The accrual accounting rate-of-return method has a significant weakness for use in

making capital budgeting decisions because it does NOT track cash flows and it ignores

the time value of money.

Under the proration approach, the sum of the amounts shown in the subsidiary ledgers

will not match the amounts shown in the general ledger because no adjustments from

budgeted to actual manufacturing overhead rates are made in the individual job-cost

records.

Outside of the relevant range, variable and fixed cost-behavior patterns change, causing

costs to become nonlinear.

Allocated fixed overhead can be expressed in terms of allocation-base units or in terms

of the budgeted fixed cost per unit.

Causes of a favorable variable overhead efficiency variance might include using

lower-skilled workers than expected.

The direct method is conceptually the most precise method because it considers the

mutual services provided among all support departments.

Managing environmental costs is an example of life-cycle costing and value

engineering.

Customer relationship management initiatives use technology to coordinate all

customer-facing activities (such as marketing, sales calls, distribution, and after-sales

support) and the design and production activities necessary to get products to

customers.

Classification of main products, joint products, and byproducts can always be done with

ease.

The possibility of exchange rate fluctuations does NOT influence the budgeting

procedures in a multinational corporation.

A performance report compares actual performance to the amount budgeted.

Nonfinancial measures are ineffective at helping managers evaluate how well they have

done on goals such as improving manufacturing cycle times and customer response

times.

Expected performance is also called budgeted performance.

Acquisition costs of direct materials include freight-in charges, sales taxes, and custom

duties.

Gathering information before making a decision is not efficient within the

decision-making process.

A favorable variance should be ignored by management.

An alternative way to implement the reciprocal method is to formula and use linear

equations.

Some companies, make environmental performance a line item on every employee’s

salary appraisal report.

The risk of peanut-butter costing rises when broad averages are used across multiple

products without managers considering the true amounts of resources consumed in the

making of each product.

The three methods used to study CVP analysis are graph method, contribution method,

and equation method.

Direct manufacturing cost labor includes plant rent and salaries paid to plant

supervisors.

In multiproduct situations, when sales mix shifts toward the product with the lowest

contribution margin, the operating income will be lower.

The cost leadership strategy is for products and services that are similar to a

competitors products and services.

An unfavorable production-volume variance indicates an overallocation of fixed

overhead costs.

Possible reasons for the larger actual materials-handling labor-hours per batch include

the possibility of inefficient layout of production facilities.

Companies which strive to achieve cost leadership should never try to implement

business process re-engineering measures.

Quality is defined as the total features and characteristics of a product or a service made

or performed according to specifications to satisfy customers at the time of purchase

and during use.

The advantages of the high-low method to estimate a cost function is that it is easy and

accurate.

One way to increase capacity is to reduce the time it takes for setups and processing.

Effort refers to physical exertion, such as a worker producing at a faster rate, but

excludes non-physical aspects like acumen and diligence of a worker.

The cost leadership strategy is best for a company if the engineering staff is more

skilled at creatively designing new products than at making process improvements.

When allocating the total indirect cost pool to cost pools such as setup costs including

depreciation and maintenance costs of setup equipment, wages of setup employees, and

allocation of supervisors is called a second-stage allocation.

The net present value method can be used in situations where the required rate of return

varies over the life of the project.

Conformance quality is the performance of a product or service relative to its design

and product specifications.

Cost accounting and cost management include calculating various costs, obtaining

financial and nonfinancial information, and analyzing relevant information for decision

making.

A company is said to be involved in predatory pricing even when it is compelled to sell

its products are a price below the average variable cost because of pricing of the

competitor.

The difference in rices between countries can vary beyond the cost of delivering the

product to each country, solely because of changes in exchange rates.

A budget helps to control activities by adhering to the prescribed plan.

The flexible-budget variance is the difference between an actual result and the

flexible-budget amount based on the level of output actually achieved in the budget

period.

Financial accounting is broader in scope than management accounting in that financial

accounting can include external reporting and reporting that helps managers plan and

control operations.

A segment has the following data:

Sales $650,000

Variable costs 386,000

Fixed costs 365,500

What will be the incremental effect on net income if this segment is eliminated,

assuming the fixed costs will be allocated to profitable segments?

A) $284,500 increase

B) $386,000 decrease

C) $264,000 decrease

D) $365,500 decrease

Dartmouth Building Products Inc. provides the following information.

Corporate advertising costs = $850,000

Division A – $5,000,000

Division B – $20,000,000

Number of ads run relevant on Division A products 500

Number of ads run relevant to Division B products 3667

Assume that customers with higher revenues benefited more from corporate advertising

costs than customers with lower revenues. What is the allocated corporate costs for

Division A?

A) $748,000

B) $212,500

C) $170,000

D) $850,000

Product-cost cross-subsidization means that:

A) when one product is overcosted, it results in more than one other product being

overcosted

B) when a company undercosts more than one of its products, it will overcost more than

one of its other products

C) when a company undercosts one of its products, it will overcost at least one of its

other products

D) when one product is overcosted it results in all other products being overcosted

Sherry and John Enterprises are using the kaizen approach to budgeting for 2018. The

budgeted income statement for January 2018 is as follows:

Under the kaizen approach, cost of goods sold and variable operating expenses are

budgeted to decline by 3% per month.

What is budgeted gross margin for March 2018?

A) $413,996

B) $426,800

C) $466,796

D) $476,642

Which of the following is the correct formula for the materials price variance?

A) (Actual price of input – Budgeted price of input) x Budgeted quantity of input

B) (Actual quantity of input used – Budgeted quantity of input allowed for actual

output) x Budgeted price of input

C) (Actual price of input – Budgeted price of input) x Actual quantity of input

D) (Actual quantity of input used – Budgeted quantity of input allowed for actual

output) x Actual price of input

Strategy specifies ________.

A) how an organization matches its own capabilities with the opportunities in the

marketplace

B) standard procedures to ensure quality products

C) incremental changes for improved performance

D) the demand created for products and services

Rules for measurement and reporting for management accounting ________.

A) state that information must only be useful to management.

B) do not need to follow GAAP but must meet the cost-benefit test.

C) must follow GAAP.

D) must follow GAAP, IRS rules or government standards.

One of the first steps to take when using CVP analysis to help make decisions is

________.

A) calculating the break-even point

B) identifying the variable and fixed costs

C) calculation of the degree of operating leverage for the company

D) estimating the volume of sales to make a good profit

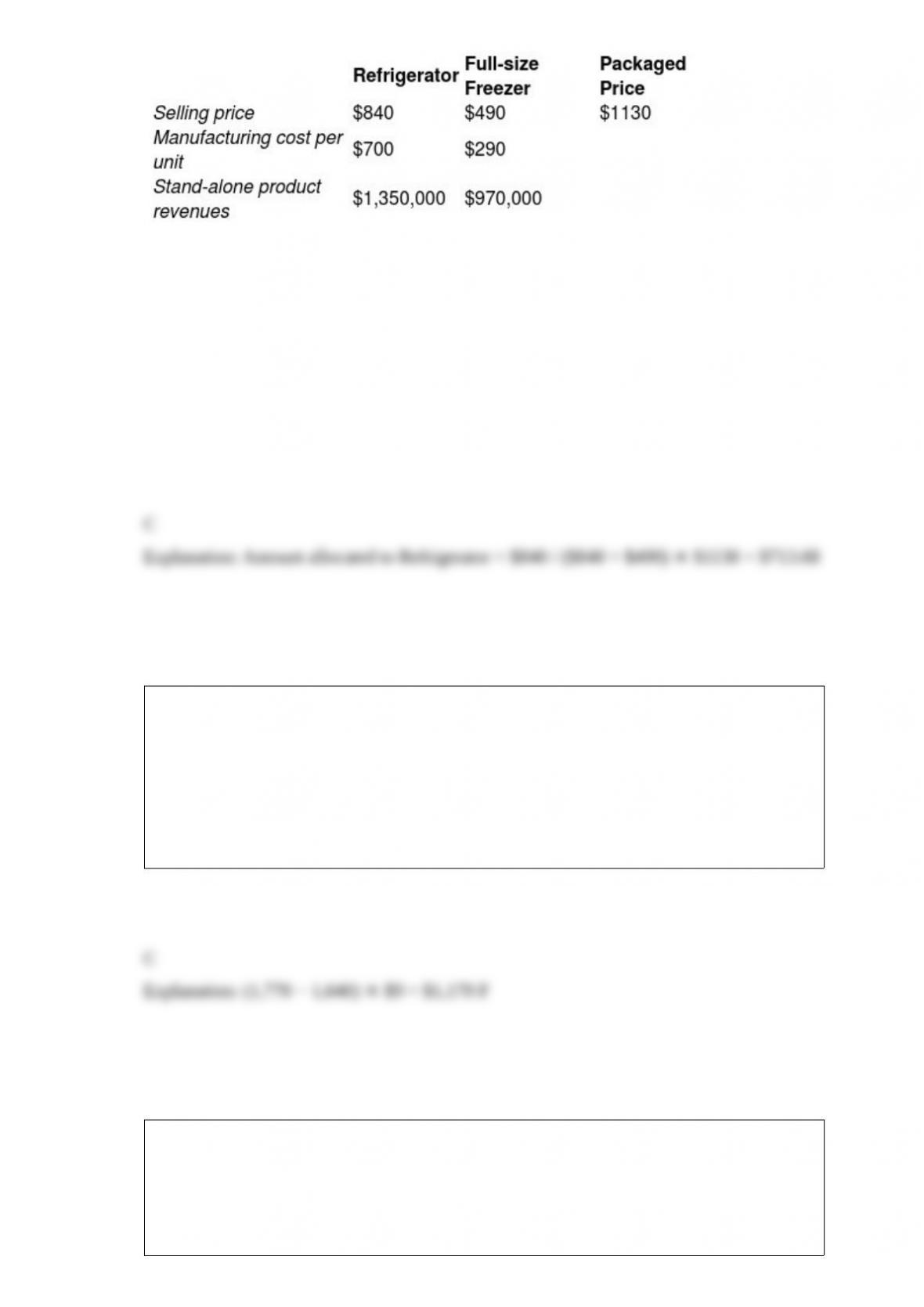

Electro Corp sells a refrigerator and a freezer as a single package for $1130. Other data

are in the chart below.

Using the stand-alone method with selling price as the weight for revenue allocation, what

amount will be allocated to the refrigerator? (Do not round any intermediary calculations.)

A) $565.00

B) $416.32

C) $713.68

D) $840.00

Jalbert Incorporated planned to use materials of $9 per unit but actually used materials

of $14 per unit, and planned to make 1,640 units but actually made 1,770 units.

The sales-volume variance for materials is ________.

A) $1,170 unfavorable

B) $1,820 unfavorable

C) $1,170 favorable

D) $1,820 favorable

The cash budget is a schedule of expected cash receipts and disbursements that

________.

A) requires an aging of accounts receivable and accounts payable

B) is a self-liquidating cycle

C) is prepared immediately after the sales forecast

D) predicts the effect on the cash position at given levels of operations

When using the high-low method, the two observations used are the high and low

observations of the ________.

A) cost driver

B) fixed cost component

C) slope coefficient

D) direct cost

The term for understanding why actual performance deviates from planned

performance is.

A) variance calculation

B) organizational learning

C) favorable variance

D) continuous improvement

Under economic-order-quantity decision model, which of the following is an

assumption? assumed that ________.

A) the quantity ordered can vary at each reorder point

B) demand, ordering costs, and carrying costs are uncertain

C) the purchasing cost per unit is affected by the order quantity

D) the same quantity is ordered at each reorder point

The real approach to incorporating inflation into the net present value method predicts

________.

A) cash inflows and outflows in real monetary units and uses a real rate as the required

rate of return

B) cash inflows and outflows in real monetary units and uses a nominal rate as the

required rate of return

C) cash inflows and outflows in nominal monetary units and uses a real rate as the

required rate of return

D) cash inflows and outflows in monetary units that are adjusted for inflation and uses a

real rate as the required rate of return

Which of the following statements is true of the production method of accounting for

byproducts?

A) It makes no journal entries until the byproduct is sold.

B) It is the preferred method because of the matching principle.

C) It records revenues of the byproduct in the income statement as revenue.

D) It adds revenues of the byproduct to the cost of goods sold in the income statement.

Cysco Corp has a budget of $1,210,000 in 2017 for prevention costs. If it decides to

automate a portion of its prevention activities, it will save $108,000 in variable costs.

The new method will require $50,400 in training costs and $145,000 in annual

equipment costs. Management is willing to adjust the budget for an amount up to the

cost of the new equipment. The budgeted production level is 206,000 units.

Appraisal costs for the year are budgeted at $510,000. The new prevention procedures

will save appraisal costs of $50,600. Internal failure costs average $32 per failed unit of

finished goods. The internal failure rate is expected to be 4% of all completed items.

The proposed changes will cut the internal failure rate by one-half. Internal failure units

are destroyed. External failure costs average $50 per failed unit. The company’s average

external failures average 2.7% of units sold. The new proposal will reduce this rate to

1%. Assume all units produced are sold and there are no ending inventories.

How much will internal failure costs change if the internal product failures are reduced

by 40% with the new procedures?

A) $151,360 decrease

B) $134,400 decrease

C) $105,472 decrease

D) $87,000 increase

An advantage of a negotiated transfer price of a product to be transferred between

divisions is the ________.

A) close relationship between the negotiated price and the market price

B) negotiated transfer price preserves divisional autonomy

C) negotiations usually do not require much time and energy

D) simplicity of its computations and close approximation to market price

Zephram Corporation has a plant capacity of 200,000 units per month. Unit costs at

capacity are:

Direct materials $6.00

Direct labor 5.00

Variable overhead 4.00

Fixed overhead 2.00

Marketing—fixed 6.00

Marketing/distribution—variable 4.60

Current monthly sales are 190,000 units at $30.00 each. Q, Inc., has contacted Zephram

Corporation about purchasing 2,500 units at $24.00 each. Current sales would not be

affected by the one-time-only special order. What is Zephram’s change in operating

profits if the one-time-only special order is accepted?

A) $11,000 increase

B) $31,500 increase

C) $22,500 increase

D) $49,000 increase

Which of the following is true of depreciation cost?

A) Depreciation cost on equipment is irrelevant in decision making because

depreciation on equipment that has already been purchased is a past cost.

B) Depreciation cost on equipment is relevant in decision making because depreciation

on equipment that has already been purchased is an opportunity cost.

C) Depreciation cost on equipment is irrelevant in decision making because there is no

cash transaction.

D) Depreciation cost on equipment is irrelevant in decision making because

depreciation on equipment that has already been purchased is an opportunity cost.

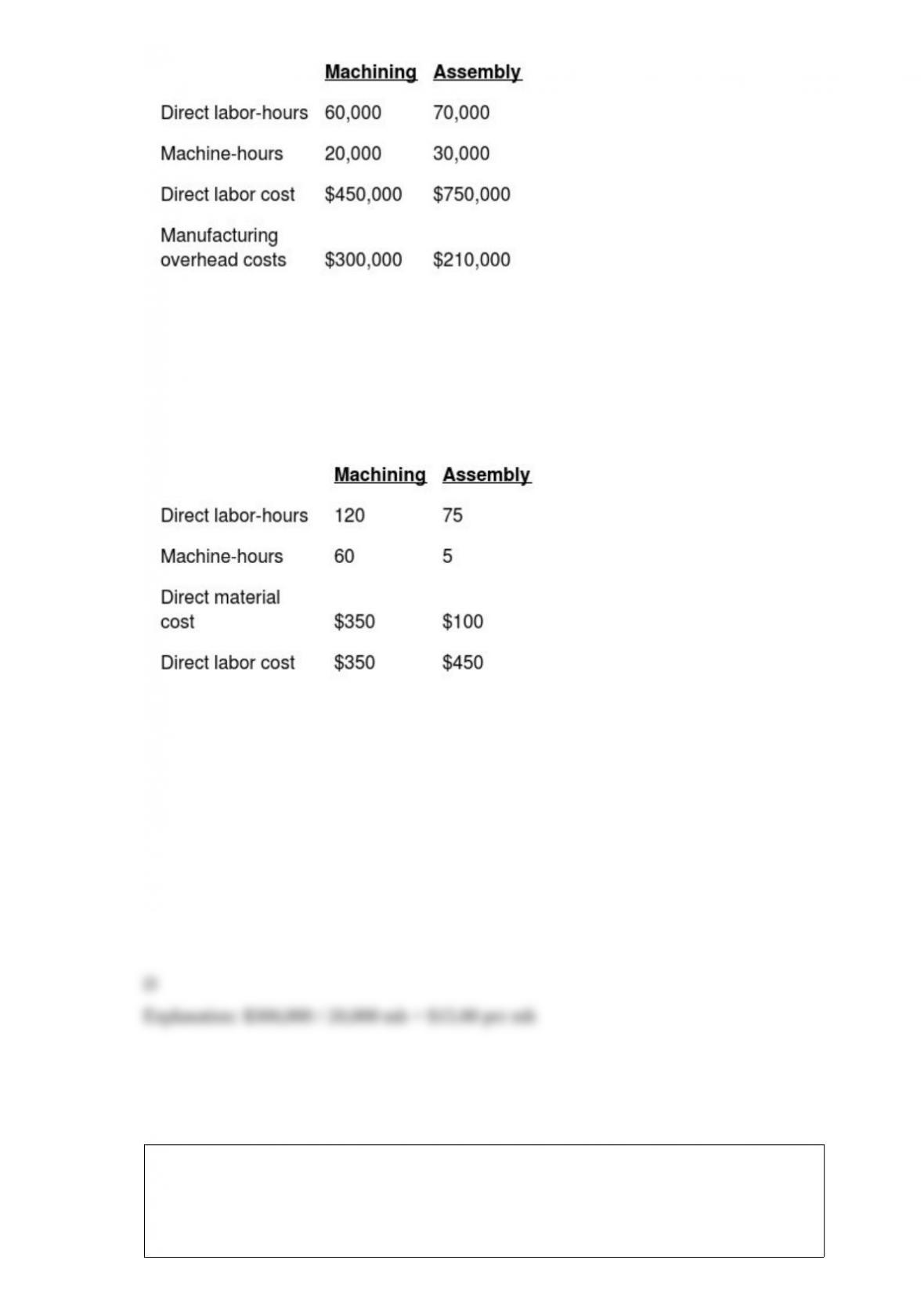

Bauer Manufacturing uses departmental cost driver rates to allocate manufacturing

overhead costs to products. Manufacturing overhead costs are allocated on the basis of

machine-hours in the Machining Department and on the basis of direct labor-hours in

the Assembly Department. At the beginning of 2018, the following estimates were

provided for the coming year:

The accounting records of the company show the following data for Job #316:

For Bauer Manufacturing, what is the annual manufacturing overhead cost-allocation rate

for the Machining Department?

A) $3.00

B) $6.00

C) $5.00

D) $15.00

The accounting firm firm of Smith & Jones LLC has a staff of 34 staff accountants and

auditors and administrative staff. Budgeted total costs of the firm total $5,000,000 of

which $2,900,000 is direct-labor costs. Assuming that the remaining costs are indirect

and direct-labor cost is the allocation base, calculate the budgeted indirect cost rate.

A) 42% of direct-labor cost

B) 72% of direct-labor cost

C) 58% of direct-labor cost

D) 172% of direct-labor cost

To complete the first setup on a new machine took an employee 320 minutes. Using an

70% cumulative average-time learning curve indicates that the second setup on the new

machine is expected to take ________.

A) 112 minutes

B) 128 minutes

C) 272 minutes

D) 224 minutes

Excellent Mugs Inc. produced 1,600,000 units in 2017 at a units of output per dollar of

input cost was $0.09. Its cost of input at 2017 prices that would have been used in 2016

was $20,000,000. How much did the total factor productivity (TFP) increase as a result

of 2017 operations?

A) about 0.1%

B) about 12.5%

C) about 0.08%

D) about 0.17%

When deciding to lease a new cutting machine or continue using the old machine, the

irrelevant cost is ________.

A) $50,000, cost of the old machine

B) $20,000, cost of the new machine

C) $10,000, selling price of the old machine

D) $3,000, annual savings in operating costs if the new machine is purchased

The Cybertronics Corporation reported the following information for its Cyclotron

Division:

Revenues $2,500,000

Operating costs 1,600,000

Operating assets 1,300,000

Income is defined as operating income.

What is the Cyclotron Division’s investment turnover ratio?

A) 1.92

B) 1.56

C) 0.81

D) 1.23

The amount of a markup percentage that customers are willing to pay is usually higher

when which of the following conditions exist?

A) there is idle capacity

B) demand is strong

C) competition is intense

D) demand is elastic

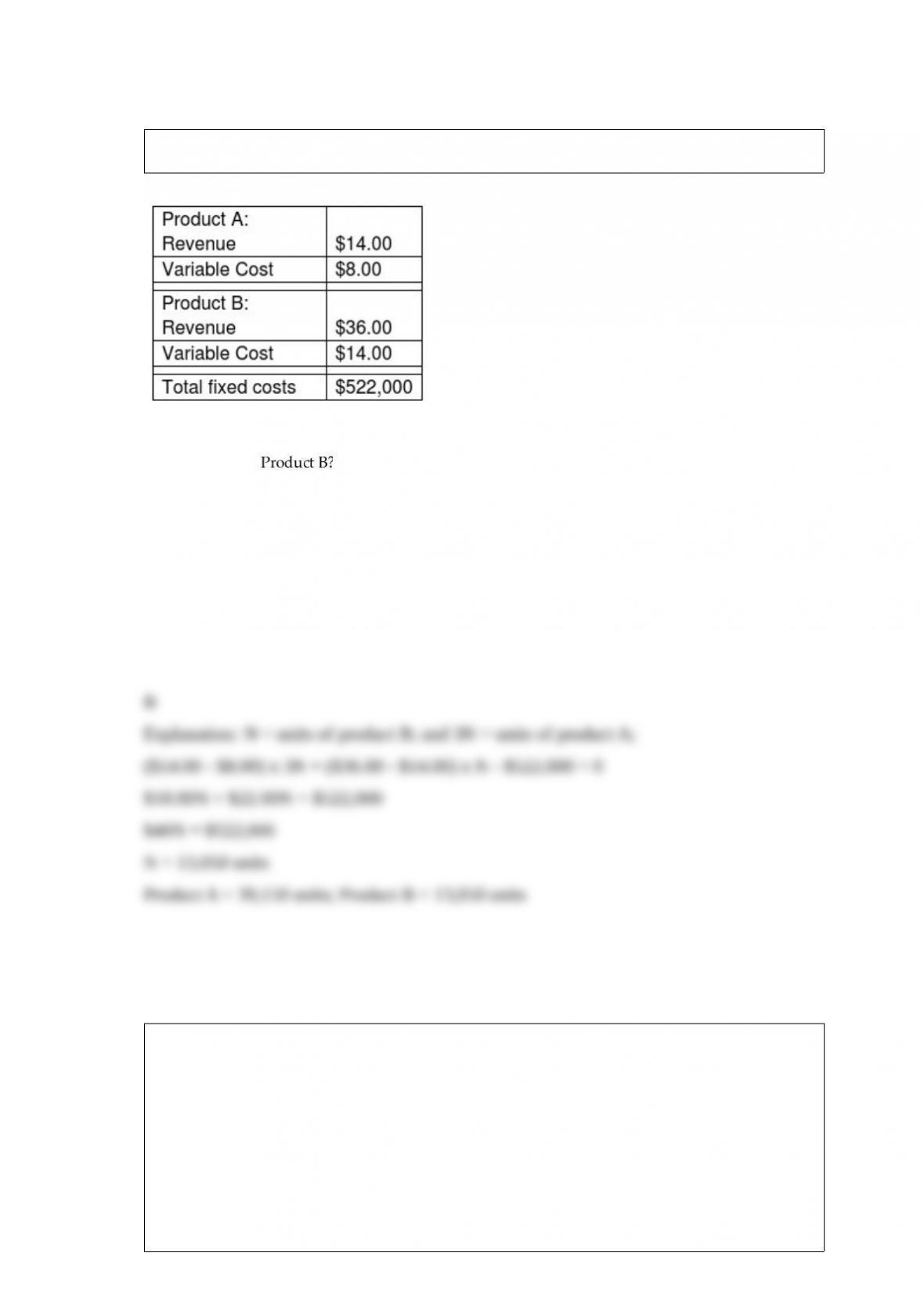

The following information is for the Jeffries Corporation:

What is the breakeven point, assuming the sales mix consists of three units of Product A

and one unit of

A) 14,500 units of A and 4,833 units of B

B) 39,150 units of A and 13,050 units of B

C) 87,000 units of A and 0 units of B

D) 13,050 units of A and 39,150 units of B

Ruben is a travel agent. He intends to sell his customers a special round-trip airline

ticket package. He is able to purchase the package from the airline for $160 each. The

round-trip tickets will be sold for $200 each and the airline intends to reimburse Ruben

for any unsold ticket packages. Fixed costs include $5,200 in advertising costs. How

many ticket packages will Ruben need to sell to break even?

A) 26 packages

B) 40 packages

C) 130 packages

D) 160 packages

Which cost estimation method uses time-and-motion studies to reveal that to make a

high quality men’s suit jacket , it takes of 3 hours of direct labor effort per jacket and 5

minutes of a salaried manager to perform quality control?

A) the accrual accounting method

B) the high-low method

C) the industrial engineering method

D) the cash accounting method

Switching production to products that absorb the highest amount of fixed

manufacturing costs is also called ________.

A) cost reduction

B) cherry picking

C) producing for sales

D) throughput costing