Use of practical capacity results in an unrealistically small fixed manufacturing cost per

unit because it is based on an idealistic and unattainable level of capacity.

To evaluate overall performance, return on investment and residual income measures

are more appropriate than return on sales.

Manufacturing companies hold only one type of inventory: direct material.

When there are multiple cost drivers the simple CVP formula of Q = (FC + OI)/CMU

can still be used.

The variable overhead efficiency variance is the difference between actual quantity of

the

cost-allocation base used and budgeted quantity of the cost-allocation base allowed for

actual output, multiplied by the budgeted variable overhead cost per unit of the

cost-allocation base.

A budget can only be used as a planning tool.

To comply with GAAP, backflush cost numbers can be adjusted by recording a journal

entry.

The constant gross-margin percentage method differs from market-based joint-cost

allocation method (sales value at split-off and estimated net realizable value) since no

account is taken of profits earned before or after the split-off point when allocating joint

costs.

Overtime premium is normally considered as a component of direct labor.

In some variations of normal costing, organizations use budgeted rates to assign direct

costs as well as indirect costs to jobs.

There are two elements that influence customer profitability – revenues and costs.

Discretionary costs arise from periodic (usually annual) decisions and have a

measurable cause-and-effect relationship between output and resources used.

Performing professional duties in accordance with relevant laws, regulations, and

technical standards is a competent responsibility.

An operation is a standardized method or technique performed repetitively, often on

different materials, resulting in different finished goods.

Engineering and human resource factors are both important when estimating theoretical

or practical capacity.

Staff management, such as management accountants and information technology and

human-resources management, provides advice, support, and assistance to line

management.

A manager’s job entails gathering information, interpreting that information and making

judgments on that information and thus is less susceptible to moral hazards than jobs

that require repetitive tasks and less subjective decision making.

A successful implementation of a JIT production system should result in a lowering of

the inventory turnover ratio.

In an EVA calculation, the measure of the invested capital for a division would be that

division’s assets minus that division’s long-term liabilities.

Goodness of fit has meaning only if the relationship between the cost drivers and costs

is economically plausible.

If the company’s fixed overhead spending variance was unfavorable it could be

attributed to higher plant-leasing costs.

The supply chain describes the flow of goods, services, and information from the initial

sources of materials and services to the delivery of products to consumers.

Companies that utilize backflush costing typically prorate underallocated or

overallocated conversion costs between work-in-process, finished goods, and cost of

goods sold.

When goods are sold, the Cost of Goods Sold account is debited while the Finished

Goods Control account is credited.

A cost may be relevant for one decision, but NOT relevant for a different decision.

An individual cost item can be simultaneously a direct cost of one cost object and an

indirect cost of another cost object.

Companies that implement JIT purchasing will emphasize developing short-term

supplier relationships with many suppliers to attain flexibility.

re-engineering benefits are most significant when they focus on one business function

rather than crossing functional lines of the business process.

The Required Rate of Return (RRR) is set externally by creditors as the interest rate on

long term liabilities.

A contractual agreement that specifies a fee per mile driven, such as with a rental of a

truck, is not considered a cause-and-effect relationship between an activity and a cost.

Lean accounting takes in to consideration all costs associated with inventories.

The sales value at split-off method of joint cost allocation involves computation of the

relative amounts of the sales value of the amount of each joint product sold during the

period.

Job-costing and process-costing are mutually exclusive, hence a hybrid costing system

that combines elements of both job and process costing cannot be used.

Life-cycle budgeting and life-cycle costing can help highlight which of the following

measures?

A) an increase in customer-service costs due to using inferior materials

B) high production costs caused by a complex design

C) large ordering costs due to the great number of component parts used

D) an increase in annual operating income resulting from the new product

Which of the following is a reason for companies to use absorption costing for internal

accounting?

A) It is the required inventory method for internal accounting as per GAAP.

B) It measures the cost of all resources, whether manufacturing or nonmanufacturing,

necessary to produce inventory.

C) It does not take into account fixed manufacturing overhead while valuing inventory

and hence is more suited for decision making.

D) It can help prevent managers from taking actions that make their performance

measure look good but that hurt the income they report to shareholders.

Inventory carrying costs equal the ________.

A) opportunity costs of the investment tied up in inventory and the cost of

manufacturing of goods

B) costs of storage only

C) opportunity costs of the investment tied up in inventory and the relevant costs of

storage

D) historical costs and the relevant costs of storage

Megatron Corp. earned net income of 16,000 Euros in its overseas branch at France. Its

headquarters is located in the U.S. The rate of conversion during set up was $1.309 /

Euro. What is the value of its income in its home currency if the rate is $1.508 / Euro at

the end of a financial year and the average rate being $1.410 / Euro?

A) $12,223

B) $22,560

C) $24,128

D) $20,944

Delinz Company sells 115 hams per week. Purchase-order lead time is 6 weeks and the

economic-order quantity is 210 hams. What is the reorder point?

A) 1950 hams

B) 690 hams

C) 1260 hams

D) 210 hams

Crandle Corp. applies manufacturing overhead costs to products at a budgeted

indirect-cost rate of $60 per direct manufacturing labor-hour. A retail outlet has

requested a bid on a special order of a necklace. Estimates for this order include: Direct

materials of $40,000; 400 direct manufacturing labor-hours at $15 per hour; and a 50%

markup rate on total manufacturing costs.

Estimated total product costs for this special order equal ________.

A) $105,000

B) $64,000

C) $46,000

D) $70,000

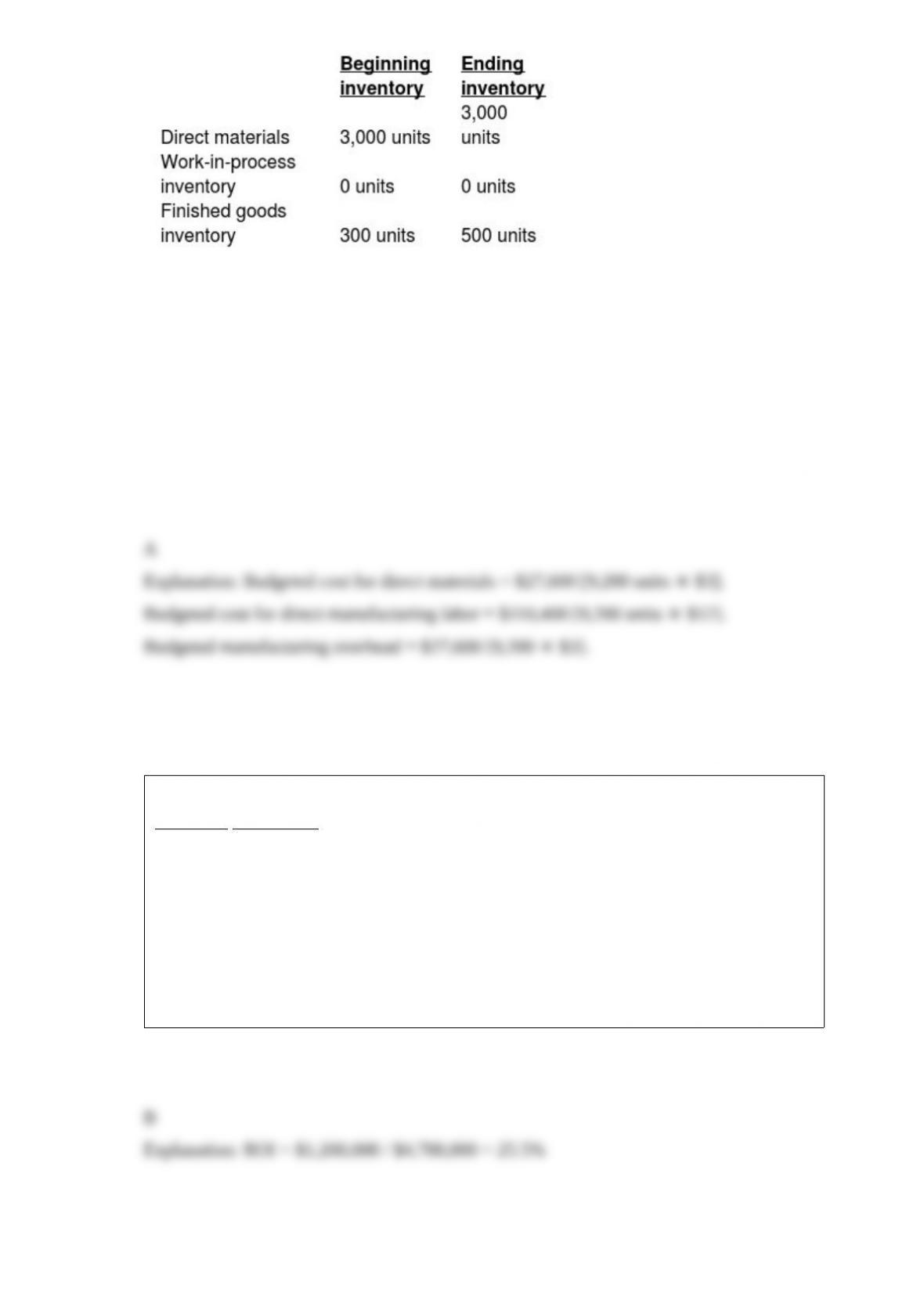

Bradford, Inc., expects to sell 9,000 ceramic vases for $21 each. Direct materials costs

are $3, direct manufacturing labor is $12, and manufacturing overhead is $3 per vase.

The following inventory levels apply to 2019:

What are the 2019 budgeted production costs for direct materials, direct manufacturing

labor, and manufacturing overhead, respectively?

A) $27,600; $110,400; $27,600

B) $27,000; $108,000; $27,000

C) $9,000; $36,000; $9,000

D) $9,000; $0; $10,500

Bouvous Corp has two regional offices. The data for each are as follows:

Maryland New Jersey

Revenues $293,000 $298,000

Operating assets 2,900,000 4,700,000

Net operating income 1,200,000 1,200,000

What is the return on investment for the New Jersey Division?

A) 6.3%

B) 25.5%

C) 41.4%

D) 19.2%

A learning curve is a function ________.

A) that measures the decline in labor-hours per unit due to workers becoming better at a

job

B) that increases at a greater rate as workers become more familiar with their tasks

C) where unit costs increase as productivity increases

D) that is linear

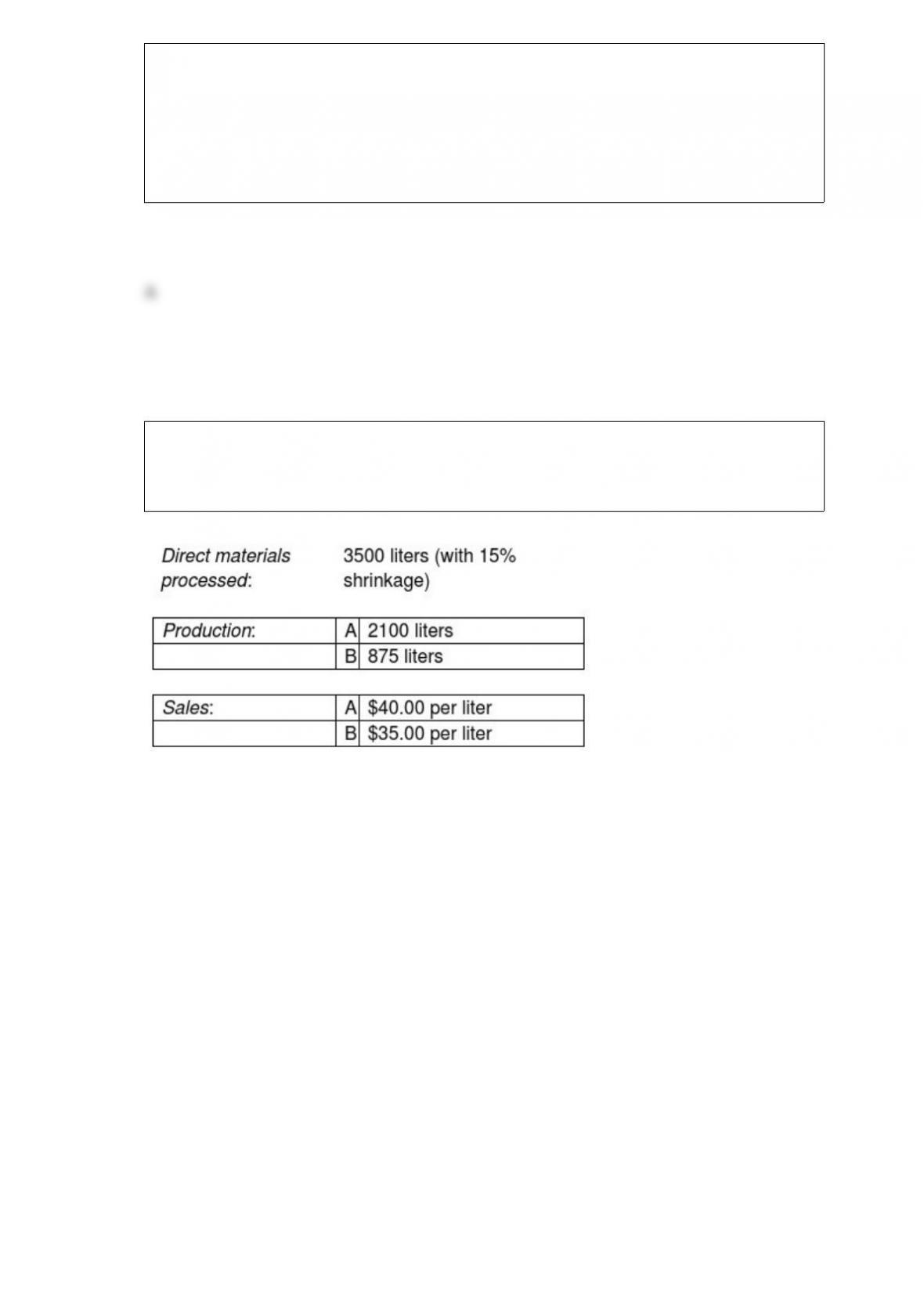

Cola Drink Company processes direct materials up to the split-off point where two

products, A and B, are obtained. The following information was collected for the month

of July:

The cost of purchasing 3500 liters of direct materials and processing it up to the split-off

point to yield a total of 2975 liters of good products was $7000. There were no inventory

balances of A and B.

Product A may be processed further to yield 2000 liters of Product Z5 for an additional

processing cost of $160. Product Z5 is sold for $60.00 per liter. There was no beginning

inventory and ending inventory was 125 liters.

Product B may be processed further to yield 800 liters of Product W3 for an additional

processing cost of $290. Product W3 is sold for $65 per liter. There was no beginning

inventory and ending inventory was 25 liters.

What is Product Z5’s estimated net realizable value at the split-off point?

A) $51,840

B) $83,840

C) $119,840

D) $120,000

Which of the following statements is true of the methods for allocating joint costs?

A) Under the cause-and-effect criterion, the physical-measure method is highly

desirable.

B) Byproducts are never excluded from the denominator used in the physical-measure

method.

C) The NRV method is never used when the selling prices of joint products vary

frequently.

D) The sales value at split-off method follows the benefits-received criterion of cost

allocation.

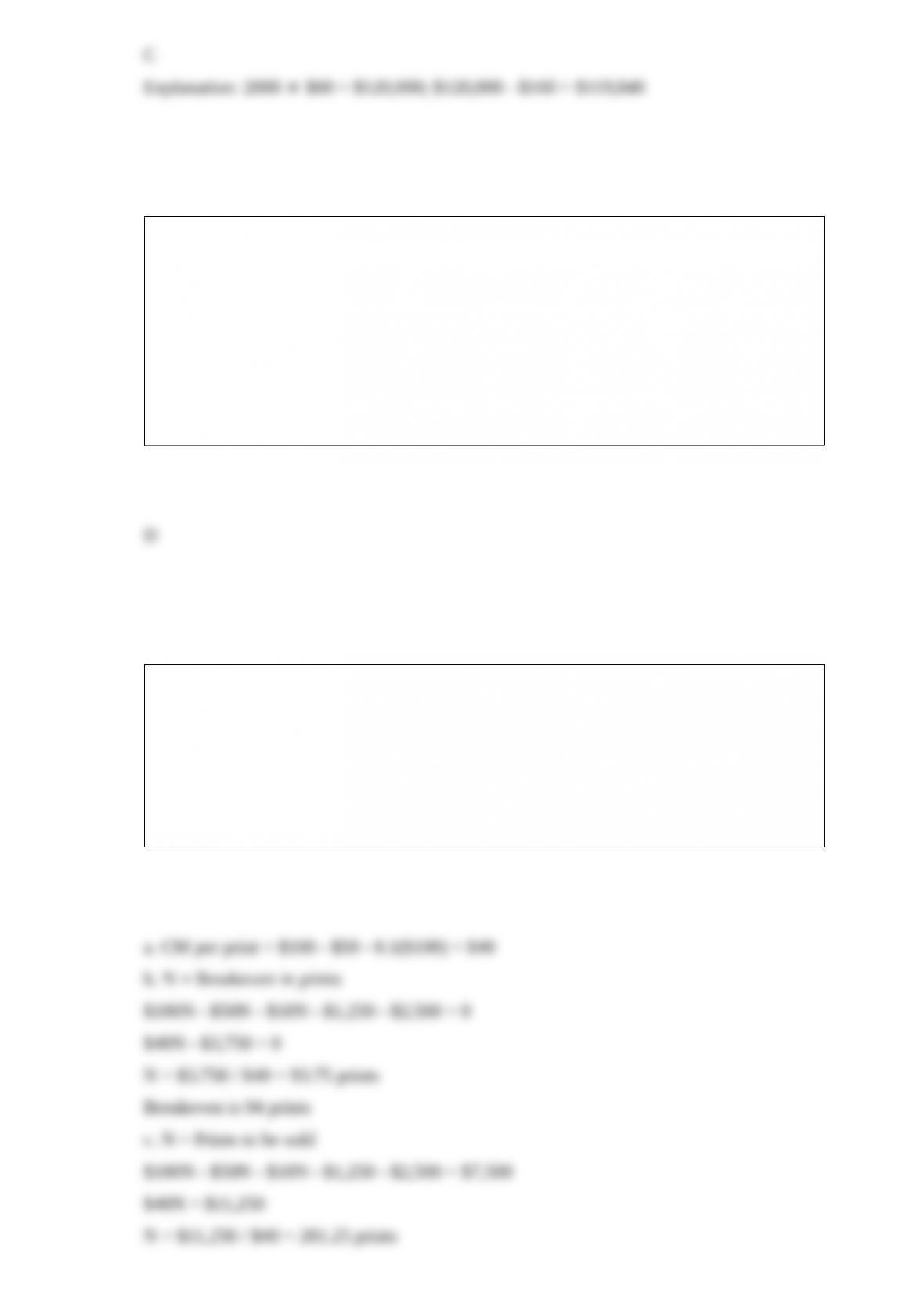

MyArt sells framed art prints for $100. The unit variable cost per phone is $50 plus a

selling commission of 10%. Fixed manufacturing costs total $1,250 per month, while

fixed selling and administrative costs total $2,500.

Required:

a. What is the contribution margin per print?

b. What is the breakeven point in prints?

c. How many prints must be sold to earn pretax income of $7,500?

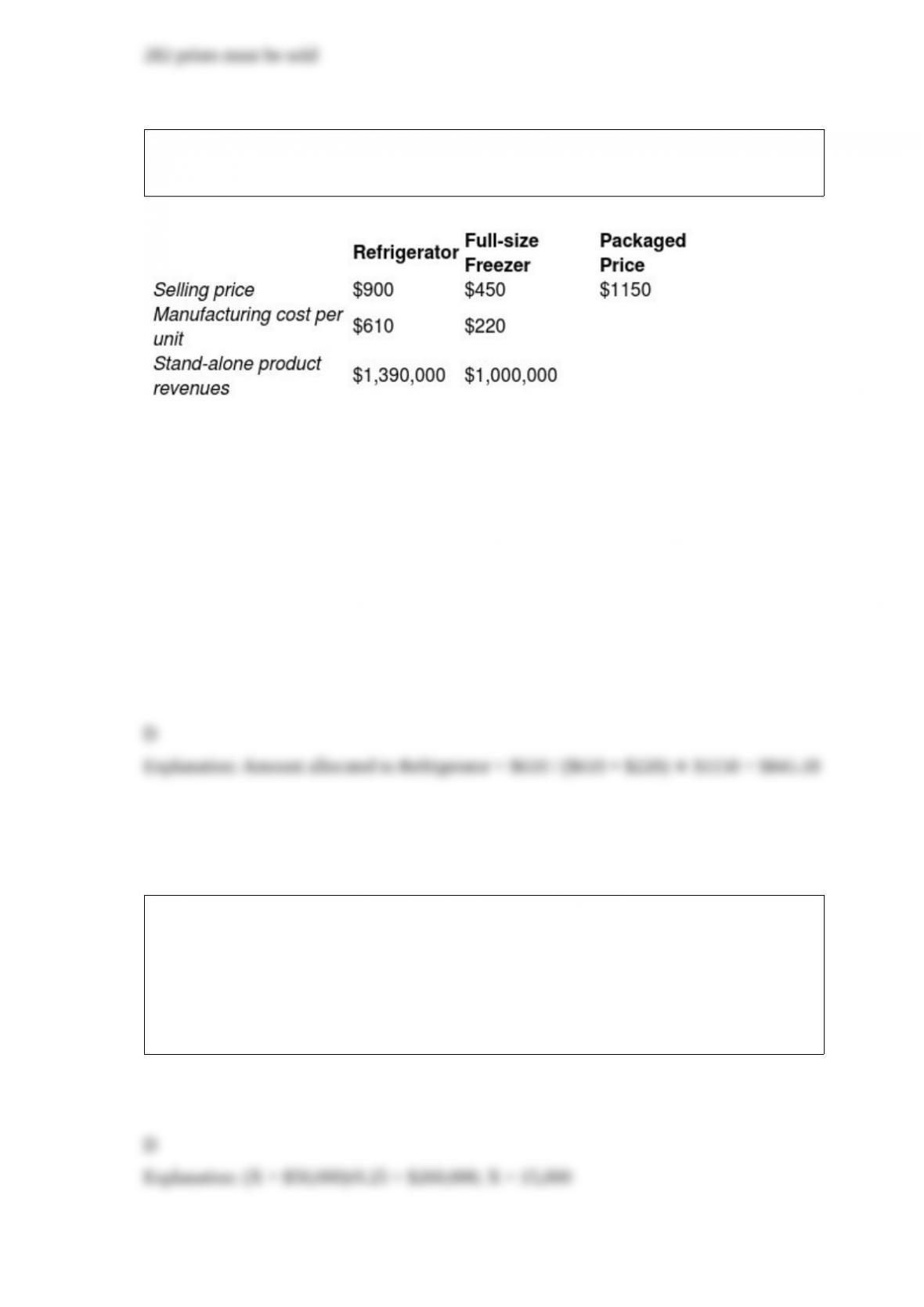

Electro Corp sells a refrigerator and a freezer as a single package for $1150. Other data

are in the chart below.

Using the stand-alone method with manufacturing cost per unit as the weight for revenue

allocation, what amount will be allocated to the refrigerator? (Do not round any

intermediary calculations.)

A) $304.82

B) $575.00

C) $661.45

D) $845.18

If the contribution margin ratio is 0.25, targeted operating income is $50,000, and

targeted sales volume in dollars is $260,000, then total fixed costs are ________.

A) $35,000

B) $210,000

C) $157,500

D) $15,000

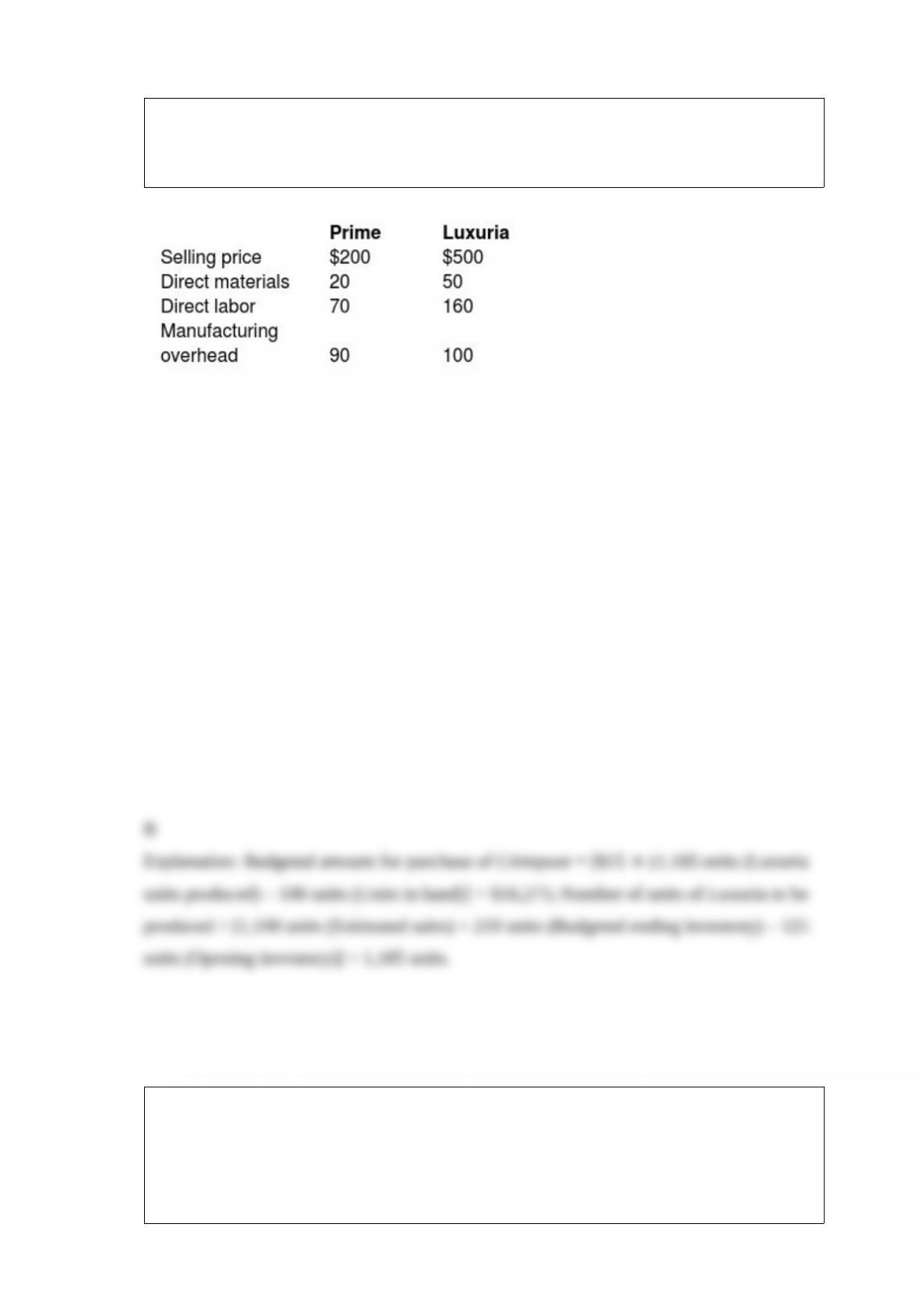

Nantucket Industries manufactures and sells two models of watches, Prime and

Luxuria. It expects to sell 4,000 units of Prime and 1,100 units of Luxuria in 2019.The

following estimates are given for 2019:

Nantucket had an inventory of 230 units of Prime and 125 units of Luxuria at the end of

2018. It has decided that as a measure to counter stock outages it will maintain ending

inventory of 360 units of Prime and 210 units of Luxuria.

Each Luxuria watch requires one unit of Crimpson and has to be imported at a cost of $15.

There were 100 units of Crimpson in stock at the end of 2018.The management does not

want to have any stock of Crimpson at the end of 2019.

What is the amount budgeted for purchase of Crimpson in 2019?

A) $61,950

B) $16,275

C) $17,775

D) $16,500

Linking rewards to performance ________.

A) helps to motivate managers

B) allows companies to charge premium prices

C) should only be based on financial information

D) enhances agency costs

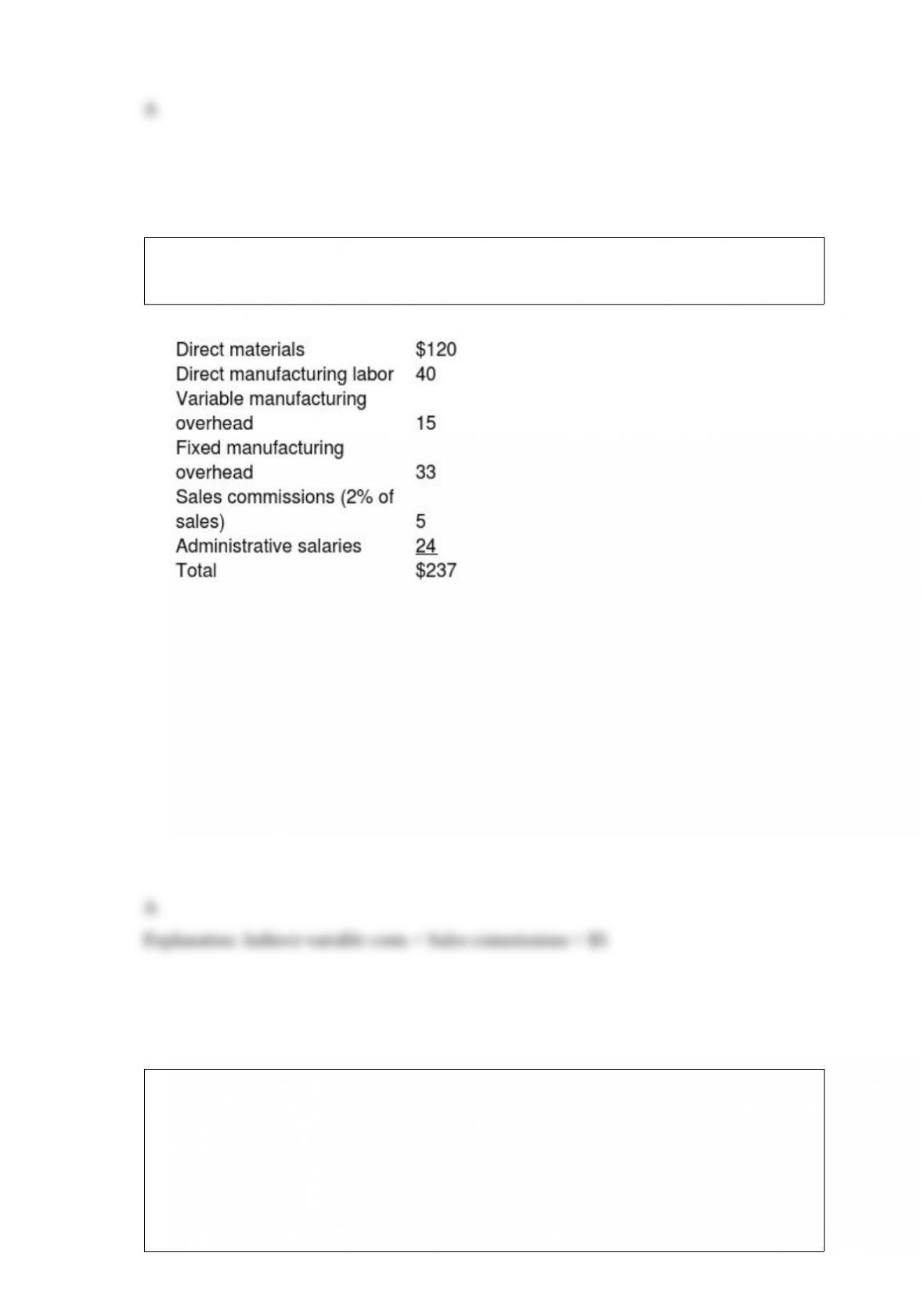

Puritan Apparels is a clothing retailer. Unit costs associated with one of its products,

Product DCF 130, are as follows:

What are the indirect nonmanufacturing variable costs per unit associated with Product

DCF130?

A) $5

B) $29

C) $160

D) $213

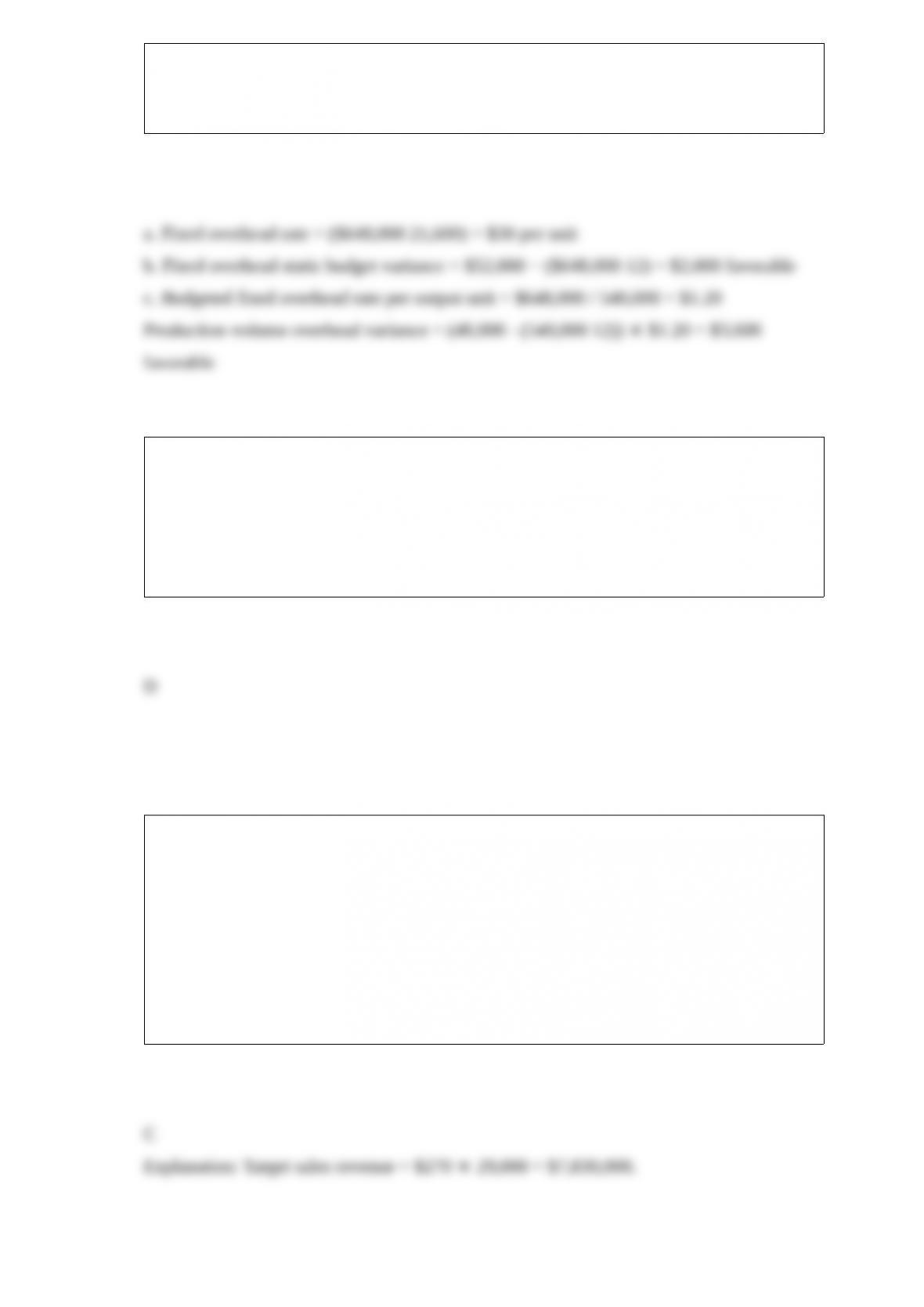

Timely Products Company makes watches. The fixed overhead costs for 2017 total

$648,000. The company uses direct labor-hours for fixed overhead allocation and

anticipates 21,600 hours during the year for 540,000 units. An equal number of units are

budgeted for each month.

During October, 48,000 watches were produced and $52,000 was spent on fixed

overhead.

Required:

a. Determine the fixed overhead rate for 2017 based on the units of input.

b. Determine the fixed overhead static-budget variance for October.

c. Determine the production-volume overhead variance for October.

Which one of the following conditions usually exists when comparing normal and

abnormal spoilage to controllability?

A) Normal is Controllable and Abnormal is Controllable

B) Normal is Controllable and Abnormal is Uncontrollable

C) Normal is Uncontrollable and Abnormal is Uncontrollable

D) Normal is Uncontrollable and Abnormal is Controllable

After conducting a market research study, Magnificent Manufacturing decided to

produce a new interior door to complement its exterior door line. It is estimated that the

new interior door can be sold at a target price of $270. The annual target sales volume

for interior doors is 29,000. Magnificent has target operating income of 40% of sales.

What are target sales revenues?

A) $3,132,000

B) $4,698,000

C) $7,830,000

D) $10,962,000

In a make-or-buy decision, which of the following would not be relevant?

A) the quality of the product

B) the portion of fixed costs that could be eliminated by outsourcing

C) a lease that could be discontinued upon accepting the “buy proposal”

D) property taxes on the plant that will still be necessary even if the product is

outsourced

Which of the following is not true of the 3 level variance analysis of operating income?

A) Level 1 shows the static budget variance for operating income

B) Level 2 shows the direct material price and efficiency variances

C) Level 2 shows the sales-volume variance for operating income

D) Level 3 shows the fixed overhead production volume variance as a component of the

sales-volume variance for operating income

The ________ is required to prepare the cash budget of an organization.

A) statement of shareholders’ equity

B) budgeted balance sheet

C) capital expenditures budget

D) budgeted statement of cash flow

A relevant cost is a cost that is a(n) ________.

A) future cost

B) past cost

C) sunk cost

D) non-cash expense

Financial accounting provides a historical perspective, whereas management accounting

emphasizes ________.

A) the future

B) past transactions

C) a current perspective

D) reports to shareholders

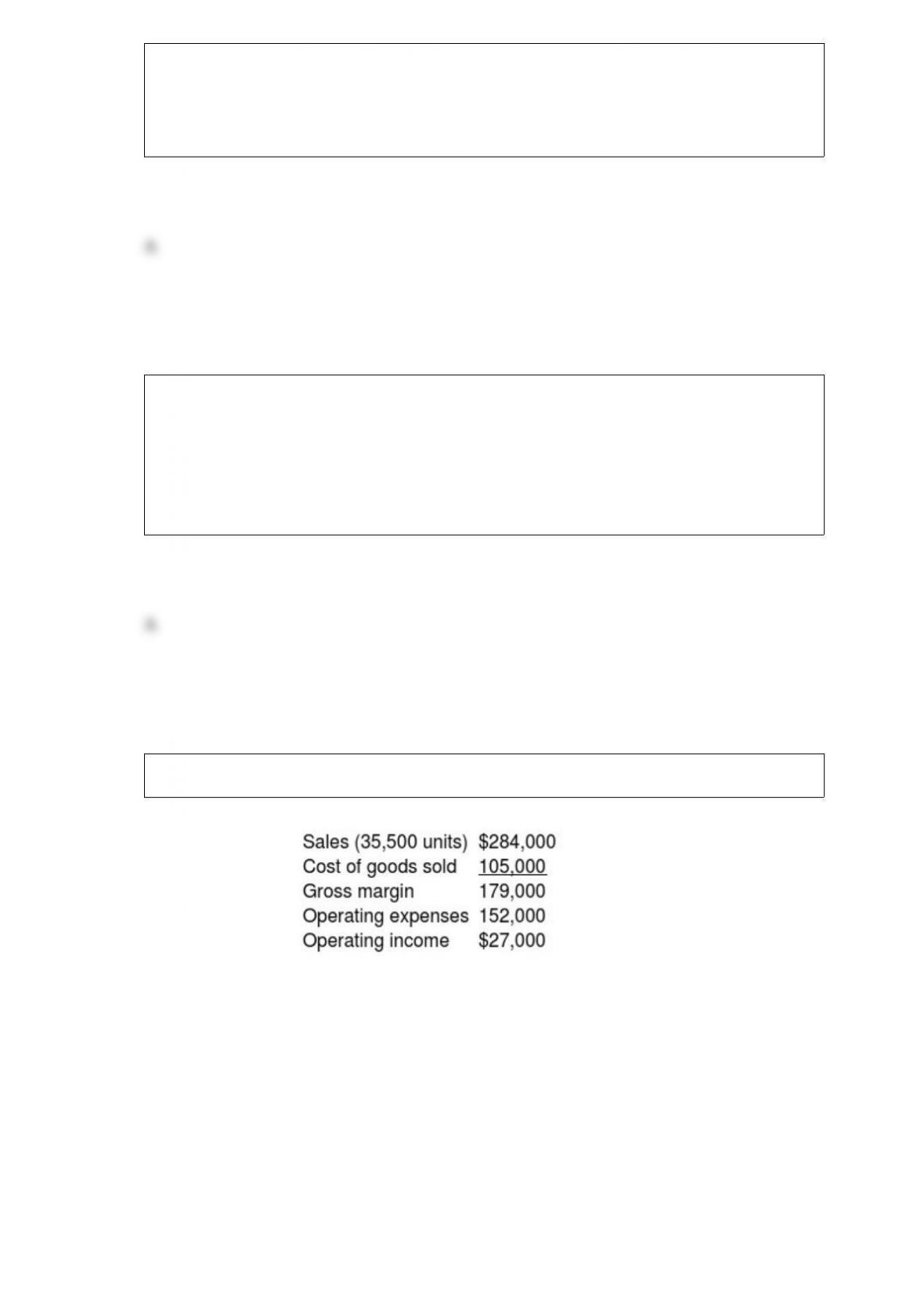

Violet Sales Corp, reports the year-end information from 2019 as follows:

Violet is developing the 2019 budget. In 2019 the company would like to increase selling

prices by 3.5%, and as a result expects a decrease in sales volume of 14%. All other

operating expenses are expected to remain constant. Assume that cost of goods sold is a

variable cost and that operating expenses are a fixed cost.

What is budgeted sales for 2019? (Round interim calculations to the nearest cent and the

final answer to the nearest dollar.)

A) $293,940

B) $252,788

C) $335,092

D) $284,001

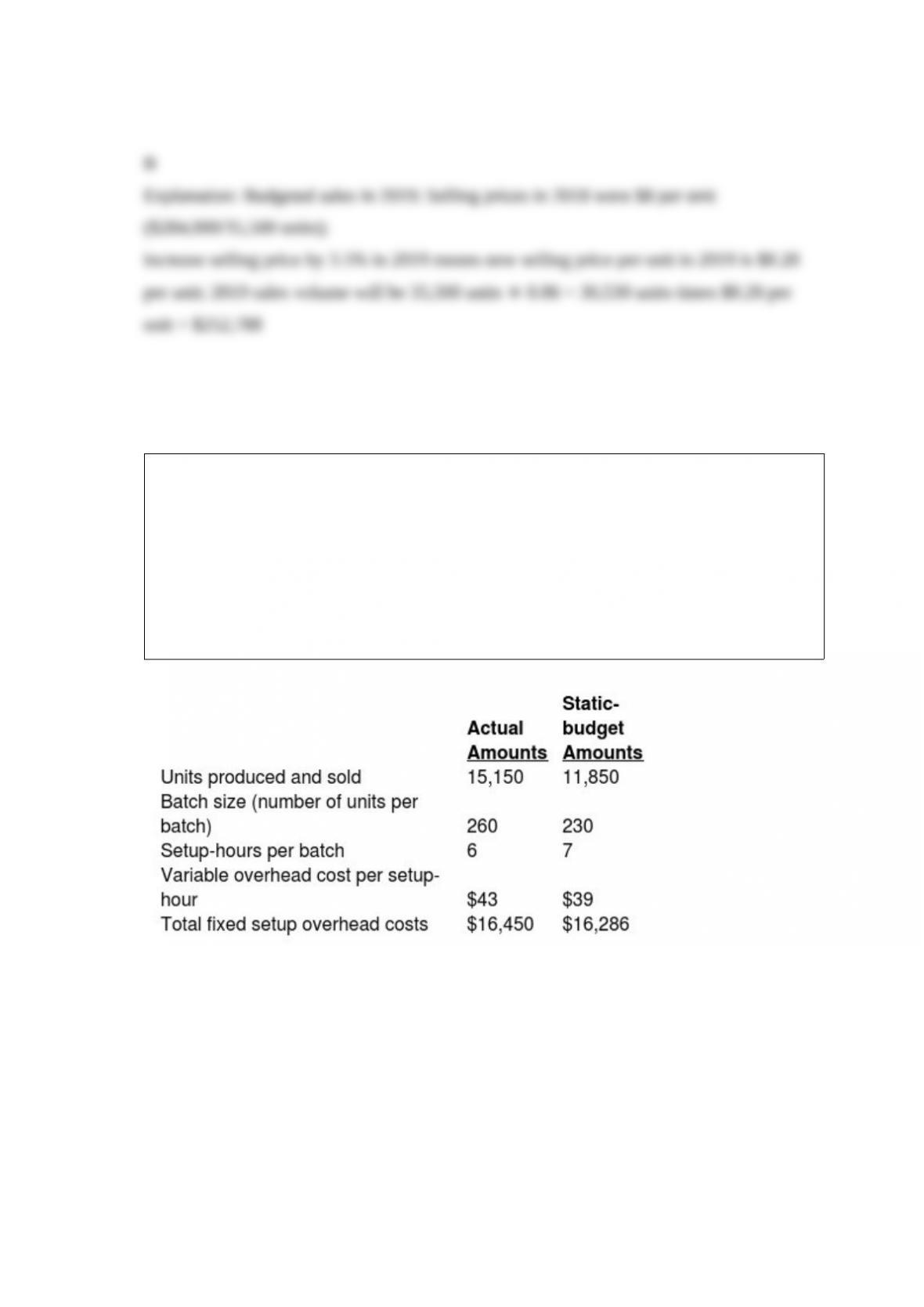

Raposa, Inc., produces a special line of plastic toy racing cars. Raposa, Inc., produces

the cars in batches. To manufacture a batch of the cars, Raposa, Inc., must set up the

machines and molds. Setup costs are batch-level costs because they are associated with

batches rather than individual units of products. A separate Setup Department is

responsible for setting up machines and molds for different styles of car.

Setup overhead costs consist of some costs that are variable and some costs that are

fixed with respect to the number of setup-hours. The following information pertains to

June 2015:

Calculate the production-volume variance for fixed overhead setup costs. (Round all

intermediary calculations to two decimal places and your final answer to the nearest whole

number.)

A) $4,537 unfavorable

B) $99 unfavorable

C) $4,537 favorable

D) $99 favorable

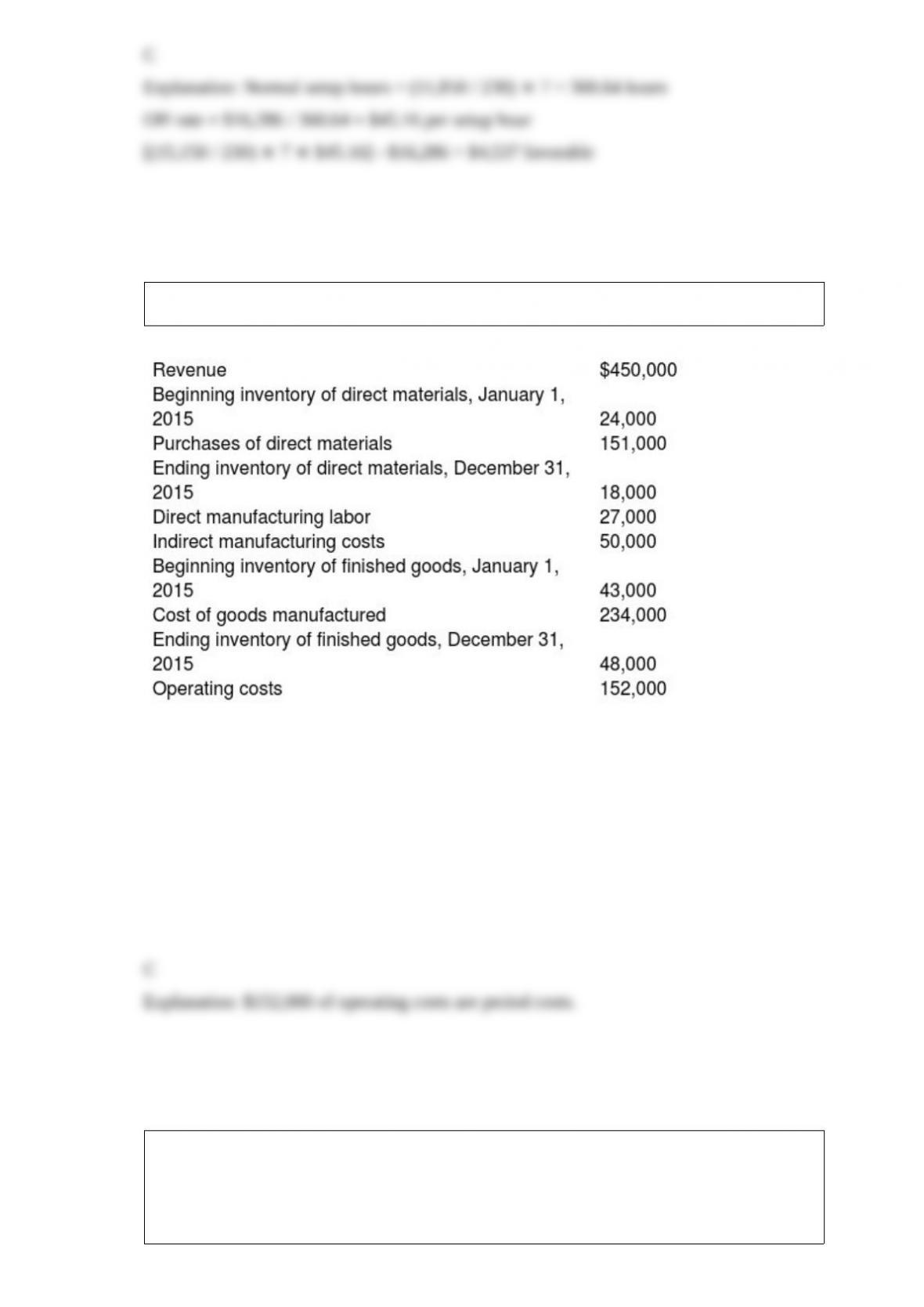

Expert Manufacturing reported the following:

How much of the above would be considered period costs for Expert Manufacturing?

A) $229,000

B) $279,000

C) $152,000

D) $284,000

Venlaz Corp makes small motorcycles. The monthly demand ranges from 80 to 100

motorcycles. The average demand is 92 motorcycles. The plant operates 300 hours a

month. Each cycle takes approximately 1.5 hours.

If the company adds a new line of scooters, initial demand will be 20 per month. Each

scooter will take 1 hour to make. To offset approaching production capacity, expanding

the assembly line is possible. This will decrease manufacturing time for all products by

20%. However, this will increase the costs of cycles from $400 to $500 and scooters

from $200 to $240. The change will also cause increases in prices from $700 to $750

for cycles and from $450 to $500 for scooters.

Required:

a. What is the average waiting time for cycles if they are the only item manufactured?

b. What are the average waiting times if both cycles and scooters are produced and the

assembly line is not enlarged?

c. What are the average waiting times if both cycles and scooters are produced and the

assembly line is enlarged?

d. What is the expected monthly margin without scooters if the company sells all 92

cycles it manufactures?

e. What are the expected monthly contribution margins if scooters are made with the

current assembly line and with the new assembly line? Assume average sales and that

sales equal production.

f. What action do you recommend?

Lights Manufacturing produces a single product that sells for $130. Variable costs per

unit equal $55. The company expects total fixed costs to be $100,000 for the next

month at the projected sales level of 1,300 units. What is the current breakeven point in

terms of number of units?

A) 770 units

B) 1,819 units

C) 541 units

D) 1,334 units

Which of the following is a cost that, if eliminated, would reduce the actual or

perceived value or utility (usefulness) customers experience from using the product or

service?

A) Non-value-added cost

B) Discretionary cost

C) Value-added cost

D) Committed cost

LaCrosse Products has a budget of $900,000 in 2017 for prevention costs. If it decides

to automate a portion of its prevention activities, it will save $81,000 in variable costs.

The new method will require $41,000 in training costs and $109,000 in annual

equipment costs. Management is willing to adjust the budget for an amount up to the

cost of the new equipment. The budgeted production level is 155,000 units.

Appraisal costs for the year are budgeted at $600,000. The new prevention procedures

will save appraisal costs of $50,200. Internal failure costs average $18 per failed unit of

finished goods. The internal failure rate is expected to be 2% of all completed items.

The proposed changes will cut the internal failure rate by one-third. Internal failure

units are destroyed. External failure costs average $50 per failed unit. The company’s

average external failures average 2% of units sold. The new proposal will reduce this

rate by 45%. Assume all units produced are sold and there are no ending inventories.

What is the net change in the budget for prevention costs if the procedures are

automated in 2017? Will management agree with the changes?

A) $69,000 decrease, yes

B) $69,000 increase, yes

C) $150,000 increase, no

D) $81,000 decrease, yes

The fixed costs of operating the maintenance facility of General Hospital are

$4,500,000 annually. Variable costs are incurred at the rate of $30 per

maintenance-hour. The facility averages 40,000 maintenance-hours a year. Budgeted

and actual hours per user for 2017 are as follows:

Assume that budgeted maintenance-hours are used to calculate the allocation rates.

Required:

a. If a single-rate cost-allocation method is used, what amount of maintenance cost will be

budgeted for each department?

b. If a single-rate cost-allocation method is used, what amount of maintenance cost will be

allocated to each department based on actual usage?

c. If a dual-rate cost-allocation method is used, what amount of maintenance cost will be

budgeted for each department?

d. If a dual-rate cost-allocation method is used, what amount of maintenance cost will be

allocated to each department based on actual usage? Based on budgeted usage for fixed

operating costs and actual usage for variable operating costs?

How is inflation related to capital budgeting? Discuss.

‘Managers should be wary of using the same unitized fixed overhead costs for planning

and control purposes’. Do you agree with this argument? Give reasons for your answer.

Northern Corp is concerned about its declining sales, especially the reduction in the

number of customers. For the last two years, its shirts have won industry awards for

high quality and trend-setting styles. At the latest executive managers’ meeting, all were

blaming each other for the decline. After much discussion and presenting some

fact-finding information, it was determined that sales relationships were the cause of

most of the problems.

Required:

What may be some of the causes and how can the causes be detected if product quality

is not an issue?

Briefly describe the list of items that managers undertake to formulate strategies.

A machine has been identified as a bottleneck and the source of the constraint for a

manufacturing company that has multiple products and multiple machines. Discuss

ways the company can overcome the bottleneck.

High Universal Industries operates a division in Brazil, a country with very high

inflation rates. Traditionally, the company has used the same costing techniques in all

countries to facilitate reporting to corporate headquarters. However, the financial

accounting reports from Brazil never seem to match the actual unit results of the

division. Management has studied the problem and it appears that beginning inventories

may be the cause of the unmatched information. The reason for this is that the

inventories have a different financial base because of the severe inflation.

Required:

How can process costing assist in addressing the problem facing Universal Industries?

“Management control systems consist of formal and informal control systems.” Briefly

explain the formal and informal management systems and enlist their components.

A hotel in Orlando, Florida, experiences peak periods and slower times. How should

prices be adjusted during peak periods? During slow times? Why?

Explain the difference between locked in costs and costs incurred. Which of these types

of costs does a traditional accounting system emphasize? At which stage of the value

chain are most costs locked-in? At which stage of the value chain are most costs

incurred? What implication does this have for good cost management?

Discuss the cost-benefit approach guideline management accountants use to provide

value in strategic decision making.

Why do conflicts arise between the EOQ model’s optimal order quantity and the order

quantity that managers regard as optimal?

Explain how activity-based costing systems can provide more accurate product costs

than traditional cost systems.

Make a list of steps of designing an accounting based performance measure. Give an

example of decisions taken under each step.

Bob and Dale have just purchased a small honey manufacturing company that was

having financial difficulties. After a brief operating period, they decided that the

company’s main problem was an improper budgeting function. The company made a

good product and market potential was great.

Required:

Describe the usual budgeting cycle that well-managed companies adopt?

Skytalk Company manufactures weathervanes. The 2015 operating budget is based on

the production of 5,300 weathervanes with 1.25 machine-hour allowed per

weathervane. Variable manufacturing overhead is anticipated to be $145,750.

Actual production for 2015 was 5,250 weathervanes using 6,050 machine-hours. Actual

variable costs were $21.75 per machine-hour.

Required:

Calculate the variable overhead spending and the efficiency variances.

What are the two components of the sales-volume variance?

Distinguish among spoilage, reworked units, and scrap. Give an example of each.