SOLUTION

(25–30 min.) Strategic analysis of operating income (continuation of 12-21).

1. Operating Income Statement

2016 2017

Revenues ($30

´

200,000; $31

´

225,000)

$6,000,000 $6,975,000

2. The Growth Component

Revenue effect

of growth

=

Actual units of Actual units of

output sold output sold

in 2017 in 2016

–

æ ö

ç ÷

è ø

×

Selling

price

in 2016

Cost effect of

growth for

variable costs

=

Units of input Actual units of

required to input used

produce 2017 to produce

output in 2016 2016 ouput

–

æ ö

ç ÷

ç ÷

è ø

×

Input

price

in 2016

Cost effect of

growth for

fixed costs

=

Actual units of capacity in Actual

2016 because adequate units of

capacity exists to produce capacity

2017 output in 2016 in 2016

–

æ ö

ç ÷

ç ÷

è ø

×

Price per unit

of capacity

in 2016

225,000 215,000

200,000

æ ö

´

ç ÷

è ø

change because adequate capacity exists in 2016 to support year 2017 output and customers.

The cost effects of growth component are

12-8

In summary, the net increase in operating income as a result of the growth component equals:

The Price-Recovery Component

Revenue effect of

price-recovery

( )

Actual units

Selling price Selling price

= of output

in 2017 in 2016 sold in 2017

– ´

Cost effect of

price-recovery for

variable costs

=

Input Input

price in price in

2017 2016

æ ö

ç ÷

–

ç ÷

è ø

×

Units of input required

to produce 2017

output in 2016

Cost effect of

price-recovery for

fixed costs

=

Price per Price per

unit of unit of

capacity capacity

in 2017 in 2016

–

æ ö

ç ÷

ç ÷

ç ÷

è ø

×

Actual units of capacity in

2016 because adequate

capacity exists to produce

2017 output in 2016

In summary, the net increase in operating income as a result of the price-recovery component

equals:

The Productivity Component

Cost effect of

productivity for

variable costs

=

Actual units of Units of input

input used required to

to produce produce 2017

2017 output ouput in 2016

–

æ ö

ç ÷

ç ÷

è ø

´

Input

price

in 2017

Cost effect of

productivity for

fixed costs

=

Actual Actual units of capacity in

units of 2016 because adequate

capacity capacity exists to produce

in 2017 2017 output in 2016

–

æ ö

ç ÷

ç ÷

è ø

´

Price per

unit of

capacity

in 2017

12-8

The productivity component of cost changes are

The change in operating income between 2016 and 2017 can be analyzed as follows:

Income

Statement

Amounts

in 2016

(1)

Revenue and

Cost Effects

of Growth

in 2017

(2)

Revenue and

Cost Effects of

Price-Recovery

in 2017

(3)

Cost Effect

of

Productivity

in 2017

(4)

Income

Statement

Amounts

in 2017

(5) =

(1) + (2) + (3) + (4)

Change in operating income

3. The analysis of operating income indicates that growth, price-recovery, and productivity

all resulted in favorable changes in operating income in 2017. Further, a significant amount of

12-23 Analysis of growth, price-recovery, and productivity components (continuation of

12-21 and 12-22). Refer to Exercise 12-21. Suppose that the market for

silk-screened T-shirts grew by 10% during 2017. All increases in sales greater

than 10% are the result of Gianni’s strategic actions.

Required:

Calculate the change in operating income from 2016 to 2017 due to growth in market size,

product differentiation, and cost leadership. How successful has Gianni been in implementing its

strategy? Explain.

SOLUTION

(20 min.) Analysis of growth, price-recovery, and productivity components

(continuation of 12-22).

Effect of the industry-market-size factor on operating income

12-8

The change in Gianni’s operating income from the industry-market size factor rather than

from specific strategic actions is:

$346,875 (the growth component in Exercise 12-22)

20,000

25, 000

$277 ,500 F

Effect of product differentiation on operating income

The change in operating income due to:

Increase in the selling price (revenue effect of price recovery) $225,000 F

Decrease in price of inputs (cost effect of price recovery) 429,750 F

Growth in market share due to product differentiation

$346,875 (the growth component in Exercise 12-22)

5,000

25, 000

69 ,375 F

Change in operating income due to product differentiation $724 ,125 F

Effect of cost leadership on operating income

The change in operating income from cost leadership is:

The change in operating income between 2016 and 2017 can be summarized as follows:

Gianni has been very successful in implementing its product differentiation strategy.

12-24 Identifying and managing unused capacity (continuation of 12-21). Refer to Exercise

12-21.

Required:

1. Calculate the amount and cost of unused administrative capacity at the beginning of 2017,

based on the actual number of customers Gianni served in 2017.

2. Suppose Gianni can only add or reduce administrative capacity in increments of 250

customers. What is the maximum amount of costs that Gianni can save in 2017 by

downsizing administrative capacity?

3. What factors, other than cost, should Gianni consider before it downsizes administrative

12-8

capacity?

SOLUTION

(15 min.) Identifying and managing unused capacity (continuation of 12-21).

1. The amount and cost of unused capacity at the beginning of year 2017 based on year

2017 needs follows:

Amount of Cost of

Unused Unused

Capacity Capacity

2. Gianni can reduce administrative capacity by another 750 customers (4,250 – 750 =

´

3. Before Gianni downsizes administrative capacity, it should consider whether sales

increases in the future would lead to a greater demand for and utilization of capacity as new

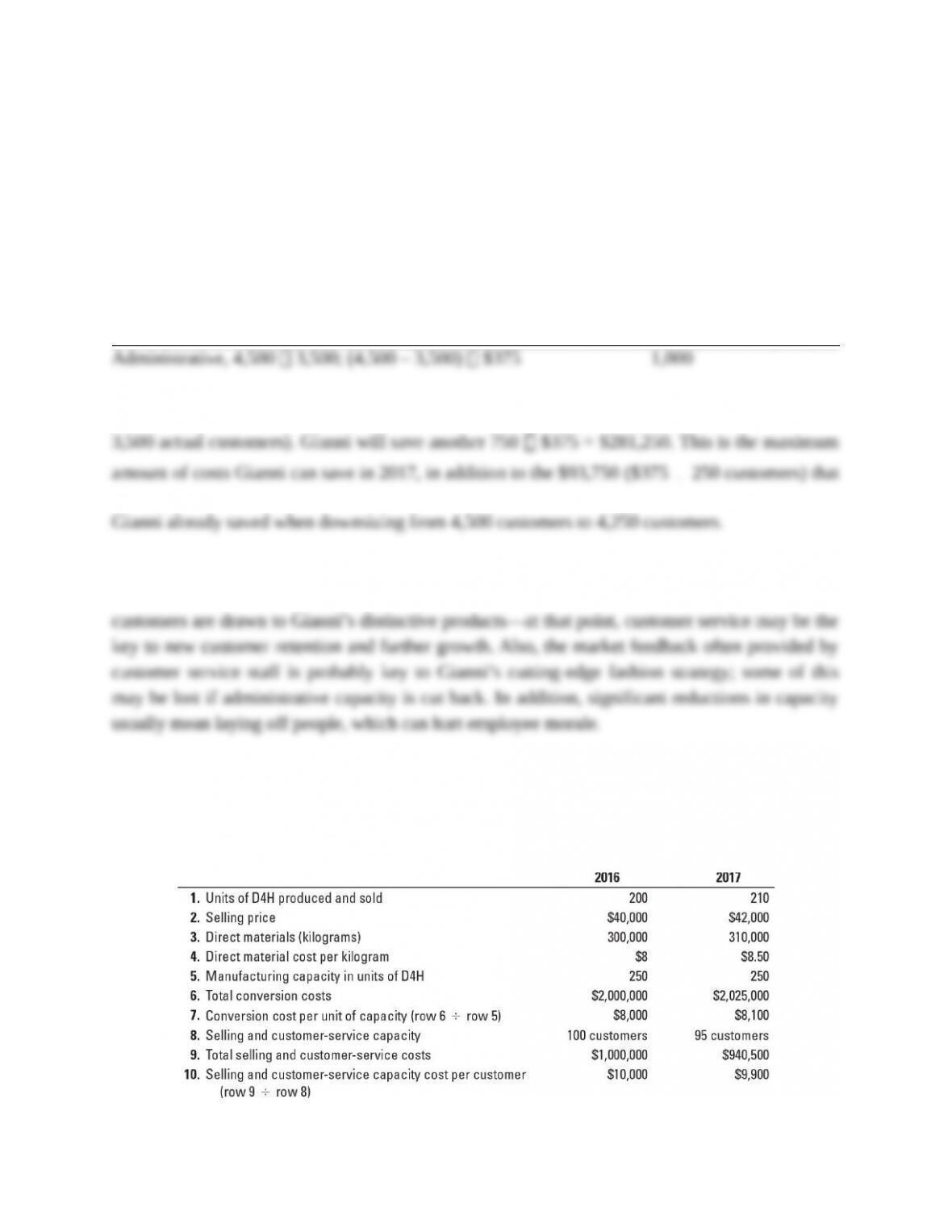

12-25 Strategy, balanced scorecard. Stanmore Corporation makes a special-purpose machine,

D4H, used in the textile industry. Stanmore has designed the D4H machine for 2017 to be

distinct from its competitors. It has been generally regarded as a superior machine. Stanmore

presents the following data for 2016 and 2017.

12-8

Stanmore produces no defective machines, but it wants to reduce direct materials usage per D4H

machine in 2017. Conversion costs in each year depend on production capacity defined in terms

of D4H units that can be produced, not the actual units produced. Selling and customer-service

costs depend on the number of customers that Stanmore can support, not the actual number of

customers it serves. Stanmore has 75 customers in 2016 and 80 customers in 2017.

Required:

1. Is Stanmore’s strategy one of product differentiation or cost leadership? Explain briefly.

2. Describe briefly key measures that you would include in Stanmore’s balanced scorecard and

the reasons for doing so.

SOLUTION

(15 min.) Strategy, balanced scorecard.

1. Stanmore Corporation follows a product differentiation strategy in 2017. Stanmore’s D4H

2. Balanced Scorecard measures for 2017 follow:

Financial Perspective

Customer Perspective

(1) Market share in high-end special-purpose textile machines, (2) customer satisfaction, (3) new

customers

Internal Business Process Perspective

(1) Manufacturing quality and reduced wastage of direct materials, (2) new product features

added, (3) order delivery time

Learning and Growth Perspective

12-8

12-26 Strategic analysis of operating income (continuation of 12-25). Refer to

Exercise 12-25.

Required:

1. Calculate the operating income of Stanmore Corporation in 2016 and 2017.

2. Calculate the growth, price-recovery, and productivity components that explain the change in

operating income from 2016 to 2017.

3. Comment on your answer in requirement 2. What do these components indicate?

SOLUTION

(30 min.) Strategic analysis of operating income (continuation of 12-25).

1. Operating income for each year is as follows:

2016 2017

2. The Growth Component

Revenue effect

of growth

=

Actual units Actual units of Selling

of output sold output sold price

in 2017 in 2016 in 2016

– ´

æ ö

ç ÷

ç ÷

è ø

12-8

Cost effect of

growth for

variable costs

=

Units of Actual units

input required of inputs

to produce used to

2017 output produce

in 2016 2016 ouput

–

æ ö

ç ÷

ç ÷

ç ÷

è ø

´

Input

price

in 2016

Cost effect of

growth for

fixed costs

=

Actual units of capacity in Actual

2016 because adequate units of

capacity exists to produce capacity

2017 output in 2016 in 2016

–

æ ö

ç ÷

ç ÷

è ø

×

Price per unit

of capacity

in 2016

Kilograms of direct materials that would be required in 2017 to produce 210 units instead of the

200 units produced in 2016, assuming the 2016 input-output relationship continued into 2017,

equal 315,000 kilograms

300,000 210

200

æ ö

´

ç ÷

è ø

. Manufacturing conversion costs and selling and

customer-service capacity will not change because adequate capacity exists in 2016 to support

year 2017 output and customers.

The cost effects of growth component are:

Direct materials costs (315,000 300,000) $8 = $120,000 U

Manufacturing conversion costs (250 250) $8,000 = 0

Selling & customer-service costs (100 100) $25,000 = 0

Cost effect of growth $120 ,000 U

In summary, the net increase in operating income as a result of the growth component equals:

The Price-Recovery Component

Revenue effect of

price-recovery

()

Actual units

Selling price Selling price

= of output

in 2017 in 2016 sold in 2017

– ´

12-8

Cost effect of

price-recovery for

variable costs

=

Input Input

price in price in

2017 2016

–

æ ö

ç ÷

è ø

×

Units of input

required to

produce 2017

output in 2016

Cost effect of

price-recovery for

fixed costs

=

Price per Price per

unit of unit of

capacity capacity

in 2017 in 2016

–

æ ö

ç ÷

ç ÷

è ø

×

Actual units of capacity in

2016 because adequate

capacity exists to produce

2017 output in 2016

In summary, the net increase in operating income as a result of the price-recovery component equals:

The Productivity Component

Cost effect of

productivity for

variable costs

=

Actual units of Units of input

input used required to

to produce produce 2017

2017 output ouput in 2016

–

æ ö

ç ÷

ç ÷

è ø

´

Input

price

in 2017

Cost effect of

productivity for

fixed costs

=

Actual Actual units of capacity in

units of 2016 because adequate

capacity capacity exists to produce

in 2017 2017 output in 2016

–

æ ö

ç ÷

ç ÷

è ø

´

Price per

unit of

capacity

in 2017

The productivity component of cost changes are

The change in operating income between 2016 and 2017 can be analyzed as follows:

Income

Statement

Amounts

in 2016

(1)

Revenue and

Cost Effects

of Growth

Component

in 2017

(2)

Revenue and

Cost Effects of

Price-Recovery

Component

in 2017

(3)

Cost Effect

of

Productivity

Component

in 2017

(4)

Income

Statement

Amounts in 2017

(5) =

(1) + (2) + (3) + (4)

12-8

Change in operating income

3. The analysis of operating income indicates that a significant amount of the increase in

operating income resulted from Stanmore’s product differentiation strategy. The company was

able to continue to charge a premium price while growing sales. Stanmore was also able to earn

12-27 Analysis of growth, price-recovery, and productivity components (continuation of

12-25 and 12-26). Suppose that during 2017, the market for Stanmore’s special-purpose

machines grew by 3%. All increases in market share (that is, sales increases greater than 3%) are

the result of Stanmore’s strategic actions.

Required:

Calculate how much of the change in operating income from 2016 to 2017 is due to the

industry-market-size factor, product differentiation, and cost leadership. How successful has

Stanmore been in implementing its strategy? Explain.

12-8