SOLUTION

(2025 min.) Physical units, inspection at various stages of completion

Inspection Inspection Inspection

at 20% at 45% at 100%

Work in process, beginning (25%)*

Started during March

2,500

30 ,000

2,500

30 ,000

2,500

30 ,000

*Degree of completion for conversion costs at the dates of the work-in-process inventories

18-44 Weighted-average method, inspection at 80% completion. (A. Atkinson) The

Horsheim Company is a furniture manufacturer with two departments: molding and finishing.

The company uses the weighted-average method of process costing. In August, the following

data were recorded for the finishing department:

Units of beginning work-in-process inventory 25,000

Percentage completion of beginning work-in-process units 25%

Total costs added during current period:

18-=

Work in process, beginning:

Conversion costs are added evenly during the process. Direct material costs are added when

Required:

1. For August, summarize total costs to account for and assign these costs to units completed

and transferred out (including normal spoilage), to abnormal spoilage, and to units in ending

work in process.

2. What are the managerial issues involved in determining the percentage of spoilage

considered normal? How would your answer to requirement 1 differ if all spoilage were

treated as normal?

SOLUTION

(35 min.) Weighted-average method, inspection at 80% completion

The computation and allocation of spoilage is the most difficult part of this problem. The units in

the ending inventory have passed inspection. Therefore, of the 200,000 units to account for

Solution Exhibit 18-44, Panel A, calculates the equivalent units of work done for each

cost category. We comment on several points in this calculation:

Ending work in process includes an element of normal spoilage since all the ending

Spoilage includes no direct materials units because spoiled units are detected and

Direct materials units are included for ending work in process, which is 95%

18-=

Solution Exhibit 18-44, Panel B, summarizes total costs to account for, computes the costs

per equivalent unit for each cost category, and assigns costs to units completed (including

normal spoilage), to abnormal spoilage, and to units in ending work in process using the

weighted-average method. The cost of ending work in process includes the assignment of normal

spoilage costs since these units have passed the point of inspection. The costs assigned to each

cost category are as follows:

Cost of good units completed and transferred out

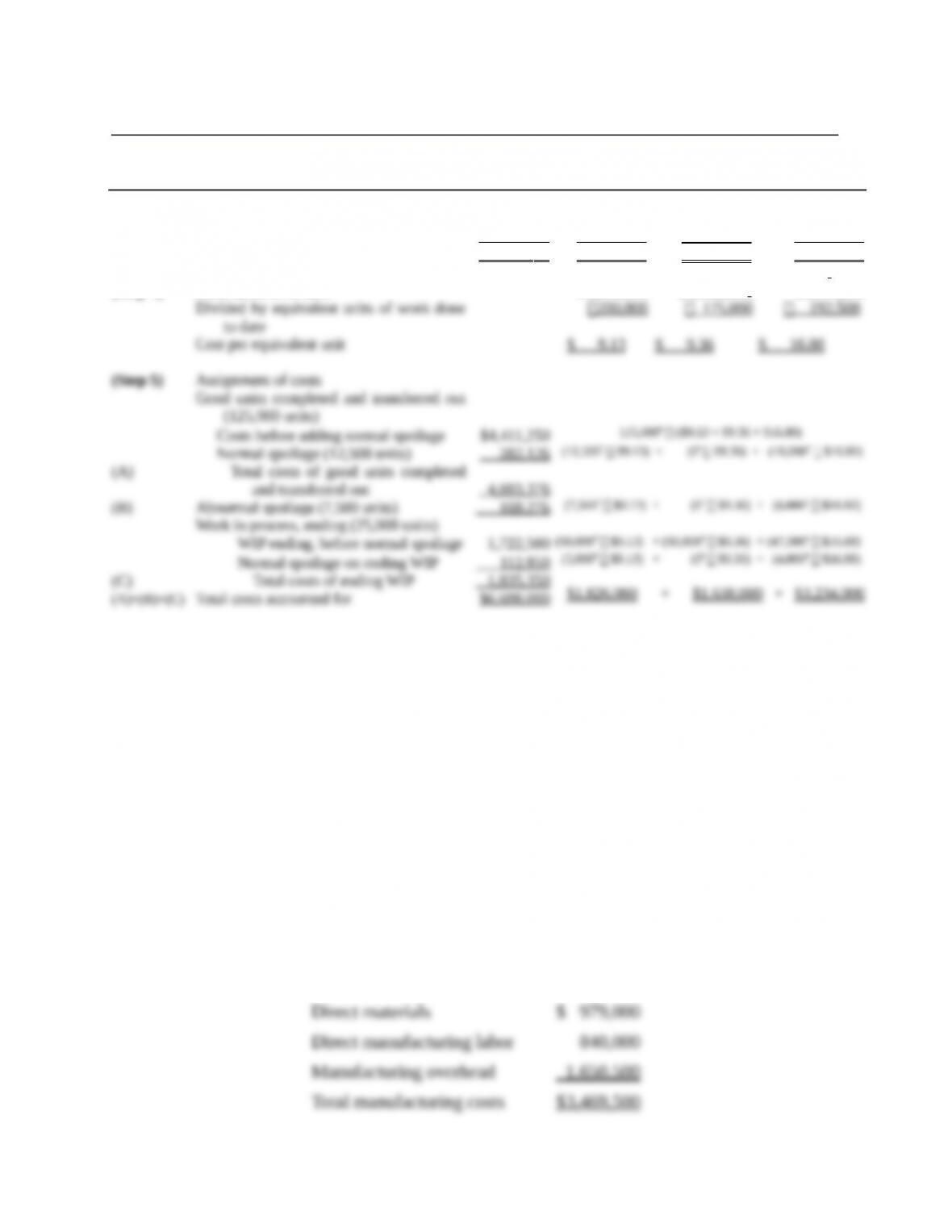

SOLUTION EXHIBIT 18-44

Weighted-Average Method of Process Costing with Spoilage,

Finishing Department of the Horsheim Company for August

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units

(Step 1) (Step 2)

Equivalent Units

Flow of Production

Physical

Units

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

To account for

25,000

175 ,0 00

20 0 ,000

PANEL B: Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit,

and Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process

Inventory

18-=

Total

Production

Costs

Transferred-

in Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

(Step 4) Costs incurred to date

$ 312,250

6 ,385,750

$ 6 ,698,0 00

$ 207,250

1 ,618,750

$1 ,826,0 00

$1,826,000

$

1 ,638,0 00

$1 ,638,0 00

$1,638,000

$ 105,000

3 , 129,0 00

$ 3 , 234,0 00

$3,234,000

(A)+(B)+(C) Total costs accounted for

$ 6 ,698,0 00

#Equivalent units of transferred-in costs, direct materials, and conversion costs calculated in Step 2 in Panel A.

18-45 Job costing, classifying spoilage, ethics. Flextron Company is a contract manufacturer

for a variety of pharmaceutical and over-the-counter products. It has a reputation for operational

excellence and boasts a normal spoilage rate of 2% of normal input. Normal spoilage is

recognized during the budgeting process and is classified as a component of manufacturing

overhead when determining the overhead rate.

Lynn Sanger, one of Flextron’s quality control managers, obtains the following information

for Job No. M102, an order from a consumer products company. The order was completed

recently, just before the close of Flextron’s fiscal year. The units will be delivered early in the

next accounting period. A total of 128,500 units were started, and 6,000 spoiled units were

rejected at final inspection, yielding 122,500 good units. Spoiled units were sold at $4 per unit.

Sanger indicates that all spoilage was related to this specific job.

The total costs for all 128,500 units of Job No. M102 follow. The job has been completed,

but the costs are yet to be transferred to Finished Goods.

18-=

Required:

1. Calculate the unit quantities of normal and abnormal spoilage.

2. Prepare the journal entries to account for Job No. M102, including spoilage, disposal of

spoiled units, and transfer of costs to the Finished Goods account.

3. Flextron’s controller, Vince Chadwick, tells Marta Suarez, the management accountant

responsible for Job No. M102, the following: “This was an unusual job. I think all 6,000

spoiled units should be considered normal.” Suarez knows that the work involved in Job No.

M102 was not uncommon and that Flextron’s normal spoilage rate of 2% is the appropriate

benchmark. She feels Chadwick made these comments because he wants to show a higher

operating income for the year.

a. Prepare journal entries, similar to requirement 2, to account for Job No. M102 if all

spoilage were considered normal. How will operating income be affected if all spoilage is

considered normal?

b. What should Suarez do in response to Chadwick’s comment?

SOLUTION

(40 min.) Job costing, classifying spoilage, ethics.

1. Analysis of the 6,000 units rejected by Flextron Company for Job No. M102 yields the

following breakdown between normal and abnormal spoilage.

Units

Normal spoilage* 2,500

2. The journal entries required to properly account for Job No. M102 are presented below

and use an average cost per unit of $27 ($3,469,500 ÷ 128,500).

18-=

To transfer 128,500 units to finished goods inventory (costs incurred on job and debited to WIP

Control, $3,469,500, minus $104,500 credited to WIP control).

1Units sold: 6,000 units at $4 each.

3a. If all spoilage were considered normal, the journal entries to account for Job No. M102

would be as follows:

To account for 6,000 units of normal spoilage, credited to WIP Control at $24,000

(6,000 units $4).

By considering all spoilage as normal, Flextron will show no abnormal loss of $80,500

3b. Incorrect reporting of spoilage as normal instead of abnormal with the goal of increasing

operating income is unethical. In assessing the situation, the management accountant should

consider the following:

Competence

Spoilage should be accounted for using relevant and reliable information. Accounting for

Integrity

The management accountant has a responsibility to avoid actual or apparent conflicts of interest

18-=

Objectivity

The management accountant’s standards of ethical conduct require that information should be

fairly and objectively communicated and that all relevant information should be disclosed. From

Suarez should indicate to Chadwick that the classification of normal and abnormal

Try It! 18-1

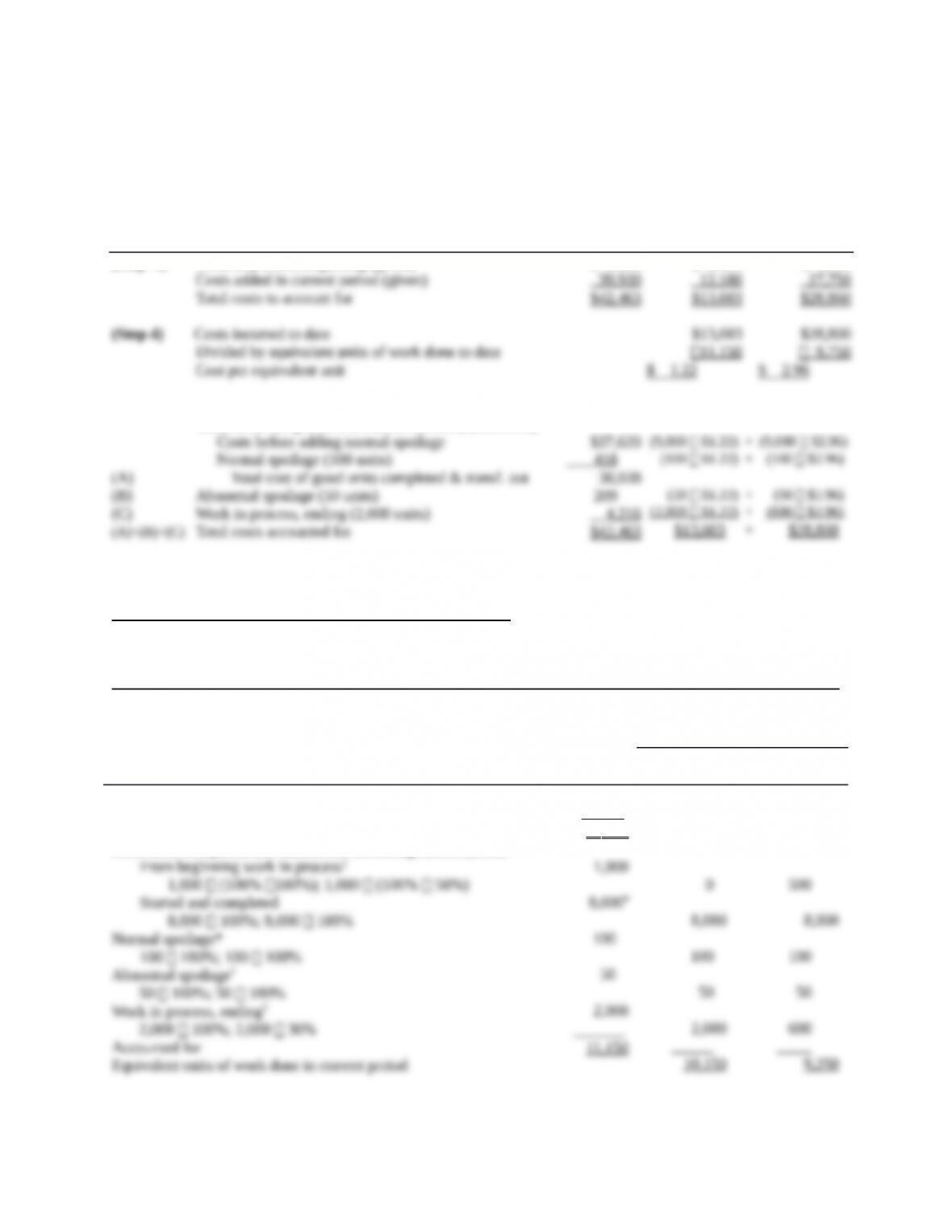

Weighted-Average Method of Process Costing:

Units started during July = 9,000 + 100 + 50 + 2,000 – 1,000 = 10,150

Summarize the Flow of Physical Units and Compute Output in Equivalent Units:

(Step 1) (Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period

To account for

Good units completed and transferred out

1,000

10 ,150

11 ,150

18-=

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign

Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process Inventory:

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

(Step 5) Assignment of costs

Good units completed and transferred out (9,000 units)

$ 2,533

$ 1,423

$ 1,110

Try It! 18-2

First-In, First-Out (FIFO) Method of Process Costing:

Summarize the Flow of Physical Units and Compute Output in Equivalent Units:

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period

To account for

Good units completed and transferred out during current period:

1,000

10 ,150a

11 ,150

||Degree of completion in this department: direct materials, 100%; conversion costs, 50%.

18-=

#9,000 physical units completed and transferred out minus 1,000 physical units completed and transferred out from

beginning work-in-process inventory.

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign

Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process Inventory:

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

$ 2,533

39 ,930

$42 ,463

$ 1,423

12 ,180

$13 ,603

$ 1,110

27 ,750

$28 ,860

Try It! 18-3

Inspection Inspection Inspection

at 15% at 40% at 100%

Work in process, beginning (20%)*

Started during March

To account for

14,000

120 ,000

134 ,000

14,000

120 ,000

134 ,000

14,000

120 ,000

134 ,000

*Degree of completion for conversion costs of the forging process at the dates of the work-in-process inventories

a14,000 beginning inventory +120,000 –10,000 spoiled – 11,000 ending inventory = 113,000

18-=

Try It! 18-4

a. Manufacturing Overhead Control (rework costs) 3,600

Normal rework on 50 units, but not attributable to any specific

controller

Loss from Abnormal Rework ($72 30) 2,160

Total costs of abnormal rework on 30 controllers

(Abnormal rework = Actual rework – Normal rework

= 80 – 50 = 30 controllers)

b. Total rework costs for controllers in August 2014 are as follows:

c. Manufacturing costs of job #9 before rework:

Manufacturing costs for 200 controllers on Job #9

Normal rework for 50 controllers attributable to Job #9

18-=