SOLUTION

(15-20 min.) Short-run pricing, capacity constraints.

1. Per pair of shorts:

Fabric (3 yards

´

$12 per yard)

If Fashion Fabrics can get all the fabric it needs and has sufficient production capacity, then the

minimum price it should charge per pair of shorts is the variable cost per pair of shorts = $36 +

$10 + $4 = $50 per pair of shorts.

2. If the fabric is in short supply, then the fabric used for 2 shorts displaces 1 pant (6 yards

of fabric per pant versus 3 yards of fabric per short).

We calculate the contribution margin per pair of pants = Selling price – Variable costs

aDirect materials, $72 + Variable direct manufacturing labor, $20 + Variable manufacturing

overhead, $8

´

That is, if fabric is in short supply, Fashion Fabrics should not agree to produce any shorts unless

the buyer is willing to pay at least $71 per pair of shorts.

11-<

11-36 International outsourcing. Riverside Clippers Corp manufactures garden tools in a

factory in Taneytown, Maryland. Recently, the company designed a collection of tools for

professional use rather than consumer use. Management needs to make a good decision about

whether to produce this line in their existing space in Maryland, where space is available or to

accept an offer from a manufacturer in Taiwan. Data concerning the decision are:

1. Should Riverside Clippers Corp manufacture the 800,000 garden tools in the Maryland

facility or purchase them from the supplier in Taiwan? Explain.

2. Riverside Clippers Corp believes that the U.S. dollar may weaken in the coming months

against the New Taiwanese Dollar and does not want to face any currency risk. Assume that

Riverside Clippers Corp can enter into a forward contract today to purchase 175 NTD for

$5.35. Should Riverside Clippers Corp manufacture the 800,000 garden tools in the

Maryland facility or purchase them from the Taiwan supplier? Explain.

3. What are some of the qualitative factors that Riverside Clippers Corp should consider when

deciding whether to outsource the garden tools manufacturing to Taiwan?

SOLUTION

(20 min.) International outsourcing.

1. Cost to purchase each tool from Taiwanese supplier =

175 NTD $5 .

35 NTD/$ =

Cost of purchasing 800,000 tools from Taiwanese supplier = $5 800,000 tools = $4,000,000

Costs of

11-<

2. If Riverside Clippers enters into a forward contract to purchase 175 NTDs for $5.35, each

tool acquired from the Taiwanese supplier will cost $5.35.

Riverside Clippers should manufacture the tools in Maryland because the relevant cost of

$4,200,000 to manufacture the tools in Maryland is less than the cost of $4,280,000 to enter into

the forward contract and purchase the tools from the Taiwanese supplier.

3. In deciding whether to purchase tools from the Taiwanese supplier, Riverside Clippers

should consider factors such as (a) quality, (b) delivery lead times, (c) fluctuations in the value of

the New Taiwanese Dollar (NTD) relative to the U.S. dollar, and (d) the negative public and

media reaction to not providing jobs in Maryland and instead supporting job creation in Taiwan.

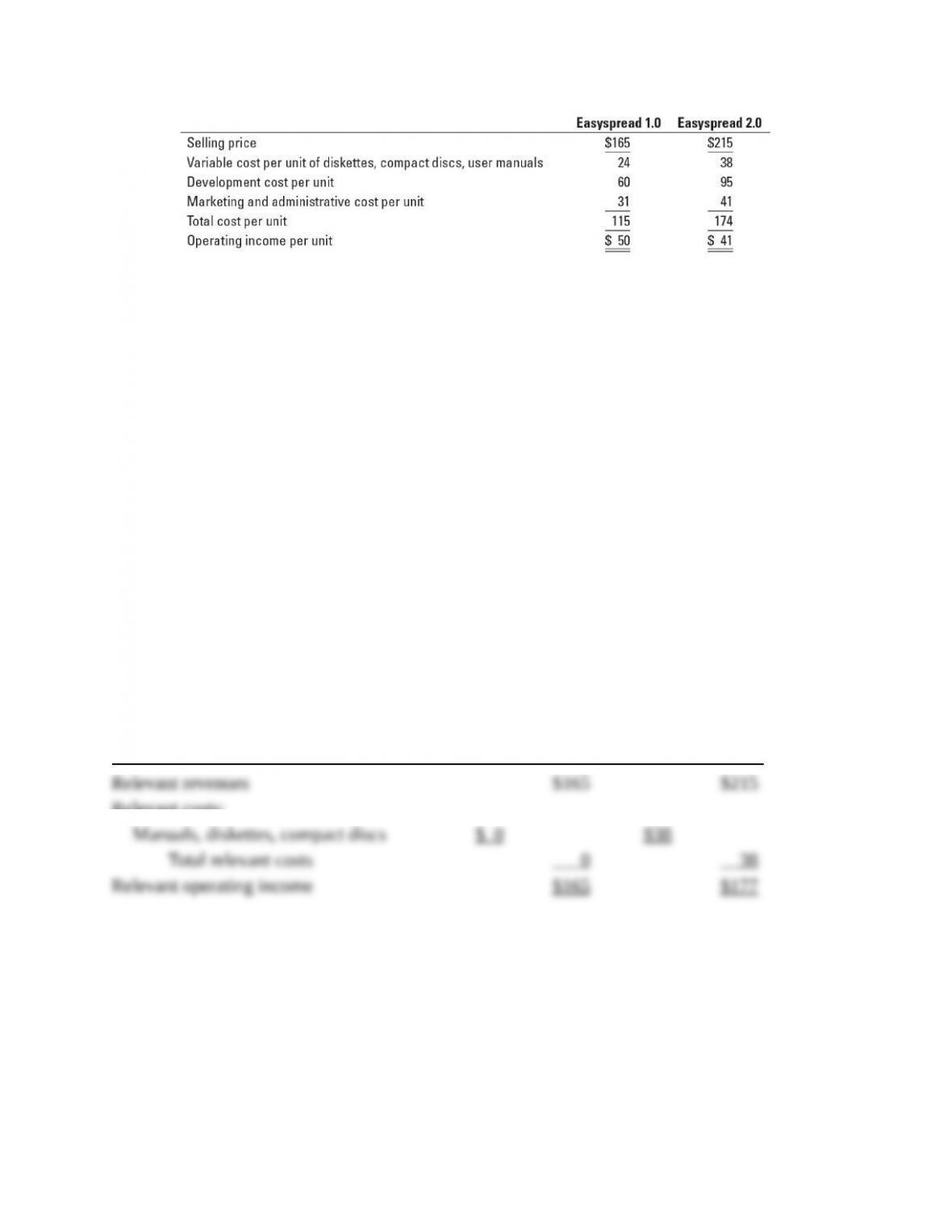

11-37 Relevant costs, opportunity costs. Gavin Martin, the general manager of Oregano

Software, must decide when to release the new version of Oregano’s spreadsheet package,

Easyspread 2.0. Development of Easyspread 2.0 is complete; however, the diskettes, compact

discs, and user manuals have not yet been produced. The product can be shipped starting July 1,

2017.

The major problem is that Oregano has overstocked the previous version of its

spreadsheet package, Easyspread 1.0. Martin knows that once Easyspread 2.0 is introduced,

Oregano will not be able to sell any more units of Easyspread 1.0. Rather than just throwing

away the inventory of Easyspread 1.0, Martin is wondering if it might be better to continue

to sell Easyspread 1.0 for the next three months and introduce Easyspread 2.0 on October 1,

2017, when the inventory of Easyspread 1.0 will be sold out.

The following information is available:

11-<

Development cost per unit for each product equals the total costs of developing the software

product divided by the anticipated unit sales over the life of the product. Marketing and

administrative costs are fixed costs in 2017, incurred to support all marketing and

administrative activities of Oregano Software. Marketing and administrative costs are

allocated to products on the basis of the budgeted revenues of each product. The preceding

unit costs assume Easyspread 2.0 will be introduced on October 1, 2017.

Required:

1. On the basis of financial considerations alone, should Martin introduce Easyspread 2.0 on

July 1, 2017, or wait until October 1, 2017? Show your calculations, clearly identifying

relevant and irrelevant revenues and costs.

2. What other factors might Gavin Martin consider in making a decision?

SOLUTION

(30 min.) Relevant costs, opportunity costs.

1. Easyspread 2.0 has a higher relevant operating income than Easyspread 1.0. Based on this

analysis, Easyspread 2.0 should be introduced immediately:

Easyspread 1.0 Easyspread 2.0

Relevant costs:

Reasons for other cost items being irrelevant are

Easyspread 1.0

Manuals, diskettes—already incurred

Development costs—already incurred

Marketing and administrative—fixed costs of period

11-<

Easyspread 2.0

Development costs—already incurred

Marketing and administration—fixed costs of period

Note that total marketing and administration costs will not change whether Easyspread 2.0 is

introduced on July 1, 2017, or on October 1, 2017.

2 2. Other factors to be considered:

a. Customer satisfaction. If 2.0 is significantly better than 1.0 for its customers, a

b. Quality level of Easyspread 2.0. It is critical for new software products to be fully

c. Importance of being perceived to be a market leader. Being first in the market with a

d. Morale of developers. These are key people at Oregano Software. Delaying

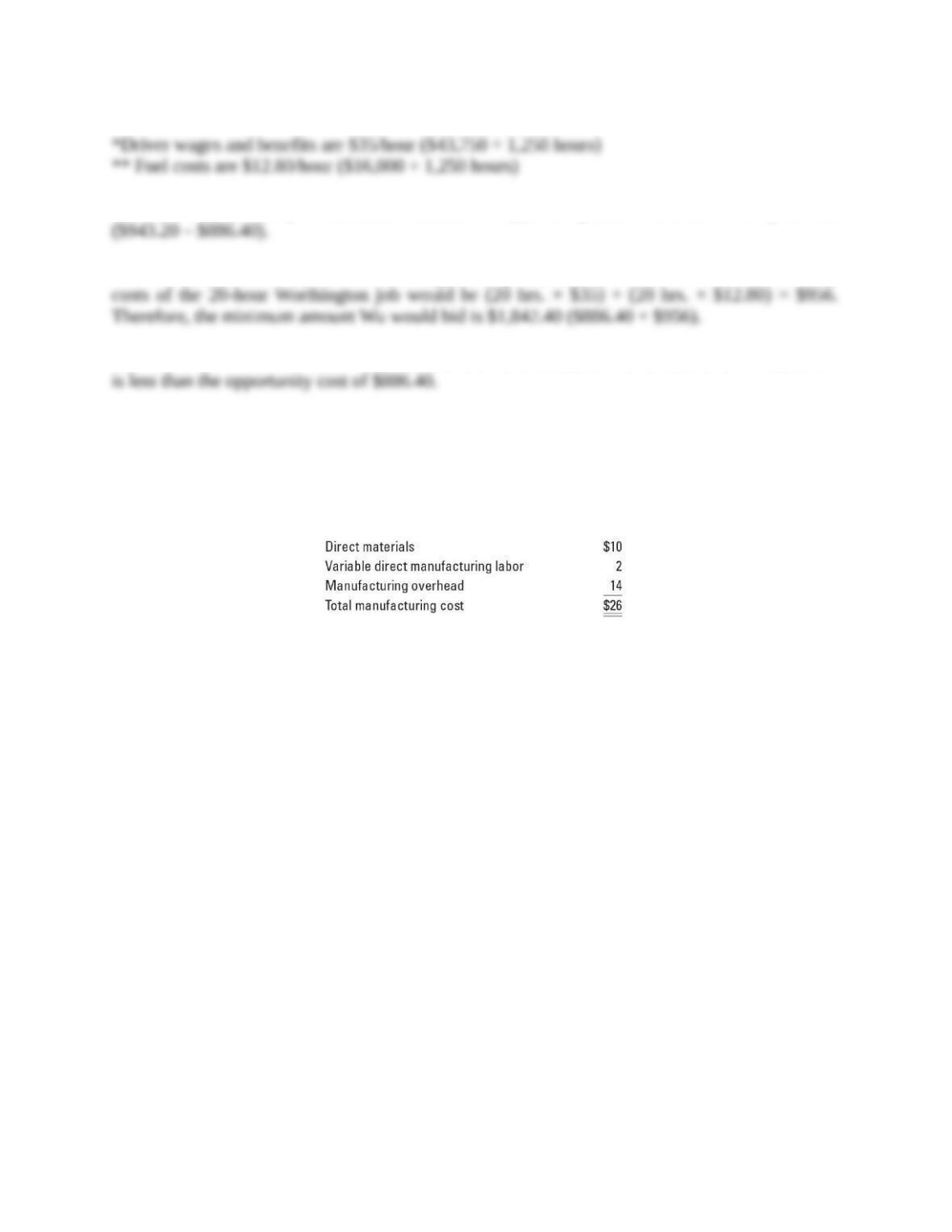

11-38 Opportunity costs and relevant costs. Jason Wu operates Exclusive Limousines, a fleet

of 10 limousines used for weddings, proms, and business events in Washington, D.C. Wu charges

customers a flat fee of $250 per car taken on contract plus an hourly fee of $80. His income

statement for May follows:

11-<

All expenses are fixed, with the exception of driver wages and benefits and fuel costs, which are both

variable per hour. During May, the company’s limousines were fully booked. In June, Wu expects

that Exclusive Limousines will be operating near capacity. Shelly Worthington, a prominent

Washington socialite, has asked Wu to bid on a large charity event she is hosting in late June. The

limousine company she had hired has canceled at the last minute, and she needs the service of five

limousines for four hours each. She will only hire Exclusive Limousines if they take the entire job.

Wu checks his schedule and finds that he only has three limousines available that day.

Required:

1. If Wu accepts the contract with Worthington, he would either have to (a) cancel two prom

contracts each for one car for six hours or (b) cancel one business event for three cars

contracted for two hours each. What are the relevant opportunity costs of accepting the

Worthington contract in each case? Which contract should he cancel?

2. Wu would like to win the bid on the Worthington job because of the potential for lucrative

future business. Assume that Wu cancels the contract in requirement 1 with the lowest

opportunity cost, and assume that the three currently available cars would go unrented if the

company does not win the bid. What is the lowest amount he should bid on the Worthington

job?

3. Another limousine company has offered to rent Exclusive Limousines two additional cars for

$300 each per day. Wu would still need to pay for fuel and driver wages on these cars for the

Worthington job. Should Wu rent the two cars to avoid canceling either of the other two

contracts?

SOLUTION

(30 min.) Opportunity costs and relevant costs

1. If Wu cancels the two prom contracts, the opportunity cost of accepting the Worthington job

would be $886.40, as follows:

Less variable costs

If Wu cancels the business event contract, the opportunity cost would be $943.20, as

follows:

Less variable costs

11-<

Wu should cancel the prom contracts because the opportunity cost would be lower by $56.80

2. If Wu cancels the two prom contracts, opportunity cost equals $886.40. In addition, variable

3. Yes, it would be in Wu’s best interest to lease the additional cars for a total of $600 because it

11-39 Opportunity costs. (H. Schaefer, adapted) The Wild Orchid Corporation is working at full

production capacity producing 13,000 units of a unique product, Everlast. Manufacturing cost per

unit for Everlast is:

Manufacturing overhead cost per unit is based on variable cost per unit of $8 and fixed costs of

$78,000 (at full capacity of 13,000 units). Marketing cost per unit, all variable, is $4, and the

selling price is $52.

A customer, the Apex Company, has asked Wild Orchid to produce 3,500 units of Stronglast,

a modification of Everlast. Stronglast would require the same manufacturing processes as

Everlast. Apex has offered to pay Wild Orchid $40 for a unit of Stronglast and share half of the

marketing cost per unit.

Required:

1. What is the opportunity cost to Wild Orchid of producing the 3,500 units of Stronglast?

(Assume that no overtime is worked.)

2. The Chesapeake Corporation has offered to produce 3,500 units of Everlast for Wild Orchid

so that Wild Orchid may accept the Apex offer. That is, if Wild Orchid accepts the

Chesapeake offer, Wild Orchid would manufacture 9,500 units of Everlast and 3,500 units of

Stronglast and purchase 3,500 units of Everlast from Chesapeake. Chesapeake would charge

Wild Orchid $36 per unit to manufacture Everlast. On the basis of financial considerations

alone, should Wild Orchid accept the Chesapeake offer? Show your calculations.

3. Suppose Wild Orchid had been working at less than full capacity, producing 9,500 units of

Everlast, at the time the Apex offer was made. Calculate the minimum price Wild Orchid

should accept for Stronglast under these conditions. (Ignore the previous $40 selling price.)

11-<

SOLUTION

(20 min.) Opportunity costs.

1. The opportunity cost to Wild Orchid of producing the 3,500 units of Stronglast is the

contribution margin lost on the 3,500 units of Everlast that would have to be forgone, as

computed below:

2. Contribution margin from manufacturing 3,500 units of Stronglast and purchasing 3,500

units of Everlast from Chesapeake is $105,000, as follows:

Manufacture

Stronglast

Purchase

Everlast Total

Selling price

Variable costs per unit:

Purchase costs

$ 40

–

$ 52

36

As calculated in requirement 1, Wild Orchid’s contribution margin from continuing to

manufacture 3,500 units of Everlast is $98,000. Accepting the Apex Company and Chesapeake

3. The minimum price would be any price greater than $22, the sum of the incremental costs

of manufacturing and marketing Stronglast as computed in requirement 2. This follows because,

if Wild Orchid has surplus capacity, the opportunity cost = $0. For the short-run decision of

11-<

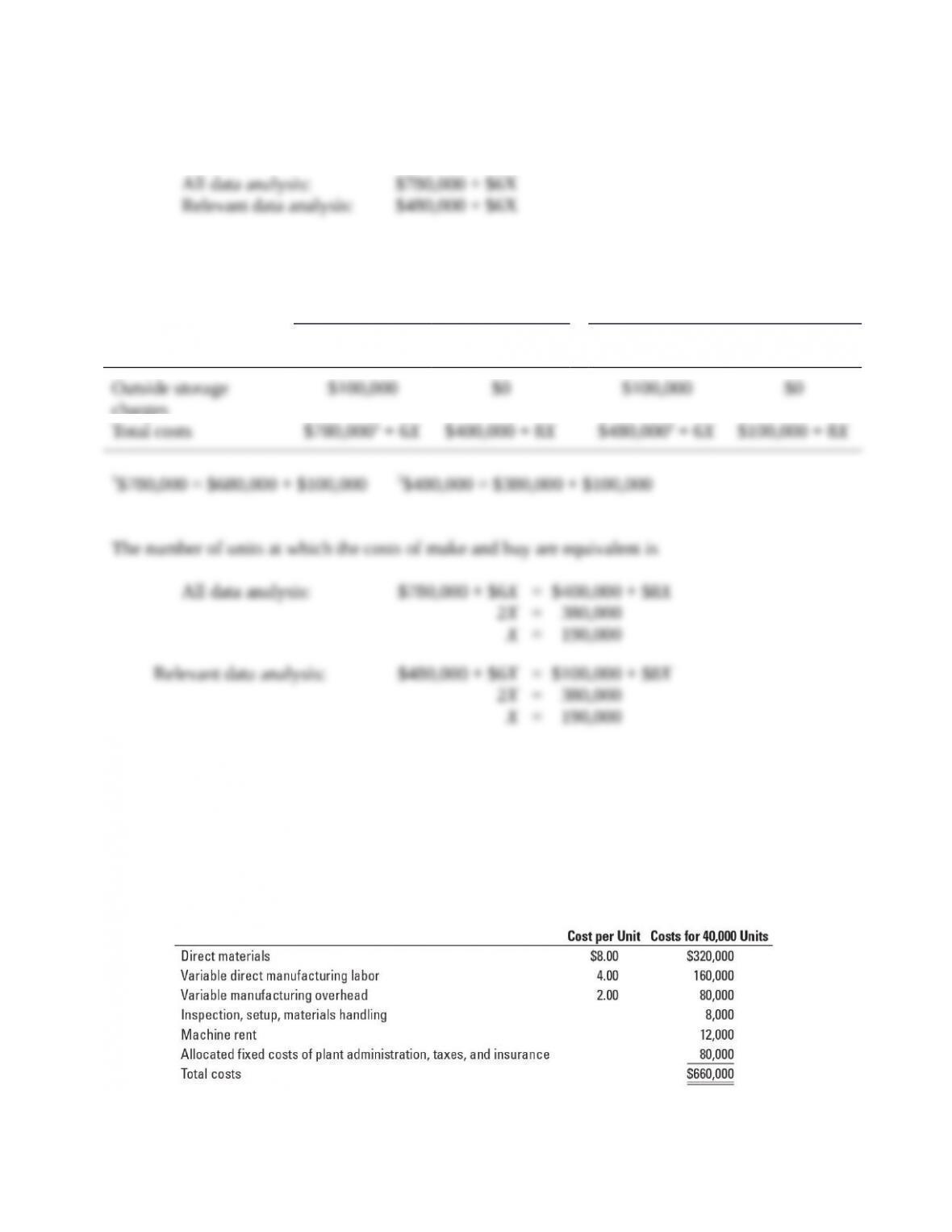

11-40 Make or buy, unknown level of volume. (A. Atkinson, adapted) Denver Engineering

manufactures small engines that it sells to manufacturers who install them in products such as

lawn mowers. The company currently manufactures all the parts used in these engines but is

considering a proposal from an external supplier who wishes to supply the starter assemblies

used in these engines.

The starter assemblies are currently manufactured in Division 3 of Denver Engineering. The

costs relating to the starter assemblies for the past 12 months were as follows:

Over the past year, Division 3 manufactured 150,000 starter assemblies. The average cost for

each starter assembly is $10 ($1,500,000 150,000).

Further analysis of manufacturing overhead revealed the following information. Of the total

manufacturing overhead, only 25% is considered variable. Of the fixed portion, $300,000 is an

allocation of general overhead that will remain unchanged for the company as a whole if

production of the starter assemblies is discontinued. A further $200,000 of the fixed overhead is

avoidable if production of the starter assemblies is discontinued. The balance of the current fixed

overhead, $100,000, is the division manager’s salary. If Denver Engineering discontinues

production of the starter assemblies, the manager of Division 3 will be transferred to Division 2

at the same salary. This move will allow the company to save the $80,000 salary that would

otherwise be paid to attract an outsider to this position.

Required:

1. Tutwiler Electronics, a reliable supplier, has offered to supply starter-assembly units at $8 per

unit. Because this price is less than the current average cost of $10 per unit, the vice president

of manufacturing is eager to accept this offer. On the basis of financial considerations alone,

should Denver Engineering accept the outside offer? Show your calculations. (Hint:

Production output in the coming year may be different from production output in the past

year.)

2. How, if at all, would your response to requirement 1 change if the company could use the

vacated plant space for storage and, in so doing, avoid $100,000 of outside storage charges

currently incurred? Why is this information relevant or irrelevant?

SOLUTION

(30–40 min.) Make or buy, unknown level of volume.

1. The variable costs required to manufacture 150,000 starter assemblies are

11-<

All Data Relevant Data

Alternative

1:

Make

Alternative

2:

Buy

Alternative

1:

Make

Alternative

2: Buy

Variable manufacturing costs

$ 6X

–

$ 6X

–

The number of units at which the costs of make and buy are equivalent is

Assuming cost minimization is the objective, then

• If production is expected to be less than 140,000 units, it is preferable to buy units

from Tutwiler.

• If production is expected to exceed 140,000 units, it is preferable to manufacture

2. The information on the storage cost, which is avoidable if self-manufacture is

discontinued, is relevant; these storage charges represent current outlays that are avoidable if

self-manufacture is discontinued. Assume these $100,000 charges are represented as an

11-<

opportunity cost of the make alternative. The costs of internal manufacture that incorporate this

$100,000 opportunity cost are

Alternatively stated, we would add the following line to the table shown in requirement 1

causing the total costs line to change as follows:

All Data Relevant Data

Alternative 1: Alternative 2: Alternative 1: Alternative 2:

Make Buy Make Buy

If production is expected to be less than 190,000, it is preferable to buy units from Tutwiler. If

production is expected to exceed 190,000, it is preferable to manufacture the units internally.

11-41 Make versus buy, activity-based costing, opportunity costs. The Lexington Company

produces gas grills. This year’s expected production is 20,000 units. Currently, Lexington makes

the side burners for its grills. Each grill includes two side burners. Lexington’s management

accountant reports the following costs for making the 40,000 burners:

11-<

Lexington has received an offer from an outside vendor to supply any number of burners

Lexington requires at $14.80 per burner. The following additional information is available:

a. Inspection, setup, and materials-handling costs vary with the number of batches in which the

burners are produced. Lexington produces burners in batch sizes of 1,000 units. Lexington

will produce the 40,000 units in 40 batches.

b. Lexington rents the machine it uses to make the burners. If Lexington buys all of its burners

from the outside vendor, it does not need to pay rent on this machine.

Required:

1. Assume that if Lexington purchases the burners from the outside vendor, the facility where

the burners are currently made will remain idle. On the basis of financial considerations

alone, should Lexington accept the outside vendor’s offer at the anticipated volume of 40,000

burners? Show your calculations.

2For this question, assume that if the burners are purchased outside, the facilities where the

burners are currently made will be used to upgrade the grills by adding a rotisserie

attachment. (Note: Each grill contains two burners and one rotisserie attachment.) As a

consequence, the selling price of grills will be raised by $48. The variable cost per unit of the

upgrade would be $38, and additional tooling costs of $160,000 per year would be incurred.

On the basis of financial considerations alone, should Lexington make or buy the burners,

assuming that 20,000 grills are produced (and sold)? Show your calculations.

3. The sales manager at Lexington is concerned that the estimate of 20,000 grills may be high

and believes that only 16,000 grills will be sold. Production will be cut back, freeing up work

space. This space can be used to add the rotisserie attachments whether Lexington buys the

burners or makes them in-house. At this lower output, Lexington will produce the burners in

32 batches of 1,000 units each. On the basis of financial considerations alone, should

Lexington purchase the burners from the outside vendor? Show your calculations.

11-<