CHAPTER 15

ALLOCATION OF SUPPORT-DEPARTMENT COSTS,

COMMON COSTS, AND REVENUES

15-1 Distinguish between the single-rate and the dual-rate methods.

The single-rate (cost-allocation) method makes no distinction between fixed costs and variable

15-2 Describe how the dual-rate method is useful to division managers in decision making.

15-3 How do budgeted cost rates motivate the support-department manager to improve

efficiency?

15-4 Give examples of allocation bases used to allocate support-department cost pools to

operating departments.

15-5 Why might a manager prefer that budgeted rather than actual cost-allocation rates be used

for costs being allocated to his or her department from another department?

The use of budgeted indirect cost allocation rates rather than actual indirect rates has several

attractive features to the manager of a user department:

15-6 “To ensure unbiased cost allocations, fixed costs should be allocated on the basis of

estimated long-run use by user-department managers.” Do you agree? Why?

15-7 Distinguish among the three methods of allocating the costs of support departments to

operating departments.

The three methods differ in how they recognize reciprocal services among support departments:

a. The direct (allocation) method ignores any services rendered by one support

c. The reciprocal (allocation) method allocates support-department costs to operating

15-8 What is conceptually the most defensible method for allocating support-department costs?

Why?

15-9 Distinguish between two methods of allocating common costs.

The stand-alone cost-allocation method uses information pertaining to each user of a cost object

as a separate entity to determine the cost-allocation weights.

The incremental cost-allocation method ranks the individual users of a cost object in the

order of users most responsible for the common costs and then uses this ranking to allocate costs

15-10 What are the challenges of using the incremental cost allocation method when allocating

common costs and how might they be overcome?

The challenges of using the incremental method is that every user wants to be considered the

lowest-ranked user because only small incremental costs are allocated to each

15-11 What role does the Cost Accounting Standards Board play when companies contract

with the U.S. government?

15-12 What is one key way to reduce cost-allocation disputes that arise with government

contracts?

15-13 Describe how companies are increasingly facing revenue-allocation decisions.

Companies increasingly are selling packages of products or services for a single price. Revenue

15-14 Distinguish between the stand-alone and the incremental revenue-allocation methods.

The incremental revenue allocation method ranks individual products in a bundle

according to criteria determined by management—such as the product in the bundle with the

15-15 Identify and discuss arguments that individual product managers may put forward to

support their preferred revenue-allocation method.

Managers typically will argue that their individual product is the prime reason why consumers

buy a bundle of products. Evidence on this argument could come from the sales of the products

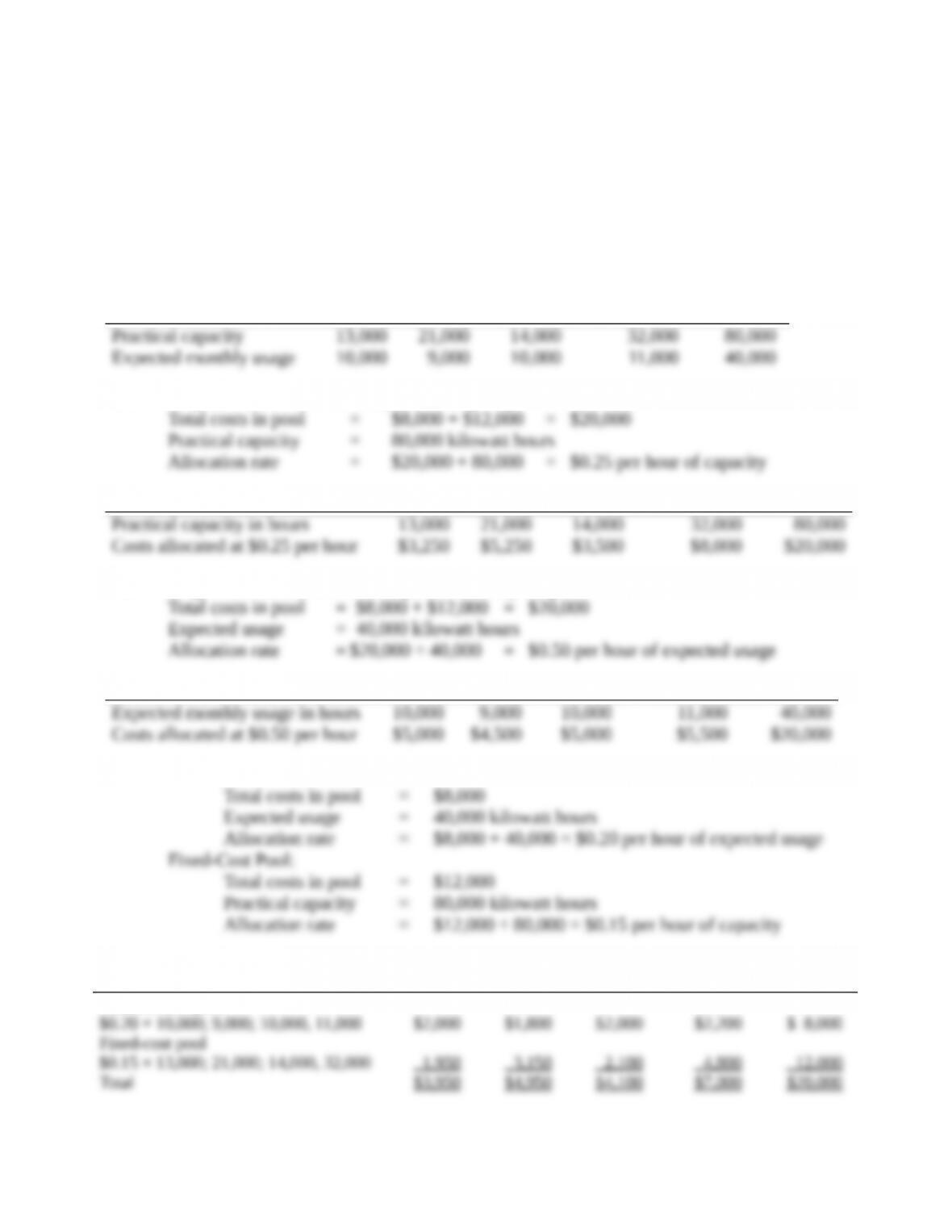

15-16 Single-rate versus dual-rate methods, support department. The Cincinnati power plant

that services all manufacturing departments of Eastern Mountain Engineering has a budget for the

coming year. This budget has been expressed in the following monthly terms:

The expected monthly costs for operating the power plant during the budget year are $20,000:

$8,000 variable and $12,000 fixed.

Required:

1. Assume that a single cost pool is used for the power plant costs. What budgeted amounts will

be allocated to each manufacturing department if (a) the rate is calculated based on practical

capacity and costs are allocated based on practical capacity and (b) the rate is calculated

based on expected monthly usage and costs are allocated based on expected monthly usage?

2. Assume the dual-rate method is used with separate cost pools for the variable and fixed costs.

Variable costs are allocated on the basis of expected monthly usage. Fixed costs are allocated

on the basis of practical capacity. What budgeted amounts will be allocated to each

manufacturing department? Why might you prefer the dual-rate method?

SOLUTION

(20 min.) Single-rate versus dual-rate methods, support department.

Bases available (kilowatt hours):

Loretta Bently Melboum Eastmoreland Total

1a. Single-rate method based on practical capacity:

Loretta Bently Melboum Eastmoreland Total

8

1b. Single-rate method based on expected monthly usage:

Loretta Bently Melboum Eastmoreland Total

2. Variable-Cost Pool:

Loretta

Bently Melboum

Eastmorelan

d Total

Variable-cost pool

The dual-rate method permits a more refined allocation of the power department costs; it permits

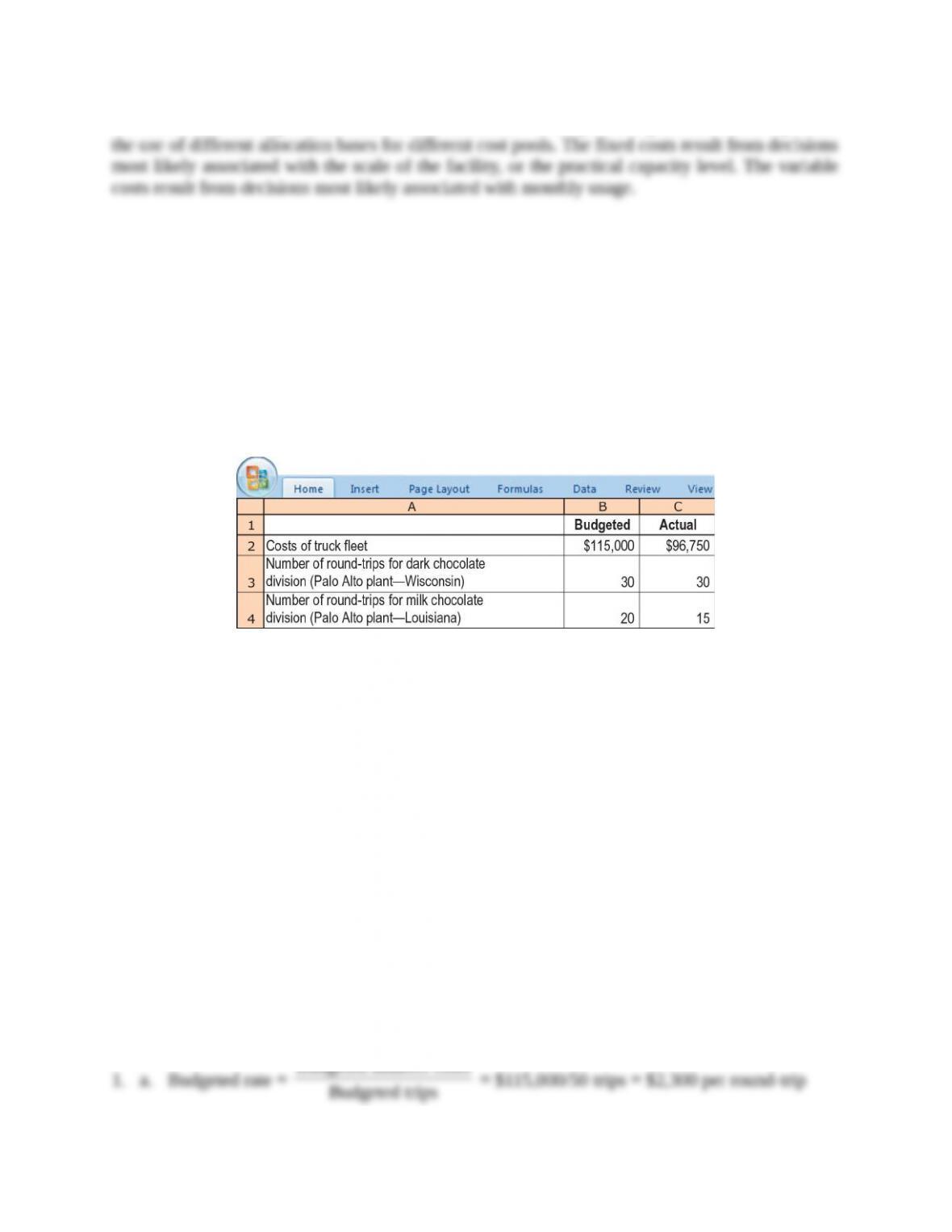

15-17 Single-rate method, budgeted versus actual costs and quantities. Chocolat Inc. is a

producer of premium chocolate based in Palo Alto. The company has a separate division for each

of its two products: dark chocolate and milk chocolate. Chocolat purchases ingredients from

Wisconsin for its dark chocolate division and from Louisiana for its milk chocolate division.

Both locations are the same distance from Chocolat’s Palo Alto plant.

Chocolat Inc. operates a fleet of trucks as a cost center that charges the divisions for variable

costs (drivers and fuel) and fixed costs (vehicle depreciation, insurance, and registration fees) of

operating the fleet. Each division is evaluated on the basis of its operating income. For 2017, the

trucking fleet had a practical capacity of 50 round-trips between the Palo Alto plant and the two

suppliers. It recorded the following information:

Required:

1. Using the single-rate method, allocate costs to the dark chocolate division and the milk

chocolate division in these three ways.

a. Calculate the budgeted rate per round-trip and allocate costs based on round-trips budgeted

for each division.

b. Calculate the budgeted rate per round-trip and allocate costs based on actual round-trips

used by each division.

c. Calculate the actual rate per round-trip and allocate costs based on actual round-trips used

by each division.

2. Describe the advantages and disadvantages of using each of the three methods in requirement

1. Would you encourage Chocolat Inc. to use one of these methods? Explain and indicate any

assumptions you made.

SOLUTION

(20–25 min.) Single-rate method, budgeted versus actual costs and quantities.

Budgeted indirect costs

Budgeted trips

b. Budgeted rate = $2,300 per round-trip

Actual indirect costs

2. When budgeted rates/budgeted quantities are used, the Dark Chocolate and Milk

Chocolate Divisions know at the start of 2017 that they will be charged a total of $69,000 and

When budgeted rates/actual quantities are used, the Dark Chocolate and Milk Chocolate

Divisions know at the start of 2017 that they will be charged a rate of $2,300 per round trip, i.e.,

they know the price per unit of this resource. This enables them to make operating decisions

The use of actual costs/actual quantities makes the costs allocated to one division a

function of the actual demand of other users. In 2017, the actual usage was 45 trips, which is 5

Using actual costs/actual rates also means that any efficiencies or inefficiencies of the

For the reasons stated previously, of the three single-rate methods suggested in this

15-18 Dual-rate method, budgeted versus actual costs and quantities (continuation of

15-17). Chocolat Inc. decides to examine the effect of using the dual-rate method for allocating

truck costs to each round-trip. At the start of 2017, the budgeted costs were:

The actual results for the 45 round-trips made in 2017 were:

Assume all other information to be the same as in Exercise 15-17.

Required:

1. Using the dual-rate method, what are the costs allocated to the dark chocolate division and

the milk chocolate division when (a) variable costs are allocated using the budgeted rate per

round-trip and actual round-trips used by each division and when (b) fixed costs are allocated

based on the budgeted rate per round-trip and round-trips budgeted for each division?

2. From the viewpoint of the dark chocolate division, what are the effects of using the dual-rate

method rather than the single-rate method?

SOLUTION

(20 min.)Dual-rate method, budgeted versus actual costs and quantities (continuation of

15-17).

1. Charges with dual rate method.

Dark Chocolate Division

2. The dual rate changes how the fixed indirect cost component is treated. By using budgeted

trips made, the Dark Chocolate Division is unaffected by changes from its own budgeted usage

or that of other divisions. When budgeted rates and actual trips are used for allocation (see

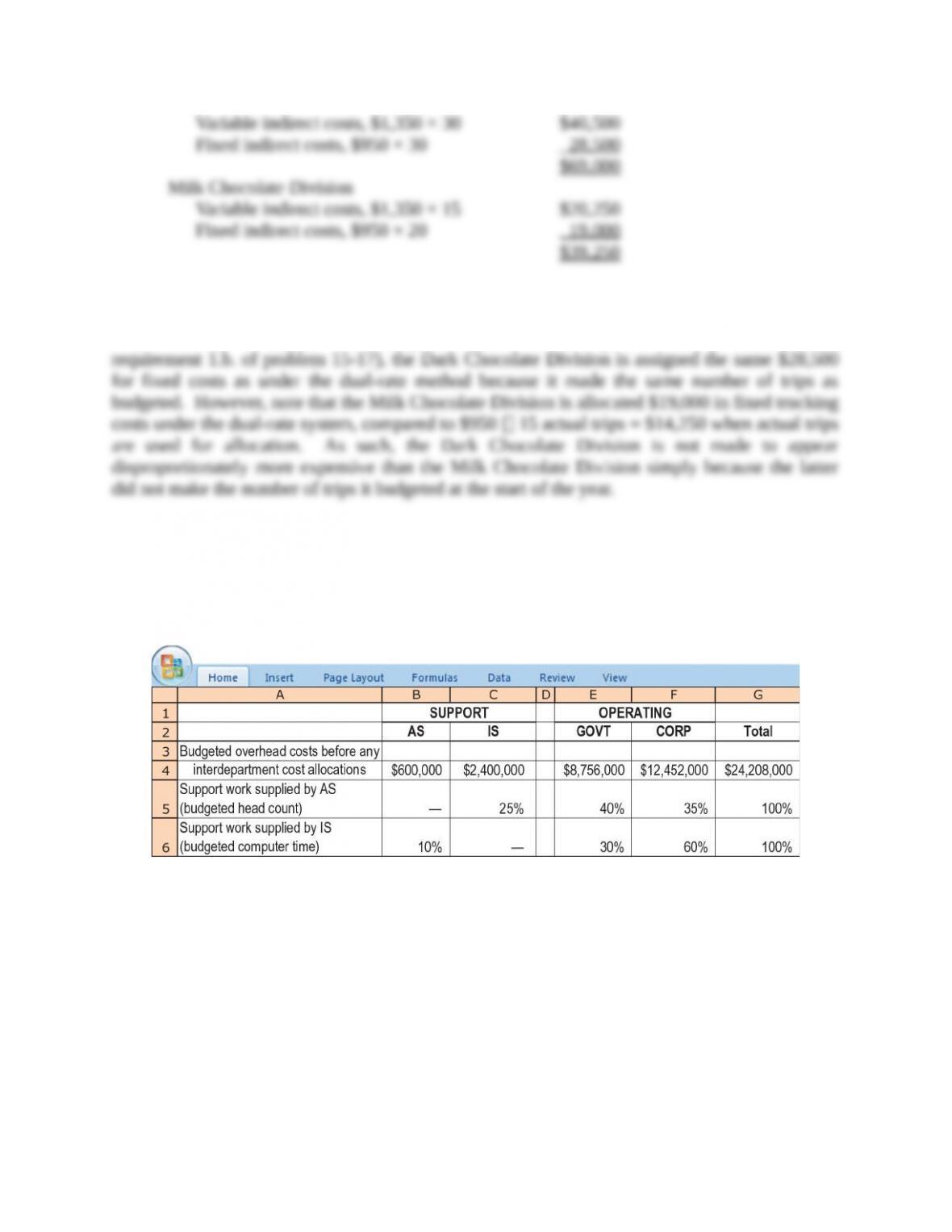

15-19 Support-department cost allocation; direct and step-down methods. Phoenix Partners

provides management consulting services to government and corporate clients. Phoenix has two

support departments—administrative services (AS) and information systems (IS)—and two

operating departments—government consulting (GOVT) and corporate consulting (CORP). For

the first quarter of 2017, Phoenix’s cost records indicate the following:

Required:

1. Allocate the two support departments’ costs to the two operating departments using the

following methods:

a. Direct method

b. Step-down method (allocate AS first)

c. Step-down method (allocate IS first)

2. Compare and explain differences in the support-department costs allocated to each operating

department.

3. What approaches might be used to decide the sequence in which to allocate support

departments when using the step-down method?

SOLUTION

(30 min.) Support department cost allocation; direct and step-down methods.

1. AS IS GOVT CORP

The direct method ignores any services to other support departments. The step-down method

partially recognizes services to other support departments. The information systems support

group (with total budget of $2,400,000) provides 10% of its services to the AS group. The AS

3. Three criteria that could determine the sequence in the step-down method are as follows:

a. Allocate support departments on a ranking of the percentage of their total services

provided to other support departments.

b. Allocate support departments on a ranking of the total dollar amount in the support

departments.

c. Allocate support departments on a ranking of the dollar amounts of service provided

to other support departments

1. Information Systems

2. Administrative Services

The approach in (a) above typically better approximates the theoretically preferred

reciprocal method. It results in a higher percentage of support-department costs provided to other

support departments being incorporated into the step-down process than does (b) or (c), above.

15-20 Support-department cost allocation, reciprocal method (continuation of 15-19). Refer

to the data given in Exercise 15-19.

Required:

1. Allocate the two support departments’ costs to the two operating departments using the

reciprocal method. Use (a) linear equations and (b) repeated iterations.

2. Compare and explain differences in requirement 1 with those in requirement 1 of Exercise

15-19. Which method do you prefer? Why?