A locked-in cost is a(n) ________.

A) opportunity cost that is fixed in the short run

B) cost that can be changed in the short run

C) cost that has not yet been incurred, but based on decisions that have already been

made, will be incurred in the future

D) cost that has been incurred, but based on decisions that have already been made, will

be not incurred in the future

Which of the following statements is true of a backflush costing system?

A) All costs are tracked sequentially as products pass through each stage of production.

B) When inventories are minimal, as in JIT production systems, backflush costing

complicates costing systems.

C) Usage of a backflush costing system does not satisfy the absorption costing rules of

GAAP

D) Backflush costing increases the ability of the accounting system to pinpoint the uses

of resources at each step in the production process.

Freetown Corporation incurred fixed manufacturing costs of $26,000 during 2017.

Other information for 2017 includes:

The budgeted denominator level is 2,600 units.

Units produced total 1,800 units.

Units sold total 1,200 units.

Beginning inventory was zero.

The company uses absorption costing and the fixed manufacturing cost rate is based on

the budgeted denominator level. Manufacturing variances are closed to cost of goods

sold.

The production-volume variance is ________. (Round any intermediary calculations to

the nearest cent and your final answer to the nearest dollar.)

A) $6,000

B) $8,000

C) $14,000

D) $0

Which of the following is an advantage of COQ measures?

A) They help managers aggregate costs to evaluate the tradeoffs of incurring prevention

costs and appraisal costs to eliminate internal and external failure costs.

B) They detect and provide immediate short-run feedback on whether

quality-improvement efforts are succeeding.

C) They forecast customer satisfaction and employee satisfaction, which are useful

indicators of long-run performance.

D) They direct attention to financial processes that help managers identify the precise

problem areas that need improvement.

Rubium Micro Devices currently manufactures a subassembly for its main product. The

costs per unit are as follows:

Direct materials $54.00

Direct labor 35.00

Variable overhead 40.00

Fixed overhead 34.00

Total $163.00

Crayola Technologies Inc. has contacted Rubium with an offer to sell 6,000 of the

subassemblies for $144.00 each. Rubium will eliminate $89,000 of fixed overhead if it

accepts the proposal. Should Rubium make or buy the subassemblies? What is the

difference between the two alternatives?

A) Buy; savings = $89,000

B) Buy; savings = $7,000

C) Make; savings = $1,000

D) Make; savings = $203,000

The selling price per unit less the variable cost per unit is the ________.

A) fixed cost per unit

B) gross margin

C) margin of safety

D) contribution margin per unit

An unfavorable fixed overhead spending variance indicates that ________.

A) there was more excess capacity than planned

B) the price of fixed overhead items cost more than budgeted

C) the fixed overhead cost-allocation base was not used efficiently

D) the denominator level was more than planned

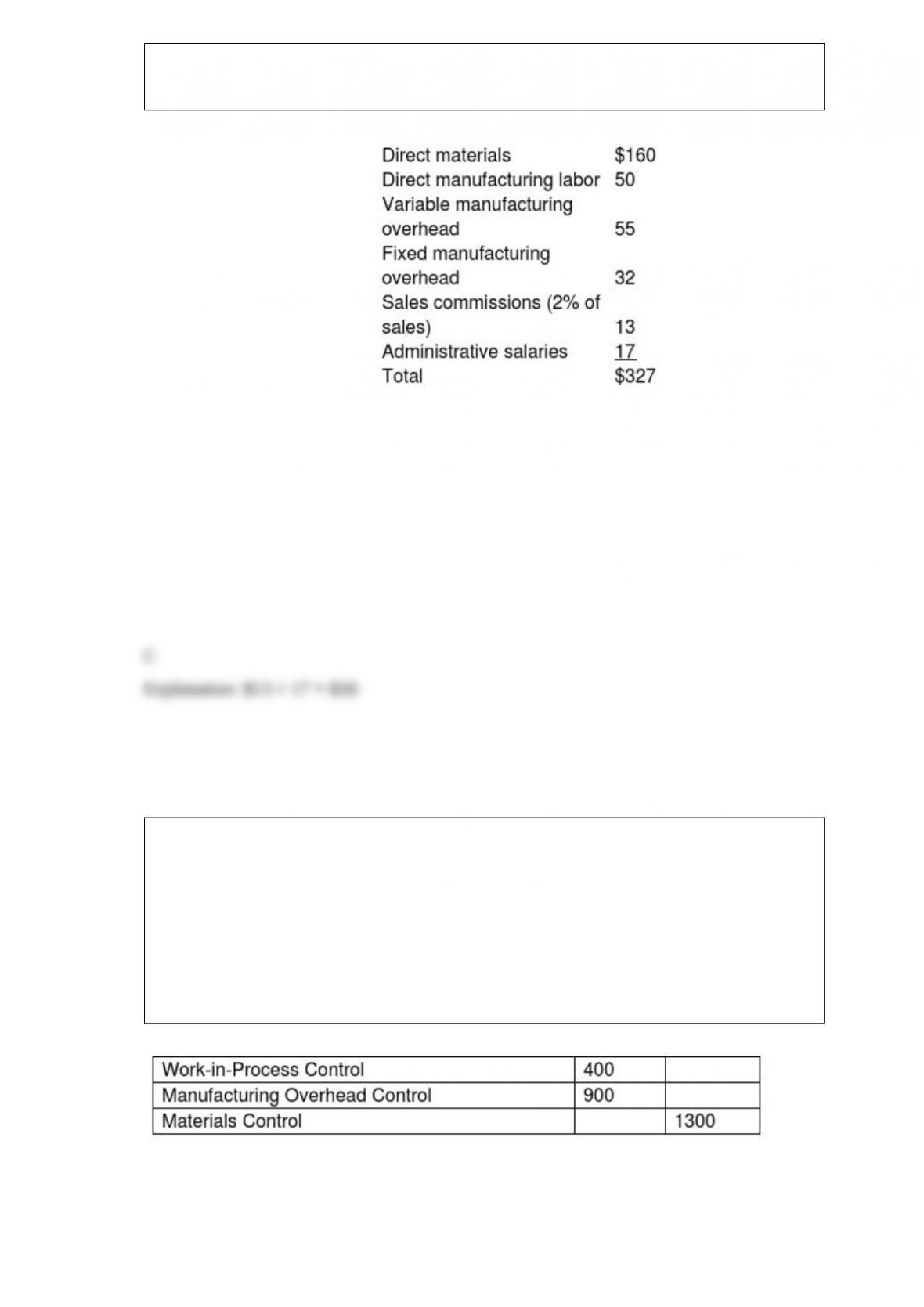

When $10,0000 direct materials are requisitioned, which of the following would be the

correct journal entry?

A) Manufacturing Overhead Control $10,000

Materials Control $10,000

B) Work-in-Process Control $10,000

Materials Control $10,000

C) Materials Control $10,000

Work-in-Process Control $10,000

D) Accounts Payable Control $10,000

Materials Control $10,000

Bouchard Company manufactures a product that currently has a full cost of $700. Its

target operating income per unit is $50 and management’s budgets assume that same

target operating income per unit for the foreseeable future. To stay competitive,

Bouchard management believes it must cut its price by 15%. What will be its new target

price?

A) $700

B) $587.50

C) $637.50

D) $50

Which of the following is a responsibility center to measure the revenues and costs of

subunits in centralized or decentralized companies?

A) investment center

B) environmental center

C) exchange policy center

D) taxation rebate center

Demand for refinements to the costing system has accelerated due to ________.

A) increase in direct costs

B) decrease in product diversity

C) decrease in indirect costs

D) competition in product markets

M & G TV and Appliance Store is a small company that has hired you to perform some

management advisory services. The following information pertains to 2017 operations.

Sales (1,200 televisions) $1,200,000

Cost of goods sold 540,000

Store manager’s salary per year 108,000

Operating costs per year 216,000

Advertising and promotion per year 24,000

Commissions (3.0% of sales) 36,000

What was the variable cost per unit sold for 2017?

A) $30

B) $480

C) $770

D) $450

A step cost functions indicates that there are

A) costs that remain the same over various ranges of activity but increases by discrete

amounts as the level of activity increases

B) greater proportions of fixed costs than variable costs at lower levels of activities

C) increases in the number of units produced during the each month of the period

D) strong relationships between fixed costs and variable costs

Which of the following is true of management accounting information?

A) It focuses on documenting past business actions of a firm.

B) It is prepared based on SEC rules and FASB accounting principles.

C) It is prepared for shareholders.

D) It helps with the coordination of elements of the value chain.

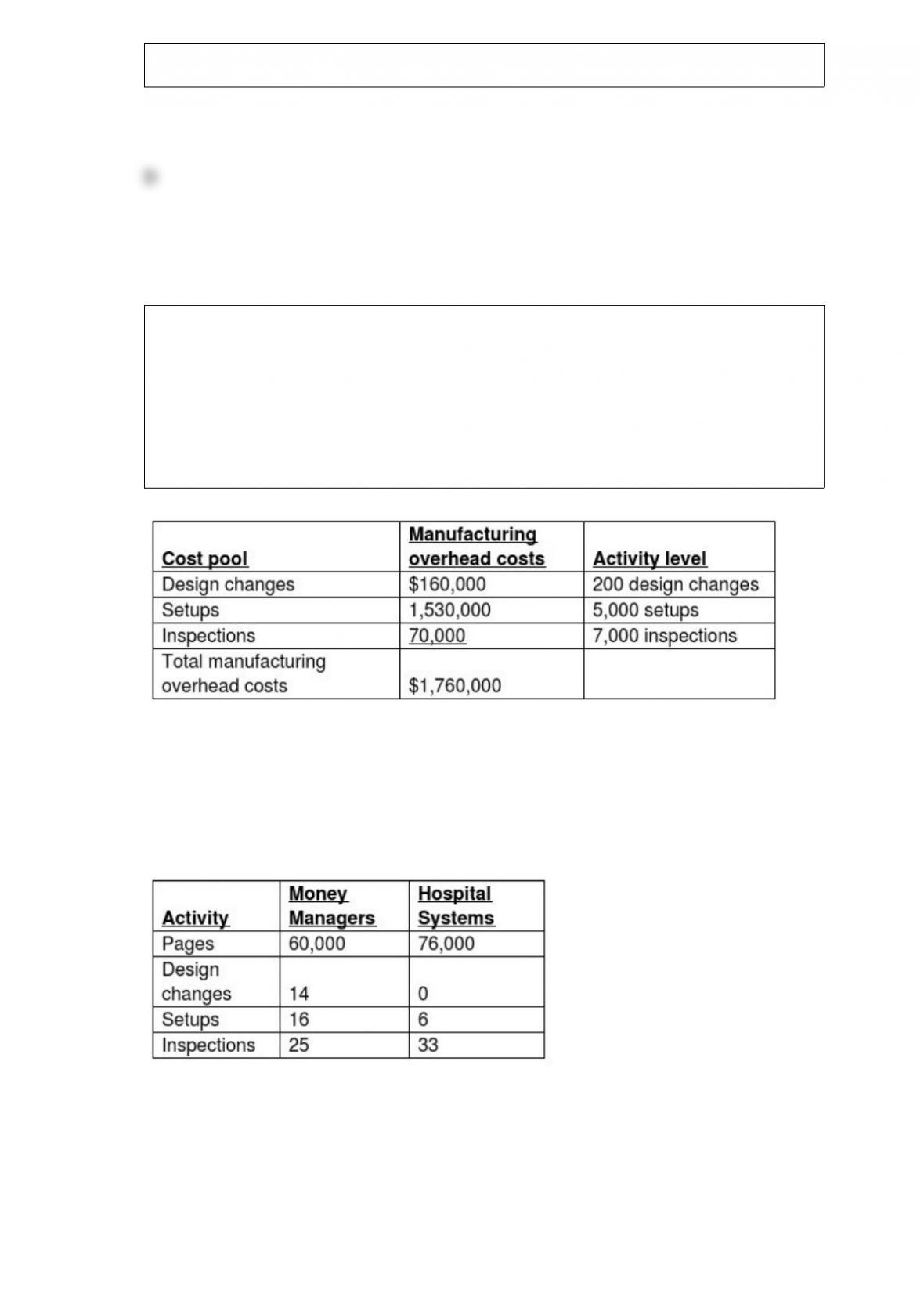

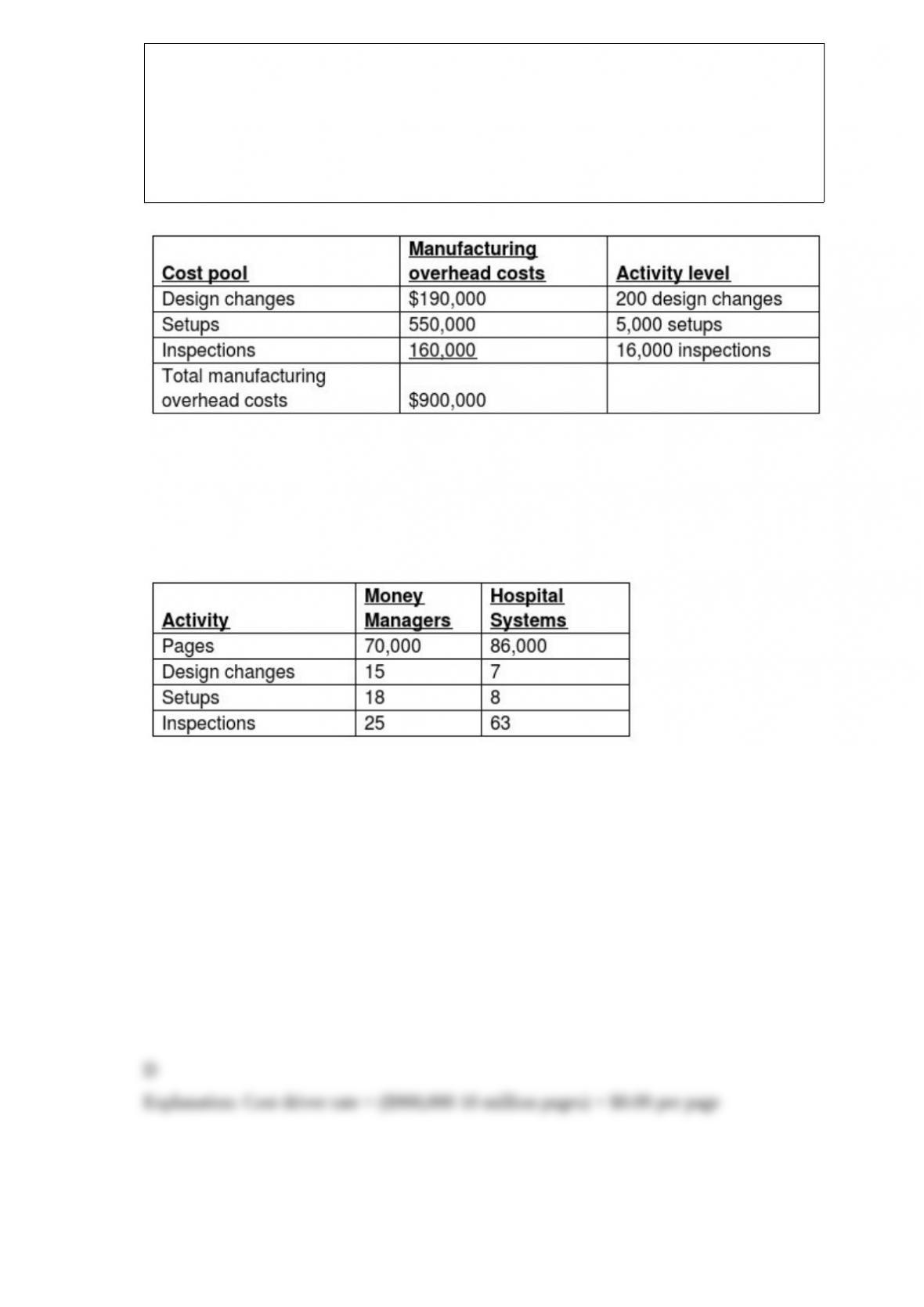

Velshi Printers has contracts to complete weekly supplements required by forty-six

customers. For the year 2018, manufacturing overhead cost estimates total $1,760,000

for an annual production capacity of 16 million pages.

For 2018 Velshi Printers has decided to evaluate the use of additional cost pools. After

analyzing manufacturing overhead costs, it was determined that number of design

changes, setups, and inspections are the primary manufacturing overhead cost drivers.

The following information was gathered during the analysis:

During 2018, two customers, Money Managers and Hospital Systems, are expected to use

the following printing services:

Assuming activity-cost pools are used, what are the activity-cost driver rates for design

changes, setups, and inspections cost pools?

A) $800.00 per change, $306.00 per setup, $10.00 per inspection

B) $800.00 per change, $14.00 per setup, $218.57 per inspection

C) $32.00 per change, $10.00 per setup, $306.00 per inspection

D) $22.86 per change, $306.00 per setup, $350 per inspection

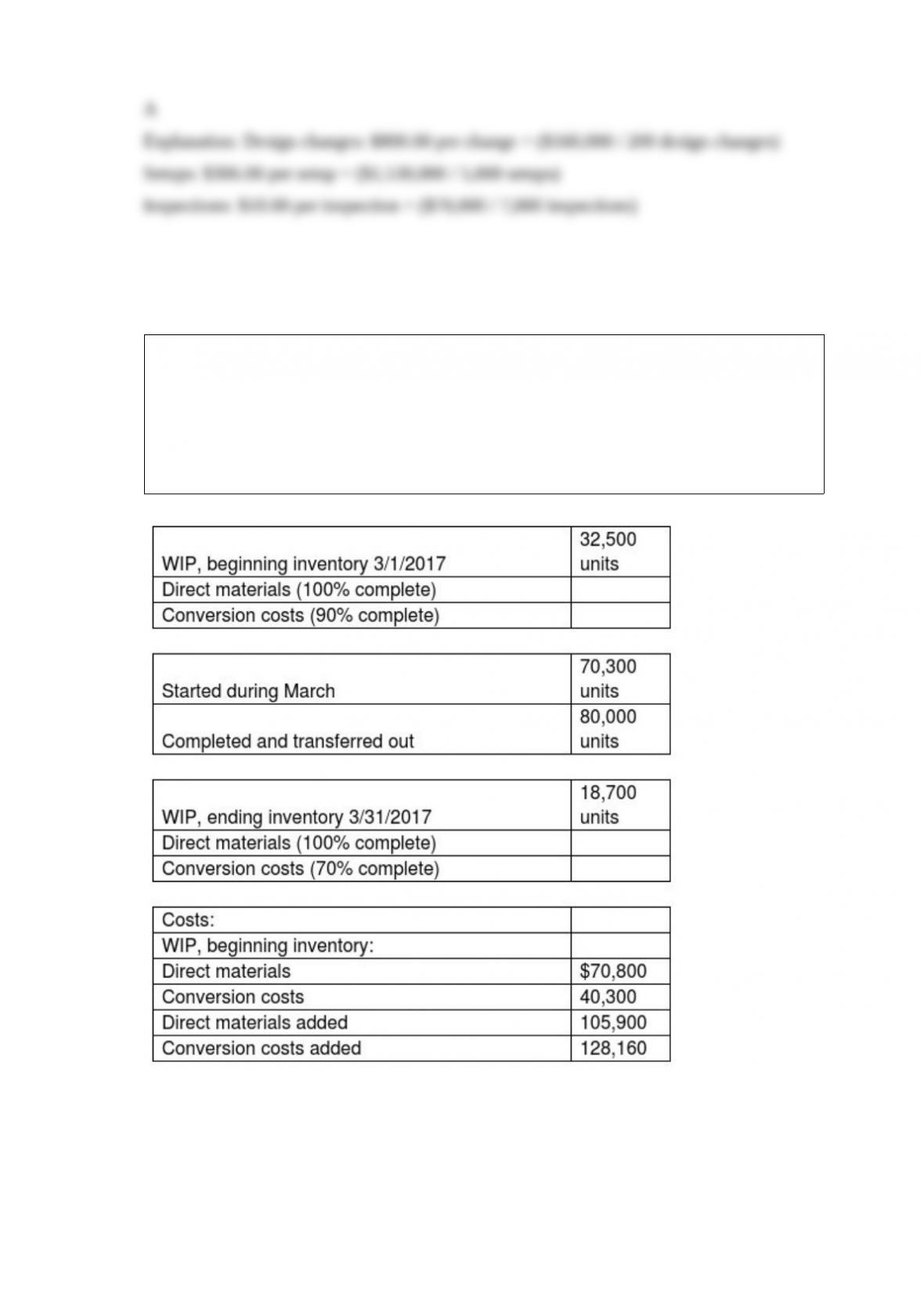

Verer Custom Carpentry manufactures chairs in its Processing Department. Direct

materials are included at the inception of the production cycle and must be bundled in

single kits for each unit. Conversion costs are incurred evenly throughout the

production cycle. Inspection takes place as units are placed into production. After

inspection, some units are spoiled due to undetectable material defects. Spoiled units

generally constitute 5% of the good units. Data provided for March 2017 are as follows:

What costs are allocated to the ending work-in-process inventory for direct materials and

conversion costs, respectively, using the FIFO method of process costing? (Round any cost

per unit calculations to the nearest cent.)

A) $64,676; $40,067

B) $28,237; $24,740

C) $28,352; $25,353

D) $28,019; $15,091

Which of the following is a difference between a diagnostic control system and an

interactive control system?

A) A diagnostic control system focuses on meeting expectations, while an interactive

control system focuses on standards of ethical behavior.

B) A diagnostic control system focuses on standards of ethical behavior while an

interactive control system focuses on meeting expectations.

C) A diagnostic control system focuses on meeting expectations, while an interactive

control system focuses on organizational attention and learning on key strategic issues.

D) A diagnostic control system focuses on organizational attention and learning on key

strategic issues, while an interactive control system focuses on meeting expectations.

These questions refer to flexible-budget variance formulas with the following

descriptions for the variables: A = Actual; B = Budgeted; P = Price; Q = Quantity. The

best label for the formula [(AP)(AQ) – (BP)(BQ)] is the ________.

A) efficiency variance.

B) price variance

C) total flexible-budget variance

D) spending variance

A local accounting firm employs 27 full-time professionals. The budgeted annual

compensation per employee is $40,500. The average chargeable time is 420 hours per

client annually. All professional labor costs are included in a single direct-cost category

and are allocated to jobs on a per-hour basis.

Other costs are included in a single indirect-cost pool, allocated according to

professional labor-hours. Budgeted indirect costs for the year are $781,500, and the

firm expects to have 75 clients during the coming year.

If ten clients are lost and the workforce stays at 27 employees, then the direct labor cost

rate per hour:

A) $34.71 per hour

B) $24.81 per hour

C) $40.05 per hour

D) $21.89 per hour

Xylon Corp. has contracts to complete weekly supplements required by forty-six

customers. For the year 2018, manufacturing overhead cost estimates total $900,000 for

an annual production capacity of 10 million pages.

For 2018, Xylon decided to evaluate the use of additional cost pools. After analyzing

manufacturing overhead costs, it was determined that number of design changes,

setups, and inspections are the primary manufacturing overhead cost drivers. The

following information was gathered during the analysis:

During 2018, two customers, Money Managers and Hospital Systems, are expected to use

the following printing services:

If manufacturing overhead costs are considered one large cost pool and are assigned based

on 10 million pages of production capacity, what is the cost driver rate? (Round the final

answer to three decimal places.)

A) $0.078 per page

B) $0.035 per page

C) $0.055 per page

D) $0.09 per page

Campus Apparels is a clothing maker. Unit costs associated with one of its products,

Product DCT121, are as follows:

What are the period costs per unit associated with Product DCT121?

A) $33

B) $17

C) $30

D) $100

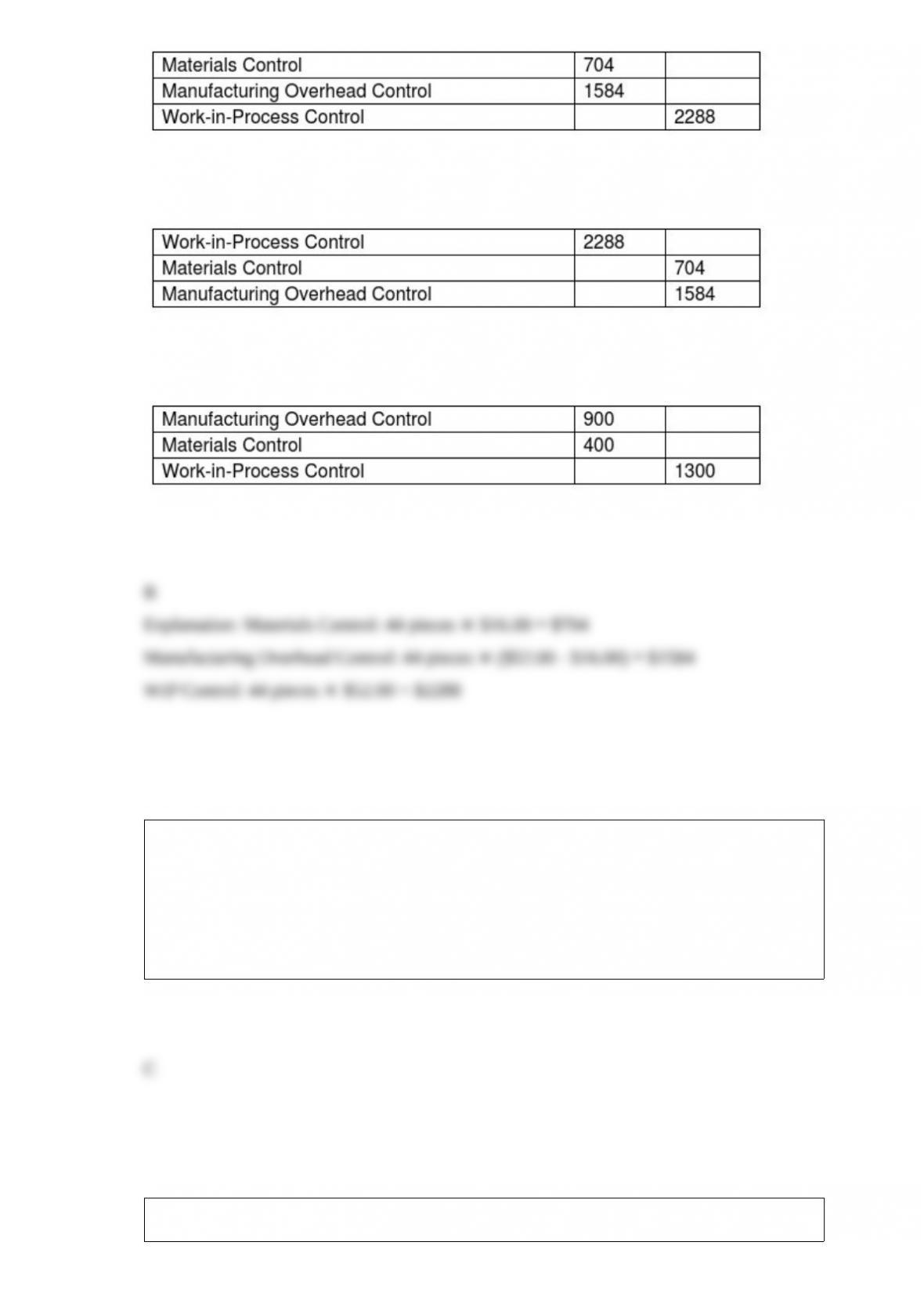

The Peric Manufacturing Shop produces motorcycle parts. Typically, 22 pieces out of a

job lot of 1800 parts are spoiled. Spoilage is considered a normal part of Peric’s

production process. Costs are assigned at the inspection point, $52.00 per unit. Spoiled

pieces may be disposed at $16.00 per unit. The spoiled goods must be inventoried

appropriately when the normal spoilage is detected. The current job requires the

production of 3600 good parts.

Which of the following journal entries properly reflects the recording of spoiled goods?

A)

B)

C)

D)

An illustration that resembles the bone structure of a fish and identifies potential

reasons why a problem exists is called ________.

A) control chart

B) Pareto diagram

C) cause-and-effect diagram

D) time-series graphs

Which of the following statements is true of costs associated with goods for sale?

A) Appraisal costs is a subcategory of shrinkage costs.

B) Special processing costs are always part of purchasing costs.

C) Opportunity costs are not recorded in the accounting system.

D) Stockout costs are costs that arise when a company runs out of a particular item for

which there is no customer demand.

Fixed costs depend on the ________.

A) amount of resources used

B) amount of unchanged costs for a given time period

C) volume of production

D) total number of units sold

Which of the following factors would guide you in classifying a product as a main

product or byproduct?

A) Number of units per processing period

B) Weight or volume of outputs per period

C) Percentage of total sales value

D) Joint costs incurred up to the split-off point

The value chain is the sequence of business functions in which ________.

A) value is deducted from the products or services of an organization

B) producing and delivering the product or service is of prime importance

C) products and services are evaluated with respect to their value to the supply chain

D) usefulness is added to the products or services of an organization

Assume you are a sophomore in college and are committed to earning an undergraduate

degree. Your current decision is whether to finish college in four consecutive years or

take a year off and work for some extra cash.

a. Identify at least two revenues or costs that are relevant to making this decision.

Explain why each is relevant.

b. Identify at least two costs that would be considered sunk costs for this decision.

c. Identify at least two opportunity costs for this decision.

d. Comment on at least one qualitative consideration for this decision.

Which of the following is a limitation of using past performance as a basis for judging

actual results?

A) It does not account for productivity increases over the periods.

B) It increases the incentive for managers to introduce budgetary slack.

C) It assumes inefficiencies of previous periods without considering possible

efficiencies of the budget period.

D) It increases the tendency of senior managers exaggerating changes in future

conditions as opposed to changes in current conditions.

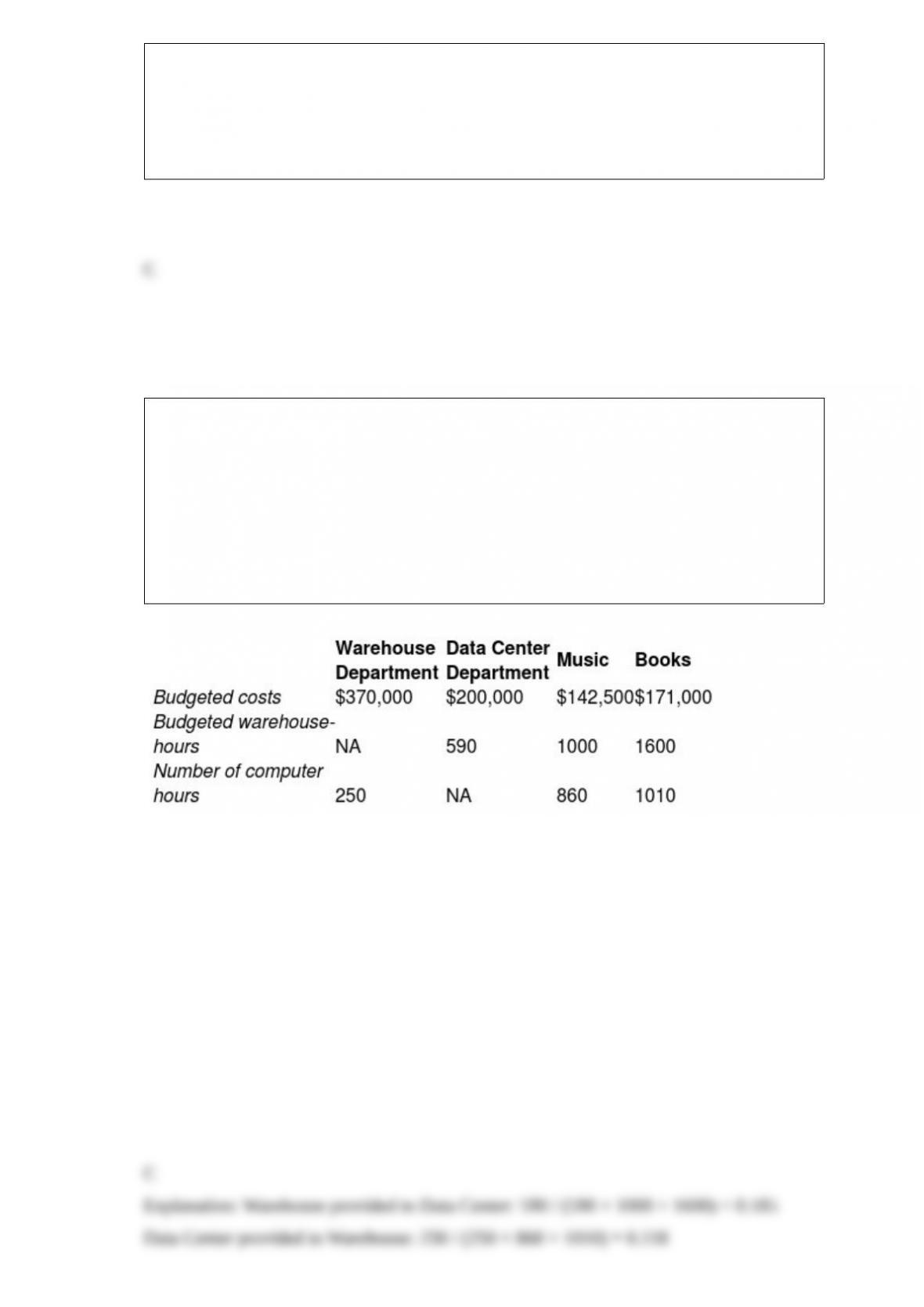

Goldfarb’s Book and Music Store has two service departments, Warehouse and Data

Center. Warehouse Department costs of $370,000 are allocated on the basis of budgeted

warehouse-hours. Data Center Department costs of $200,000 are allocated based on the

number of computer log-on hours. The costs of operating departments Music and Books

are $142,500 and $171,000, respectively. Data on budgeted warehouse-hours and

number of computer log-on hours are as follows:

Production

Support Departments Departments

Using the step-down method, what amount of Data Center Department cost will be

allocated to Department Music if the service department with the highest percentage of

interdepartmental support service is allocated first? (Round intermediary calculations to

three decimal places.)

A) $144,992

B) $91,979

C) $123,487

D) $108,021

If Kenton Inc. has a safety stock of 215 units and the average weekly demand is 35

units, how many days can be covered if the shipment from the supplier is delayed by 16

days?

A) 16 days

B) 43 days

C) 59 days

D) 27 days

To reduce distribution-channel costs, a company could ________.

A) improve the efficiency of the ordering process

B) make fewer customer visits

C) eliminate distribution to retailers and only service wholesalers

D) reduce product-handling costs