SOLUTION

(20 min.) Gross margin and contribution margin.

1. Ticket sales ($24

´

525 attendees) $12,600

2. Ticket sales ($24

´

1,050 attendees) $25,200

3-53 Ethics, CVP analysis. Megaphone Corporation produces a molded plastic casing,

M&M101, for many cell phones currently on the market. Summary data from its 2017 income

statement are as follows:

Joshua Kirby, Megaphone’s president, is very concerned about Megaphone Corporation’s poor

profitability. He asks Leroy Gibbs, production manager, and Tony DiNunzo, controller, to see if

there are ways to reduce costs.

After 2 weeks, Leroy returns with a proposal to reduce variable costs to 55% of revenues by

reducing the costs Megaphone currently incurs for safe disposal of wasted plastic. Tony is

concerned that this would expose the company to potential environmental liabilities. He tells

Leroy, “We would need to estimate some of these potential environmental costs and include them

in our analysis.” “You can’t do that,” Leroy replies. “We are not violating any laws. There is

some possibility that we may have to incur environmental costs in the future, but if we bring it

up now, this proposal will not go through because our senior management always assumes these

costs to be larger than they turn out to be. The market is very tough, and we are in danger of

shutting down the company and costing all of us our jobs. The only reason our competitors are

making money is because they are doing exactly what I am proposing.”

Required:

1. Calculate Megaphone Corporation’s breakeven revenues for 2017.

2. Calculate Megaphone Corporation’s breakeven revenues if variable costs are 55% of

revenues.

3. Calculate Megaphone Corporation’s operating income for 2017 if variable costs had been 55%

of revenues.

4. Given Leroy Gibbs’s comments, what should Tony DiNunzo do?

SOLUTION

(30 min.) Ethics, CVP analysis.

1. Contribution margin percentage =

Revenues osts

Revenues

Variable c

=

$5, 000, 000 $3, 250, 000

$5,000,000

–

=

$1,750,000

$5,000,000

= 35%

Breakeven revenues =

percentagemargin on Contributi

costs Fixed

=

$1,890,000

0.35

= $5,400,000

2. If variable costs are 55% of revenues, contribution margin percentage equals 45%

(100% 55%)

Breakeven revenues =

percentagemargin on Contributi

costs Fixed

=

$1,890,000

0.45

= $4,200,000

3. Revenues $5,000,000

4. Incorrect reporting of environmental costs with the goal of continuing operations is

Competence

Clear reports using relevant and reliable information should be prepared. Preparing reports on

Integrity

The management accountant has a responsibility to avoid actual or apparent conflicts of interest

Credibility

The management accountant’s Standards of Ethical Conduct require that information should be

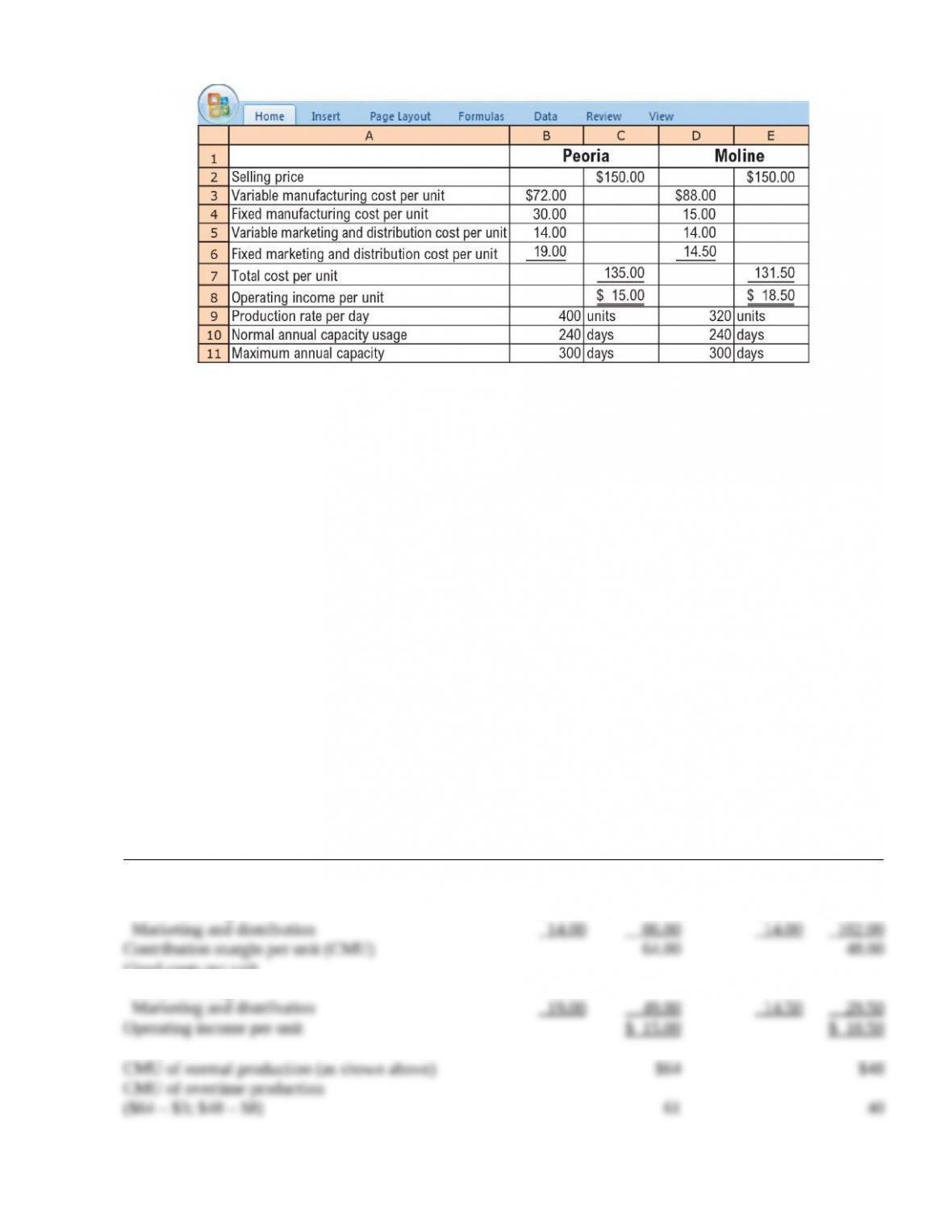

3-54 Deciding where to produce. (CMA, adapted) Portal Corporation produces the same

power generator in two Illinois plants, a new plant in Peoria and an older plant in Moline. The

following data are available for the two plants:

All fixed costs per unit are calculated based on a normal capacity usage consisting of 240

working days. When the number of working days exceeds 240, overtime charges raise the

variable manufacturing costs of additional units by $3.00 per unit in Peoria and $8.00 per unit in

Moline.

Portal Corporation is expected to produce and sell 192,000 power generators during the

coming year. Wanting to take advantage of the higher operating income per unit at Moline, the

company’s production manager has decided to manufacture 96,000 units at each plant, resulting

in a plan in which Moline operates at maximum capacity (320 units per day × 300 days) and

Peoria operates at its normal volume (400 units per day × 240 days).

Required:

1. Calculate the breakeven point in units for the Peoria plant and for the Moline plant.

2. Calculate the operating income that would result from the production manager’s plan to

produce 96,000 units at each plant.

3. Determine how the production of 192,000 units should be allocated between the Peoria and

Moline plants to maximize operating income for Portal Corporation. Show your calculations.

SOLUTION

(35 min.) Deciding where to produce.

Peoria Moline

Selling price $150.00 $150.00

Variable cost per unit

Manufacturing $72.00 $88.00

Fixed costs per unit

Manufacturing 30.00 15.00

1.

Annual fixed costs = Fixed cost per unit

´

Daily

´

($49

´

400 units

´

240 days;

´

´

¸

¸

2.

Normal annual volume (units)

CM from overtime production units

(0; 19,200

´

$40)

0 768,000

Total contribution margin 6,144,000 4,454,400

3. The optimal production plan is to produce 120,000 units at the Peoria plant and 72,000

units at the Moline plant. The full capacity of the Peoria plant, 120,000 units (400 units × 300

days), should be used because the contribution from these units is higher at all levels of

production than is the contribution from units produced at the Moline plant.

Contribution margin per plant:

Peoria, 96,000 × $64 $ 6,144,000

The contribution margin is higher when 120,000 units are produced at the Peoria plant and

Try It 3-1 Solution

Equation Method:

Selling Quantity of Variable cost Quantity of Fixed Operating

price units sold per unit units sold costs income

é ù

æ ö æ ö æ ö æ ö

´ – ´ – =

ê ú

ç ÷ ç ÷ ç ÷ ç ÷

è ø è ø è ø è ø

ë û

Operating income =

Contribution Method:

Operating income = $100 × 2,000 – $150,000 = $50,000

Try It 3-2 Solution

Breakeven Fixed costs $150,000 1,500 units

number of units Contribution margin per unit $100 per unit

= = =

Breakeven revenues Breakeven number of units Selling price

1,500 units $500 per unit $750, 000

= ´

= ´ =

(b)

Selling Quantity of Variable cost Quantity of Fixed Operating

price units sold per unit units sold costs income

é ù

æ ö æ ö æ ö æ ö

´ – ´ – =

ê ú

ç ÷ ç ÷ ç ÷ ç ÷

è ø è ø è ø è ø

ë û

(Equation 1)

We denote by Q the unknown quantity of units Bernard Windows must sell to earn an

operating income of $100,000. Selling price is $500, variable cost per package is $400, fixed

Target Target

Target net income Tax rate

operating income operating income

Target net income (Target operating income) (1 Tax rate)

Target net income $63,000

Target operating income 1 Tax rate 1

æ æ æ æ

= ´

æ æ æ æ

æ æ æ æ

= ´

= =

$90,000

0.30

=

In other words, to earn a target net income of $63,000, Bernard Windows’s target operating

Proof: Target operating income $90,000

The key step is to take the target net income number and convert it into the corresponding target

operating income number. We can then use equation 1 to determine the target operating income

Budgeted Breakeven

Margin of safety $1,200,000 $750, 000 $450,000

revenues revenues

Margin of Budgeted Breakeven 2, 400 1,500 900 units

safety (in units) sales (units) sales (units)

= – = – =

= – = – =

The margin of safety indicates that sales would have to decrease by 900 units and revenues by

$450,000 before the breakeven point is reached.

Sometimes margin of safety is expressed as a percentage:

( )

Margin of safety in dollars

Margin of safety percentage Budgeted or actual revenues

=

In our example, margin of safety percentage

$450,000 37.5%

$1, 200, 000

= =

Try It 3-5 Solution

At any given level of sales,

Degree of Contribution margin

operating leverage Operating income

=

The following table shows the degree of operating leverage at sales of 2,500 units for the two

options.

Option 1

No Commission

Option 2

5% Commission

1. Selling price $ 500 $ 500

2. Variable cost ($400; $400 + 0.05 × $500) $ 400 $ 425

3. Contribution margin per unit $ 100 $ 75

These results indicate that, when sales are 2,500 units, a 1% change in sales and contribution

margin will result in 2.5% change in operating income for Option 1. For Option 2, a 1% change

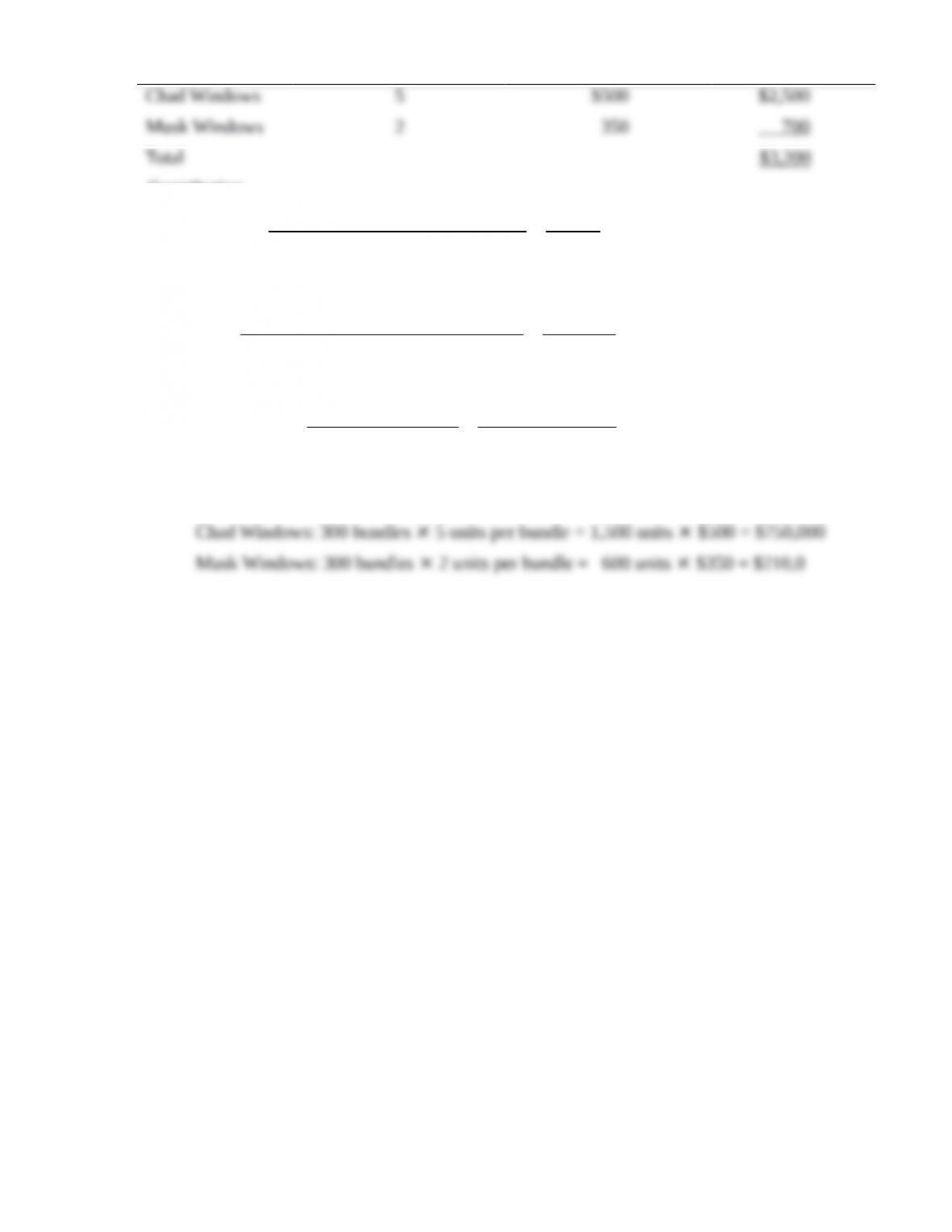

We assume that the budgeted sales mix (2,500 units of Chad Windows sold for every 1,000 units

of Musk Windows sold, that is, a ratio of 5:2) will not change at different levels of total unit

Each bundle yields a contribution margin of $650, calculated as follows:

Number of Units of

Chad Windows and

Musk Windows in

Each Bundle

Contribution Margin

per Unit for Chad

Windows and Musk

Windows

Contribution

Margin of the

Bundle

Chad Windows 5 $100 $500

Musk Windows 2 75 150

Total $650

To compute the breakeven point, we calculate the number of bundles Bernard needs to sell.

Breakeven Fixed costs $195,000

point in 300 bundles

Contribution margin per bundle $650 per bundle

bundles

= = =

The breakeven point in units of Chad Windows and Musk Windows is as follows:

The breakeven point in dollars for Chad Windows and Musk Windows is as follows:

When there are multiple products, it is often convenient to use the contribution margin

percentage. Under this approach, Bernard also calculates the revenues from selling a bundle of 5

units of Chad Windows and 2 units of Musk Windows:

Number of Units of

Chad Windows and

Musk Windows in Each

Bundle

Selling Price for Chad

Windows and Musk

Windows

Revenue of the

Bundle

Contribution

margin Contribution margin of the bundle $650 0.203125, or 20.3125%

percentage for Revenue of the bundle $3, 200

the bundle

= = =

Breakeven Fixed costs $195, 000 $960, 000

revenues Contribution margin % for the bundle 0.203125

= = =

Number of bundles Breakeven revenues $960,000

required to be sold 300 bundles

Revenue per bundle $3, 200 per bundle

to break even

= = =

The breakeven point in units and dollars for Chad Windows and Musk Windows are as follows: