SOLUTION

(50 min.) ABC, implementation, ethics.

1. Plum Electronics should not emphasize the Maximum model and should not phase out

the Mammoth model. Under activity-based costing, the Maximum model has an operating

income percentage of less than 3%, while the Mammoth model has an operating income

percentage of nearly 43%.

Cost driver rates for the various activities identified in the activity-based costing (ABC) system

are as follows:

Plum Electronics

Calculation of Costs of Each Model

under Activity-Based Costing

Mammoth Maximum

Direct materials ($228.80 22,000; $642.40 4,000) $ 5,033,600

Direct manuf. labor ($13.20 1.5 hrs. 22,000;

$13.20 3.5hrs. 4,000) 435,600

184,800

Indirect costs

Soldering ($0.66 1,185,000; $0.66 385,000) 782,100

Shipments ($47.30 16,200; $47.30 3,800) 766,260

5-1

Total indirect costs 3 ,476,110

Profitability analysis

Mammoth Maximum Total

Revenues $21,780,000 $5,016,000 $26,796,000

Per-unit calculations:

Selling price

($21,780,000 22,000;

Cost of goods sold

($12,430,110 22,000;

Gross margin percentage 42.9% 2.8%

2. Plum’s simple costing system allocates all manufacturing overhead other than machine

costs on the basis of machine-hours, an output unit-level cost driver. Consequently, the more

The ABC analysis recognizes several batch-level cost drivers such as purchase orders,

shipments, and setups. Maximum uses these resources much more intensively than Mammoth.

The ABC system recognizes Maximum’s use of these overhead resources. Consider, for example,

Recognizing Maximum’s more intensive use of manufacturing overhead results in

Maximum showing a much lower profitability under the ABC system. By the same token, the

3. Clark’s comments about ABC implementation are valid. When designing and

implementing ABC systems, managers and management accountants need to trade off the costs

5-2

4. Activity-based management (ABM) is the use of information from activity-based costing

to make improvements in a firm. For example, a firm could revise product prices on the basis of

5. Incorrect reporting of ABC costs with the goal of retaining both the Mammoth and

Maximum product lines is unethical. In assessing the situation, the specific “Standards of Ethical

Competence

Integrity

accountant to communicate favorable as well as unfavorable information.

Credibility

Jacobs should indicate to Clark that the product cost calculations are, indeed, appropriate.

If Clark still insists on modifying the product cost numbers, Jacobs should raise the matter with

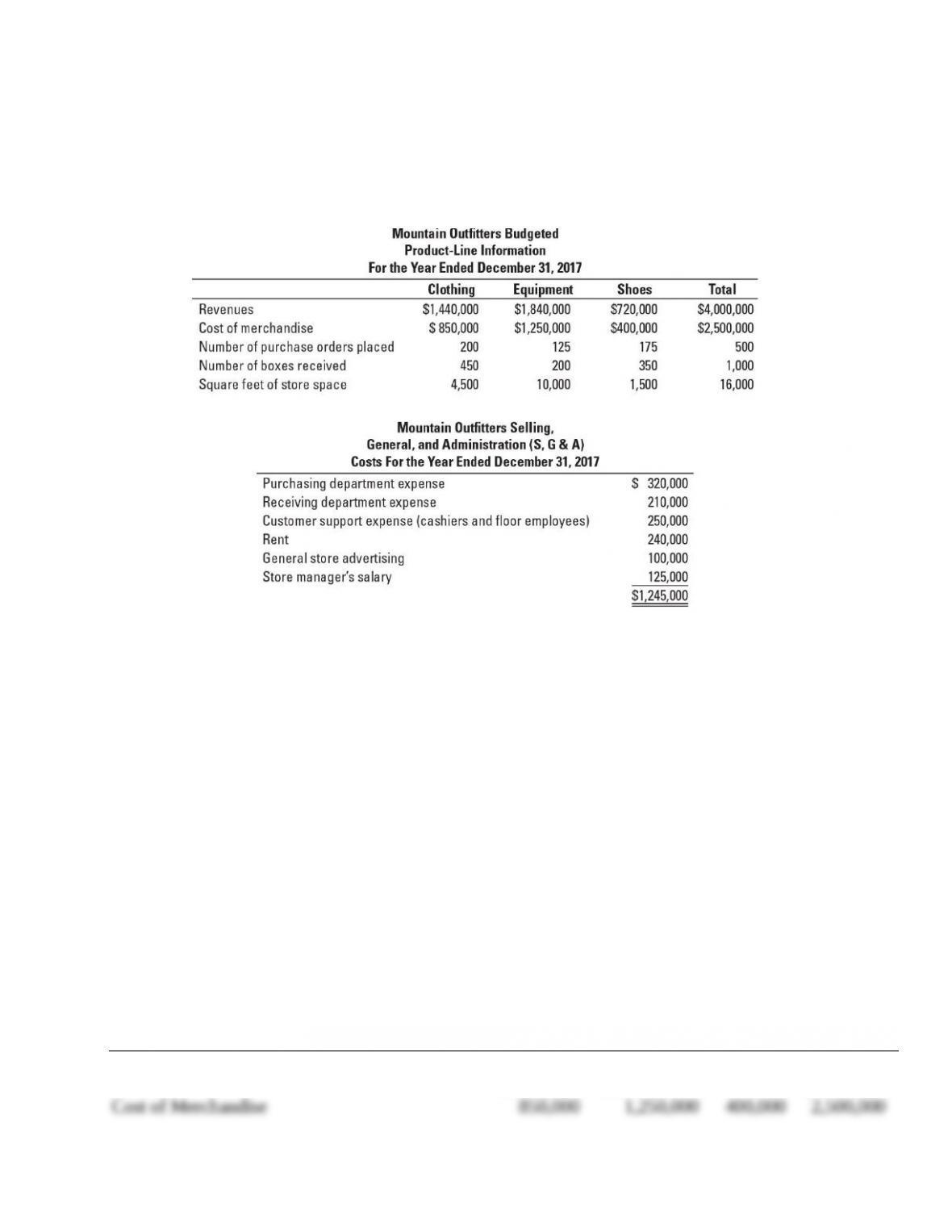

5-43 Activity-based costing, activity-based management, merchandising. Mountain

Outfitters operates a large outdoor clothing and equipment store with three main product lines:

clothing, equipment, and shoes. Mountain Outfitters operates at capacity and allocates selling,

general, and administration (S, G & A) costs to each product line using the cost of merchandise

5-3

of each product line. The company wants to optimize the pricing and cost management of each

product line and is wondering if its accounting system is providing it with the best information

for making such decisions. Store manager Aaron Budd gathers the following information

regarding the three product lines:

For 2017, Mountain Outfitters budgets the following selling, general, and administration costs:

Required

1. Suppose Mountain Outfitters uses cost of merchandise to allocate all S, G & A costs. Prepare

budgeted product-line and total company income statements.

2. Identify an improved method for allocating costs to the three product lines. Explain. Use the

method for allocating S, G & A costs that you propose to prepare new budgeted product-line

and total company income statements. Compare your results to the results in requirement 1.

3. Write a memo to Mountain Outfitters management describing how the improved system

might be useful for managing the store.

SOLUTION

(30-40 mins.) Activity-based costing, activity-based management, merchandising.

1.

Mountain Outfitters

Budgeted Income Statement

For the Year Ended 31 December, 2017

Clothing Equipment Shoes Total

Revenues $1,440,000 $1,840,000

$720,00

0 $4,000,000

5-4

Allocated Selling, General and Administration

Costsa

2. Selling, general, and administration (S, G, & A) is comprised of a variety of costs that are

unlikely to be consumed uniformly across product lines based on the cost of merchandise.

Mountain Outfitters should consider an activity-based costing system to clarify how each

product line uses these S, G, & A resources.

Clothing

Equipment

Shoes

Total

Number of purchase orders

Number of boxes received

Square feet of store space

Purchasing department

Receiving department

Customer support

Rent

General store advertising

5-5

Store manager’s salary

Clothing

Equipment

Shoes

Total

Revenues

Cost of Merchandise

Gross margin

Purchasing

($640 × 200; 125; 175 orders)

Receiving

($210 × 450; 200; 350 deliveries)

Customer Support

($0.0625 × $1,440,000; 1,840,000; $720,000)

Rent

5-6

General store advertising

($0.025 × $1,440,000; 1,840,000; $720,000)

Store manager’s salary

($0.05 × $850,000; $1,250,000; $400,000)

Total S, G, & A costs

Operating income

$ 29,000

3.

To: Mountain Outfitters Management Team

From: Cost Analyst

Re: Costing System

The percentage revenue, COGS, and activity costs for each product line are:

Clothing Equipment Shoes Total

5-7

Revenues

Cost of merchandise

Activity areas:

36%

34%

46%

50%

18%

16%

100%

100%

The current accounting system allocates indirect costs (S,G, & A) to product lines based on the

Cost of Merchandise sold. Using this method, the S, G, & A costs are assigned 34%, 50%, 16%,

to the Clothing, Equipment, and Shoes product lines, respectively. As the preceding table

I recommend that the organization switch to an activity-based costing (ABC) method. With ABC,

the product lines are assigned indirect costs based on their consumption of the activities that give

An ABC analysis can also help Mountain Outfitters manage its costs by reducing the number of

Try It 5-1 Solution

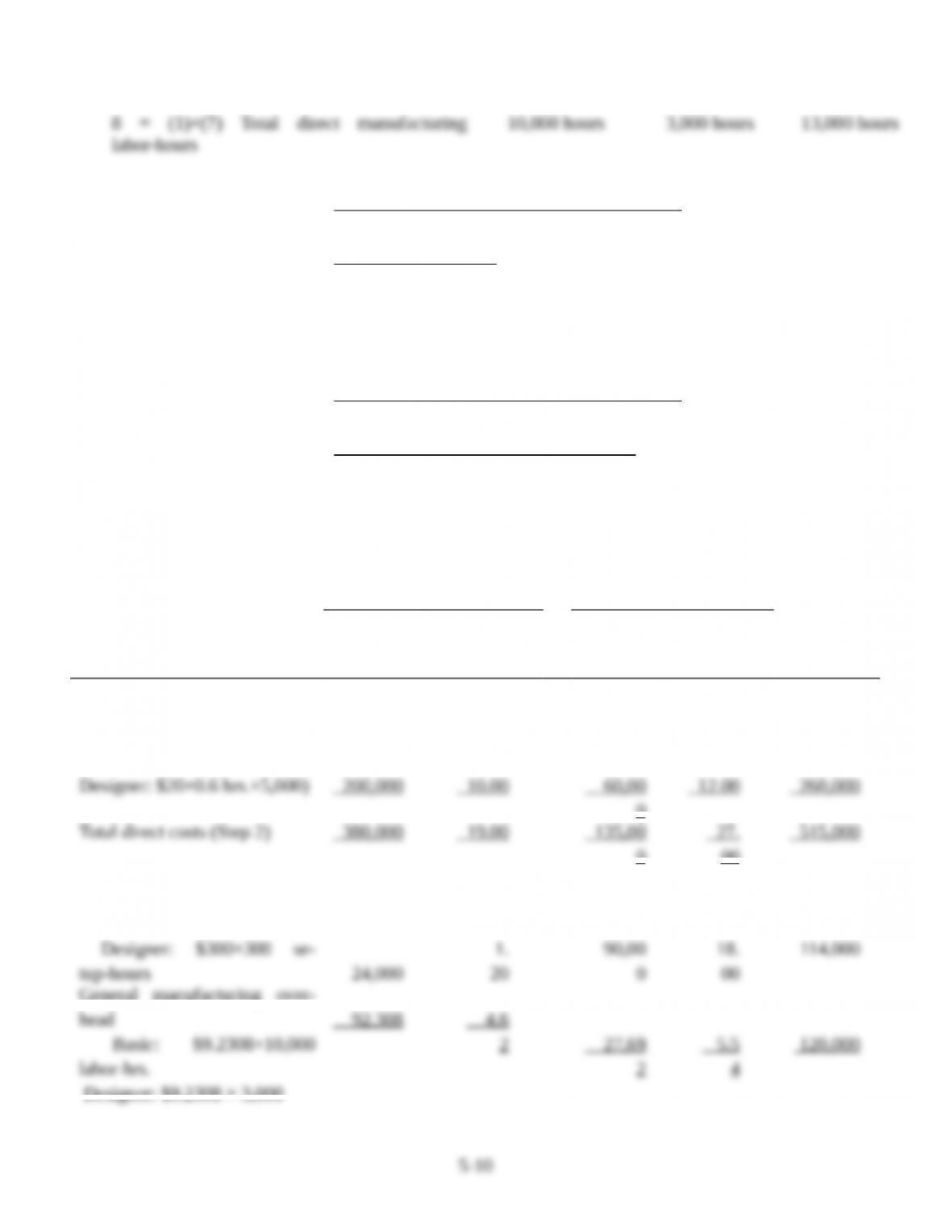

We first calculate the budgeted indirect cost rate for the overhead cost pool

Total budgeted direct manufacturing labor-hours = 0.5hrs. × 20,000 + 0.6 hrs. × 5,000 = 13,000 hours

Budgeted total costs in indirect-cost pool

Budgeted indirect-cost rate Budgeted total quantity of cost-allocation base

$234,000

13,000 direct manufacturing labor-hours

$18 per direct manufacturing labor-ho

=

=

=ur

5-8

20,000 5,000

Basic Lamps Designer Lamps

Total per Unit Total per Unit Total

(1) (2)=(1)÷20,0

00

(3) (4)=(3)÷5,00

0

(5)=(1)+(

3)

Direct materials $180,00

0

$

9

$

75,000

$15.

00

$255,00

0

Direct manufacturing labor

(Basic: $20 × 0.5hrs. × 20,000;

0

28

0

80

0

Try It Solution 5-2

We first calculate the overhead rates for each indirect cost pool.

Basic Lamps Designer Lamps Total

1Quantity of lamps produced 20,000 lamps 5,000 lamps

2Number of lamps produced per batch 250 lamps per

batch

50 lamps per

batch

3 = (1)÷(2) Number of batches 80 batches 100 batches

7 Direct manufacturing labor-hours per lamp 0.5 hours 0.6 hours

5-9

8 = (1)×(7) Total direct manufacturing

10,000 hours 3,000 hours 13,000 hours

labor-hrs.

2

2

54

5-11