Manufacturing Cycle Efficiency (MCE) = Value-added Manufacturing Time divided by

Manufacturing Cycle Time.

Practical capacity is the level of capacity that reduces theoretical capacity by

considering unavoidable operating interruptions, such as scheduled maintenance time

and shutdowns for holidays.

Using practical capacity as the denominator level sets the cost of capacity at the cost of

supplying the capacity, regardless of the demand for the capacity.

The full cost plus a markup transfer-pricing method can sometimes lead to goal

incongruence.

The shorter the time horizon, the lower the percentage of total costs considered fixed.

In the decision making of a one-time-only special order, it is assumed that accepting the

special order is

not expected to affect the selling price to other customers.

If a cost pool is homogeneous, the cost allocations using that pool will be the same as

they would be if costs of each individual activity in that pool were allocated separately.

Research shows that the performance of employees falls when they are asked to adhere

to challenging budgets.

The accrual accounting rate-of-return method is a discounted cash flow approach to

analyzing possible capital budget expenditures.

Management accounting ensures communication of an organization’s financial position

to investors, banks, and regulators.

A company usually prepares a budget for nonmanufacturing costs after preparing all

operating budgets.

An example of a physical cause-and-effect relationship is when additional units of

production increase total direct material costs.

In joint costing, the physical measures are generally used for products or services that

are processed and, after split-off, additional value is added to the product and a selling

price can be determined.

Contribution margin = Contribution margin percentage × Revenues (in dollars).

The cost of natural gas used to heat a production facility that makes three products

(A,B, and C) would be classified as an indirect cost when the cost object is one of the

products (either A, B, or C).

The controller is usually responsible for budgeting.

Corporate-sustaining costs are costs of activities to support individual customers,

regardless of the number of units or batches of product delivered to the customer.

Contribution margin percentage = Selling price – Variable cost per unit

Activity-based costing analysis takes a long-run perspective and treats all activity costs

as variable costs.

When calculating the equivalent units, we should only focus on dollar amounts of

inventory.

Variable costs per unit vary with the level of production or sales volume.

Weighted-average cost per equivalent unit is obtained by dividing the sum of costs for

beginning work in process plus costs for work done in the current period by total

equivalent units of work done to date.

The account analysis method of cost estimation classifies account costs as fixed, mixed,

or variable using qualitative judgments.

The stand-alone method uses the product in the bundle with the most sale and then uses

this ranking to allocate bundled revenues to individual products.

With the use of a bar chart, the number of “unprofitable” customers and the magnitude

of their losses are apparent.

Incongruent decision making occurs when individuals and groups work toward

achieving the organization’s goals even if departmental performance is adversely

affected.

Variable costing only includes direct manufacturing costs in inventoriable costs.

When choosing among cost drivers, managers trade off level of detail, accuracy,

feasibility, and costs of estimating functions.

Budgets are sometimes called targets or commitments by some companies and as such

are “set in stone” to provide effective benchmarks for management.

Transfer-pricing systems enable managers to focus on maximizing the performance of

their subunits.

Companies operating in competitive markets generally use the cost-plus approach to

price products.

Quantitative factors, such as direct material costs, are outcomes that are measured in

numerical terms.

Oil refining companies primarily use job costing to estimate costs.

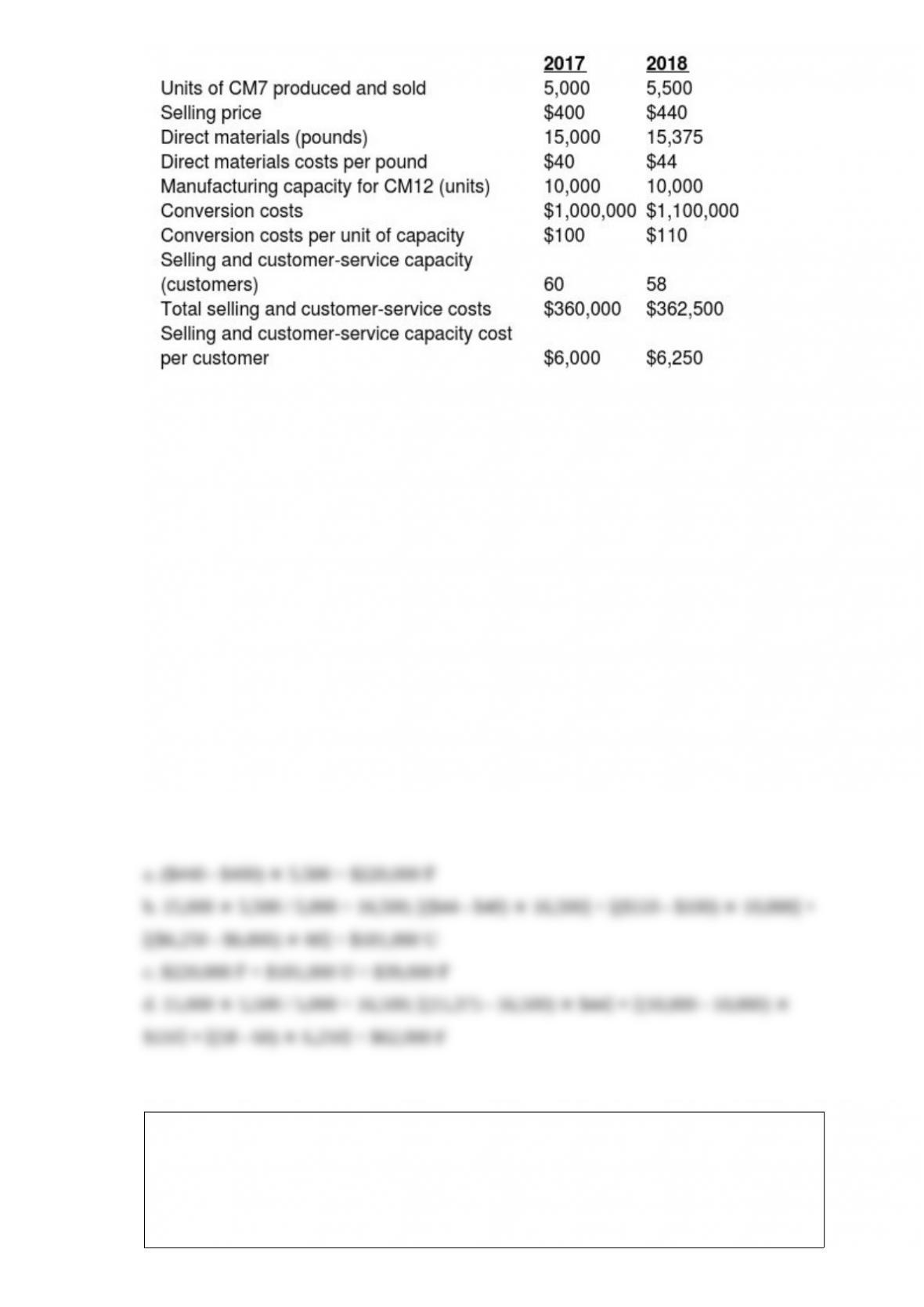

Following a strategy of product differentiation, Somerset Corporation makes a high-end

computer monitor, CM7. Somerset Corporation presents the following data for the

years 2017 and 2018:

Somerset Corporation produces no defective units but it wants to reduce direct materials

usage per unit of CM7 in 2017. Manufacturing conversion costs in each year depend on

production capacity defined in terms of CM7 units that can be produced. Selling and

customer-service costs depend on the number of customers that the customer and service

functions are designed to support. Ernsting Corporation has 100 customers in 2017 and

115 customers in 2018. The industry market size for high-end computer monitors increased

5% from 2017 to 2018.

Required:

a. What is the revenue effect of the price-recovery component?

b. What is the cost effect of the price-recovery component?

c. What is the net effect on operating income as a result of the price-recovery component?

d. What is the net effect on operating income as a result of the productivity component?

Which of the following is not true regarding balanced scorecard measures?

A) Both financial and nonfinancial measures help managers manage performance along

the time dimension

B) Nonfinancial measures help managers evaluate goal achievement regarding

manufacturing cycle time

C) the balanced scorecard does not help highlight linkages across the financial and

nonfinancial perspectives of the balance scorecard

D) revenue and cost measures help managers evaluate the financial effects of increases

and decreases in nonfinancial measures

Manton Manufacturing applies manufacturing overhead costs to products at a budgeted

indirect-cost rate of $60 per direct manufacturing labor-hour. A retail outlet has

requested a bid on a special order of the Toy Bear product. Estimates for this order

include: Direct materials of $79,000; 680 direct manufacturing labor-hours at $25 per

hour; and a 25% markup rate on total manufacturing costs. Manufacturing overhead

cost estimates for this special-order total ________.

A) $60,550

B) $57,800

C) $40,800

D) $59,250

Which of the following is true of relevant information?

A) All fixed costs are relevant.

B) All Future revenues and expenses are relevant.

C) Future

D) All fixed costs are not relevant.

Which of the following departments is most likely to be a cost center?

A) sales department of a company selling industrial tools

B) call center of a company that serves customers and cross-sells other products

C) maintenance department of a luxury resort

D) research department of a company providing consultancy services

Which of the following statements regarding manufacturing overhead allocation is true?

A) It includes all manufacturing costs that cannot be directly traced to a product or

service.

B) The costs can be grouped only as a single indirect-cost pool.

C) Total costs are unknown at the end of the accounting period.

D) Allocated amounts are debited to Manufacturing Overhead Control.

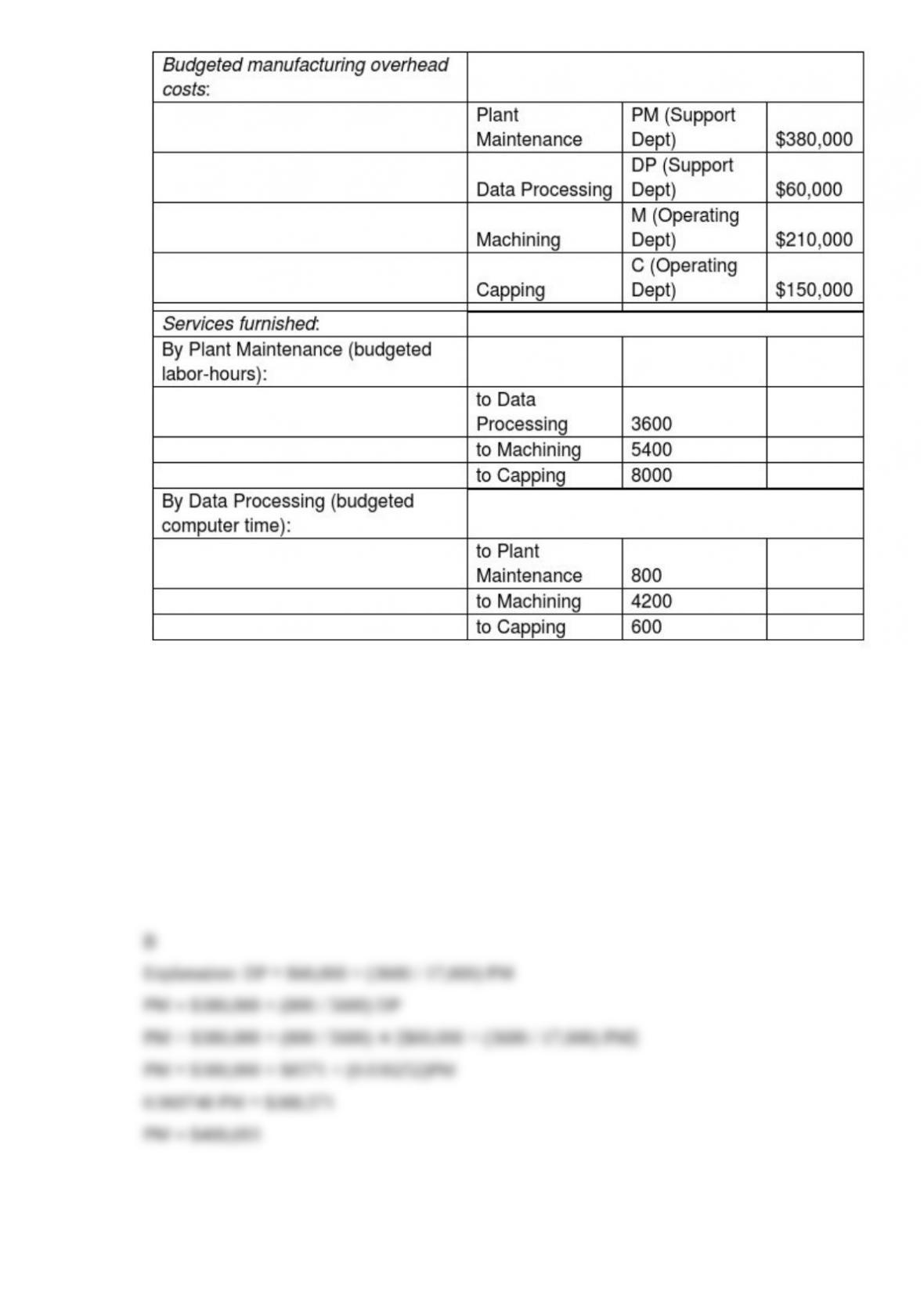

Alfred, owner of Hi-Tech Fiberglass Fabricators, Inc., is interested in using the

reciprocal allocation method. The following data from operations were collected for

analysis:

What is the complete reciprocated cost of the Plant Maintenance Department? (Do not

round any intermediary calculations.)

A) $411,143

B) $400,693

C) $440,000

D) $404,957

Which of the following journal entries is used to record fixed overhead costs allocated?

A) Fixed Overhead Allocated

Work-in-Process Control

B) Work-in-Process Control

Fixed Overhead Allocated

C) Fixed Overhead Control

Work-in-Process Control

D) Fixed Overhead Allocated

Fixed Overhead Control

When fixed costs are $70,000 and variable costs are 60% of the selling price, then

breakeven sales are ________. (Round the final answer to the nearest dollar.)

A) $116,667

B) $175,000

C) $112,000

D) $98,000

When machine-hours are used as an overhead cost-allocation base, the most likely

cause of a favorable variable overhead spending variance is ________.

A) excessive machine breakdowns

B) the production scheduler efficiently scheduled jobs

C) a decline in the cost of energy

D) strengthened demand for the product

Auto Tires has been in the tire business for four years. It rents a building but owns all of

its equipment. All employees are paid a fixed salary except for the busy season

(April-June), when temporary help is hired by the hour. Utilities and other operating

charges remain fairly constant during each month except those in the busy season.

Selling prices per tire average $75 except during the busy season. Because a large

number of customers buy tires prior to winter, discounts run above average during the

busy season. A 15% discount is given when two tires are purchased at one time. During

the busy months, selling prices per tire average $60.

The president of Auto Tires is somewhat displeased with the company’s management

accounting system because the cost behavior patterns displayed by the monthly

breakeven charts are inconsistent; the busy months’ charts are different from the other

months of the year. The president is never sure if the company has a satisfactory margin

of safety or if it is just above the breakeven point.

Required:

a. Why might it be difficult to use CVP in this situation?

b. How can the information be presented in a better format for the president?

A master budget is ________.

A) a budget which starts from a zero base

B) based on the level of expected output at the start of the budget period

C) developed at the end of a period

D) a type of flexible budget once actual results are known

BarGraphs Corp. had capacity to produce 4000 units of L3 using 40,000 kg of direct

materials. BarGraphs produced 3850 units of L3 by processing 35,500 kg of direct

materials. Conversion cost per unit is $7.00. BarGraphs can add or reduce

manufacturing capacity in increments of 4500 kgs.

What would be the cost savings if BarGraphs decides to reduce manufacturing capacity

by 4500 kgs?

A) $3150

B) $700

C) $1050

D) $4500

The time from which a machine is setup for order till the product becomes a

manufactured good is ________.

A) waiting time

B) manufacturing time

C) manufacturing cycle time

D) customer-response time

If selling price per unit is $55, variable costs per unit are $25, total fixed costs are

$24,000, the tax rate is 35%, and the company sells 7,000 units, net income is

________.

A) $186,000

B) $75,250

C) $136,500

D) $120,900

When there is an excess capacity, it makes sense to accept a one-time-only special order

for less than the current selling price if ________.

A) incremental revenues exceed incremental costs

B) additional fixed costs is incurred to accommodate the order

C) the company placing the order is in the same market segment as your current

customers

D) incremental revenue equals incremental operating income

Dartmouth Building Products Inc. provides the following information.

Corporate advertising costs = $860,000

Division A – $4,900,000

Division B – $19,600,000

Number of ads run on Division A products 600

Number of ads run on Division B products 4400

Assume that customers with higher revenues benefited more from corporate advertising

costs than customers with lower revenues. What is the allocated corporate costs for

Division B?

A) $756,800

B) $215,000

C) $688,000

D) $172,000

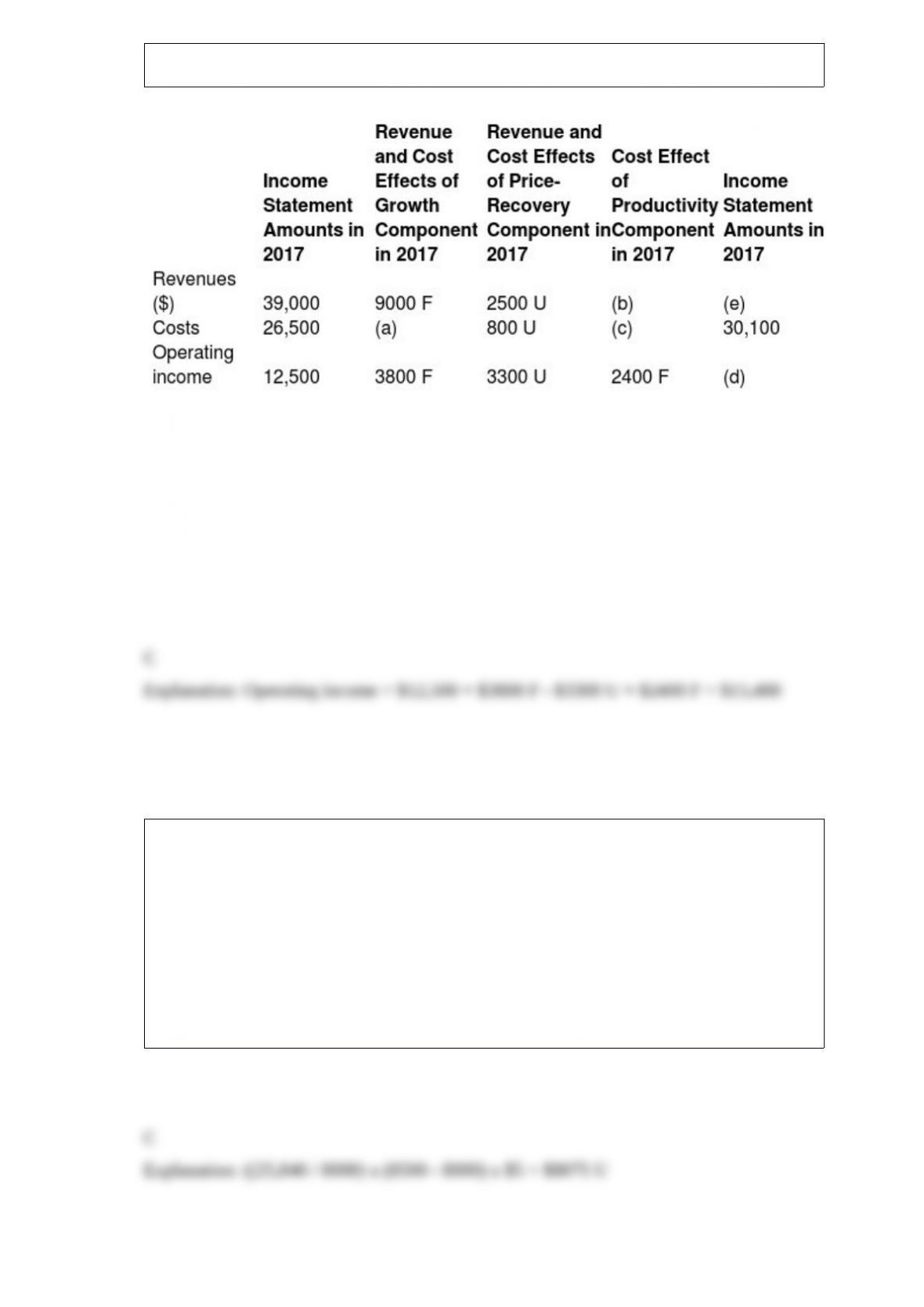

Strategic Analysis of Profitability of King Philip Company:

What is the operating income amount for 2017 (d)?

A) $45,500

B) $32,500

C) $15,400

D) $9600

In 2016, Smart Office Systems Inc. (SOSI) used 25,840 pounds of plastic (direct

materials) to produce 8000 units as opposed to 2017 when SOSI produced 8500 units

using 27,840 pounds of plastic. The type of plastic SOSI uses cost $5 per pound in 2016

and rose to $5.25 per pound in 2017. In comparing results for these two years, what

would be the cost effect of growth for the plastic material?

A) $8075 F

B) $8479 U

C) $8075 U

D) $10,000 U

For each of the following (actual real-world examples), develop products that can be

sold from the listed scrap.

a. The Federal Reserve Banks destroy old money. Burning this money is usually

forbidden under the environmental laws of most municipalities.

b. A manufacturer of cotton undergarments for prisoners has much cotton left over. The

manufacturer is located in a very rural area of Alabama.

c. A hog renderer has hog bristles as a result of the slaughtering process.

Which of the following reports to the CFO?

A) external auditor

B) distribution manager

C) production manager

D) treasurer

Serile Pharma places 800 units in production during the month of January. All 800 units

are completed during the month. It had no opening inventory. Direct material costs

added during January was $74,000 and conversion costs added during January was

$8400. What is the total cost per unit of the product produced during January?

A) $103

B) $10

C) $80

D) $93

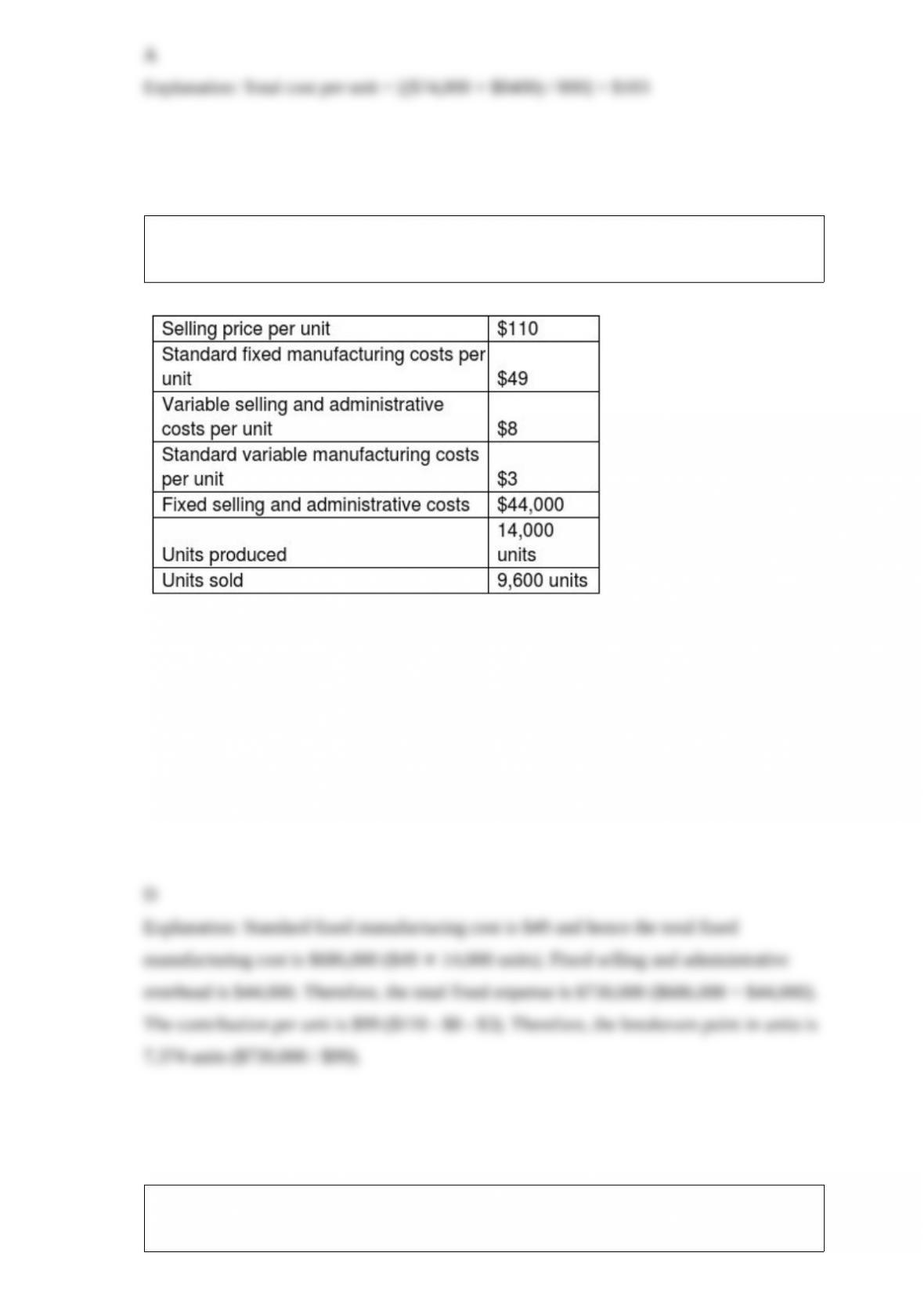

Jenkins Corporation sells one product. The following information is available for the

current month:

What is the variable costing breakeven point in units? (Round your final answer up to the

next whole unit.)

A) 6,930 units

B) 7,796 units

C) 7,157 units

D) 7,374 units

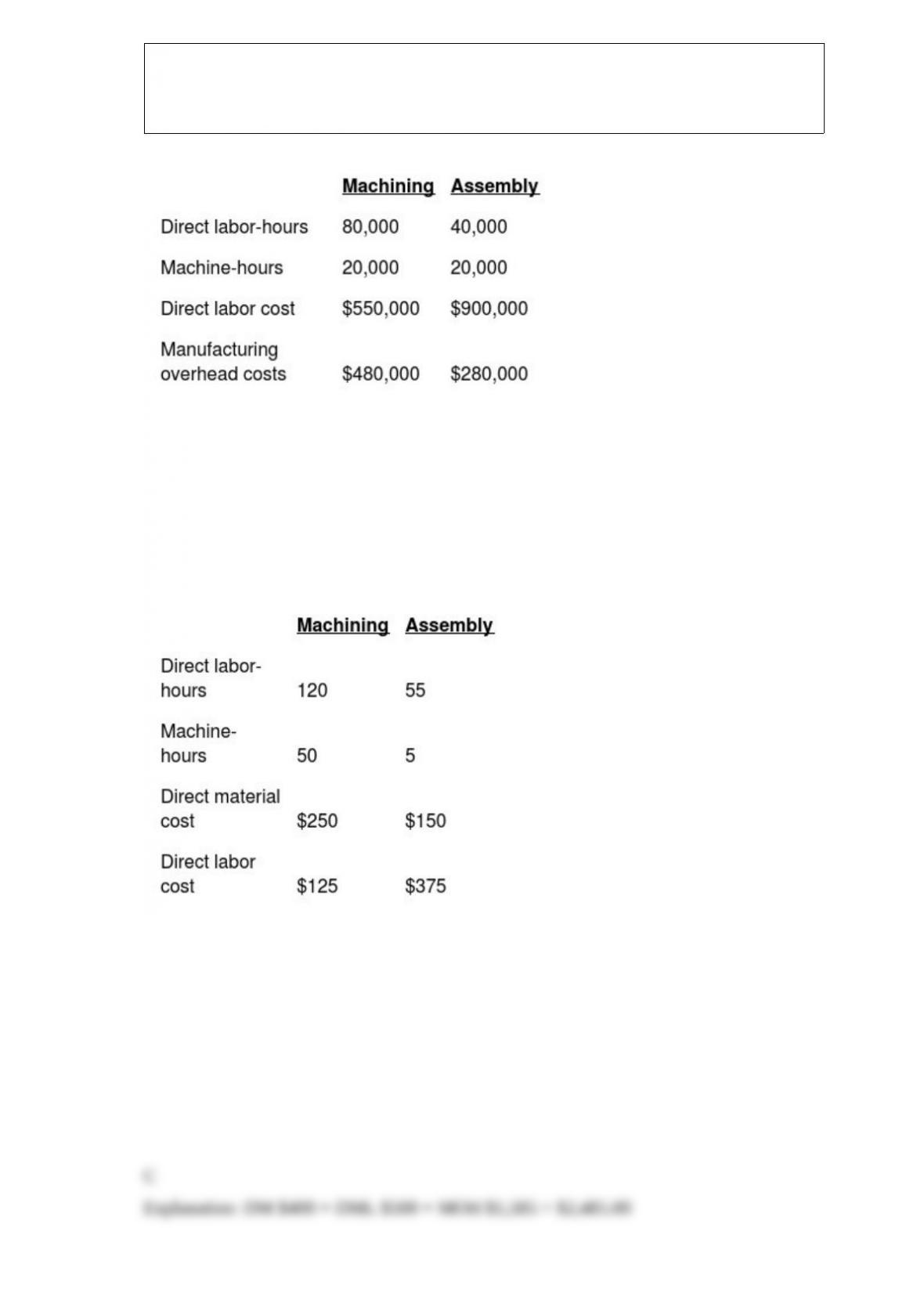

Bauer Manufacturing uses departmental cost driver rates to allocate manufacturing

overhead costs to products. Manufacturing overhead costs are allocated on the basis of

machine-hours in the Machining Department and on the basis of direct labor-hours in

the Assembly Department. At the beginning of 2018, the following estimates were

provided for the coming year:

The accounting records of the company show the following data for Job #316:

What are the total manufacturing costs of Job #316?

A) $1,885.00

B) $2,085.00

C) $2,485.00

D) $900.00

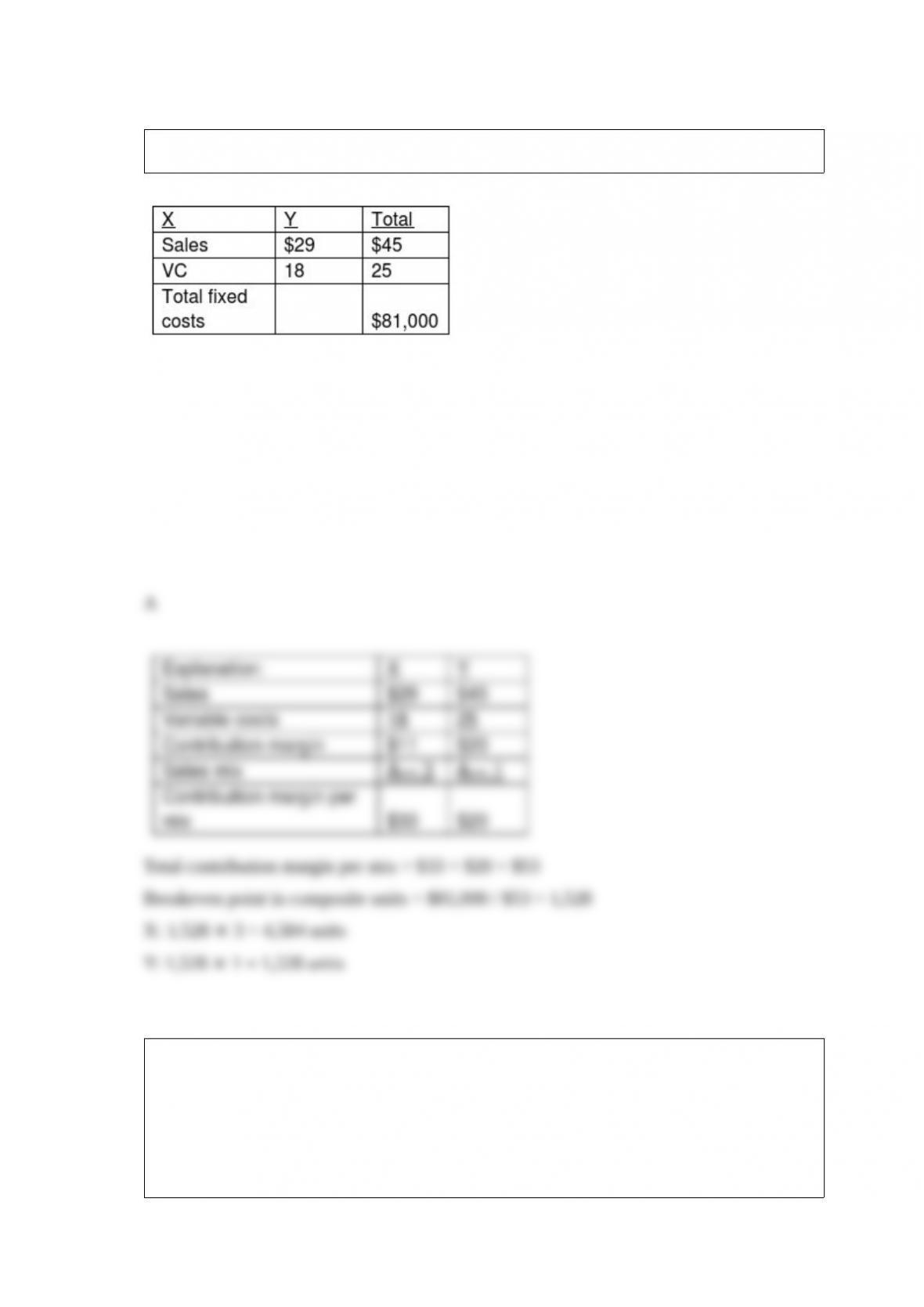

Assuming a constant mix of 3 units of X for every 1 unit of Y.

The breakeven point in units would be ________.

A) 4,584 units of X and 1,528 units of Y

B) 1,528 units of X and 1,528 units of Y

C) 3,056 units of X and 9,168 units of Y

D) 1,528 units of X and 4,584 units of Y

The ________ adjusts individual job-cost records to account for underallocated or

overallocated overhead.

A) adjusted allocation-rate

B) proration approach

C) write-off to cost of goods sold approach

D) weighted-average cost approach

For long-run pricing decisions, using stable prices has the advantage of ________.

A) minimizing the need to monitor competitor’s prices frequently

B) reducing the need to change cost structures frequently

C) reducing competition

D) helping to build buyer-seller relationships

The following information pertains to the January operating budget for Casey

Corporation.

∙ Budgeted sales for January $201,000 and February $101,000.

∙ Collections for sales are 40% in the month of sale and 60% the next month.

∙ Gross margin is 25% of sales.

∙ Administrative costs are $13,000 each month.

∙ Beginning accounts receivable is $25,000.

∙ Beginning inventory is $17,000.

∙ Beginning accounts payable is $73,000. (All from inventory purchases.)

∙ Purchases are paid in full the following month.

∙ Desired ending inventory is 25% of next month’s cost of goods sold (COGS).

For January, budgeted cash collections are ________.

A) $201,000

B) $105,400

C) $80,400

D) $25,000

Davis Company produced 159,000 sport jackets during 2015 and 530,000 direct

manufacturing labor-hours were used at $3 per hour. The conversion costs were $1.20

per jackets produced.

What is the total factor productivity for Davis Company?

A) 0.089 units of output per dollar

B) 0.300 units of output per dollar

C) 0.298 units of output per dollar

D) 2.500 units of output per dollar

Sail Safe currently sells motor boats for $60,000. It has costs of $46,500. A competitor

is bringing a new motor boat to the market that will sell for $55,000. Management

believes it must lower the price to $55,000 to compete in the market for motor boats.

The marketing department believes that the new price will cause sales to increase by

12.5%, even with a new competitor in the market. Sail Safe’s sales are currently 2,000

motor boats per year. 3

Required:

a. What is the target cost for the new target price if target operating income is 20% of

sales?

b. What is the change in operating income if marketing department is correct and only

the sales price is changed?

c. What is the target cost if the company wants to maintain its same income level, and

marketing department is correct?

Which of the following would be considered an example of an element of an informal

control system?

A) procedures developed by first level managers to help guide staff in their daily work

B) a policy that requires all employees to take at least two weeks of vacation each year

C) Shared values within an organization’s culture

D) the master budget

Which of the following capacity levels should a company choose, from a long-run

product costing perspective, to allocate budgeted fixed manufacturing costs to

products?

A) master-budget capacity utilization to highlight unused capacity

B) normal capacity utilization for benchmarking purposes

C) practical capacity for pricing decisions

D) theoretical capacity for performance evaluation

The management accountant aids in MRP by ________.

A) doing journal entries as requested

B) preparing plant appropriation requests

C) maintaining accurate records of inventory and its costs

D) contacting vendors to make sure they can deliver the materials in time

Process engineering is an example of ________.

A) prevention costs

B) appraisal costs

C) internal failure costs

D) external failure costs