SOLUTION

(50 min.) Activity-based costing.

1. Overhead allocation using a simple job-costing system, where overhead is allocated based

on machine hours:

Job 220 Job 330

2. Overhead allocation using an activity-based job-costing system:

Budgeted

Overhead

(1)

Activity Driver

(2)

Budgeted

Activity Driver

(3)

Activity Rate

(4) = (1) (3)

Purchasing $ 28,500 Purchase orders processed 1,500 $19.00

Job 220 Job 330

Overhead allocated

Purchasing ($19 21; 9 orders) $399 $171

3. The manufacturing manager likely would find the ABC job-costing system more useful in

Marketing managers can use ABC information to bid for jobs more competitively because

ABC provides managers with a more accurate reflection of the resources used for and the costs

5-1

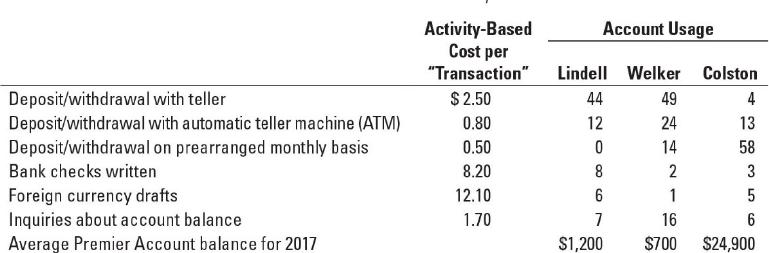

5-30 ABC, product costing at banks, cross-subsidization. United Savings Bank (USB) is

examining the profitability of its Premier Account, a combined savings and checking account.

Depositors receive a 2% annual interest rate on their average deposit. USB earns an interest rate

spread of 3% (the difference between the rate at which it lends money and the rate it pays

depositors) by lending money for home-loan purposes at 5%. Thus, USB would gain $60 on the

interest spread if a depositor had an average Premier Account balance of $2,000 in 2017

($2,000 3% = $60)

The Premier Account allows depositors unlimited use of services such as deposits,

withdrawals, checking accounts, and foreign currency drafts. Depositors with Premier Account

balances of $1,000 or more receive unlimited free use of services. Depositors with minimum

balances of less than $1,000 pay a $22-a-month service fee for their Premier Account.

USB recently conducted an activity-based costing study of its services. It assessed the

following costs for six individual services. The use of these services in 2017 by three customers

is as follows:

Assume Lindell and Colston always maintain a balance above $1,000, whereas Welker always

has a balance below $1,000.

Required

1. Compute the 2017 profitability of the Lindell, Welker, and Colston Premier Accounts at

USB.

2. Why might USB worry about the profitability of individual customers if the Premier Account

product offering is profitable as a whole?

3. What changes would you recommend for USB’s Premier Account?

SOLUTION

(30 min.) ABC, product-costing at banks, cross-subsidization.

5-2

1.

Lindell Welker Colston Total

Revenues

Spread revenue on annual basis

(3% ; $1,200, $700, $24,900)

Monthly fee charges

$ 36.00

$ 21.00

$747.00

$ 804.00

Costs

Deposit/withdrawal with teller

2. Cross-subsidization across individual Premier Accounts occurs when profits made on

some accounts are offset by losses on other accounts. The aggregate profitability on the three

5-3

The facts also suggest that the customers do not use the bank services uniformly. For

example, Lindell and Welker have a lot of transactions with the teller and also inquire about their

3. Possible changes USB could make are:

a. Offer higher interest rates on high-balance accounts to increase USB’s

competitiveness in attracting and retaining these accounts.

b. Introduce charges for individual services. The ABC study reports the cost of each

service. USB has to decide if it wants to price each service at cost, below cost, or

above cost. If it prices above cost, it may use advertising and other means to

encourage additional use of those services by customers. Of course, in determining its

pricing strategy, USB would need to consider how other competing banks are pricing

their products and services.

5-31 Job costing with single direct-cost category, single indirect-cost pool, law firm.

Wharton Associates is a recently formed law partnership. Denise Peyton, the managing partner

of Wharton Associates, has just finished a tense phone call with Gus Steger, president of Steger

Enterprises. Gus strongly complained about the price Wharton charged for some legal work done

for his company.

Peyton also received a phone call from its only other client, Bluestone, Inc., which was very

pleased with both the quality of the work and the price charged on its most recent job.

Wharton Associates operates at capacity and uses a cost-based approach to pricing (billing)

each job. Currently it uses a simple costing system with a single direct-cost category

(professional labor-hours) and a single indirect-cost pool (general support). Indirect costs are

allocated to cases on the basis of professional labor-hours per case. The job files show the

following:

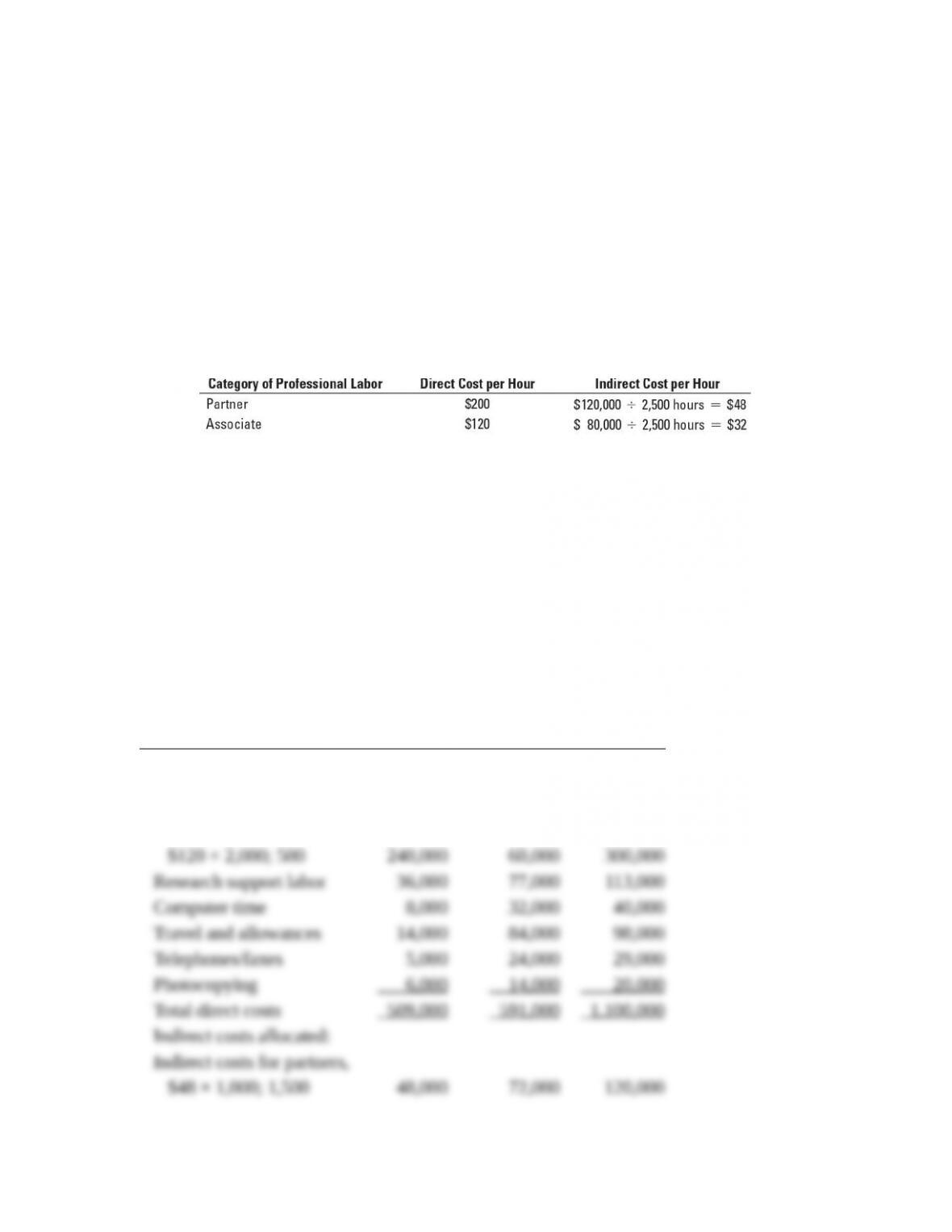

Professional labor costs at Bradley Associates are $160 an hour. Indirect costs are allocated to

cases at $100 an hour. Total indirect costs in the most recent period were $500,000.

Required

1. Why is it important for Bradley Associates to understand the costs associated with individual

jobs?

2. Compute the costs of the Steger Enterprises and Bluestone Inc. jobs using Bradley’s simple

costing system.

SOLUTION

5-4

(15 min.) Job costing with single direct-cost category, single indirect-cost pool, law

firm.

In some editions of the book, there are some references to Bradley Associates. All references

to Bradley Associates should be read as Wharton Associates.

1. Pricing decisions at Wharton Associates are heavily influenced by reported cost numbers.

Suppose Wharton is bidding against another firm for a client with a job similar to that of Steger

2. Steger Bluestone

Enterprises Inc. Total

Direct professional labor,

5-32 Job costing with multiple direct-cost categories, single indirect-cost pool, law firm

(continuation of 5-31). Peyton asks her assistant to collect details on those costs included in the

$500,000 indirect-cost pool that can be traced to each individual job. After analysis, Wharton is able

to reclassify $300,000 of the $500,000 as direct costs:

Peyton decides to calculate the costs of each job as if Wharton had used six direct-cost pools and

a single indirect-cost pool. The single indirect-cost pool would have $200,000 of costs and would

be allocated to each case using the professional labor-hours base.

Required

1. Calculate the revised indirect-cost allocation rate per professional labor-hour for Wharton

Associates when total indirect costs are $200,000.

2. Compute the costs of the Steger Enterprises and Bluestone Inc. jobs if Wharton Associates

had used its refined costing system with multiple direct-cost categories and one indirect-cost

pool.

3. Compare the costs of Steger Enterprises and Bluestone Inc. jobs in requirement 2 with those

in requirement 2 of Problem 5-31. Comment on the results.

5-5

SOLUTION

(20–25 min.) Job costing with multiple direct-cost categories, single indirect-cost

pool, law firm (continuation of 5-31).

1. Indirect costs = $200,000

2.

3.

Steger Bluestone

Enterprises Inc. Total

Problem 5-31 $780,000 $520,000 $1,300,000

The Problem 5-32 approach directly traces $300,000 of general support costs to the individual

jobs. In Problem 5-31, these costs are allocated on the basis of direct professional labor-hours.

5-33 Job costing with multiple direct-cost categories, multiple indirect-cost pools, law firm

(continuation of 5-31 and 5-32). Wharton has two classifications of professional staff: partners

5-6

Steger

Enterprises

Bluestone

Inc. Total

Direct costs:

Direct professional labor,

$160 × 3,000; $160 × 2,000

$480,000 $320,000 $ 800,000

and associates. Peyton asks his assistant to examine the relative use of partners and associates on

the recent Steger Enterprises and Bluestone Inc. jobs. The Steger Enterprises job used 1,000

partner-hours and 2,000 associate-hours. The Bluestone Inc. job used 1,500 partner-hours and 500

associate-hours. Therefore, totals of the two jobs together were 2,500 partner-hours and 2,500

associate-hours. Peyton decides to examine how using separate direct-cost rates for partners and

associates and using separate indirect-cost pools for partners and associates would have affected

the costs of the Steger Enterprises and Bluestone Inc. jobs. Indirect costs in each indirect-cost

pool would be allocated on the basis of total hours of that category of professional labor. From the

total indirect cost-pool of $200,000, $120,000 is attributable to the activities of partners and

$80,000 is attributable to the activities of associates.

The rates per category of professional labor are as follows:

Required

1. Compute the costs of the Steger Enterprises and Bluestone Inc. jobs using Wharton’s further

refined system, with multiple direct-cost categories and multiple indirect-cost pools.

2. For what decisions might Wharton Associates find it more useful to use this job-costing

approach rather than the approaches in Problem 5-31 or 5-32?

SOLUTION

(30 min.) Job costing with multiple direct-cost categories,

multiple indirect-cost pools, law firm (continuation of 5-31 and 5-32).

1. Steger Bluestone

Enterprises Inc. Total

Direct costs:

Partner professional labor,

$200 × 1,000; 1,500 $200,000 $300,000 $ 500,000

Associate professional labor,

5-7

Indirect costs for associates,

Steger Bluestone

Comparison Enterprises Inc. Total

Single direct cost/

The higher the percentage of costs directly traced to each case, and the greater the number of

homogeneous indirect cost pools linked to the cost drivers of indirect costs, the more accurate the

product cost of each individual case.

The Steger and Bluestone cases differ in how they use “resource areas” of Wharton Associates:

Steger Bluestone

Enterprises Inc.

Partner professional labor 40.0% 60.0%

The Steger Enterprises case makes relatively low use of the higher-cost partners but relatively

higher use of the lower-cost associates than does Bluestone Inc.. As a result, it also uses less of

2. The specific areas where the multiple direct/multiple indirect (MD/MI) approach can

provide better information for decisions at Wharton Associates include the following:

Pricing and product (case) emphasis decisions. In a bidding situation using single direct/single

indirect (SD/SI) or multiple direct/single indirect (MD/SI) data, Wharton may win bids for legal

5-8

From a strategic viewpoint, SD/SI or MD/SI exposes Wharton Associates to

cherry-picking by competitors. Other law firms may focus exclusively on Steger Enterprises-type

cases and take sizable amounts of “profitable” business from Wharton Associates. MD/MI

reduces the likelihood of Wharton Associates losing cases on which it would have made money.

Cost control. The MD/MI approach better highlights the individual cost areas at Wharton

Associates than does the SD/SI or MD/SI approaches:

MD/MI SD/SI MD/SI

Number of direct cost categories 7 1 7

MD/MI is likely to promote better cost-control practices than SD/SI or MD/SI, as the nine cost

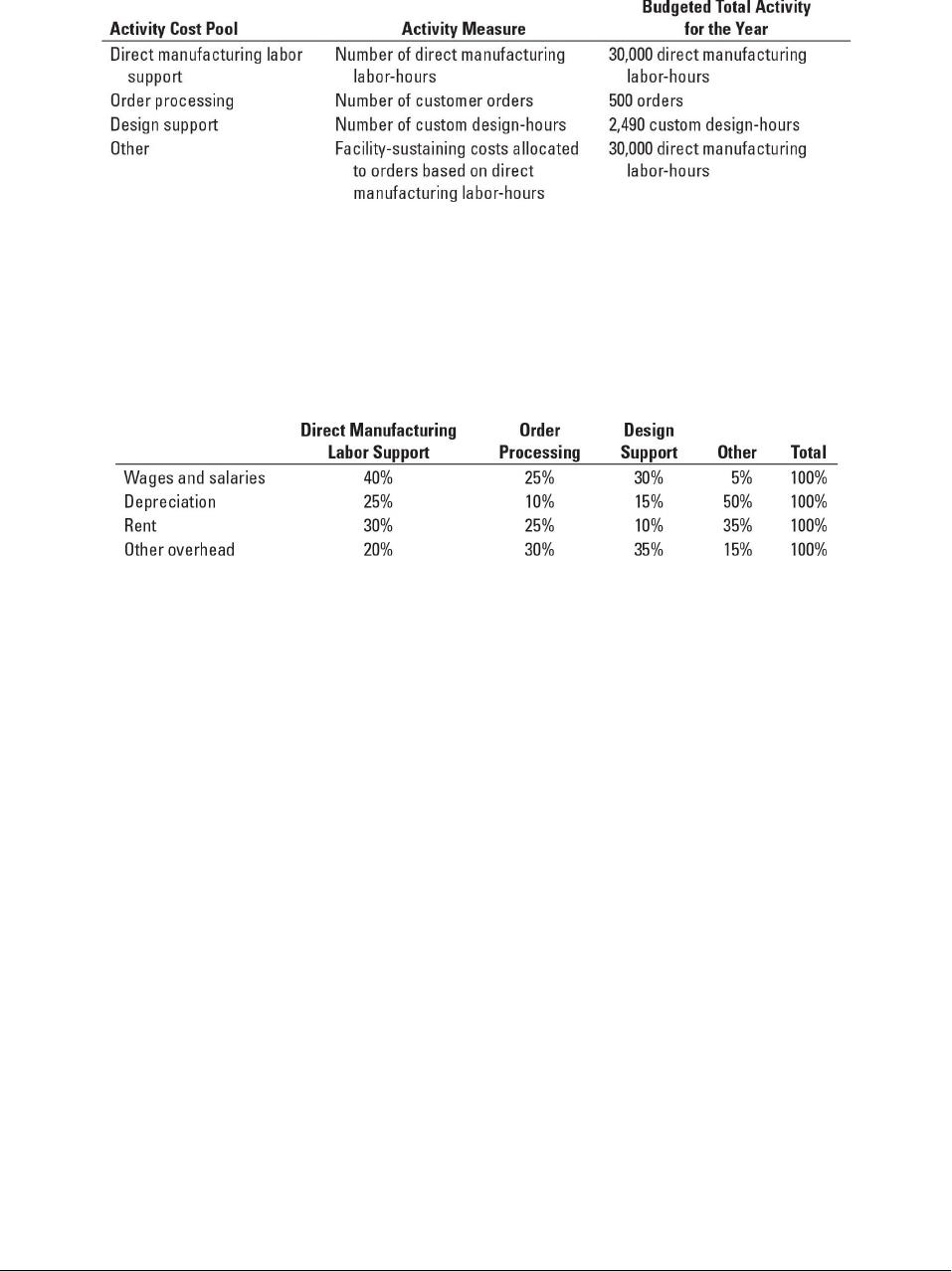

5-34 First-stage allocation, time-driven activity-based costing, manufacturing sector.

Marshall Devices manufactures metal products and uses activity-based costing to allocate

overhead costs to customer orders for pricing purposes. Many customer orders are won through

competitive bidding based on costs. Direct material and direct manufacturing labor costs are

traced directly to each order. Marshall’s direct manufacturing labor rate is $20 per hour. The

company reports the following budgeted yearly overhead costs:

Marshall has established four activity cost pools and the following budgeted activity for each

cost pool:

5-9

Some customer orders require more complex designs, while others need simple designs.

Marshall estimates that it will do 120 complex designs during a year, which will each take 11.75

hours for a total of 1,410 design-hours. It estimates it will do 180 simple designs, which will

each take 6 hours for a total of 1,080 design-hours.

Paul Napoli, Marshall’s controller, has prepared the following estimates for distribution of

the overhead costs across the four activity-cost pools:

Order 277100 consists of four different metal products. Three products require a complex design

and one requires a simple design. Order 277100 requires $4,550 of direct materials and 80 direct

manufacturing labor-hours.

Required

1. Allocate the overhead costs to each activity cost pool. Calculate the activity rate for each

pool.

2. Determine the cost of Order 277100.

3. How does activity-based costing enhance Marshall’s ability to price its orders? Suppose

Marshall used a simple costing system to allocate all overhead costs to orders on the basis of

direct manufacturing labor-hours. How might this have affected Marshall’s pricing decision

for Order 227100?

4. When designing its activity-based costing system, Marshall uses time-driven activity-based

costing system (TDABC) for its design department. What does this approach allow Marshall

to do? How would the cost of Order 277100 have been different if Marshall had used the

number of customer designs rather than the number of custom design-hours to allocate costs

to different customer orders? Which cost driver do you prefer for design support? Why?

SOLUTION

(30 min.) First stage allocation, time-driven activity-based costing, manufacturing sector.

1.

Direct Manuf. Order Design Other Total

5-10

Labor Support Processing Support

Wages and salaries $192,000 $120,000 $144,000 $ 24,000 $480,000

Depreciation 15,000 6,000 9,000 30,000 60,000

Rent 36,000 30,000 12,000 42,000 120,000

Cost Allocation Base Allocation Rate

2. Cost of Order 277100:

3. Activity-based costing allows Marshall to only assign resources used by orders to the

orders. Activity-based costing leads to more accurate costing of orders. This, in turn, leads to

more competitive pricing. If Marshall allocated all overhead costs to orders on the basis of

direct manufacturing labor hours, they would tend to overprice larger, simple orders and

underprice smaller, complex orders. Consider, for example order-processing costs, which is a

Marshall would likely lose bids on the overpriced orders and win the underpriced orders,

4. If Marshall had used the number of custom designs rather than the number of custom

design-hours to allocate costs to different customer orders, it would have calculated the design

support allocation rate as follows:

5-11

Allocating costs on the basis of the number of custom designs ignores the fact that complex

designs take nearly twice as long as simple designs (11.75 hours versus 6 hours) and so will

place greater demands on design support resources. Order 277100 has several complex designs

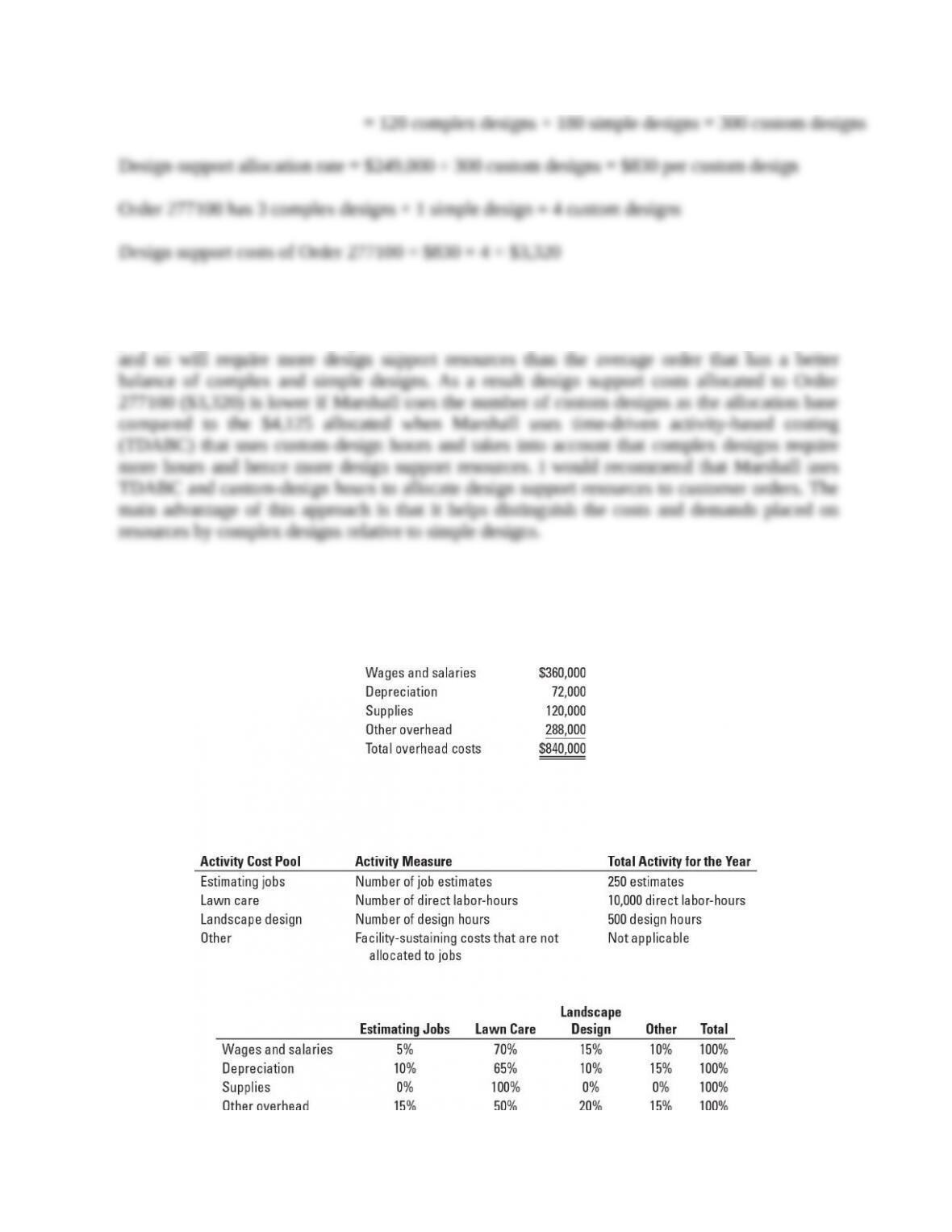

5-35 First-stage allocation, time-driven activity-based costing, service sector. LawnCare

USA provides lawn care and landscaping services to commercial clients. LawnCare USA uses

activity-based costing to bid on jobs and to evaluate their profitability. LawnCare USA reports

the following budgeted annual costs:

John Gilroy, controller of LawnCare USA, has established four activity cost pools and the

following budgeted activity for each cost pool:

Gilroy estimates that LawnCare USA’s costs are distributed to the activity-cost pools as follows:

5-12

Sunset Office Park, a new development in a nearby community, has contacted LawnCare USA to

provide an estimate on landscape design and annual lawn maintenance. The job is estimated to

require a single landscape design requiring 40 design hours in total and 250 direct labor-hours

annually. LawnCare USA has a policy of pricing estimates at 150% of cost.

Required

1. Allocate LawnCare USA’s costs to the activity-cost pools and determine the activity rate for

each pool.

2. Estimate total cost for the Sunset Office Park job. How much would LawnCare USA bid to

perform the job?

3. LawnCare USA does 30 landscape designs for its customers each year. Estimate the total cost

for the Sunset Office park job if LawnCare USA allocated costs of the Landscape Design

activity based on the number of landscape designs rather than the number of landscape

design-hours. How much would LawnCare USA bid to perform the job? Which cost driver

do you prefer for the Landscape Design activity? Why?

4. Sunset Office Park asks LawnCare USA to give an estimate for providing its services for a

2-year period. What are the advantages and disadvantages for LawnCare USA to provide a

2-year estimate?

5-13