SOLUTION

(20 min.) Activity-based costing, batch-level variance analysis

1. Static budget number of crates = Budgeted pairs shipped / Budgeted pairs per crate

2. Flexible budget number of crates = Actual pairs shipped / Budgeted pairs per crate

3. Actual number of crates shipped = Actual pairs shipped / Actual pairs per box

4. Static budget number of hours = Static budget number of crates × budgeted hours per box

Fixed overhead rate = Static budget fixed overhead / static budget number of hours

5. Variable Direct Variance Analysis for Audrina’s Fleet Feet, Inc. for 2017

Actual Actual hours Budgeted hours allowed for

Variable Cost x Budgeted rate Actual output x Budgeted rate

Price variance Efficiency variance

6. Fixed Overhead Variance Analysis for Audrina’s Fleet Feet, Inc. for 2017

Actual Static Budget Budgeted hours allowed for

Fixed Overhead Fixed Overhead Actual output × Budgeted Rate

(12,000 × 0.9 × $4.0)

Spending variance Production volume variance

8-41 Overhead variances and sales-volume variance. The Roller Bag Company manufactures

extremely light and rolling suitcases. It was one of the first companies to produce rolling

suitcases and sales have increased for the past several years. In 2017, Roller Bag budgeted to sell

150,000 suitcases for $80 each.

The budgeted standard machine hours for production in 2017 were 375,000 machine hours.

Budgeted fixed overhead costs are $525,000, and variable overhead cost was budgeted at $1.75

per machine-hour.

In 2017, Roller Bag experienced a drop in sales due to increased competition for rolling

suitcases. Roller Bag used 310,000 machine-hours to produce the 120,000 suitcases it sold in

2017. Actual variable overhead costs were $488,000 and actual fixed overhead costs were

$532,400. The average selling price of the suitcases sold in 2017 was $72.

Actual direct materials and direct labor costs were the same as standard costs, which were

$20 per unit and $18 per unit, respectively.

Required:

1. Calculate the variable overhead and fixed overhead variances (spending, efficiency,

spending, and volume).

2. Create a chart like that in Exhibit 7-2 showing Flexible Budget Variances and Sales-Volume

Variances for revenues, costs, contribution margin, and operating income.

3. Calculate the operating income based on budgeted profit per suitcase.

4. Reconcile the budgeted operating income from requirement 3 to the actual operating income

from your chart in requirement 2.

5. Calculate the operating income volume variance and show how the sales-volume variance is

composed of the production-volume variance and the operating income volume variance.

SOLUTION

(30 – 40 minutes) Overhead variances and sales volume variance

1. Variable overhead variances:

Actual Actual Hours Standard Hours

Variable Overhead × Budgeted Rate × Standard Rate

(310,000 × $1.75) (120,000 × 2.5 × $1.75)

$488,000 $542,500 $525,000

Spending variance Efficiency variance

Fixed overhead variances:

Actual Static Budget Standard Hours

Fixed Overhead Fixed Overhead × Budgeted Rate

(120,000 × 2.5 × $1.40*)

Spending variance Production-volume variance

2.

Actual

Results

(1)

Flexible-Bu

dget

Variances

(2) = (1) –

(3)

Flexible

Budget

(3)

Sales-Volum

e

Variances

(4) = (3) –

(5)

Static

Budget

(5)

Units sold 120,000 120,000 150,000

Unit price $72 $80 $80

Variable costs

3. Budgeted cost per rolling suitcase:

Direct materials per bag (given) $20.00

Direct labor per bag (given) 18.00

Budgeted sales revenue, 120,000 actual units sold

Budgeted Cost of Goods sold

4. Budgeted operating income (from #3) $4,095,000

5. Operating income volume variance:

Budgeted operating income for actual output – static budget operating income

Sales volume variance

8-42 Activity-based costing, batch-level variance analysis. The Saluki Company specializes in

making fraternity and sorority T-shirts for the college market. Due to the high setup costs for

each batch printed, Saluki holds the T-shirt requests until demand is approximately 100 shirts. At

that point Saluki will schedule the setup and production of the shirts. For rush orders, Saluki will

produce smaller batches for an additional charge of $175 per setup.

Budgeted and actual costs for the production process for 2017 were as follows:

Static-Budget

Amounts

Actual

Results

Number of shirts produced 125,000 114,000

Average number of shirts

per setup

100 95

Hours to set up machines 5 5.20

Direct variable cost per

setup-hour

$ 30 $ 32

Total fixed setup overhead

costs

$56,250 $56,000

Required:

1. What is the static budget number of setups for 2017?

2. What is the flexible-budget number of setups for 2017?

3. What is the actual number of setups in 2017?

4. Assuming fixed setup overhead costs are allocated using setup-hours, what is the

predetermined fixed setup overhead allocation rate?

5. Does Saluki’s charge of $175 cover the budgeted direct variable cost of an order? The budgeted

total cost?

6. For direct variable setup costs, compute the price and efficiency variances.

7. For fixed setup overhead costs, compute the spending and the production-volume variances.

8. What qualitative factors should Saluki consider before accepting or rejecting a special order?

SOLUTION

(30 min.) Activity-based costing, batch-level variance analysis

1. Static budget number of setups = Budgeted shirts produced/ Budgeted shirts per setup

2. Flexible budget number of setups = Actual shirts produced / Budgeted shirts per setup

3. Actual number of setups = Actual shirts produced / Actual shirts per setup

4. Static budget number of hours = Static budget # of setups × Budgeted hours per setup

Fixed overhead rate = Static budget fixed overhead / Static budget number of hours

= $56,250/6,250 = $9 per hour

5. Budgeted direct variable cost of a setup

= Budgeted variable cost per setup-hour × Budgeted number of setup-hours

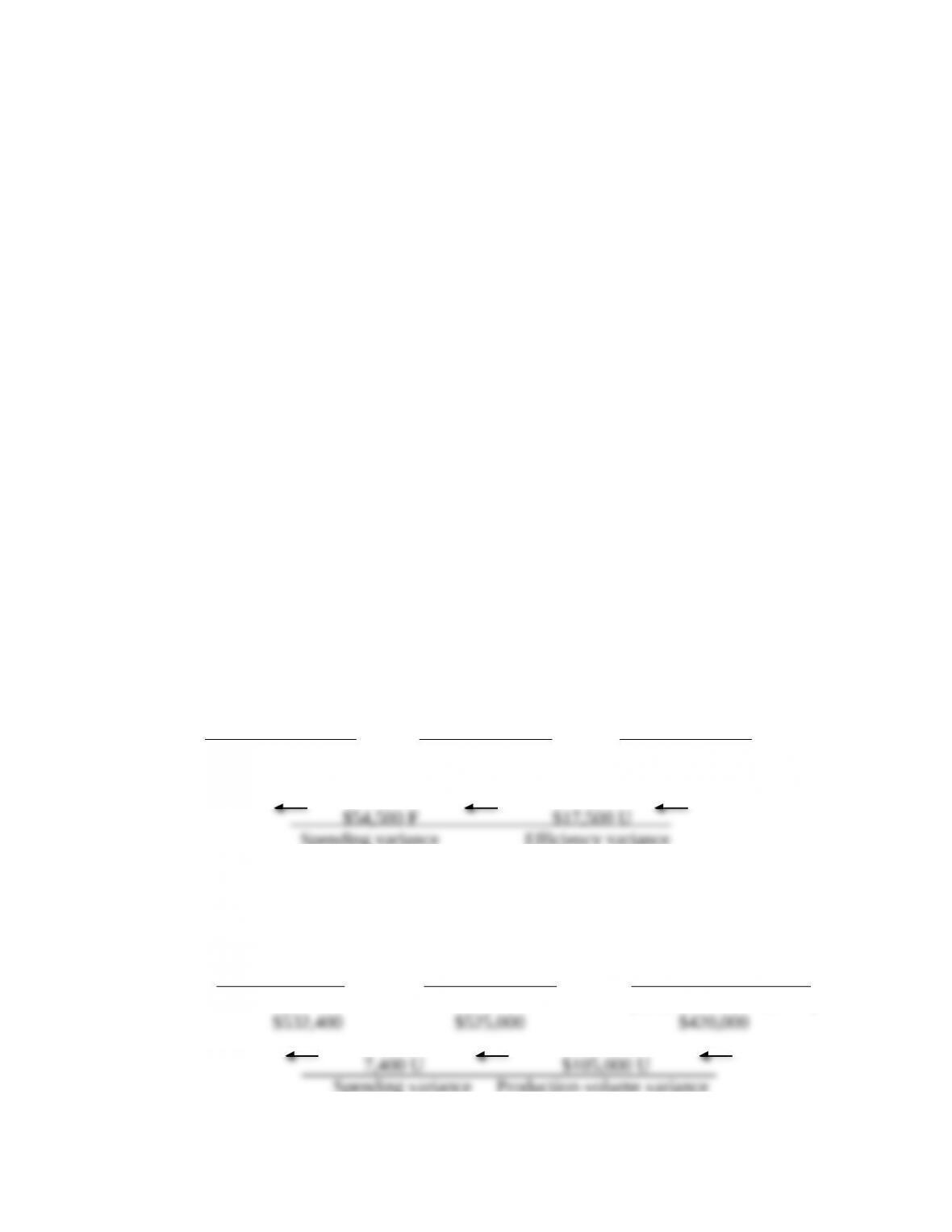

6. Direct Variable Variance Analysis for Saluki Company for 2017

Actual Actual hours Standard hours

Variable Cost x Budgeted rate x Standard rate

7. Fixed Setup Overhead Variance Analysis for Saluki Company for 2017

Actual Static Budget Standard hours

Fixed Overhead Fixed Overhead x Budgeted Rate

(1,140 × 5.0 × $9)

$56,000 $56,250 $51,300

8. Rejecting an order may have implications for future orders (i.e., groups might be

reluctant to order shirts from this supplier again). Saluki should consider factors such as

prior history with the customer and potential future sales.

8-43 Comprehensive review of Chapters 7 and 8, working backward from given variances.

The Gallo Company uses a flexible budget and standard costs to aid planning and control of its

machining manufacturing operations. Its costing system for manufacturing has two direct-cost

categories (direct materials and direct manufacturing labor—both variable) and two

overhead-cost categories (variable manufacturing overhead and fixed manufacturing overhead,

both allocated using direct manufacturing labor-hours).

At the 50,000 budgeted direct manufacturing labor-hour level for August, budgeted direct

manufacturing labor is $1,250,000, budgeted variable manufacturing overhead is $500,000, and

budgeted fixed manufacturing overhead is $1,000,000.

The following actual results are for August:

Direct materials price variance (based on

purchases)

$179,300 F

Direct materials efficiency variance 75,900 U

Direct manufacturing labor costs incurred 535,500

Variable manufacturing overhead

flexible-budget variance

10,400 U

Variable manufacturing overhead efficiency

variance

18,100 U

Fixed manufacturing overhead incurred 957,550

The standard cost per pound of direct materials is $11.50. The standard allowance is 6 pounds of

direct materials for each unit of product. During August, 20,000 units of product were produced.

There was no beginning inventory of direct materials. There was no beginning or ending work in

process. In August, the direct materials price variance was $1.10 per pound.

In July, labor unrest caused a major slowdown in the pace of production, resulting in an

unfavorable direct manufacturing labor efficiency variance of $40,000. There was no direct

manufacturing labor price variance. Labor unrest persisted into August. Some workers quit. Their

replacements had to be hired at higher wage rates, which had to be extended to all workers. The

actual average wage rate in August exceeded the standard average wage rate by $0.50 per hour.

Required:

1. Compute the following for August:

a. Total pounds of direct materials purchased

b. Total number of pounds of excess direct materials used

c. Variable manufacturing overhead spending variance

d. Total number of actual direct manufacturing labor-hours used

e. Total number of standard direct manufacturing labor-hours allowed for the units produced

f. Production-volume variance

2. Describe how Gallo’s control of variable manufacturing overhead items differs from its

control of fixed manufacturing overhead items.

SOLUTION

(3040 min.) Comprehensive review of Chapters 7 and 8, working backward from given

variances.

1. Solution Exhibit 8-43 outlines the Chapter 7 and 8 framework underlying this solution.

a. Pounds of direct materials purchased = $179,300 ÷ $1.10 = 163,000 pounds

e. Standard variable manufacturing overhead rate = $500,000 ÷ 50,000

= $10 per direct manuf. labor-hour

f. Budgeted fixed manufacturing overhead rate = $1,000,000 ÷ 50,000 hours

1. The control of variable manufacturing overhead requires the identification of the cost drivers

for such items as energy, supplies, and repairs. Control often entails monitoring nonfinancial

SOLUTION EXHIBIT 8-43

Actual Costs

Incurred

(Actual Input Qty.

Actual Rate)

Actual Input Qty.

Budgeted Rate

Purchases Usage

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

Budgeted Rate

Labor

Actual Costs

Incurred

Actual Input Qty.

Actual Rate

Actual Input Qty.

Budgeted Rate

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

Budgeted Rate

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

Budgeted Rate

Actual Costs

Incurred

(1)

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(2)

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

Fixed

50,000 × $20

19,190× $20

$179,300 F

Price variance

$75,900 U

Efficiency variance

$10,500 U

Price variance

$55,750 U

Efficiency variance

$66,250 U

Flexible-budget variance

Spending variance

Efficiency

variance

Never a variance

Flexible-budget variance Never a variance

8-44 Review of Chapters 7 and 8, 3-variance analysis. (CPA, adapted) The Beal

Manufacturing Company’s costing system has two direct-cost categories: direct materials and

direct manufacturing labor. Manufacturing overhead (both variable and fixed) is allocated to

products on the basis of standard direct manufacturing labor-hours (DLH). At the beginning of

2017, Beal adopted the following standards for its manufacturing costs:

Input Cost per Output

Unit

Direct materials 5 lb. at $4 per lb. $ 20.00

Direct manufacturing labor 4 hrs. at $16 per hr. 64.00

Manufacturing overhead:

Variable $8 per DLH 32.00

Fixed $9 per DLH 36.00

Standard manufacturing cost per

output unit

$152.00

The denominator level for total manufacturing overhead per month in 2017 is 37,000 direct

manufacturing labor-hours. Beal’s budget for January 2017 was based on this denominator level.

The records for January indicated the following:

Direct materials purchased 40,300 lb. at $3.80 per lb.

Direct materials used 37,300 lb.

Direct manufacturing labor 31,400 hrs. at $16.25 per hr.

Total actual manufacturing overhead (variable and

fixed)

$650,000

Actual production 7,600 output units

Required:

1. Prepare a schedule of total standard manufacturing costs for the 7,600 output units in January

2017.

2. For the month of January 2017, compute the following variances, indicating whether each is

favorable (F) or unfavorable (U):

a. Direct materials price variance, based on purchases

b. Direct materials efficiency variance

c. Direct manufacturing labor price variance

d. Direct manufacturing labor efficiency variance

e. Total manufacturing overhead spending variance

f. Variable manufacturing overhead efficiency variance

g. Production-volume variance