SOLUTION

(30 min.) Direct-cost and selling price variances.

1. Computing unit selling prices and unit costs of inputs:

Actual selling price = $3,626,700 ÷ 462,000

2., 3., and 4.

The actual and budgeted unit costs are:

Actual Budgeted

Direct materials

Direct manuf. labor

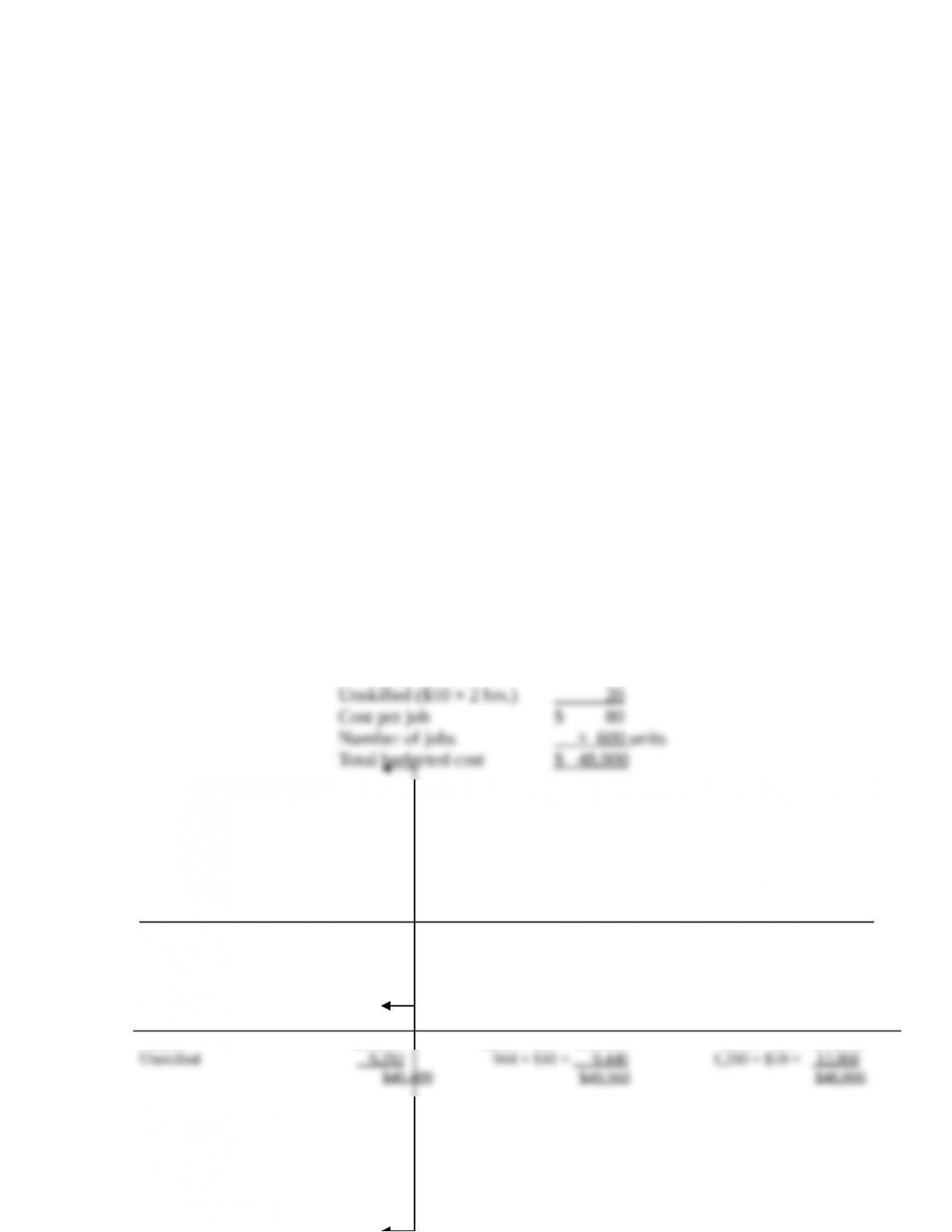

The actual output achieved is 462,000 Mini SDs.

The direct cost price and efficiency variances are:

Actual Costs

Incurred

(Actual Input Qty.

× Actual Price)

(1)

Price

Variance

(2)=(1)–(3)

Actual

Input Qty.

× Budgeted

Price

(3)

Efficiency

Variance

(4)=(3)–(5)

Flex. Budget

(Budgeted Input

Qty. Allowed for

Actual Output

× Budgeted Price)

(5)

Direct materials

Direct manuf. labor costs

Comments on the variances include:

Selling price variance. This may arise from a proactive decision to reduce price to ex–

Material price variance. The $0.01 increase in the price per connector pin could arise

Material efficiency variance. For all three material inputs, usage is greater than bud–

Labor efficiency variance. There is a small favorable efficiency variance for setup la–

Labor price variance. There is an unfavorable price variance for fabrication as a result of the

$1 higher wage per hour paid for that labor. The higher labor quality could also explain the sig–

nificant efficiency variance for fabrication labor7-46 Variances in the service sector. Derek Wilson oper-

ates Clean Ride Enterprises, an auto detailing company with 20 employees. Jamal Jackson has recently been hired

by Wilson as a controller. Clean Ride’s previous accountant had done very little in the area of variance analysis, but

Jackson believes that the company could benefit from a greater understanding of his business processes. Because of

the labor-intensive nature of the business, he decides to focus on calculating labor variances.

Jackson examines past accounting records, and establishes some standards for the price and

quantity of labor. While Clean Ride’s employees earn a range of hourly wages, they fall into two

general categories: skilled labor, with an average wage of $20 per hour, and unskilled labor, with

an average wage of $10 per hour. One standard 5-hour detailing job typically requires a combina–

tion of 3 skilled hours and 2 unskilled hours.

Actual data from last month, when 600 detailing jobs were completed, are as follows:

Skilled (2,006 hours) $ 39,117

Unskilled (944 hours) 9,292

Total actual direct labor cost $ 48,409

Looking over last month’s data, Jackson determines that Clean Ride’s labor price variance

was $1,151 favorable, but the labor efficiency variance was $1,560 unfavorable. When Jackson

presents his findings to Wilson, the latter is furious. “Do you mean to tell me that my employees

wasted $1,560 worth of time last month? I’ve had enough. They had better shape up, or else!”

Jackson tries to calm him down, saying that in this case the efficiency variance doesn’t necessari–

ly mean that employees were wasting time. Jackson tells him that he is going to perform a more

detailed analysis, and will get back to him with more information soon.

Required:

1. What is the budgeted cost of direct labor for 600 detailing jobs?

2. How were the $1,151 favorable price variance and the $1,560 unfavorable labor efficiency

variance calculated? What was the company’s flexible-budget variance?

3. What do you think Jackson meant when said that “in this case the efficiency variance doesn’t

necessarily mean that employees were wasting time”?

4. For the 600 detailing jobs performed last month, what is the actual direct labor input mix per–

centage? What was the standard mix for labor?

5. Calculate the total direct labor mix and yield variances.

6. How could these variances be interpreted? Did the employees waste time? Upon further in–

vestigation, you discover that there were some unfilled vacancies last month in the unskilled

labor positions that have recently been filled. How will this new information likely impact

the variances going forward?

SOLUTION

(35 min.) Variances in the service sector

1.

Skilled ($20 × 3 hrs.) $ 60

2. Solution Exhibit 7-46A presents the total price variance ($318 F), the total efficiency variance

($2,200 U), and the total flexible-budget variance ($1,882 U).

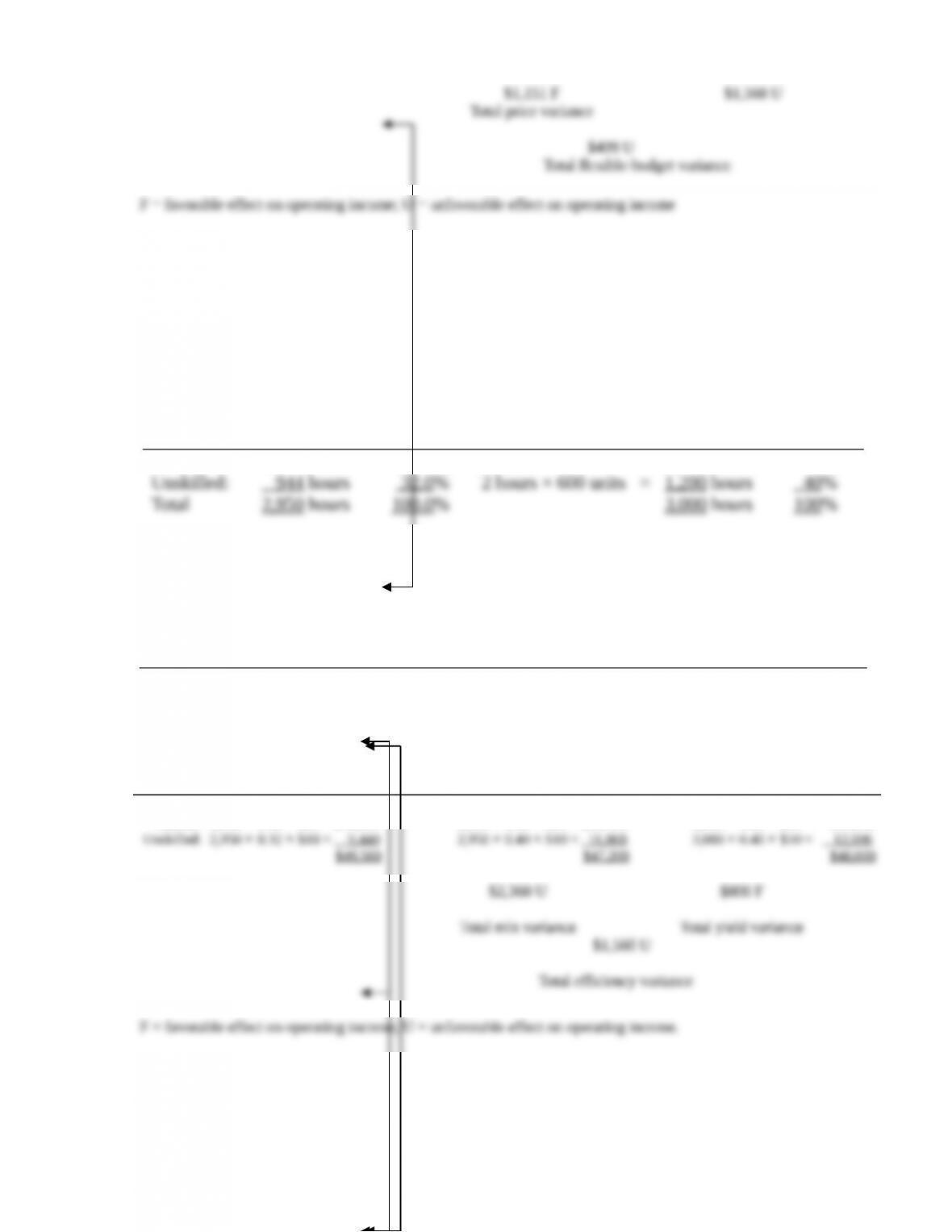

SOLUTION EXHIBIT 7-46A

Columnar Presentation of Direct Labor Price and Efficiency Variances for Clean Ride Enterprises

Actual Costs

Incurred

(Actual Input Quantity

× Actual Price)

(1)

Actual Input Quantity

× Budgeted Price

(2)

Flexible Budget

(Budgeted Input Quantity

Allowed for Actual Output

× Budgeted Price)

(3)

Skilled

$39,117

2,006 × $20 = $40,120

1,800 × $20 = $36,000

3. In a company where there is a mixture of workers, some at higher wages and others at lower,

all working on the same projects, an unfavorable efficiency variance can be the result of which

employees worked on the project, not just how many hours were spent. If higher paid workers

worked more than their standard percentage of the time, an unfavorable efficiency variance will

result.

4.

Actual Quan-

tity

of Input

Actual

Mix

Budgeted Quantity

of Input for Actual Output

Budgeted

Mix

Skilled: 2,006 hours 68.0% 3 hours × 600 units = 1,800 hours 60%

5. Solution Exhibit 7-46B presents the total direct labor yield and mix variances for Clean Ride

Enterprises.

SOLUTION EXHIBIT 7-46B

Columnar Presentation of Direct Labor Yield and Mix Variances for Clean Ride Enterprises

Actual Total Quantity

of All Inputs Used

× Actual Input Mix

× Budgeted Price

(1)

Actual Total Quantity

of All Inputs Used

× Budgeted Input Mix

× Budgeted Price

(2)

Flexible Budget:

Budgeted Total Quantity of

All Inputs Allowed for

Actual Output ×

Budgeted Input Mix

× Budgeted Price

(3)

Skilled: 2,950 × 0.68 × $20 = $40,120

2,950 × 0.60 × $20 = $35,400

3,000 × 0.60 × $20 = $36,000

6. While the efficiency variance was unfavorable, it was due to the mix of labor, not the total

hours used. The unfavorable mix variance is the result of a higher than standard percentage of

7-47 Price and efficiency variances, benchmarking and ethics. Sunto Scientific manufac-

tures GPS devices for a chain of retail stores. Its most popular model, the Magellan XS, is assem–

bled in a dedicated facility in Savannah, Georgia. Sunto is keenly aware of the competitive threat

from smartphones that use Google Maps and has put in a standard cost system to manage pro-

duction of the Magellan XS. It has also implemented a just-in-time system so the Savannah facil–

ity operates with no inventory of any kind.

Producing the Magellan XS involves combining a navigation system (imported from Sunto’s

plant in Dresden at a fixed price), an LCD screen made of polarized glass, and a casing devel–

oped from specialty plastic. The budgeted and actual amounts for Magellan XS for July 2017

were as follows:

Budgeted Amounts Actual Amounts

Magellan XS units produced 4,000 4,400

Navigation systems cost $81,600 $89,000

Navigation systems 4,080 4,450

Polarized glass cost $40,000 $40,300

Sheets of polarized glass used 800 816

Plastic casing cost $12,000 $12,500

Ounces of specialty plastic used 4,000 4,250

Direct manufacturing labor costs $36,000 $37,200

Direct manufacturing labor-hours 2,000 2,040

The controller of the Savannah plant, Jim Williams, is disappointed with the standard costing

system in place. The standards were developed on the basis of a study done by an outside consul–

tant at the start of the year. Williams points out that he has rarely seen a significant unfavorable

variance under this system. He observes that even at the present level of output, workers seem to

have a substantial amount of idle time. Moreover, he is concerned that the production supervisor,

John Kelso, is aware of the issue but is unwilling to tighten the standards because the current le–

nient benchmarks make his performance look good.

Required:

1. Compute the price and efficiency variances for the three categories of direct materials and for

direct manufacturing labor in July 2017.

2. Describe the types of actions the employees at the Savannah plant may have taken to reduce

the accuracy of the standards set by the outside consultant. Why would employees take those

actions? Is this behavior ethical?

3. If Williams does nothing about the standard costs, will his behavior violate any of the stan–

dards of ethical conduct for practitioners described in the IMA Statement of Ethical Profes–

sional Practice (see Exhibit 1-7 on page 17)?

4. What actions should Williams take?

5. Williams can obtain benchmarking information about the estimated costs of Sunto’s competi–

tors such as Garmin and TomTom from the Competitive Intelligence Institute (CII). Discuss

the pros and cons of using the CII information to compute the variances in requirement 1.

SOLUTION

(30 min.) Price and efficiency variances, benchmarking and ethics.

1. Budgeted navigation systems per unit = 4,080 systems ÷ 4,000 units = 1.02 systems

Budgeted cost of navigation system = $81,600 ÷ 4,080 units = $20 per system

Budgeted sheets of polarized glass per unit = 800 sheets ÷ 4,000 units = 0.20 sheets

Budgeted cost of sheet of polarized glass = $40,000 ÷ 800 sheets = $50 per sheet

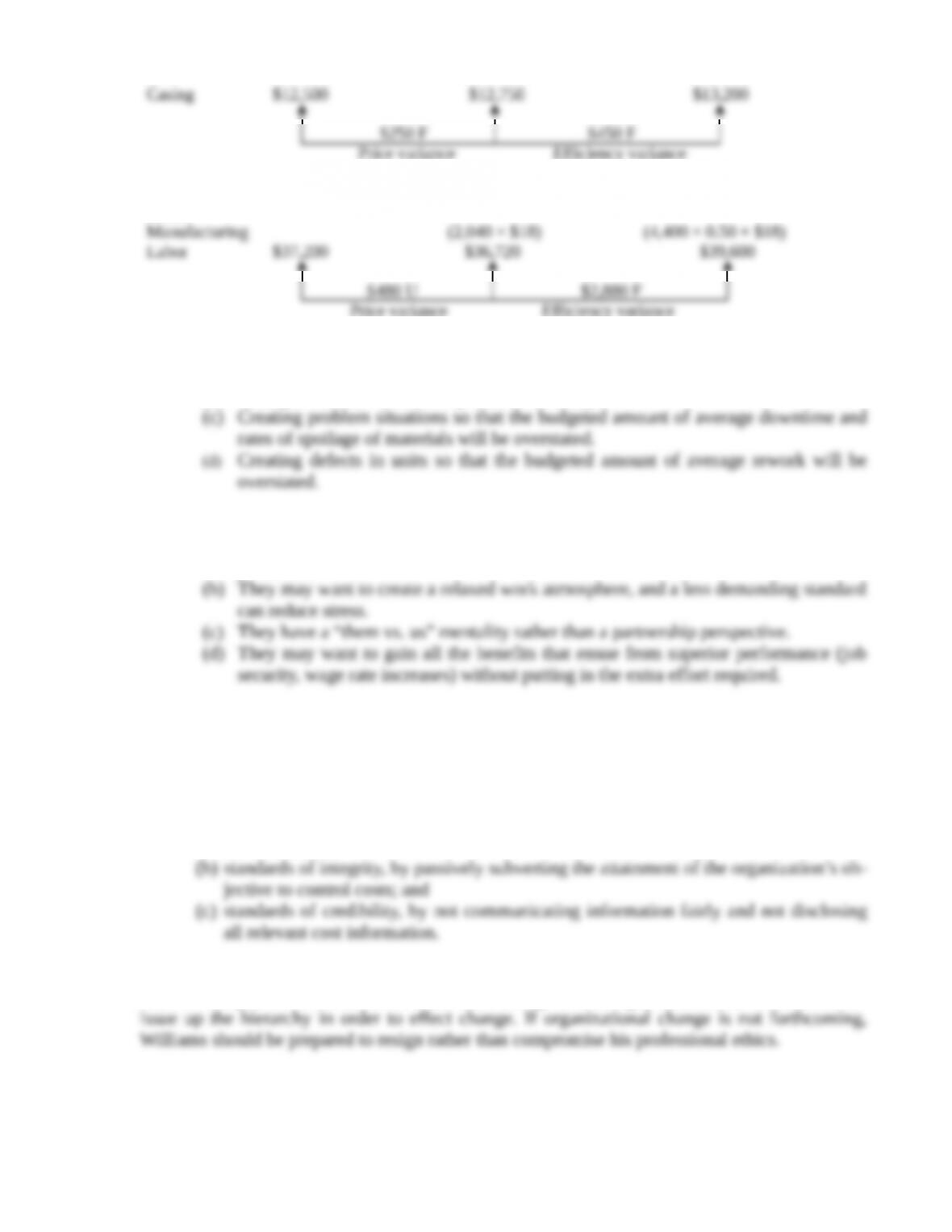

Flexible Budget

Actual Costs (Budgeted Input

Incurred Qty. Allowed for

(Actual Input Qty. Actual Input Qty. Actual Output

× Actual Price) × Budgeted Price × Budgeted Price)

$0 $760 F

Price variance Efficiency variance

Price variance Efficiency variance

Direct

Price variance Efficiency variance

2. Actions employees may have taken include:

(a) Adding steps that are not necessary in working on a GPS unit.

(b) Taking more time on each step than is necessary.

Employees may take these actions for several possible reasons.

(a) They may be paid on a piece-rate basis with incentives for above-budgeted

production.

This behavior is unethical if it is deliberately designed to undermine the credibility of the

standards used at Sunto Scientific.

3. If Williams does nothing about standard costs, his behavior will violate the “Standards of

Ethical Conduct for Management Accountants.” In particular, he would be violating the

(a) standards of competence, by not performing technical duties in accordance with rele–

vant standards;

4. Williams should discuss the situation with Kelso and point out that the standards are lax

and that this practice is unethical. If Kelso does not agree to change, Williams should escalate the

5. Main pros of using Competitive Intelligence Institute information to compute variances

are

(a) Highlights to Sunto in a direct way how it may or may not be cost-competitive.

(b) Provides a “reality check” to many internal positions about efficiency or

effectiveness.

Try It! 7-1

(a) Static-budget variance for revenues = (28,000 units × $11) − (27,500 units × $12)

(b) Static-budget variance for variable costs = $90,000 − (27,500 units × $3)

(c) Static-budget variance for fixed costs = $55,000 − $58,000

Actual Static Static-Budget

Results Budget Variance

Units sold 28,000 27,500

Revenues $308,000 $330,000 $22,000 U

Try It! 7-2

(a) Flexible budget for revenues = Actual units × Budgeted selling price per unit

(b) Flexible budget for variable costs = Actual units × Budgeted variable cost per unit

(c) Flexible budget for fixed costs = Static budget

Try It! 7-3

Variance Analysis for Zenefit Corporation

Actual

Results

(1)

Flexible-

Budget

Variances

(2) = (1)-(3)

Flexible

Budget

(3)

Sales –

Volume

Variance

(4) = (3)-(5)

Static

Budget

(5)

Units sold 28,000 28,000 27,500

Try It! 7-4

a. Direct materials variances:

Actual unit cost = $68,600/14,000 square yards

b. Direct manufacturing labor variances: