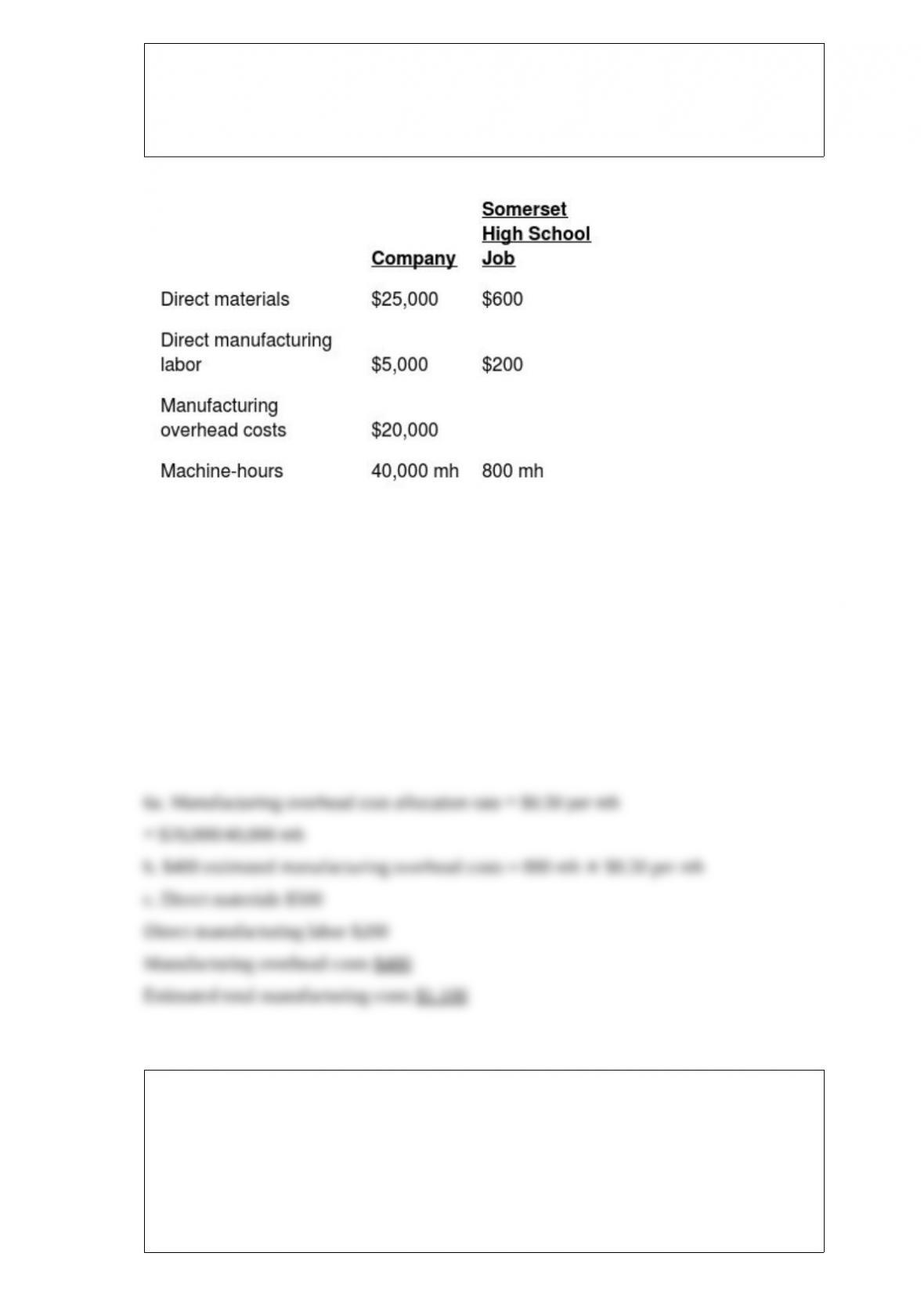

Chief Manufacturing is a small textile manufacturer using machine-hours as the single

indirect-cost rate to allocate manufacturing overhead costs to the various jobs

contracted during the year. The following estimates are provided for the coming year

for the company and for the Somerset High School Science Olympiad Jacket job.

Required:

a. For Chief Manufacturing, determine the annual manufacturing overhead cost-allocation

rate.

b. Determine the amount of manufacturing overhead costs allocated to the Somerset High

School job.

c. Determine the estimated total manufacturing costs for the Somerset High School job.

Which of the following is a sign that an ABC system may be useful for an organization?

A) Significant amounts of indirect costs are allocated using multiple cost pools.

B) Products make similar demands on resources because of similarities in volume,

process steps, batch size, or complexity.

C) Many indirect costs are described as batch-level costs, product-sustaining costs, or

facility-sustaining costs.

D) Operations staff disagrees with accountants about the costs of manufacturing and

marketing products and services.

Sales of Granite City Products Inc. have been on a steady decline for the last 12

months. A market research study conducted revealed that the product of Granite City

Products Inc. can be sold only for $480 as opposed to the current market price charged

of $580 per unit. Granite City Products Inc. has decided to revise its sales price to $480.

The annual sales target volume of the product after price revision is 280 units. Granite

City Products Inc. wants to earn 30% on its sales amount.

What is the target cost per unit?

A) $625.00

B) $336.00

C) $480.00

D) $145.00

What is the cost of goods manufactured for 2018?

A) $404,000

B) $399,000

C) $301,000

D) $311,000

Canton Corp. manufactures two sizes of ceramic paperweights, regular and jumbo. The

following information applies to their expectations for the planning period:

Cost Pool Overhead Costs Activity-cost driver

Materials handling $46,000 94,000 orders

Machine maintenance $310,000 20,000 maintenance hours

Setups $261,000 45,000 setups

Inspections $132,370 21,700 inspections

Total support costs $749,370

Production Estimates

Production units:

Regular = 8,000,000 units

Jumbo = 16,000,000 units

Machine-hours = 500,000 mh

Labor-hours = 1,000,000 dlh

Expected direct costs amounts to $942,000 for the period. Support cost requirements of

both products are substantially different from one another. Canton uses an ABC costing

system.

The setups activity-cost driver rate is ________.

A) $6.10 per setup

B) $5.80 per setup

C) $4.15 per setup

D) $15.50 per setup

When an industry has excess capacity, market prices may drop well below their

historical average. If this drop is temporary, it is called ________.

A) distress prices

B) dropped prices

C) low-average prices

D) substitute prices

Product testing is an example of ________.

A) prevention costs

B) appraisal costs

C) internal failure costs

D) external failure costs

Johnson Superior Products Inc. produces hospital equipment and the setup requirements

vary from product to product. Johnson produces its products based on customer orders

and uses ABC costing. In one of its indirect cost pools, setup costs and distribution

costs are pooled together. Costs in this pool are allocated using number of customer

orders for the easiness of costing operations. Based on the information provided, which

of the following arguments is valid?

A) Johnson has clearly failed to identify as many direct costs as is economically

feasible.

B) All costs in a homogeneous cost pool have the same or a similar cause-and-effect

relationship with the single cost driver that is used as the cost-allocation base for

Johnson.

C) Johnson has unnecessarily wasted resources by classifying setup and distribution

costs as they could have been considered as direct costs.

D) Johnson has failed to use the correct cost driver as the cost-allocation base for setup

costs.

Premier Corp expects to spend $800,500 in 2017 in appraisal costs if it does not change

its incoming materials inspection method. If it decides to implement a new receiving

method, it will save $60,100 in fixed appraisal costs and variable costs of $0.50 per

materials units received. The new method involves $140,600 in training costs and an

additional $150,000 in annual equipment rental.

Internal failure costs average $160 per failed unit of finished goods. During 2016, 4%

of all completed items had to be reworked. External failure costs average $430 per

failed unit. The company’s average external failures are 1% of units sold. The company

carries no ending inventories, because all jobs are on a per order basis and a just-in-time

inventory ordering method is used.

What is the net effect on appraisal costs for 2017, assuming the new receiving method

is implemented and that 800,500 material units are received?

A) $1292 increase

B) $169,750 decrease

C) $290,600 decrease

D) $4003 increase

Value chain and classification of costs, car company.

General Motors incurs the following costs:

a. Electricity costs for the plant assembling the Chevrolet Camaro

b. Transportation costs for shipping the Camaro to dealers

c. Payment to Shelby Designs for the design of the Camaro.

d. Salary of an engineer working on the next generation of Camaros

e. Cost of GM employees’ visit to an auto show to demonstrate the Camaro

f. Testing the Camaro at the GM track

g. Payment to television network for running Camaro advertisements

h. Cost of brake pads purchased from outside supplier to be installed on the Camaro

Required:

Classify each of the cost items (a-h) into one of the business functions of the value

chain.

1) Research and development

2) Design of products and processes

3) Production

4) Marketing and sales

5) Distribution

6) Customer service

The transfer-pricing method that reduces the goal-congruence problems associated with

a pure cost-plus-based transfer-pricing method is the ________.

A) dual pricing

B) market pricing

C) single pricing

D) distress pricing

SaleCo sells 11,000 units resulting in $110,000 of sales revenue, $50,000 of variable

costs, and $45,000 of fixed costs. To achieve $150,000 in operating income, sales must

total ________. (Round intermediate calculations to two decimal places and the final

answer to the nearest dollar.)

A) $245,000

B) $253,846

C) $160,000

D) $357,500

Concose Park Department is considering a new capital investment. The cost of the

machine is $280,000. The annual cost savings if the new machine is acquired will be

$165,000. The machine will have a 3-year life and the terminal disposal value is

expected to be $35,000. There are no tax consequences related to this decision. If

Concose Park Department has a required rate of return of 14%, which of the following

is closest to the present value of the project?

A) $190,880

B) $87,750

C) $126,755

D) $103,130

Bright Colors Company placed 315,000 gallons of direct materials into the mixing

process. All direct materials are placed in mixing at the beginning of the process and

conversion costs occur evenly during the process. Bright Colors uses weighted-average

costing. The initial forecast for the end of the month was to have 75,000 gallons still in

process, 15% converted as to labor and factory overhead.

Required:

a. Determine the total equivalent units (in process and transferred out) for direct

materials and for conversion costs, assuming there was no beginning inventory.

b. With the installation of a new paint processing filtration device, the forecast for the

end of the month was to have 50,000 gallons still in process, 70% converted as to labor

and factory overhead. In this event, determine the equivalent units (in process and

transferred out) for direct materials and for conversion costs, assuming there was no

beginning inventory.

The Swivel Chair Company manufacturers a standard recliner. During February, the

firm’s Assembly Department started production of 145,000 chairs. During the month,

the firm completed 183,000 chairs and transferred them to the Finishing Department.

The firm ended the month with 24,000 chairs in ending inventory. All direct materials

costs are added at the beginning of the production cycle. Weighted-average costing is

used by Swivel. Of the 145,000 units Swivel started during February, how many were

finished during the month?

A) 183,500

B) 218,200

C) 121,000

D) 217,000

An unfavorable production-volume variance ________.

A) is not a good measure of a lost production opportunity

B) indicates that the company had reduced its per unit fixed overhead cost to improve

sales

C) measures the amount of extra fixed costs planned for but not used

D) takes into account the effect of additional revenues due to maintaining higher prices

ABC Manufacturing Inc. ends the month with two jobs still in progress. Job 5 has

$10,000 of materials, $2,000 of direct labor and $8,000 of manufacturing overhead

allocated. Job 6 has $30,000 of materials, $2,000 of direct labor and $12,000 of

manufacturing overhead allocated. The cost of goods sold for the month was $40,000

and there was no finished goods in stock as the month ended. If the manufacturing

overhead was underallocated by $10,000, which of the following choices would be the

correct way to prorate it based on ending balances before proration?

A) The entire $10,000 of underallocated manufacturing overhead should be allocated to

cost of goods sold

B) $4,000 of the underallocated manufacturing overhead should be split between Job 6

and cost of goods sold

C) $2,000 of the overallocation should be allocated to Job 5

D) The entire $10,000 of underallocated manufacturing overhead should be added to

operating expenses for the month

What is the operating income for 2018?

A) $73,000

B) $49,000

C) $36,000

D) $62,000

Quantum Company uses the high-low method to estimate the cost function. The

information for 2017 is provided below:

Machine-hours Labor Costs

Highest observation of cost driver 900 $36,000

Lowest observation of cost driver 100 $14,000

What is the estimated total cost when 450 machine-hours are used?

A) $63,000

B) $32,000

C) $18,000

D) $23,625

In a normal costing system, the Manufacturing Overhead Control account ________.

A) is increased by allocated manufacturing overhead

B) is credited with amounts transferred to Work-in-Process

C) is decreased by allocated manufacturing overhead

D) is debited with actual overhead costs

Three major influences on pricing decisions are ________.

A) competition, costs, and customers

B) competition, demand, and production efficiency

C) continuous improvement, customer satisfaction, and supply

D) variable costs, fixed costs, and mixed costs

Assume only the specified parameters change in a CVP analysis. The contribution

margin percentage increases when ________.

A) total fixed costs increase

B) total fixed costs decrease

C) variable costs per unit increase

D) variable costs per unit decrease

Premier Corp expects to spend $800,900 in 2017 in appraisal costs if it does not change

its incoming materials inspection method. If it decides to implement a new receiving

method, it will save $60,500 in fixed appraisal costs and variable costs of $0.50 per unit

of finished product. The new method involves $140,500 in training costs and an

additional $150,300 in annual equipment rental.

Internal failure costs average $250 per failed unit of finished goods. During 2016, 6%

of all completed items had to be reworked. External failure costs average $450 per

failed unit. The company’s average external failures are 2% of units sold. The company

carries no ending inventories, because all jobs are on a per order basis and a just-in-time

inventory ordering method is used.

What would be the change in the external failure budget, if 600,300 units are used and

assuming external failures are reduced by 12%.

A) $48,054 increase

B) $250,150 decrease

C) $648,324 decrease

D) $304,342 decrease

In general, profit potential of an organization decreases with ________.

A) lesser competition and stronger potential entrants

B) greater competition and stronger potential entrants

C) lesser competition and weaker potential entrants

D) greater competition and weaker potential entrants

Denver City Manufacturing currently produces 2,000 glasses per month. The following

per unit data apply for sales to regular customers and is based on 1,000 units produced.

The plant has capacity for 3,000 glasses. Plant supervisor’s salary is $15,000.

Required:

a. What is the total cost of producing 2,000 glasses?

b. What is the total cost of producing 1,600 glasses?

c. What is the per unit cost when producing 1,500 glasses?

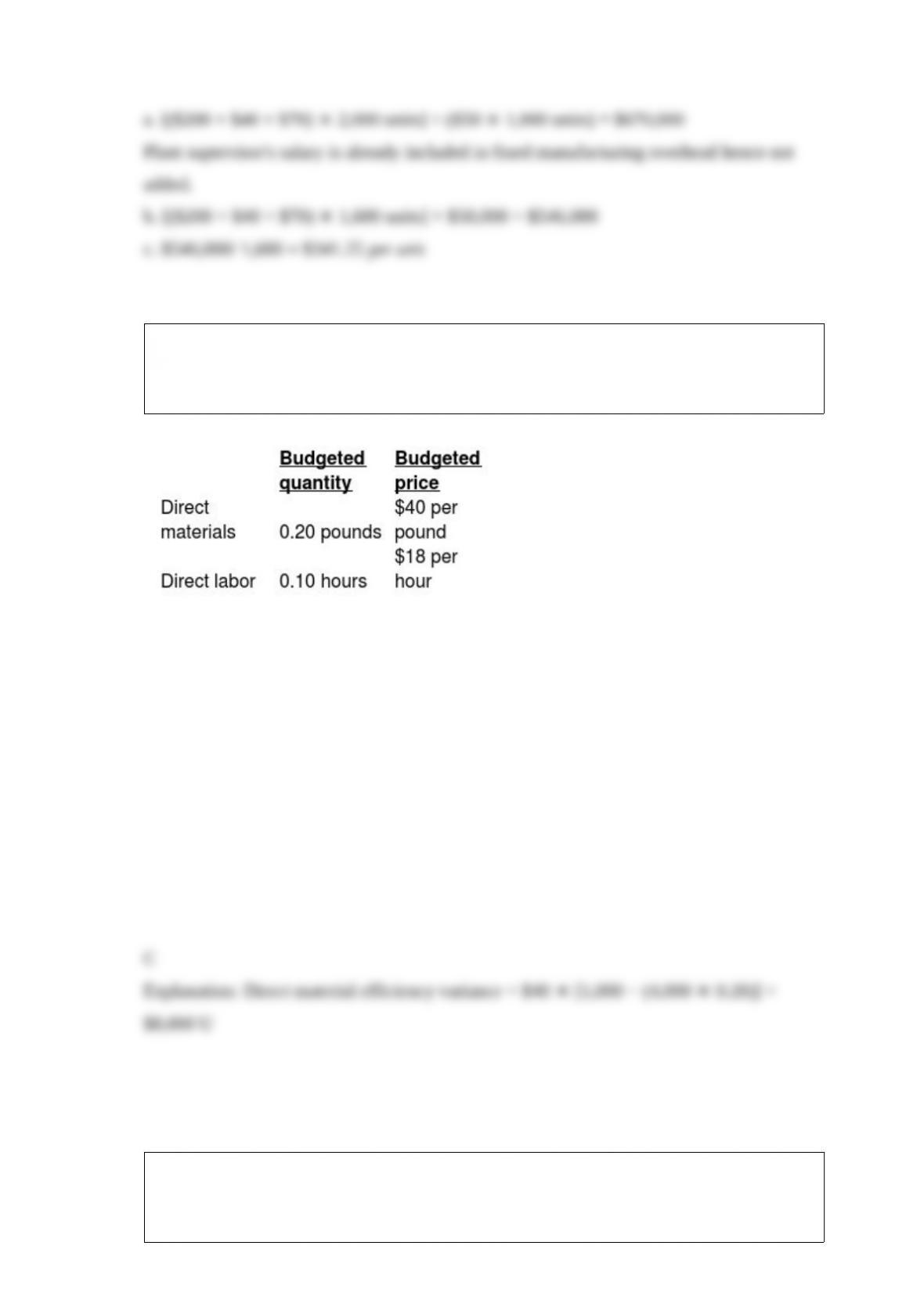

Genent Industries, Inc. (GII), developed standard costs for direct material and direct

labor. In 2017, GII estimated the following standard costs for one of their major

products, the 30-gallon heavy-duty plastic container.

During July, GII produced and sold 4,000 containers using 1,000 pounds of direct

materials at an average cost per pound of $37 and 475 direct manufacturing labor hours at

an average wage of $18.75 per hour.

The direct material efficiency variance during July is ________.

A) $5,000 unfavorable

B) $7,400 favorable

C) $8,000 unfavorable

D) $5,000 favorable

Which of the following statements is true of the methods for allocating joint costs?

A) Constant gross-margin percentage method results in same joint production cost per

unit for all products.

B) Estimated net realizable value method results in same gross margin percentage for

all products.

C) Present value allocation method is the least preferred method due to its complex

calculations.

D) Sales value at split-off method uses the sales value of the entire production of the

accounting period to allocate costs.

Which of the following statements best relates to the balanced scorecard’s financial

perspective?

A) How can we maximize profits for the current year?

B) How can we increase shareholder value?

C) How will we achieve continuous improvements?

D) How can we maximize customer satisfaction?

The costs used in cost-based transfer prices ________.

A) are actual costs

B) are budgeted costs

C) can either be actual or budgeted costs

D) are lower than the market-based transfer prices

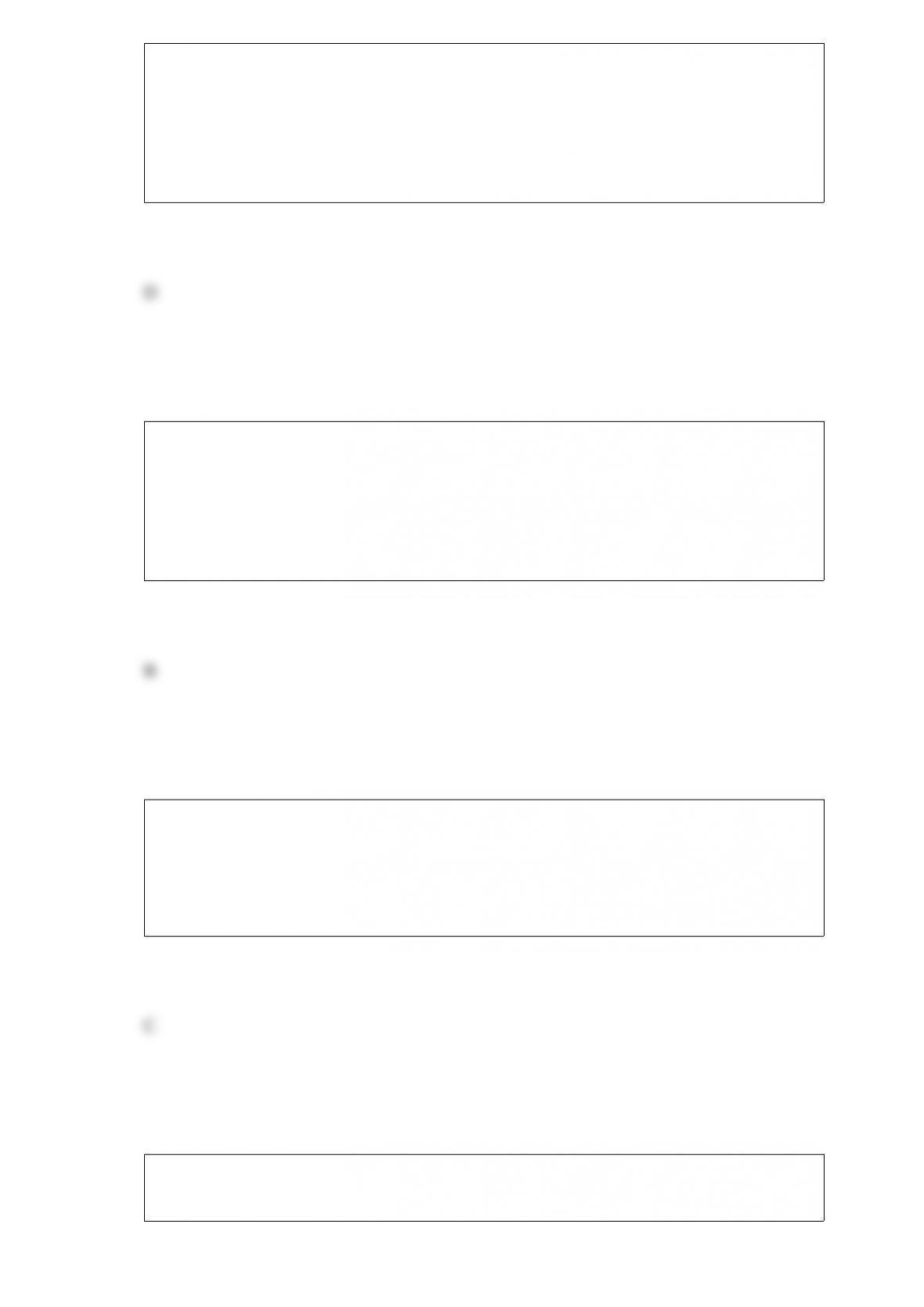

Schooner Corporation used the following data to evaluate its current operating system.

The company sells items for $25 each and used a budgeted selling price of $25 per unit.

What is the static-budget variance of variable costs?

A) $36,000 favorable

B) $36,000 unfavorable

C) $204,000 favorable

D) $204,000 unfavorable

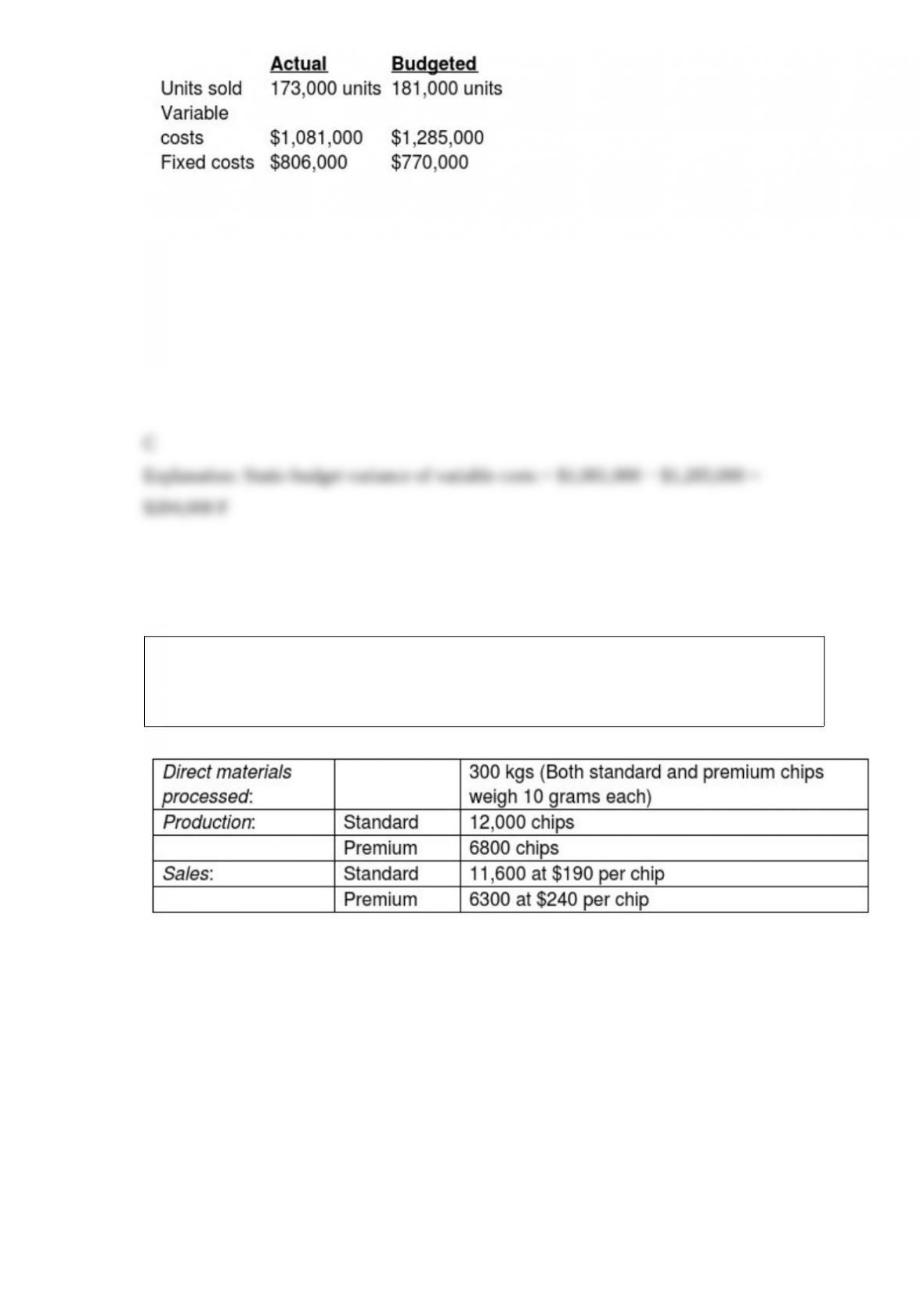

Netzone Company is in semiconductor industry and fabrication of silicon-wafer chips

splits off two types of memory chips, Standard and Premium. The following

information was collected for last quarter of the calendar year:

The cost of purchasing 300 kgs of direct materials and processing it up to the split-off

point to yield a total of 18,800 chips of good products was $2,030,000. Beginning

inventories totalled 150 chips for Standard and 80 chips for Premium. Ending inventory

amounts reflected 150 chips of Standard and 80 chips of Premium. October costs per unit

were the same as November. When using a physical-volume measure, what is the

approximate amount of joint costs that will be allocated Premium chips? (Round

intermediary percentages to the nearest hundredth.)

A) $734,251

B) $714,469

C) $1,015,000

D) $669,106

Sensitivity analysis is ________.

A) a way of determining what will happen if assumptions change

B) a way of seeing how employees will be affected by changes

C) a way of determining how customers will react to new products

D) a way of seeing how far from budget actual results are

Which of the following is the expression of the DuPont method of profitability

analysis?

A) Income / Investment = Income / Total costs + Revenues / Equity

B) Income / Investment = Income / Revenues + Revenues / Investment

C) Income / Investment = Income / Revenues × Revenues / Investment

D) Income / Investment = Income / Total costs × Revenues / Equity

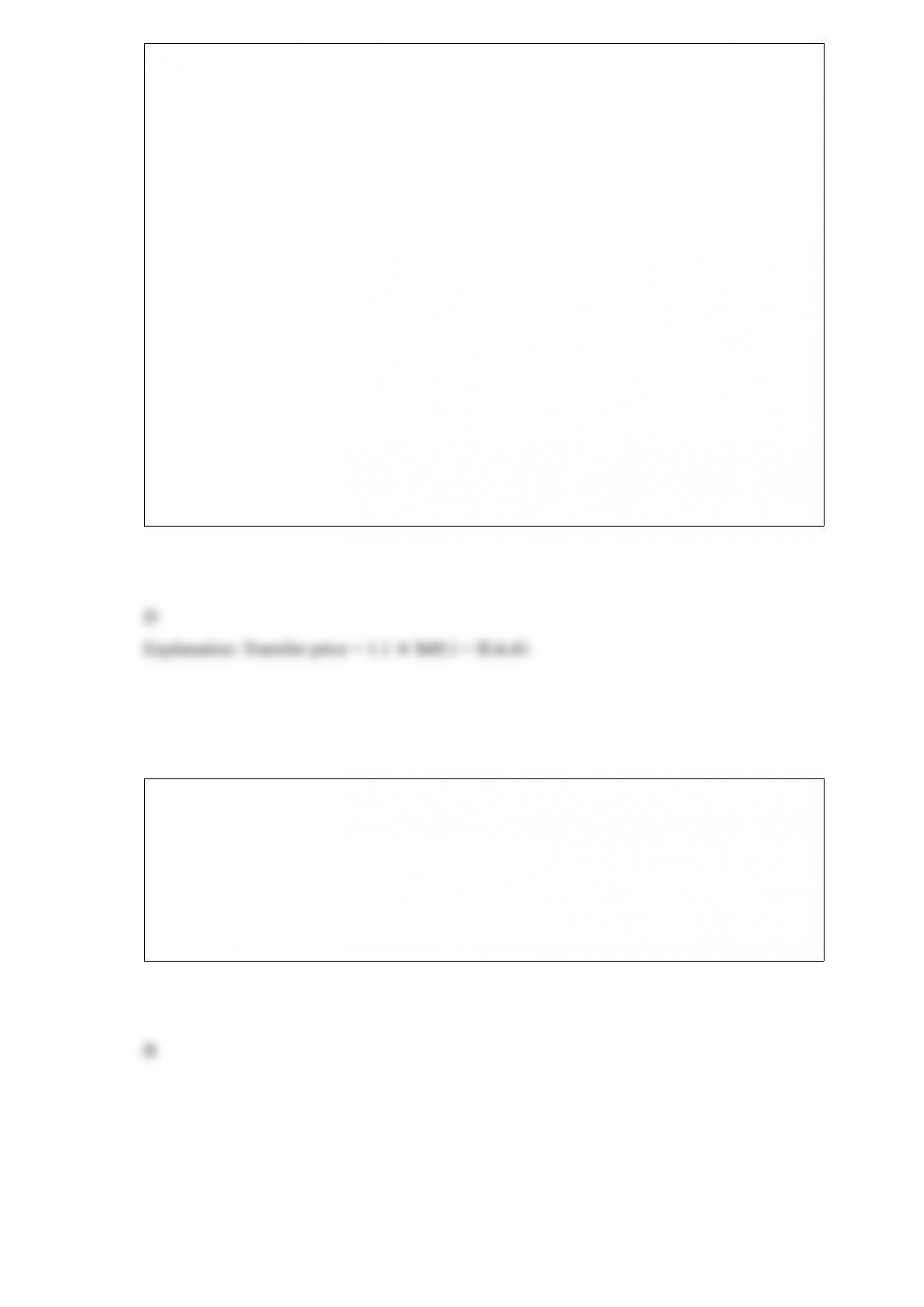

Plish Company manufactures only one type of washing machine and has two divisions,

the Compressor Division, and the Fabrication Division. The Compressor Division

manufactures compressors for the Fabrication Division, which completes the washing

machine and sells it to retailers. The Compressor Division “sells” compressors to the

Fabrication Division. The market price for the Fabrication Division to purchase a

compressor is $60.00. (Ignore changes in inventory.) The fixed costs for the

Compressor Division are assumed to be the same over the range of 8000-13,000 units.

The fixed costs for the Fabrication Division are assumed to be $11.50 per unit at 13,000

units.

Compressor’s costs per compressor are:

Direct materials $18

Direct labor $17.00

Variable overhead $6.50

Division fixed costs $8.00

Fabrication‘s costs per completed air conditioner are:

Direct materials $162.00

Direct labor $66.00

Variable overhead $23.00

Division fixed costs $8.00

What is the transfer price per compressor from the Compressor Division to the

Fabrication Division if the transfer price per compressor is 110% of full costs?

A) $19.80

B) $32.45

C) $47.30

D) $54.45

Regression analysis ________.

A) calculates the slope coefficient using only two observed values within the relevant

range and their respective costs

B) measures the average amount of change in the dependent variable associated with a

unit change in one or more independent variables

C) estimates the cost functions using the time-and-motion studies

D) measures the variability or dispersion in a set of data points