SOLUTION

(20 min.) Support-department cost allocations: direct, step-down, and reciprocal methods.

1 a. Allocate the total Support Department costs to the operating departments under the

Direct Allocation Method:

Eastern

Department

Western

Department

Departmental Overhead Costs $650,000 $ 920,000

From:

Information Technology

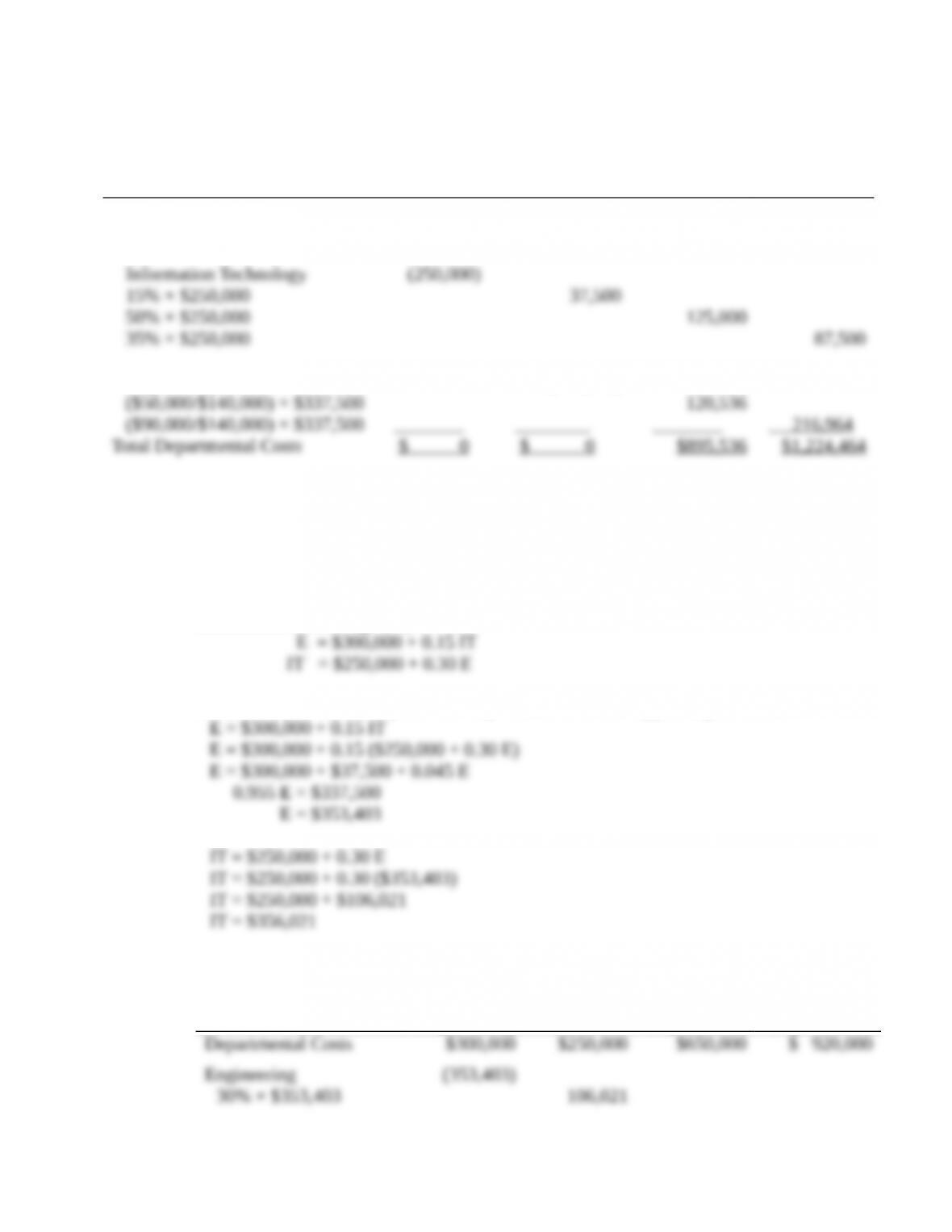

b. Allocate the Support Department Costs to the Operating Departments under the

Step-down (Sequential) Allocation Method with Engineering first sequentially:

To:

Engineering IT

Eastern

Department

Western

Department

Departmental Overhead Costs $ 300,000 $250,000 $650,000 $ 920,000

From:

Information Technology (340,000)

c. Allocate the Support Department Costs to the Operating Departments under the

Step-down (Sequential) Allocation Method IT first sequentially:

To:

IT Engineering

Eastern

Department

Western

Department

Departmental Costs $250,000 $300,000 $650,000 $ 920,000

From:

Engineering (337,500)

Total Costs to account for: $2,120,000

d. Allocate the Support Department Costs to the Operating Departments under the

Reciprocal Allocation Method:

Assign reciprocal equations to the support departments: Engineering (E) and

Information Technology (IT)

Solve the equation to complete the reciprocal costs of the support departments

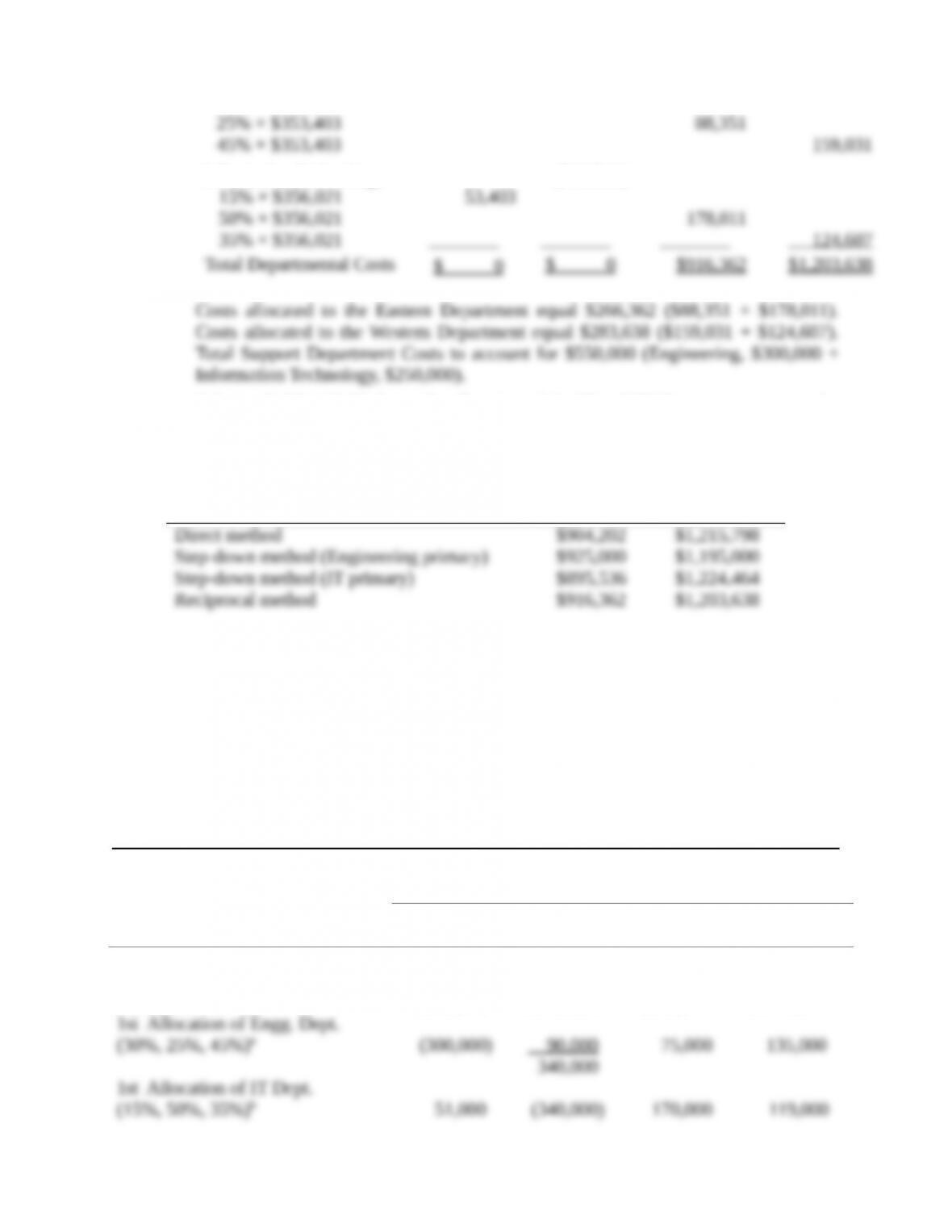

Allocate Reciprocal costs to departments (all numbers rounded to nearest dollar)

Engineering IT

Eastern

Department

Western

Department

Information Technology (356,021)

Solution Exhibit 15-36 shows the allocation of the IT and HR Department costs to the

Eastern Department and to the Western Department using repeated iterations.

2. Summary of cost allocation resulting from the four methods in part 1:

Eastern

Department

Western

Department

Although the reciprocal method produces the most accurate support department cost allocation, it

is also the most complicated. The step-down method with Engineering being the primary

department produces similar results. That is due to the fact that 30% of Engineering services are

provided to the IT department, another support department, while only 15% of IT services are

provided to Engineering. Therefore, the step-down method with Engineering as the primary

department would be an acceptable substitute for the reciprocal method.

SOLUTION EXHIBIT 15-36

Reciprocal Method of Allocating Support Department Costs for Ballantine Tours Using

Repeated Iterations.

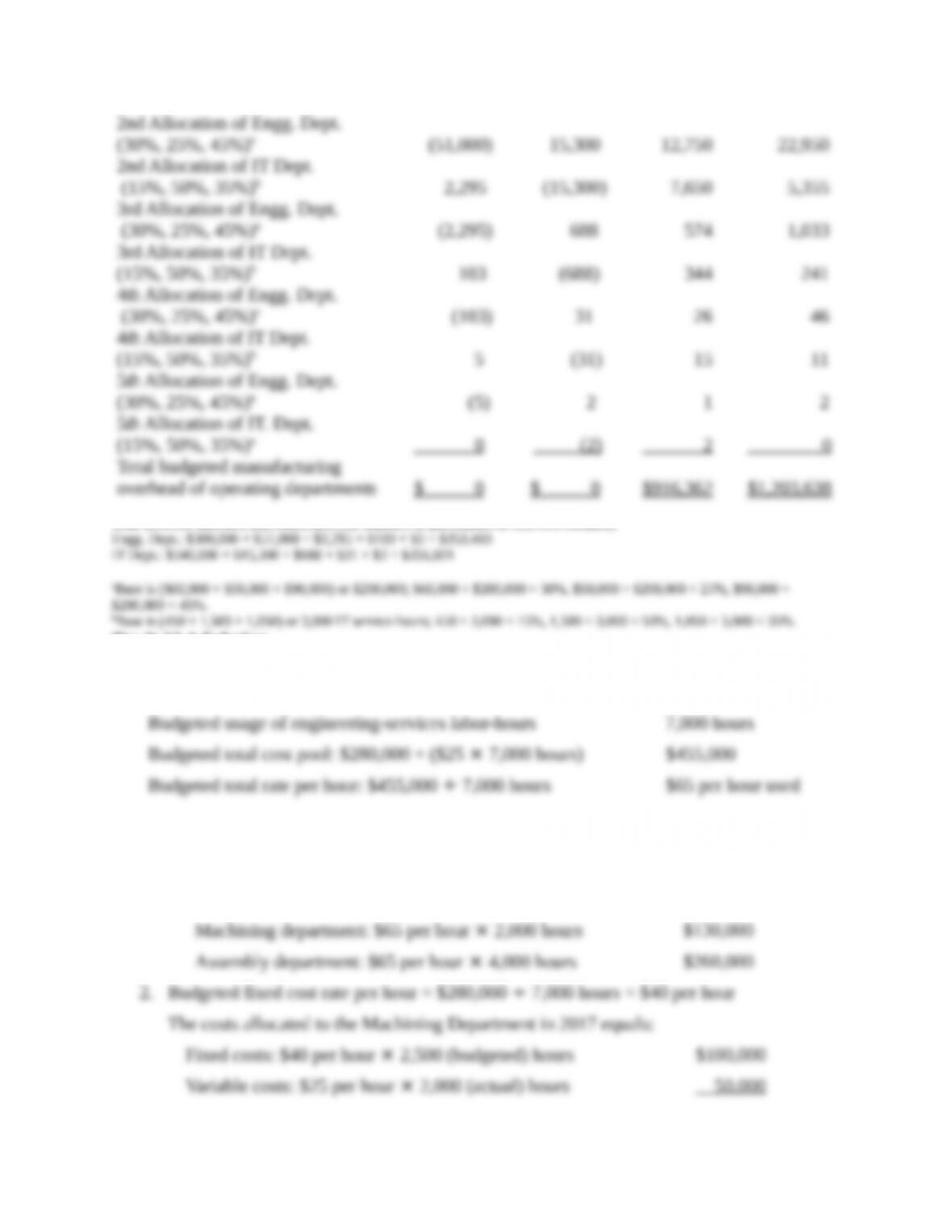

Support Departments Operating Departments

Engineeri

ng IT Eastern Western

Budgeted manufacturing overhead

costs before any interdepartmental

cost allocations $300,000 $250,000 $650,000 $ 920,000

Total accounts allocated and reallocated (the numbers in parentheses in first two columns)

Try It 15-1 Solution

1. A combined budgeted rate is used for fixed and variable costs. The rate is calculated as

follows:

The rate of $65 per hour is used to allocate engineering-services department costs to the

machining and assembly departments.

Under the single-rate method, the Machining and Assembly Departments are charged the

budgeted rate for each hour of actual use of engineering services.

The costs allocated to the Assembly Department in 2017 equals:

3. Using the 8,000 hours of practical capacity of the Engineering Services Department, the

budgeted rate is:

Budgeted fixed-cost rate per hour, $280,000 ÷ 8,000 hours

Under the single rate method, the Engineering Services Department costs are allocated to the

Machining and Assembly Departments as follows:

Machining Department: $60 per hour × 2,000 (actual) hours

Fixed costs of unused engineering-services capacity:

$35 per hour × 2,000 hoursa

4. Under the dual rate method, the Engineering Services Department costs are allocated to

the Machining and Assembly Departments as follows:

Machining Department

Fixed costs: $35 per hour × 2,500 (budgeted) hours

Assembly Department

Fixed costs: $35 per hour × 4,500 (budgeted) hours

Fixed costs of unused engineering-services capacity:

b1,000 hours

=

Practical capacity of 8,000 hours − (2,500 hours budgeted to be used by Machining Department

+

4,500 hours budgeted to be used by Assembly Department).

Try It 15-2 Solution

1a. Allocate the total Support Department costs to the operating departments under the Direct

Allocation Method:

Domestic Tours World Tours

Total Costs to account for: $3,790,000

b. Allocate the Support Department Costs to the Operating Departments under the

Step-down (Sequential) Allocation Method with Administration first sequentially:

To:

Administration IT

Domestic

Tours

World

Tours

Total Costs to account for: $3,790,000

c. Allocate the Support Department Costs to the Operating Departments under the

Step-down (Sequential) Allocation Method IT first sequentially:

To:

IT Administration

Domestic

Tours

World

Tours

Total Costs to account for: $3,790,000

d. Allocate the Support Department Costs to the Operating Departments under the

Reciprocal Allocation Method:

Assign reciprocal equations to the support departments

Solve the equation to complete the reciprocal costs of the support departments

Allocate Reciprocal costs to departments (all numbers rounded to nearest dollar)

Administration IT

Domestic

Tours

World

Tours

Costs allocated to the Domestic Tours Department equal $356,250 ($116,357 +

$239,893). Costs allocated to the World Tours Department equal $293,750 ($162,899

+ $130,851). Total Support Department Costs to account for $650,000

(Administration, $400,000 + Information Technology, $250,000).

Try It Exhibit 15-2 shows the allocation of the IT and HR Department costs to the

Domestic Tours Department and to the World Tours Department using repeated

iterations.

TRY IT EXHIBIT 15-2

Reciprocal Method of Allocating Support Department Costs for Montvale Tours Using

Repeated Iterations.

Support Departments Operating Departments

Administratn. IT Domestic World

Budgeted manufacturing overhead

costs before any interdepartmental

Total accounts allocated and reallocated (the numbers in parentheses in first two columns)

Try It 15-3 Solution

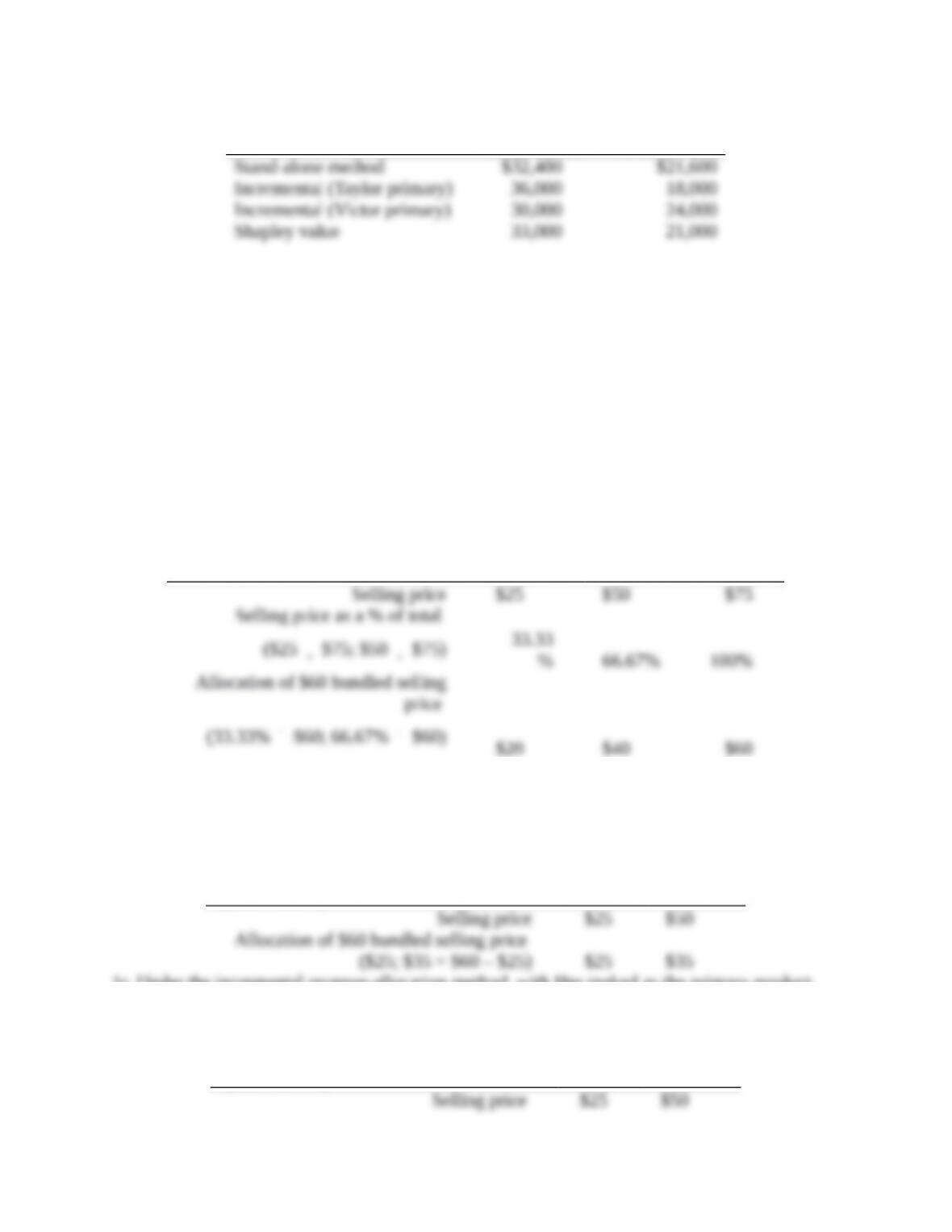

1. Stand-alone cost-allocation method.

Taylor Inc. =

Victor Inc. =

$54,000

2. With Taylor Inc. as the primary party:

Party Costs Allocated

Cumulative Costs

Allocated

With Victor Inc. as the primary party:

Party Costs Allocated

Cumulative Costs

Allocated

3. To use the Shapley value method, consider each party as first the primary party and then

the incremental party. Compute the average of the two to determine the allocation.

Taylor Inc.:

Using this approach, Taylor Inc. is allocated $33,000, and Victor, Inc. is allocated $21,000 of the

total costs of $54,000.

4. The results of the four cost-allocation methods are shown below.

Taylor Inc. Victor Inc.

The allocations are very sensitive to the method used. With the incremental cost-allocation

method, Taylor Inc. and Victor Inc. would probably have disputes over who is the primary party

because the primary party gets allocated all of the primary party’s costs. The stand-alone method

is simple and fair because it allocates the common cost of the dyeing machine in proportion to

the individual costs of leasing the machine. The Shapley values are also fair. They result in

allocations that are similar to those of the stand-alone method. Either of the methods can be

chosen. Given its simplicity, the stand-alone method is likely more acceptable.

Try It 15-4 Solution

1a. Under the stand-alone revenue-allocation method based on selling price, Him will be

allocated 33.33% of all revenues, or $20 of the bundled selling price, and Her will be

allocated 66.67% of all revenues, or $40 of the bundled selling price, as shown below.

Stand-alone method, based on

selling prices Him Her Total

1b. Under the incremental revenue-allocation method, with Him ranked as the primary

product, Him will be allocated $25 (its own stand-alone selling price), and Her will be

allocated $35 of the $60 selling price, as shown below.

Incremental Method

(Him rank 1)

Hi

m Her

1c. Under the incremental revenue-allocation method, with Her ranked as the primary product,

Her will be allocated $50 (its own stand-alone selling price) and Him will be allocated $10 of

the $60 selling price, as shown below.

Incremental Method

(Her rank 1) Him Her

1d.Under the Shapley value method, each product will be allocated the average of its

allocations in 1b and 1c, i.e., the average of its allocations when it is the primary product and

when it is the secondary product, as shown below.

Shapley Value Method Him Her

2. A summary of the allocations based on the four methods in requirement 1 is shown below.

Stand-alone

(Selling Prices)

Incrementa

l (Him

first)

Incremental

(Her first)

Shaple

y

If there is no clear indication of which product is the more “important” product, or if it can

be reasonably assumed that the two products are equally important to the company’s strategy,

the Shapley value method is the fairest of all the methods because it averages the effect of