SOLUTION

(25 min.) Nonfinancial measures of quality and time.

1.

2016 2017

125 = 5%

400 = 4%

Required:

1. Compute the manufacturing cycle efficiency for an order for 2016 and 2017.

2. For each year 2016 and 2017, calculate the following:

a. Percentage of goods returned

b. Defective units reworked as a percentage of units shipped

c. Percentage of on-time deliveries

d. Percentage of hours spent by each employee on quality training

3. Evaluate management’s performance on quality and timeliness in 2016 and 2017.

SOLUTION

(15 min.) Nonfinancial measures of quality, manufacturing cycle efficiency.

1. Manufacturing cycle time = Total time from receipt of an order by production until its

completion.

Some students may argue that a part of inspection time is also value-added time. Turnkey

reduced inspection time to 3 days in 2017, so if we think of 2 days of inspection as value-added

time in 2016 (out of 5 days) and in 2017:

Turnkey has become more efficient in its value-added manufacturing time as a percentage of

total manufacturing time during the last year.

Some students might ask if inspection has been excessively reduced or simply become

more efficient. The key is to improve processes and only then reduce inspection so that the

percentage of goods returned does not increase.

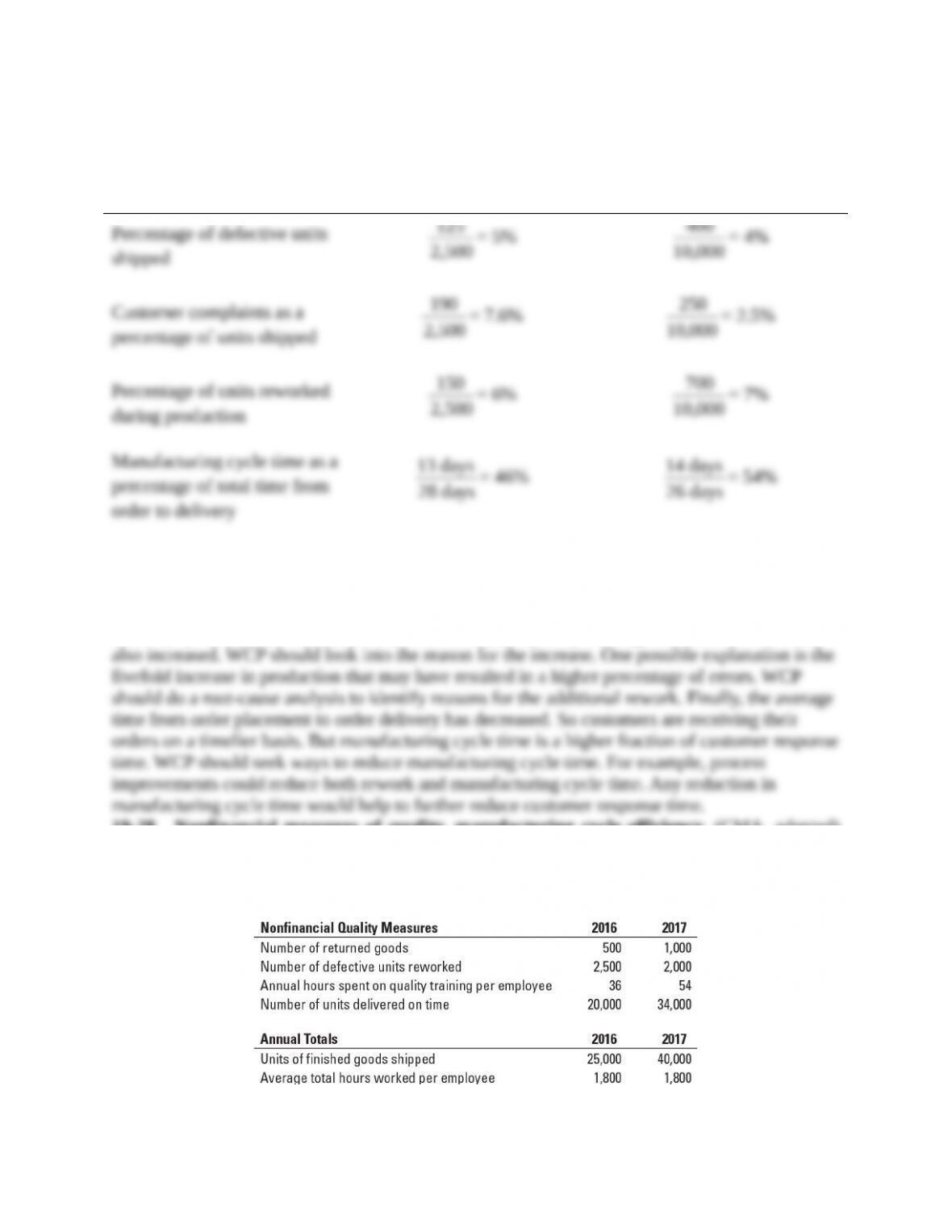

2.

Non-Financial Quality Measure 2016 2017

Percentage of goods returned (as a percentage of units shipped)

(500 25,000; 1,000 40,000) 2.00% 2.50%

Defective units reworked as a percentage of units shipped 10.00% 5.00%

3. Turnkey has become more efficient in its value-added manufacturing time as a percentage

of manufacturing cycle time and has improved the company’s lead time. This improved

efficiency should result in cost savings for the company as well as greater customer satisfaction.

It is important to evaluate the other nonfinancial quality measures in relation to annual

totals (total units shipped, etc.) rather than as absolute values. For example, the total number of

Management also had two noteworthy areas of improvement related to the nonfinancial

quality measures above. The first is the reduction in the total number of defective units reworked.

This is a significant improvement compared to the prior year. However, it should be noted that a

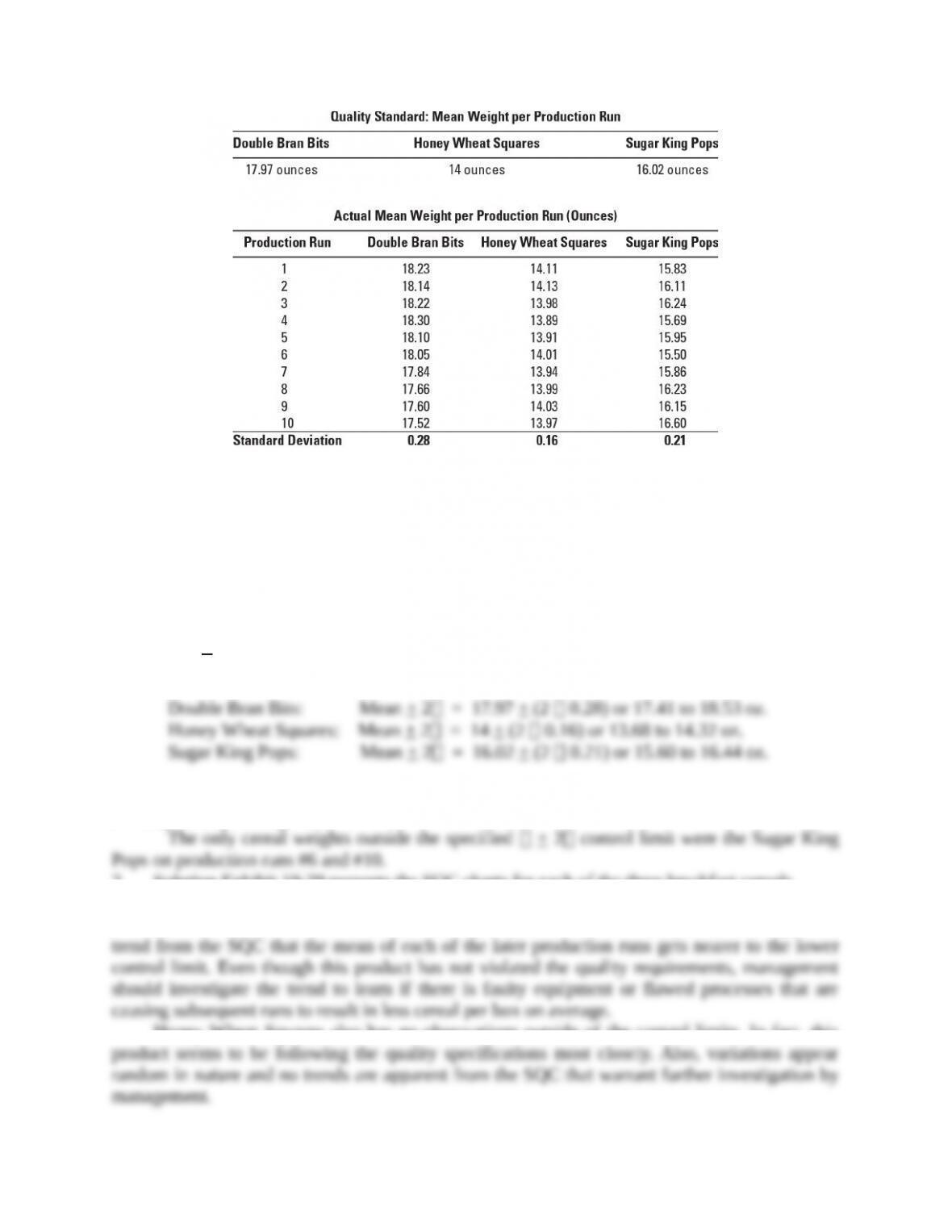

19-29 Statistical quality control. Harvest Cereals produces a wide variety of breakfast products.

The company’s three best-selling breakfast cereals are Double Bran Bits, Honey Wheat Squares,

and Sugar King Pops. Each box of a particular type of cereal is required to meet predetermined

weight specifications, so that no single box contains more or less cereal than another. The

company measures the mean weight per production run to determine if there are variances over

or under the company’s specified upper- and lower-level control limits. A production run that

falls outside of the specified control limit does not meet quality standards and is investigated

further by management to determine the cause of the variance. The three Harvest breakfast

cereals had the following weight standards and production run data for the month of March:

Required:

1. Using the ±2 rule, what variance investigation decisions would be made?

2. Present control charts for each of the three breakfast cereals for March. What inferences can

you draw from the charts?

3. What are the costs of quality in this example? How could Harvest employ Six Sigma

programs to improve quality?

SOLUTIONStatistical quality control.

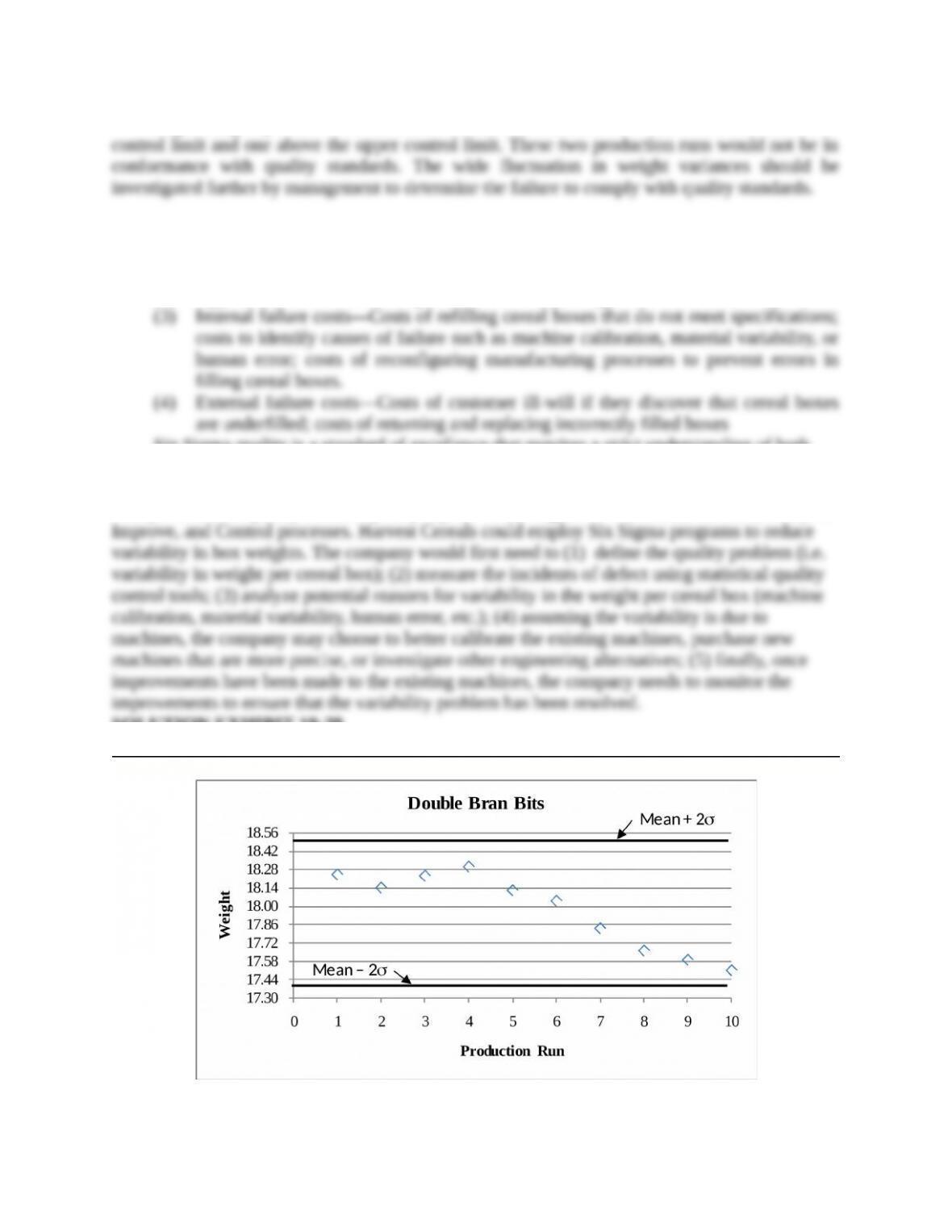

1. The + 2 rule will trigger a decision to investigate when mean weight per production run

is outside the control limit:

Any weight less than the lower control limit or greater than the upper control limit will trigger an

investigation by management.

2. Solution Exhibit 19-29 presents the SQC charts for each of the three breakfast cereals.

Double Bran Bits had no observations outside the control limits. Each of the production

runs is considered to be in conformance with quality standards. However, there is an apparent

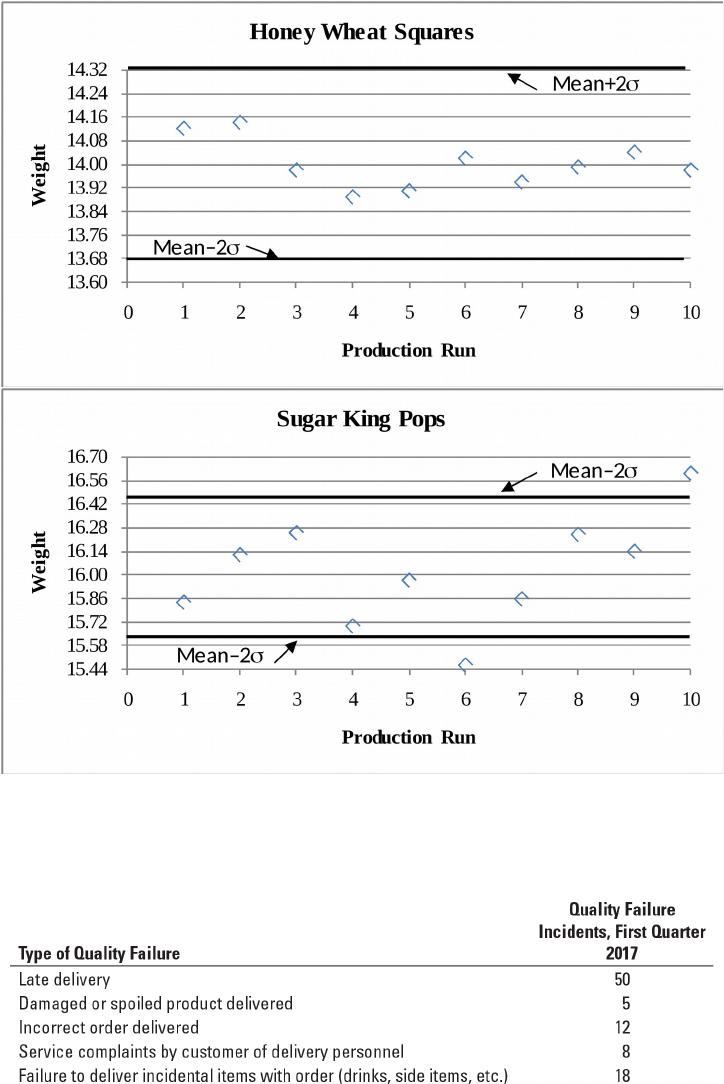

Honey Wheat Squares also has no observations outside of the control limits. In fact, this

Sugar King Pops has two observations outside the control limits. One falls below the lower

3. The costs of quality include

(1) Prevention costs—Costs of designing the process, maintaining equipment, and

employee training to operate the production line.

(2) Appraisal costs—Costs of inspection to check the weight of cereal boxes.

Six Sigma quality is a standard of excellence that requires a strict understanding of both

customer expectations and reasons for manufacturing defects to improve current quality

performance. The statistical term Six Sigma translates to 3.4 defects per 1 million incidents, or

near perfection in quality variability. Key aspects of Six Sigma are to Define, Measure, Analyze,

SOLUTION EXHIBIT 19-29

Plots of Mean Weight per Production Run for Keltrex Cereals

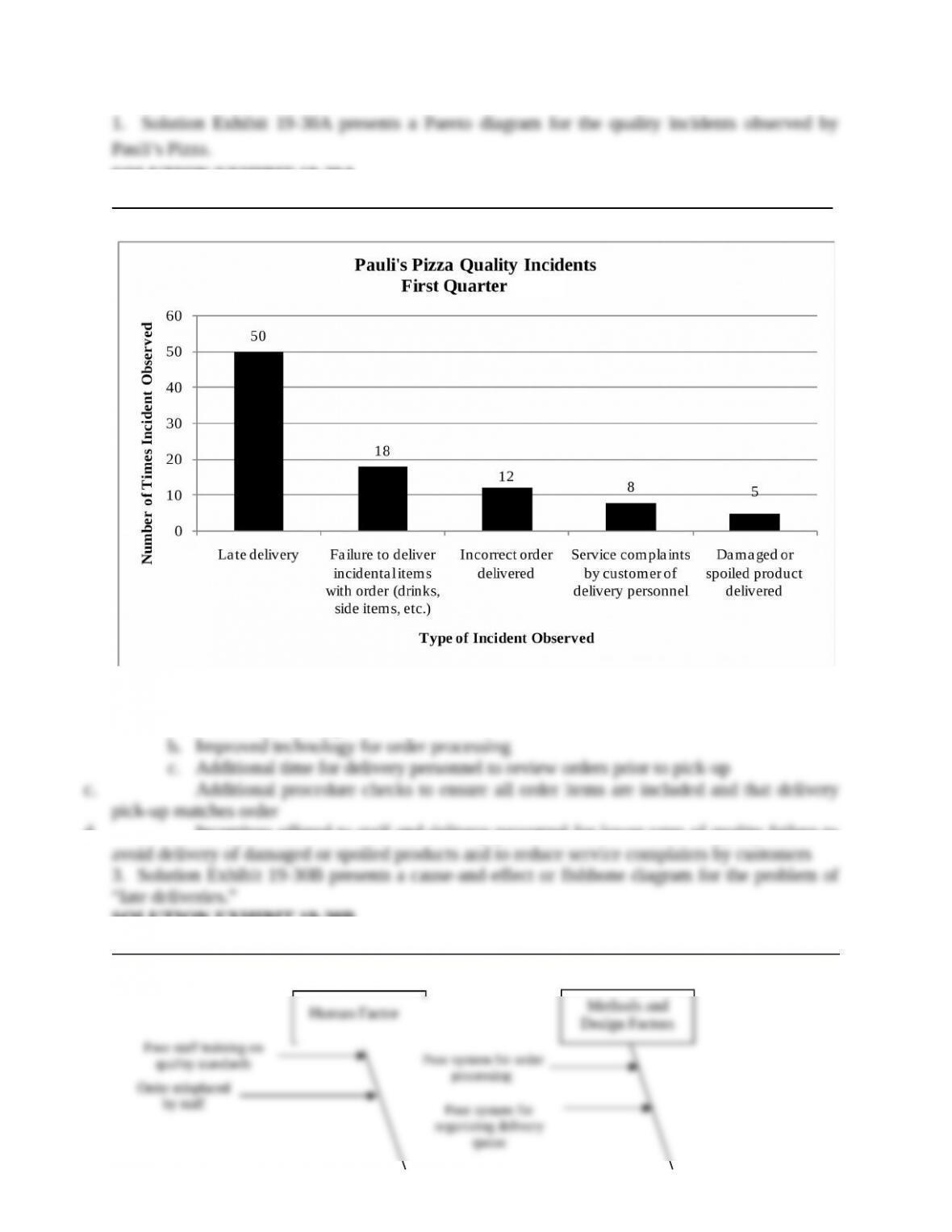

19-30 Quality improvement, Pareto diagram, cause-and-effect diagram. Pauli’s Pizza has

recently begun collecting data on the quality of its customer order processing and delivery.

Pauli’s made 1,800 deliveries during the first quarter of 2017. The following quality data pertain

to first-quarter deliveries:

Required:

1. Draw a Pareto diagram of the quality failures experienced by Pauli’s Pizza.

2. Give examples of prevention activities that could reduce the failures experienced by Pauli’s.

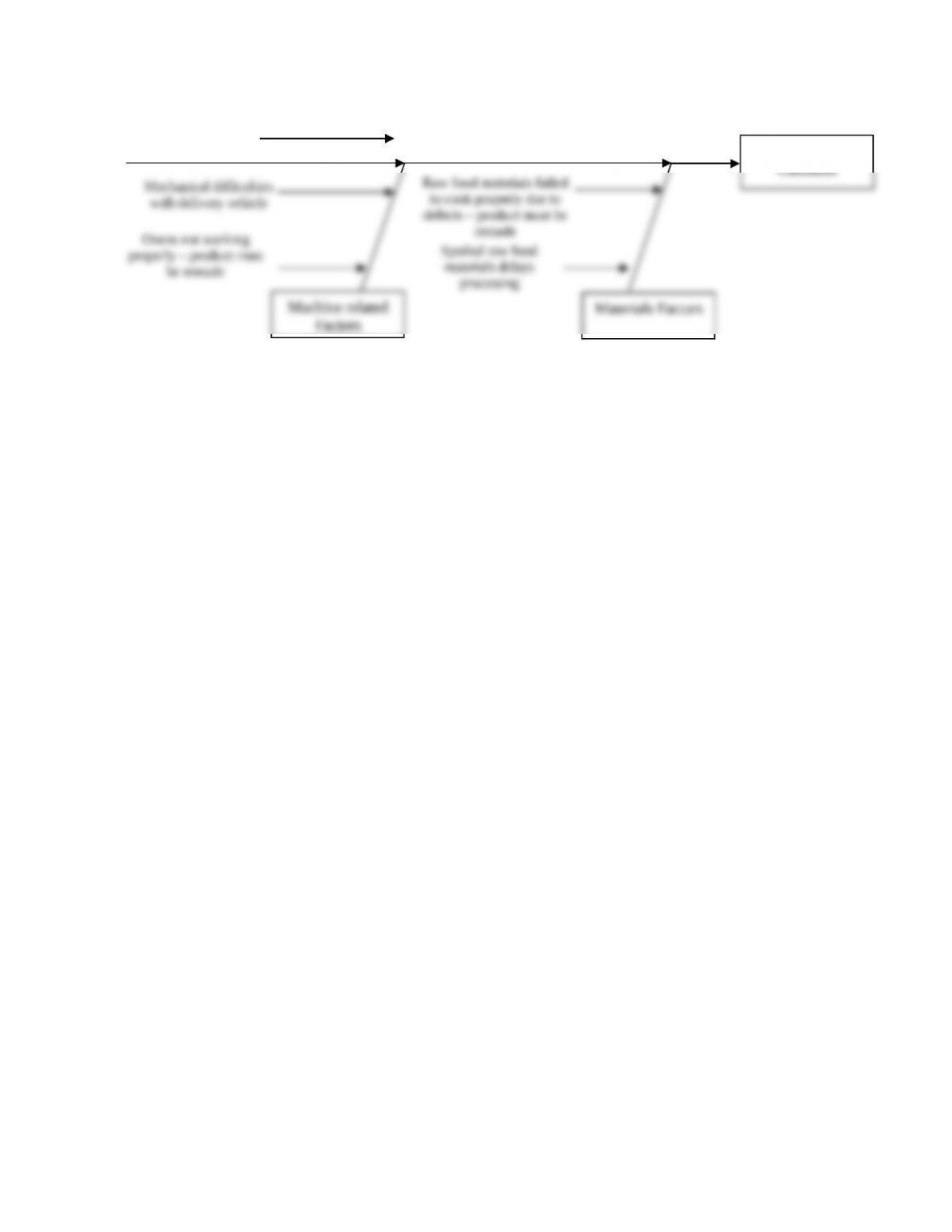

3. Draw a cause-and-effect diagram of possible causes for late deliveries.

SOLUTION

(25 min.) Quality improvement, Pareto diagram, cause-and-effect diagram.

SOLUTION EXHIBIT 19-30A

Quality improvement, Pareto diagram, cause-and-effect diagram

2. Prevention activities that could reduce failures in Pauli’s Pizza deliveries could include

the following:

a. Better staff training

d. Incentives offered to staff and delivery personnel for lower rates of quality failure to

SOLUTION EXHIBIT 19-30B

Cause-and-Effect Diagram for incidents of “late delivery” to customer at Pauli’s Pizza

2017

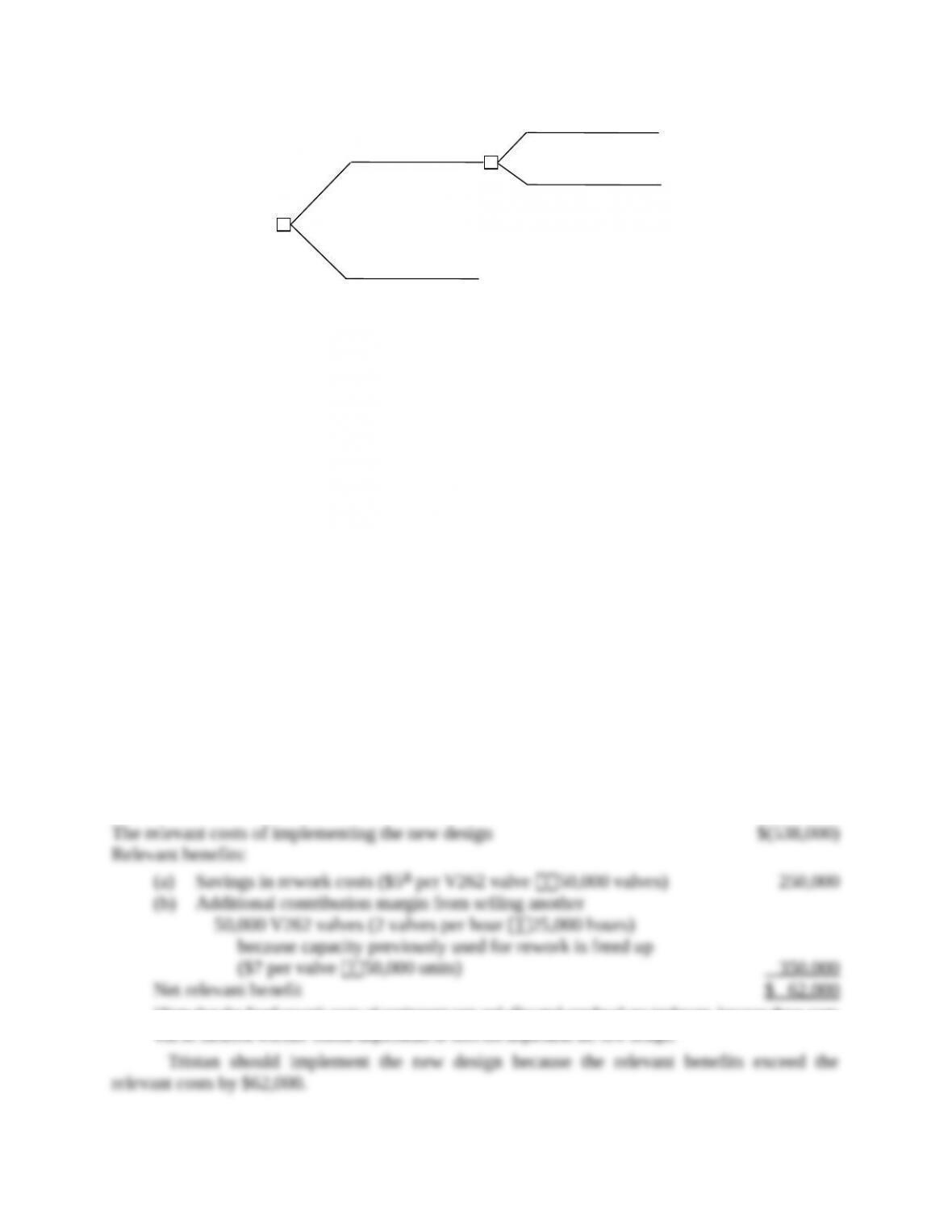

19-31 Quality improvement, relevant costs, and relevant revenues. The Tristan Corporation

sells 250,000 V262 valves to the automobile and truck industry. Tristan has a capacity of 150,000

machine-hours and can produce two valves per machine-hour. V262’s contribution margin per

unit is $7. Tristan sells only 250,000 valves because 50,000 valves (20% of the good valves)

need to be reworked. It takes 1 machine-hour to rework two valves, so 25,000 hours of capacity

are used in the rework process. Tristan’s rework costs are $550,000. Rework costs consist of the

following:

Direct materials and direct rework labor (variable costs): $5 per unit

Fixed costs of equipment, rent, and overhead allocation: $6 per unit

Tristan’s process designers have developed a modification that would maintain the speed of the

process and ensure 100% quality and no rework. The new process would cost $538,000 per year.

The following additional information is available:

The demand for Tristan’s V262 valves is 400,000 per year.

The Colton Corporation has asked Tristan to supply 27,000 T971 valves (another product) if

Tristan implements the new design. The contribution margin per T971 valve is $12. Tristan

can make one T971 valve per machine-hour with 100% quality and no rework.

Required:

1. Suppose Tristan’s designers implement the new design. Should Tristan accept Colton’s order

for 27,000 T971 valves? Show your calculations.

2. Should Tristan implement the new design? Show your calculations.

3. What nonfinancial and qualitative factors should Tristan consider in deciding whether to

implement the new design?

SOLUTION

(30 min.) Quality improvement, relevant costs, and relevant revenues.

One way to present the alternatives is via a decision tree, as shown below.

Machine related

Factors

Materials Factors

Mechanical difficulties

with delivery vehicle

Ovens not working

properly – product must

be remade

Raw food materials failed

to cook properly due to

defects – product must be

remade

Spoiled raw food

materials delays

processing

Delivery driver falls

behind schedule

Late Delivery to

Customer

Implement

new design

Do not implement

new design

Make T971

Do not make T971

The idea is to first evaluate the best action that Tristan should take if it implements the

new design (that is, make or not make T971). Tristan can then compare the best mix of products

to produce if it implements the new design against the status quo of not implementing the new

design.

1. Tristan has capacity constraints. Demand for V262 valves (400,000 valves) exceeds

production capacity of 300,000 valves (2 valves per hour 150,000 machine-hours). Because

capacity is constrained, Tristan will choose to sell the product that maximizes contribution

margin per machine-hour (the constrained resource).

Contribution margin per

=

machine-hour for V262

$7 per valve 2 valves per hour = $14

Contribution margin per

=

machine-hour for T971

$12 per valve 1 valve per hour = $12.

Tristan should reject Colton Corporation’s offer and continue to manufacture only V262

valves.

2. Now compare the alternatives of (a) not implementing the new design versus

(b) implementing the new design. By implementing the new design, Tristan will save 25,000

machine-hours of rework time. This time can then be used to make and sell 50,000 (2 valves per

hour 25,000 hours) additional V262 valves. The relevant costs and benefits of implementing

the new design follow:

a Note that the fixed rework costs of equipment rent and allocated overhead are irrelevant, because these costs

will be incurred whether Tristan implements or does not implement the new design.

3. Tristan Corporation should also consider other benefits of improving quality. For

example, the process of quality improvement will help Tristan’s managers and workers gain

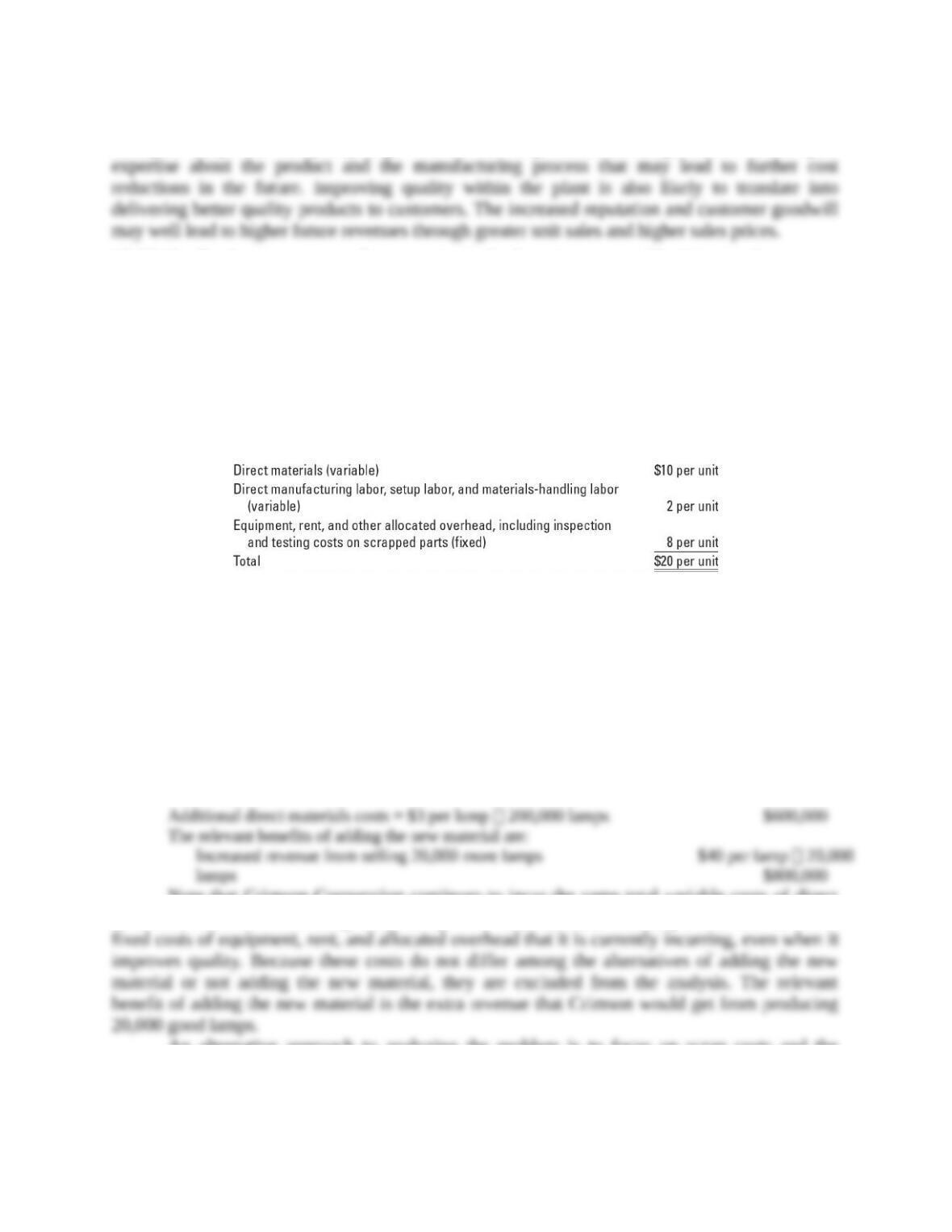

19-32 Quality improvement, relevant costs, and relevant revenues. The Crimson Corporation

uses multicolored molding to make plastic lamps. The molding operation has a capacity of

200,000 units per year. The demand for lamps is very strong. Crimson will be able to sell

whatever output quantities it can produce at $40 per lamp.

Crimson can start only 200,000 units into production in the molding department because of

capacity constraints on the molding machines. If a defective unit is produced at the molding

operation, it must be scrapped at a net disposal value of zero. Of the 200,000 units started at the

molding operation, 20,000 defective units (10%) are produced. The cost of a defective unit,

based on total (fixed and variable) manufacturing costs incurred up to the molding operation,

equals $20 per unit, as follows:

Crimson’s designers have determined that adding a different type of material to the existing

direct materials would result in no defective units being produced, but it would increase the

variable costs by $3 per lamp in the molding department.

Required:

1. Should Crimson use the new material? Show your calculations.

2. What nonfinancial and qualitative factors should Crimson consider in making the decision?

SOLUTION

(30 min.) Quality improvement, relevant costs, and relevant revenues.

1. By implementing the new method, Crimson would incur additional direct materials costs

on all the 200,000 units started at the molding operation.

Note that Crimson Corporation continues to incur the same total variable costs of direct

materials, direct manufacturing labor, setup labor and materials handling labor, and the same

An alternative approach to analyzing the problem is to focus on scrap costs and the

benefits of reducing scrap.

The relevant benefits of adding the new material are:

a Note that only the variable costs of defective lamps: $12 per lamp (direct materials, $10 per lamp; direct manufacturing

labor, setup labor, and materials handling labor, $2 per lamp) are relevant because improving quality will save these costs.

Fixed costs of producing a defective lamp of equipment, rent, and other allocated overhead are irrelevant because

thesecosts will be incurred whether Crimson Corporation adds or does not add the new material.

On the basis of quantitative considerations alone, Crimson should use the new material.

Relevant benefits of $800,000 exceed the relevant costs of $600,000 by $200,000.

2. Other nonfinancial and qualitative factors that Crimson should consider in making a

decision include the effects of quality improvement on

a. gaining manufacturing expertise that could lead to further cost reductions in the

future;

19-33 Waiting times, manufacturing cycle times. The Sandstone Corporation uses an injection

molding machine to make a plastic product, Z35, after receiving firm orders from its customers.

Sandstone estimates that it will receive 60 orders for Z35 during the coming year. Each order of

Z35 will take 100 hours of machine time. The annual machine capacity is 8,000 hours.

Required:

1. Calculate (a) the average amount of time that an order for Z35 will wait in line before it is

processed and (b) the average manufacturing cycle time per order for Z35.

2. Sandstone is considering introducing a new product, Y21. The company expects it will