SOLUTION

(20 min.) Target costs, effect of product-design changes on product costs.

1. and 2. Manufacturing costs of HJ6 in 2016 and 2017 are as follows:

2016 2017

Per Unit Per Unit

Total (2) = Total (4) =

(1) (1) ÷ 2,700 (3) (3) ÷ 4,600

Direct materials, $1,400 × 2,700; $1,300 × 4,600 $3,780,000 $1,400 $5,980,000$1,300

Batch-level costs (setup, prodn.-order, matl. handlg.)

Actual manufacturing cost per unit of HJ6 in 2017 was $1,747. Hence, Neuro did achieve its

target manufacturing cost per unit.

4. To reduce the manufacturing cost per unit in 2017, Neuro reduced the cost per unit in

each of the four cost categories—direct materials costs, batch-level costs, manufacturing

operations costs, and engineering change costs. It also reduced machine-hours, reduced the

5. Neuro’s managers might encounter the following challenges in achieving the target costs:

• Employees may feel they are being pushed too hard to attain target costs. The actual

costs in 2017 are well below the target costs.

To overcome these challenges, managers should: (1) encourage employee participation and

13-2

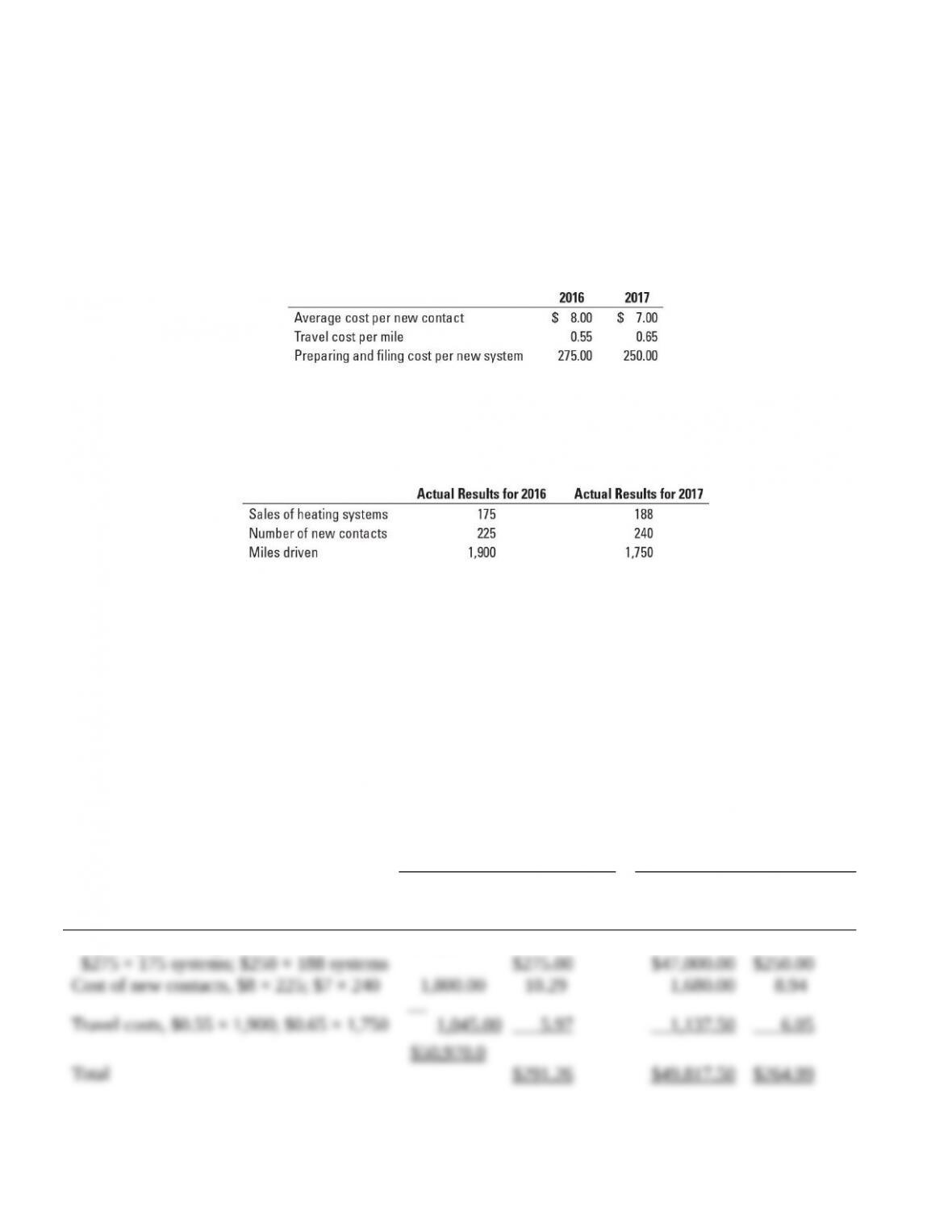

3. Target cost per sale in 2017 = Cost per sale in 2016 × 92%

Actual cost per heating system sold in 2017 was $264.99. Hence, Solar Energy Systems did

achieve its target cost per system sold of $267.96.

The company was able to reduce the cost per heating system sold in 2017 by reducing the costs

of preparing and filing forms for rebates, tax credits and financing from $275 per system sold to

4. The challenges Solar Energy Systems may face in achieving their target cost include

employee resistance to changes in processes, unexpected increases in the cost of supplies, fuel,

etc, and new compliance requirements imposed from the federal and/or state governments that

13-22 Cost-plus target return on investment pricing. Jason Brady is the managing partner of

a business that has just finished building a 60-room motel. Brady anticipates that he will rent

these rooms for 15,000 nights next year (or 15,000 room-nights). All rooms are similar and will

rent for the same price. Brady estimates the following operating costs for next year:

The capital invested in the motel is $1,500,000. The partnership’s target return on investment is

20%. Brady expects demand for rooms to be uniform throughout the year. He plans to price the

rooms at full cost plus a markup on full cost to earn the target return on investment.

13-3

Required:

1. What price should Brady charge for a room-night? What is the markup as a percentage of the

full cost of a room-night?

2. Brady’s market research indicates that if the price of a room-night determined in requirement

1 is reduced by 10%, the expected number of room-nights Brady could rent would increase

by 10%. Should Brady reduce prices by 10%? Show your calculations.

SOLUTION

(20 min.) Cost-plus target return on investment pricing.

1. Target operating income = target return on investment invested capital

Proof

The full cost of a room = variable cost per room + fixed cost per room

Markup per room = Rental price per room – Full cost of a room

2. If price is reduced by 10%, the number of rooms Brady could rent would increase by 10%.

Because the contribution margin of $693,000 at the reduced price of $45 is less than the

13-4

13-23 Cost-plus, target pricing, working backward. KidsPlay, Inc., manufactures and sells

table sets. In 2016, it reported the following:

Units produced and sold 3,000

Investment $3,000,000

Markup percentage on full cost 10%

Rate of return on investment 15%

Variable cost per unit $600

Required:

1. What was KidsPlay’s operating income in 2016? What was the full cost per unit? What was

the selling price? What was the percentage markup on variable cost to achieve the selling

price? What are the total fixed costs?

2. KidsPlay is considering increasing the annual spending on advertising by $200,000. The

managers believe that the investment will translate into a 10% increase in unit sales. Should

the company make the investment? Show your calculations.

3. Refer back to the original data. In 2017, KidsPlay believes that it will be able to sell only

2,700 units at the price calculated in requirement 1. Management has identified $185,000 in

fixed cost that can be eliminated. If KidsPlay wants to maintain a 10% markup on full cost,

what is the target variable cost per unit?

SOLUTION

(25 min.) Cost-plus, target pricing, working backwards.

1. Investment $3,000,000

Rate of return on investment 15%

Total fixed costs = (Full cost per unit – Variable cost per unit) Units sold

13-5

3.

Revenues ($1,650 × 2,700 units) $4 ,455,000

KidsPlay’s target variable cost at a sales volume of 2,700 units is nearly $32 lower than the

current actual cost. This will present a significant challenge as will the reduction of $185,000 in

fixed costs. Nevertheless, KidsPlay’s senior executives would need to challenge its managers to

work together to achieve these targets in order to stay competitive.

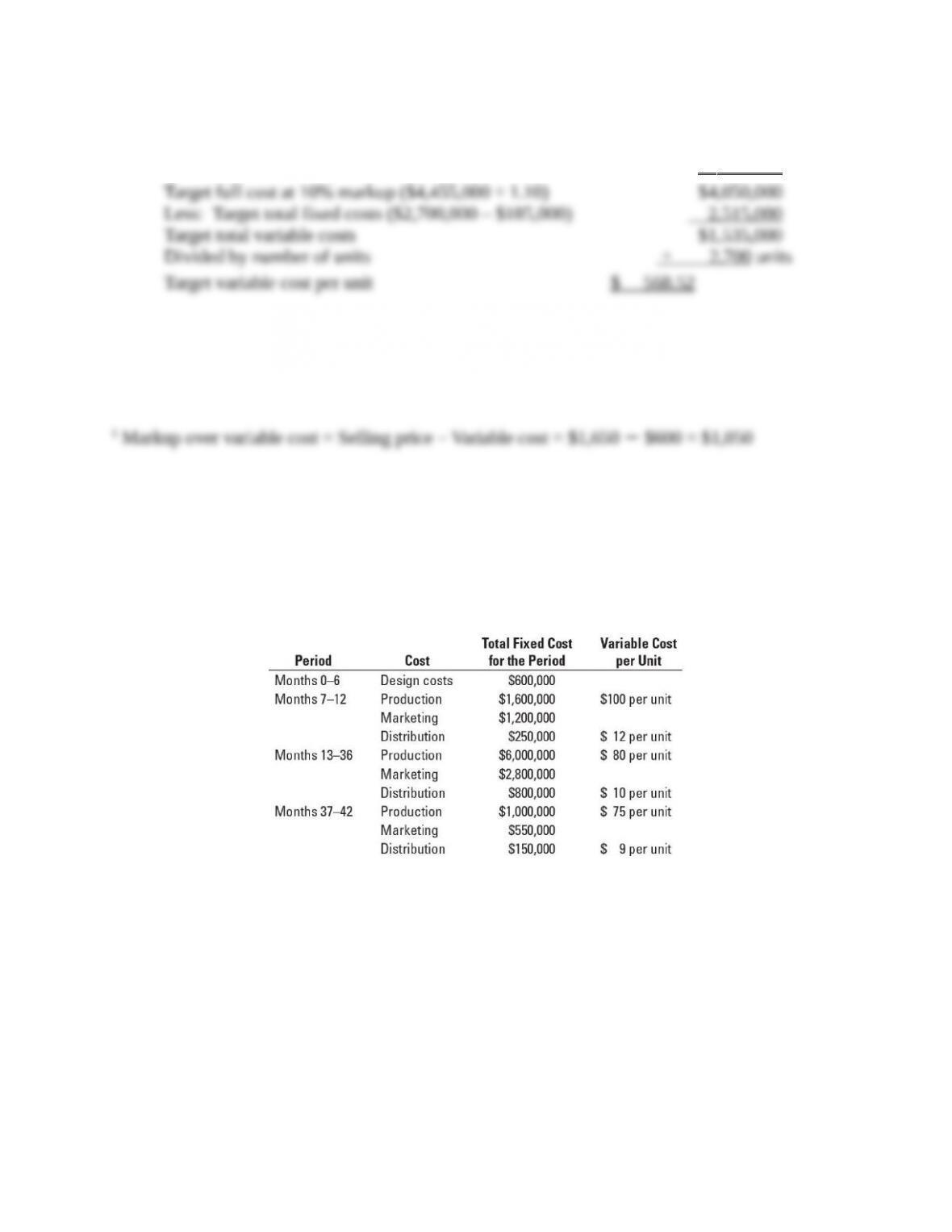

13-24 Life-cycle budgeting and costing. Arnold Manufacturing, Inc., plans to develop a new

industrial-powered vacuum cleaner for household use that runs exclusively on rechargeable

batteries. The product will take 6 months to design and test. The company expects the vacuum

sweeper to sell 12,000 units during the first 6 months of sales; 24,000 units per year over the

following 2 years; and 10,000 units over the final 6 months of the product’s life cycle. The

company expects the following costs:

Ignore the time value of money.

Required:

1. If Arnold prices the sweepers at $400 each, how much operating income will the company

make over the product’s life cycle? What is the operating income per unit?

2. Excluding the initial product design costs, what is the operating income in each of the three

sales phases of the product’s life cycle, assuming the price stays at $400?

3. How would you explain the change in budgeted operating income over the product’s life

cycle? What other factors does the company need to consider before developing the new

13-6

vacuum sweeper?

4. Arnold is concerned about the operating income it will report in the first sales phase. It is

considering pricing the vacuum sweeper at $450 for the first 6 months and decreasing the

price to $400 thereafter. With this pricing strategy, Arnold expects to sell 10,000 units instead

of 12,000 units in the first 6 months, and the same number of units for the remaining life

cycle. Assuming the same cost structure given in the problem, which pricing strategy would

you recommend? Explain.

SOLUTION

Life-cycle budgeting and costing.

1.

Projected Life Cycle Income Statement

Revenues [$400 × (12,000 + 24,000 + 24,000 + 10,000)] $28 ,000,000

Variable costs:

Fixed costs:

2.

Projected Life Cycle Income Statement (in 000s)

Months 7–12

Revenues ($400 × 12,000) $4 ,800,000

Variable costs:

13-7

Projected Life Cycle Income Statement (in 000s)

Months 13–36

Revenues ($400 × 48,000) $19,200,000

Variable costs:

Projected Life Cycle Income Statement (in 000s)

Months 37–42

Revenues 400 × 10,000) $ 4,000,000

Variable costs:

3. In analyzing the relative profitability of the product during the three sales phases of its

life cycle, the results are as expected. During the initial growth phase, all fixed costs, including

marketing, are higher in order to successfully launch the new product. In addition, variable costs

are higher per unit because the company has not yet capitalized on economies of scale. As the

13-8

The company would need to consider several other factors before it decides to develop the new

vacuum cleaner. The company may need to analyze the probability that the price will be able to

4.

Projected Life Cycle Income Statement

Revenues [$450 × 10,000 + $400 × (48,000 + 10,000)] $27 ,700,000

Variable costs:

Months 7–12 ($112 × 10,000 ) 1,120,000

Arnold earns more profit under its original plan ($6,546,000) than it does if it increases the price

to $450 for the first six months ($6,470,500). The higher price is more than offset by the decline

in sales decreasing operating income. Therefore, Arnold should keep the price of the

vacuum-cleaners at $400 for the first six months rather than increasing it to $450.

Arnold could also simply have compared the contribution margin in Months 7 − 12 from

increasing prices:

Arnold earns a higher contribution margin in the Months 7 − 12 at a price of $400 from selling

12, 000 units. The revenue and costs over the remaining months are identical and so irrelevant.

13-9

13-25 Considerations other than cost in pricing decisions. Happy Times Hotel operates a

100-room hotel near a busy amusement park. During June, a 30-day month, Happy Times Hotel

experiences a 70% occupancy rate from Monday evening through Thursday evening (weeknights).

On Friday through Sunday evenings (weekend nights), however, occupancy increases to 90%.

(There were 18 weeknights and 12 weekend nights in June.) Happy Times Hotel charges $80 per

night for a suite. The company recently hired Gina Davis to manage the hotel to increase the hotel’s

profitability. The following information relates to Happy Times Hotel’s costs:

Happy Times Hotel offers free breakfast to guests. In June, there are an average of two breakfasts

served per room-night on weeknights and four breakfasts served per room-night on weekend

nights.

Required:

1. What was Happy Times Hotel’s operating income or loss for the month?

2. Gina Davis estimates that if Happy Times Hotel decreases the nightly rates to $70, weeknight

occupancy will increase to 80%. She also estimates that if the hotel increases the nightly rate

on weekend nights to $100, occupancy on those nights will remain at 90%. Would this be a

good move for Happy Times Hotel? Show your calculations.

3. Why would Happy Times Hotel have a $30 price difference between weeknights and

weekend nights?

4. A discount travel clearinghouse has approached Happy Times Hotel with a proposal to offer

last-minute deals on empty rooms on both weeknights and weekend nights. Assuming that

there will be an average of three breakfasts served per night per room, what is the minimum

price that Happy Times Hotel could accept on the last-minute rooms?

13-10