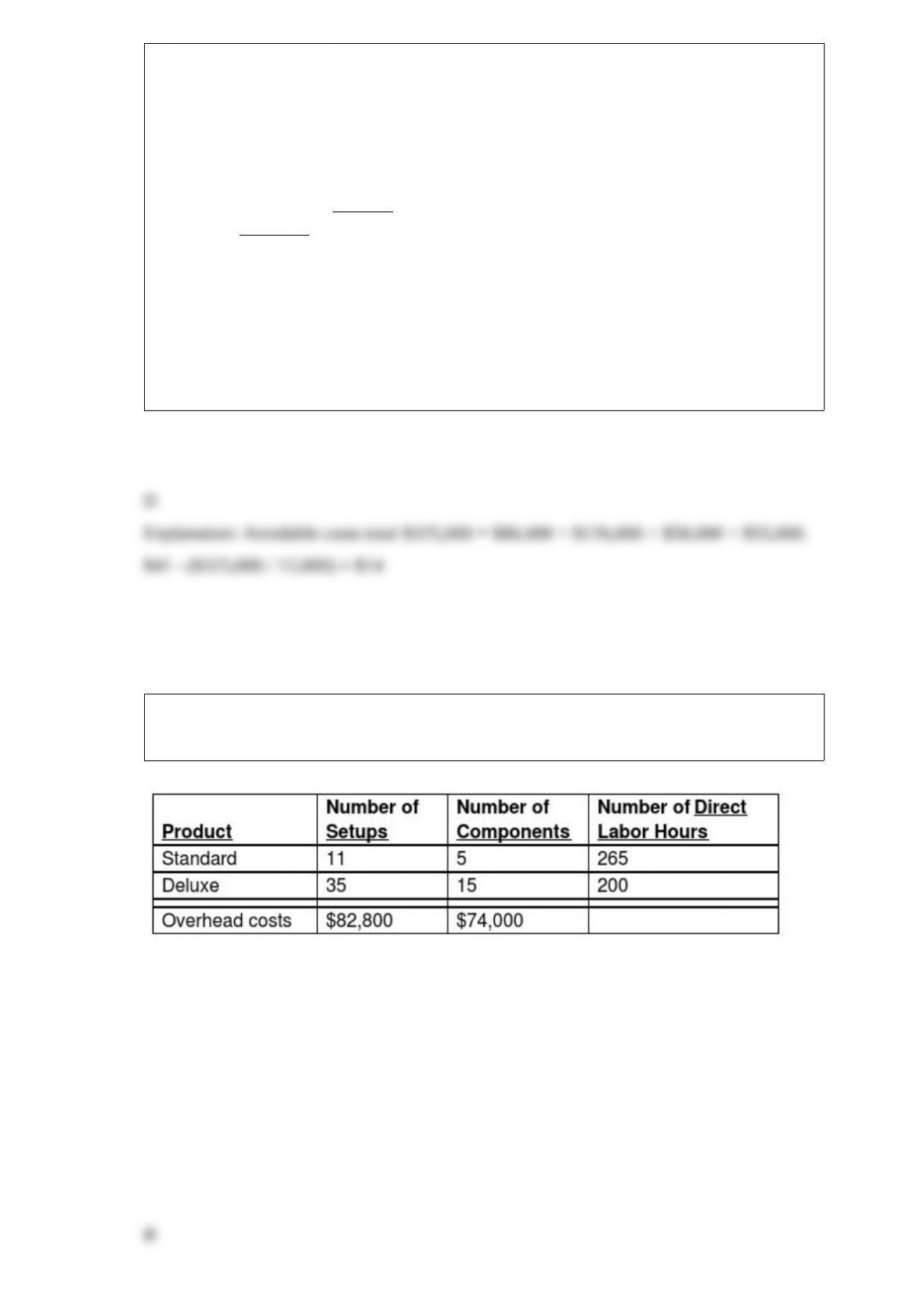

Dartmouth Corporation manufactures two models of office chairs, a standard and a

deluxe model. The following activity and cost information has been compiled:

Assume a traditional costing system applies the overhead costs based on direct labor hours.

What is the total amount of overhead costs assigned to the deluxe model?

A) $31,828

B) $67,441

C) $35,613

D) $78,400

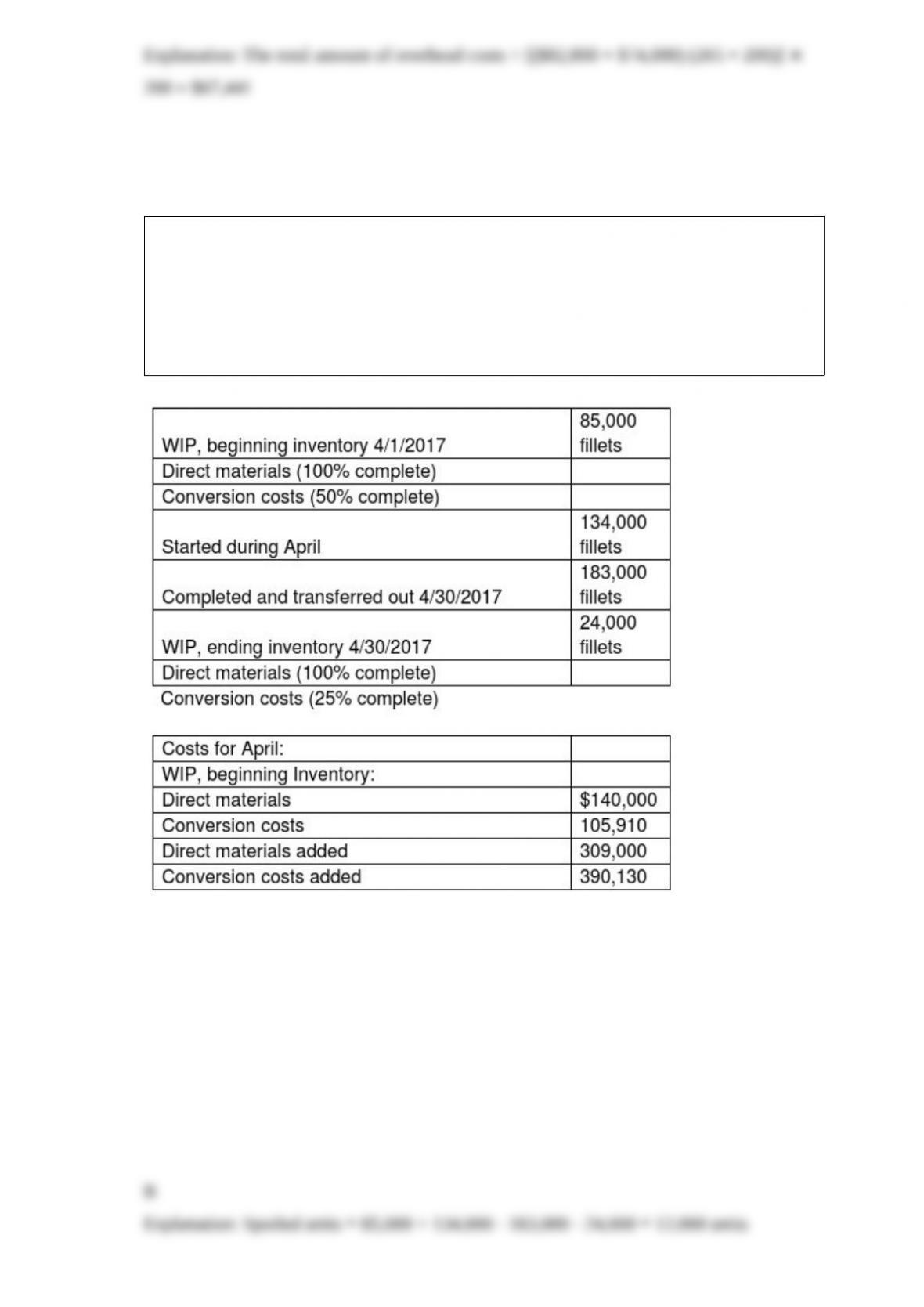

Fish Fillet Incorporated obtains fish and then processes them into frozen fillets and then

prepares the frozen fish fillets for distribution to its retail sales department. Direct

materials are added at the initiation of the cycle. Conversion costs are incurred evenly

throughout the production cycle. Before inspection, some fillets are spoiled due to

undetectable defects. Inspection occurs when units are 40% converted. Spoiled fillets

generally constitute 6% of the good fillets. Data for April 2017 are as follows:

What cost is allocated to abnormal spoilage using the weighted-average process-costing

method? (Round any cost per unit calculations to the nearest cent.)

A) $ 0

B) $4610

C) $2091

D) $2106

Speedy Dress Manufacturing has two workstations, cutting and finishing. The cutting

station is limited by the speed of operating the cutting machine. Finishing is limited by

the speed of the workers. Finishing normally waits for work from cutting. Each

department works an eight-hour day. If cutting begins work two hours earlier than

finishing each day, the two departments generally finish their work at about the same

time. Not only does this eliminate the bottleneck, but also it increases finished units

produced each day by 210 units. All units produced can be sold even though the change

increases inventory stock by 15% from 430 units. The cost of operating the cutting

department two more hours each day is $1430. The contribution margin of the finished

products is $12 each. Inventory carrying costs are $0.50 per unit per day.

What is the change in the daily contribution margin if the change is made?

A) $684

B) $703

C) $1058

D) $715

In decentralized organizations, a manager might look to further the success of their

subunit to the detriment of other subunits. Such behavior would be from which of the

following results of decentralization?

A) duplication of output

B) gains from raid decision making

C) unhealthy competition

D) broadening the reach of top management

The budgeted fixed manufacturing cost rate is the lowest for ________.

A) practical capacity

B) theoretical capacity

C) master-budget capacity utilization

D) normal capacity utilization

Which of the following describes reciprocal support?

A) the accounting department provides services to production

B) molding provides services to production and accounting provides services to both

molding and production

C) assembling department provides services to three other departments

D) the materials management department provides support to all departments including

the production control department which also provides services to the materials

management department

Which component of strategy measures the changes in operating income attributed

solely to an increase in the quantity of output between Year 1 and Year 2?

A) the growth component

B) the price-recovery component

C) the productivity component

D) the cost leadership component

Under the writeoff approach, the difference between Manufacturing Overhead Control

and Manufacturing Overhead Allocated is adjusted in the ________.

A) Cost of Goods Sold account

B) Work-in Process account

C) Manufacturing Overhead account

D) Miscellaneous Expenses account

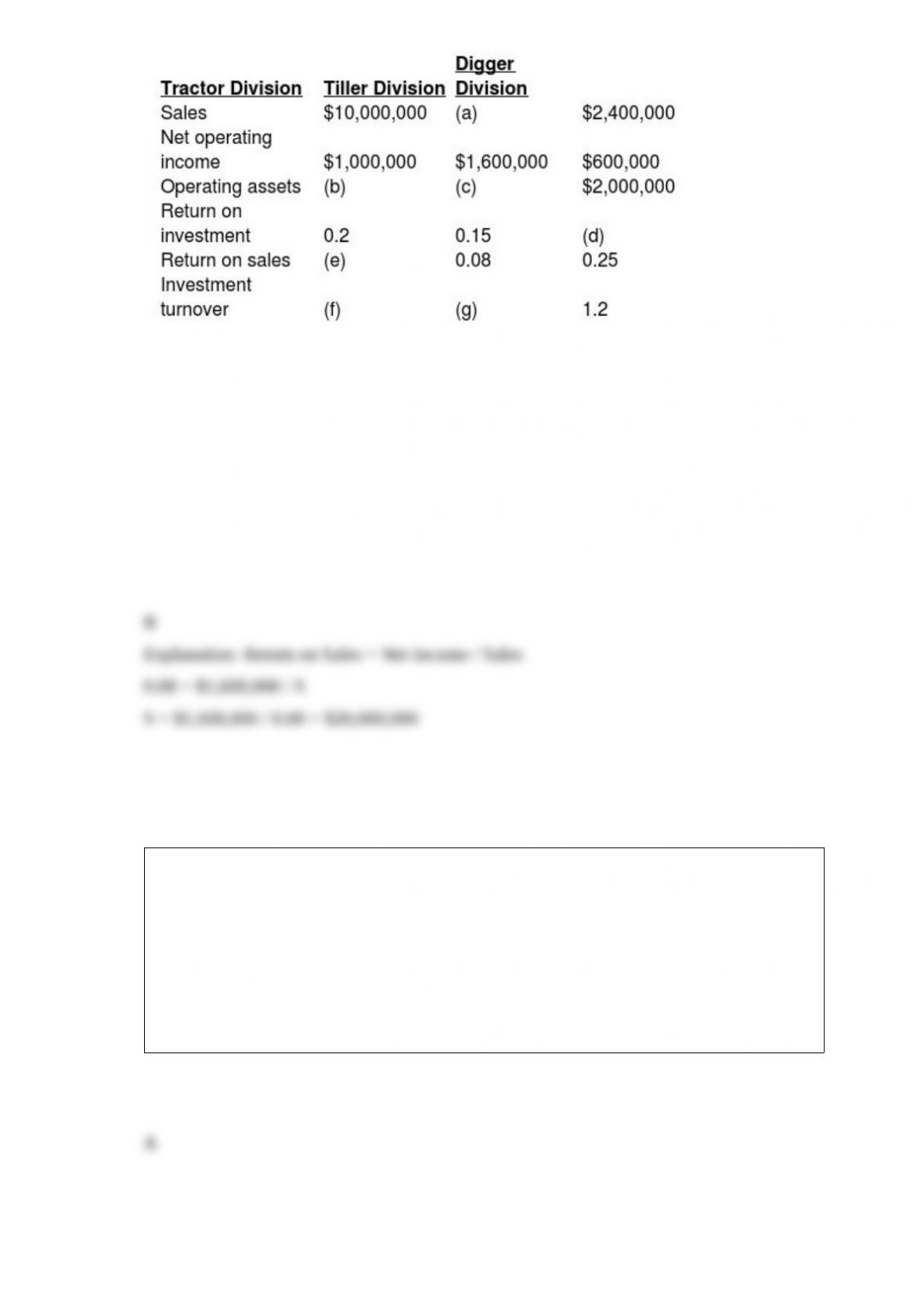

The top management at Groundsource Company, a manufacturer of lawn and garden

equipment, is attempting to recover from a fire that destroyed some of their accounting

records. The main computer system was also severely damaged. The following

information was salvaged:

What were the sales for the Tiller Division? (Round the final answer to the nearest whole

dollar.)

A) $10,666,667

B) $20,000,000

C) $3,000,000

D) $853,333

Which of the following best describes the stand-alone revenue-allocation method?

A) uses product-specific information on the products in the bundle as weights for

allocating the bundled revenues to the individual products

B) ranks individual products in a bundle according to criteria determined by

management

C) ranks individual products in a bundle according to costs allocated to the products

D) survey customers about the importance of each of the individual products in their

purchase decision

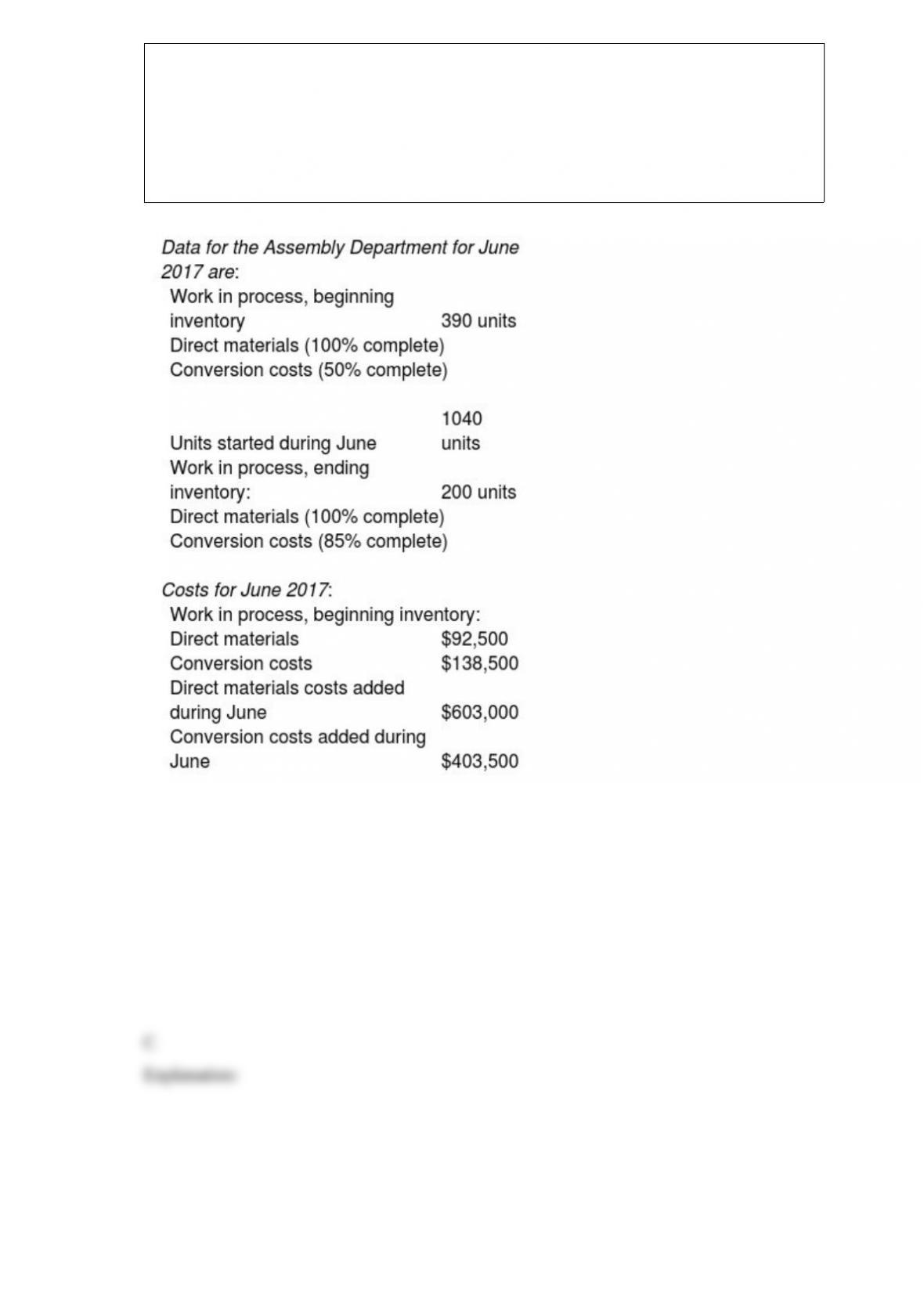

Timekeeper Inc. manufactures clocks on a highly automated assembly line. Its costing

system uses two cost categories, direct materials and conversion costs. Each product

must pass through the Assembly Department and the Testing Department. Direct

materials are added at the beginning of the production process. Conversion costs are

allocated evenly throughout production. Timekeeper Inc. uses weighted-average

costing.

What is the conversion cost per equivalent unit in June?

A) $482.99

B) $659.27

C) $387.14

D) $354.51

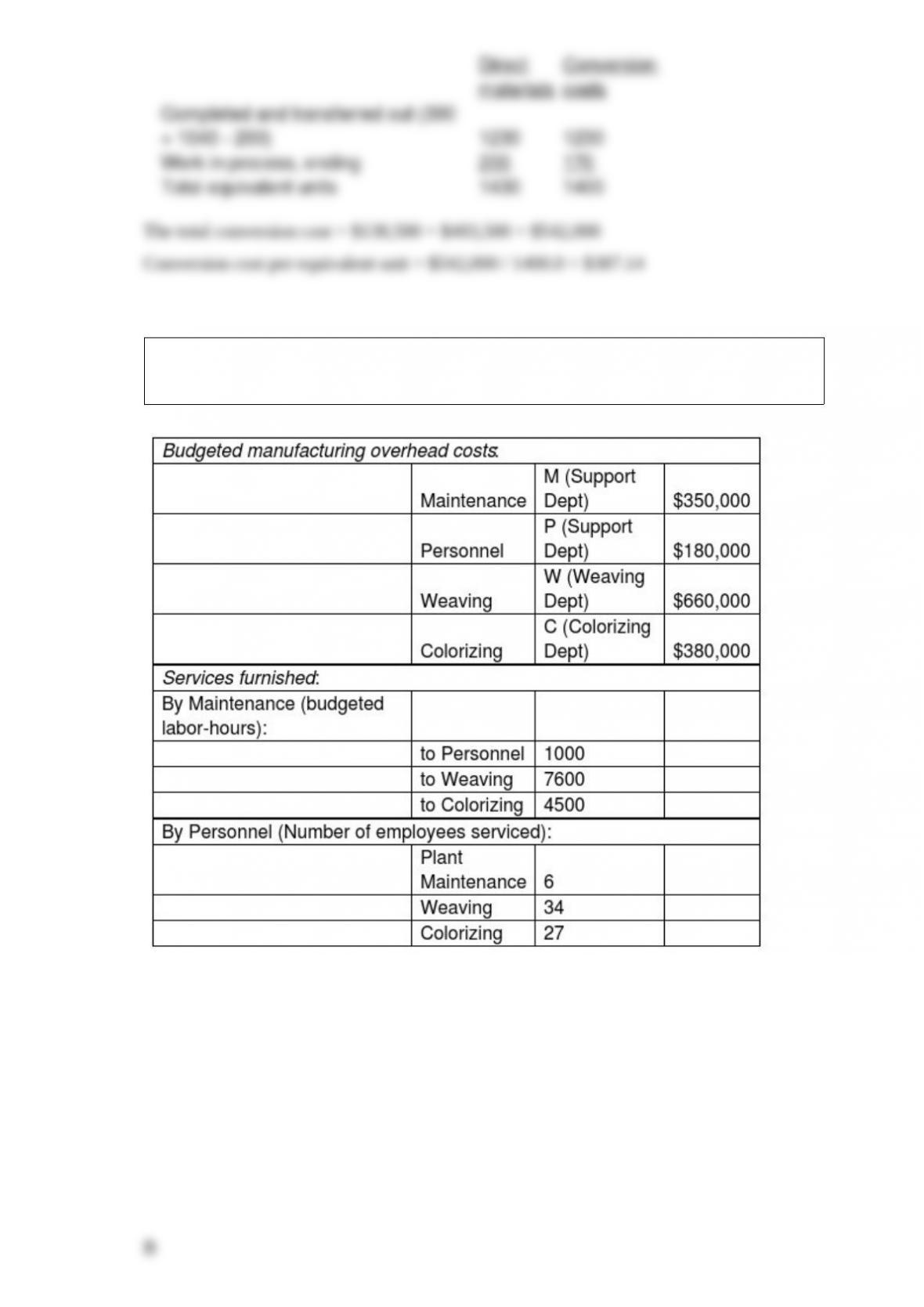

Hugo, owner of Automated Fabric, Inc., is interested in using the reciprocal allocation

method. The following data from operations were collected for analysis:

What is the complete reciprocated cost of the Personnel Department? (Do not round any

intermediary calculations.)

A) $170,000

B) $208,140

C) $180,000

D) $213,012

The slope of the line of regression is the ________.

A) rate at which the dependent variable varies

B) rate at which the independent variable varies

C) difference between the fixed cost and variable cost associated with the cost driver

D) difference between actual cost and estimated cost for each observation of the cost

driver

Without nonfinancial quality measures, ________.

A) the operating income cannot be improved

B) the short-run effectiveness of financial quality measures is questionable

C) the precise problem areas that need improvement cannot be identified

D) quality problems might not be identified until it is too late

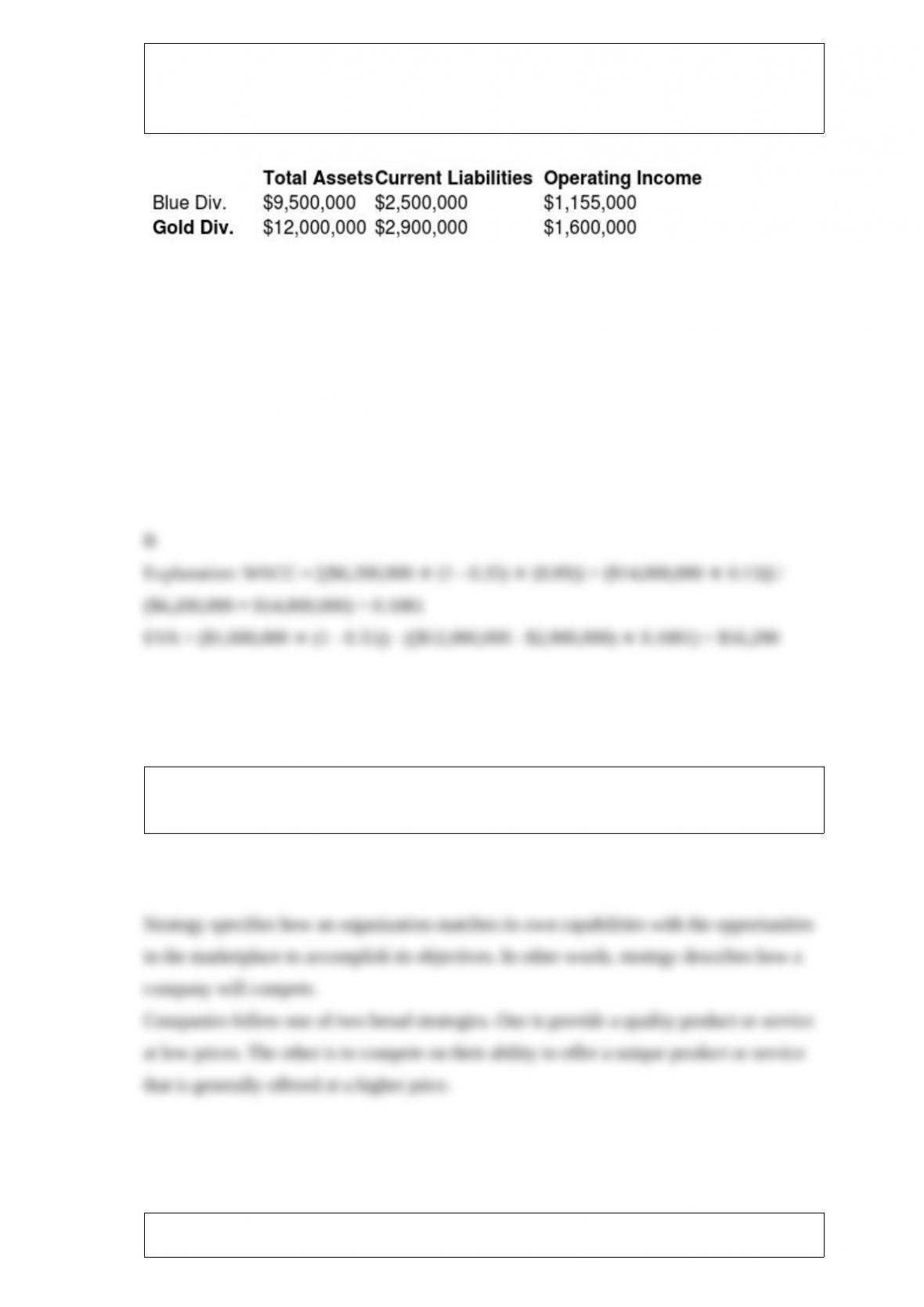

Stonex Corp, whose tax rate is 35%, has two sources of funds: long-term debt with a

market value of $6,200,000 and an interest rate of 9%, and equity capital with a market

value of $14,000,000 and a cost of equity of 13%. Stonex has two operating divisions,

the Blue division and the Gold division, with the following financial measures for the

current year:

Calculate EVA for the Gold Division. (Round intermediary calculations to four decimal

places.)

A) -$56,290

B) $56,290

C) $1,040,000

D) $983,710

What is strategy? Briefly describe the two broad types of strategies that companies may

choose to pursue.

Briefly explain the planning and control activities in management accounting. How are

these two activities linked to each other?

An analysis of Revere Beach Corporation’s operating income changes between 2017

and 2018 show the following:

Operating income for 2017 $4,750,000

Add growth component 180,000

Deduct price-recovery component (60,000)

Add productivity component 285,000

Operating income for 2018 $5,155,000

Required:

Is Revere’s operating income gain consistent with the product differentiation or cost

leadership strategy? Explain briefly.

Companies are increasingly using nonfinancial measures to evaluate performance.

Why? Since these numbers do not come from the company’s financial records, why are

they used?

Explain the difference between a static budget and a flexible budget. Explain what is

meant by a static budget variance and a flexible budget variance.

Should a company with high fixed costs and unused capacity raise selling prices to try

to fully recoup its costs?

An accounting firm completes an audit for a local union and has the following cost

information for the year.

Indirect labor $60,000

Office lease $22,000

Depreciation on office equipment $8,000

Marketing expense $20,000

Utilities $15,000

The firm’s direct labor costs are budgeted at $500,000 for the year and overhead is

allocated based on direct labor costs. The firm used 1 partner and 2 audit associates on

the audit. Partners are paid $150 per hour while audit associates earn $50 per hour. The

partner spent 6 hours on the engagement while the audit associates spent a total of 40

hours.

Required:

What is the cost of the audit?

What advice would you give a company to avoid the appearance of predatory pricing?

The Pitt Corporation has been outsourcing data processing in the belief that such

outsourcing would reduce costs and increase corporate profitability. In spite of this,

there has been no meaningful increase in corporate profitability.

Previously, Pitt used a single-rate method to allocate data processing costs. A per unit

cost for data processing was computed and compared to the price of the outside

supplier. The price of the outside supplier was lower and thus, the outside bid was

accepted.

Required:

Formulate a possible reason why Pitt’s profitability has not shown improvement in

terms of the cost allocation method used.

The Controller of Nip-it-in-the-Bud Inc. has studied the possibility of implementing a

JIT production system. The annual incremental retooling costs of the JIT system is

projected to be about $67,000 however, the new system will lower insurance costs by

$10,000 and storage costs will drop by $20,000 a year as the company will be able to

reuse warehouse space for other strategic purposes. In addition, material handling costs

will drop by $10,000 a year and because of a resulting increase in quality and faster

delivery, the company’s contribution margin on the product will increase by $2.00 on

annual sales of 20,000 units.

Required:

Calculate the net incremental benefit of the JIT system implementation.

Cost behavior is approximated by a linear cost function within the relevant range.

List the four standards of ethical conduct for management accountants. For each

standard, give an example that demonstrates compliance with that standard.

There is an overlap or intersection between management accounting and financial

accounting. Explain.

A company has a plant in a high tax jurisdiction that produces products for a facility in

a low tax jurisdiction. Suggest a strategy, including transfer prices, which will result in

the lowest tax for the overall corporation.

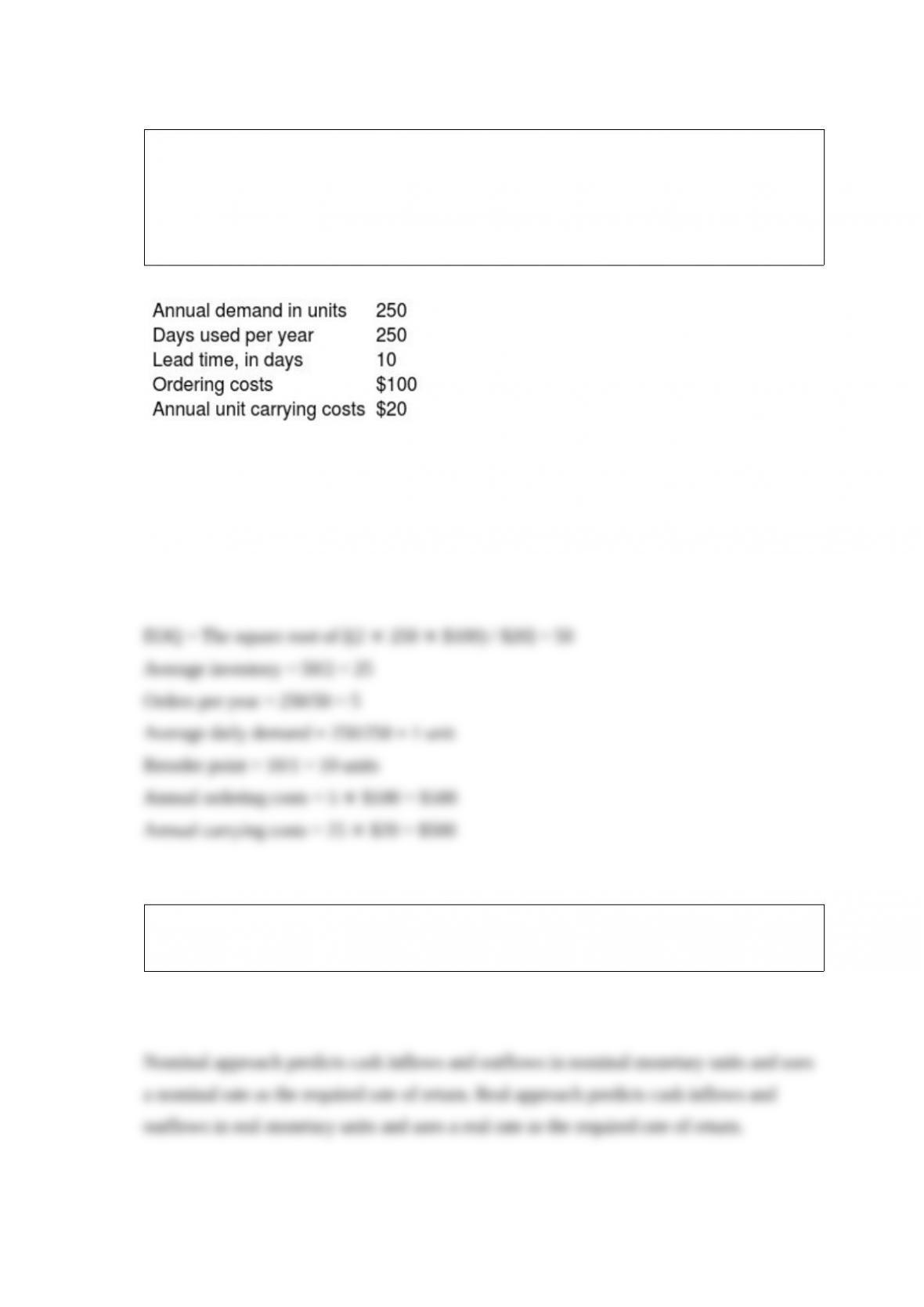

For supply item ABC, Andrews Company has been ordering 125 units based on the

recommendation of the salesperson who calls on the company monthly. A new

purchasing agent has been hired by the company who wants to start using the

economic-order-quantity method and its supporting decision elements. She has gathered

the following information:

Required:

Determine the EOQ, average inventory, orders per year, average daily demand, reorder

point, annual ordering costs, and annual carrying costs.

What is the difference between nominal approach and real approach to incorporating

inflation into the net present value method?

Do activity-based costing systems always provide more accurate product costs than

conventional cost systems? Why or why not?

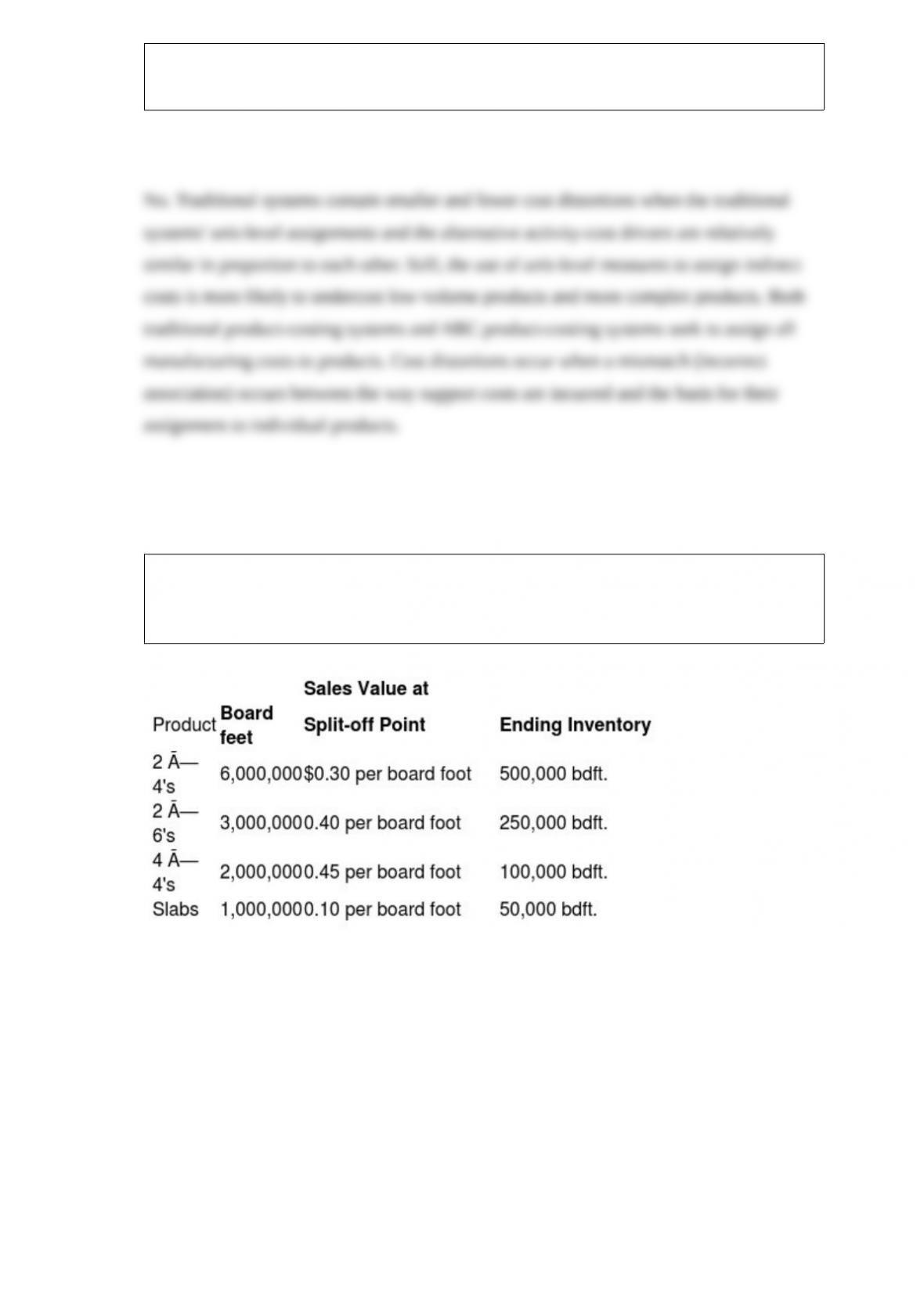

Oregon Lumber processes timber into four products. During January, the joint costs of

processing were $280,000. There was no inventory at the beginning of the month.

Production and sales value information for the month is as follows:

Required:

Determine the value of ending inventory if the sales value at split-off method is used for

product costing. Round to 3 decimal places when necessary.