SOLUTION

(20 min.) Overhead variances, service setting.

1. and 2. Variable and Fixed Technology Overhead Variance Analysis for Carlyle Capital

Company for the first quarter of 2017

Actual Costs

Incurred

Actual Input Qty.

Budgeted Rate

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

Budgeted Rate

Allocated:

(Budgeted Input Qty.

Allowed for

Actual Output

Budgeted Rate)

Variable

Technology

Overhead $11,200

(5,500 $2)

$11,000

(13,600 0.4 $2)

$10,880

(13,600 0.4 $2)

$10,880

Fixed

Technology

(13,600 0.4 $3)

$16,320

3. Carlyle Capital has done a reasonable job overall of managing its technology overhead costs.

It has both an unfavorable variable overhead spending and efficiency variance. Carlyle had

an unfavorable efficiency variance because it used too many CPU units of processing time

relative to the number of client interactions it had. This is not an issue if the goal was to meet

the high-performance computing needs of clients and resulted in higher levels of client

satisfaction or revenues. For the 5,500 CPU units used, Carlyle spent almost $2.04 per unit

From the standpoint of capacity utilization, Carlyle Capital was successful at managing the

fixed technology overhead resources. They handled 13,600 client interactions, compared to

an expected output of 12,000. It would be useful to know what the firm views as the

8-33 Identifying favorable and unfavorable variances. Tred-America, Inc., manufactures tires

for large auto companies. It uses standard costing and allocates variable and fixed manufacturing

overhead based on machine-hours. For each independent scenario given, indicate whether each of

the manufacturing variances will be favorable or unfavorable or, in case of insufficient

information, indicate “CBD” (cannot be determined).

Scenario

Variable

Overhead

Spending

Variance

Variable

Overhead

Efficiency

Variance

Fixed

Overhead

Spending

Variance

Fixed

Overhead

Production-

Volume

Variance

Production output is 8% more

than budgeted, and actual fixed

manufacturing overhead costs

are 7% less than budgeted

Production output is 11% more

than budgeted; actual

machine-hours are 5% less than

budgeted

Production output is 15% less

than budgeted

Actual machine-hours are 18%

greater than flexible-budget

machine-hours

Relative to the flexible budget,

actual machine-hours are 10%

greater, and actual variable

manufacturing overhead costs

are 15% less

SOLUTION

(15 min.) Identifying favorable and unfavorable variances.

Scenario

VOH

Spending

Variance

VOH

Efficiency

Variance

FOH

Spending

Variance

FOH

Production-Volu

me Variance

Production output is 8%

more than budgeted, and

Cannot be

determined: no

Cannot be

determined: no

Favorable:

actual fixed

Favorable:

output is greater

Production output is

Cannot be

Cannot be

Cannot be

Unfavorable:

Actual machine-hours

are 18% greater than

Cannot be

determined: no

Unfavorable:

too many

Cannot be

determined: no

Cannot be

determined: no

Relative to the flexible

budget, actual

less

Favorable:

actual VOH rate

Unfavorable:

actual

Cannot be

determined: no

Cannot be

determined: no

8-34 Flexible-budget variances, review of Chapters 7 and 8. Eric Williams is a cost

accountant and business analyst for Diamond Design Company (DDC), which manufactures

expensive brass doorknobs. DDC uses two direct-cost categories: direct materials and direct

manufacturing labor. Williams feels that manufacturing overhead is most closely related to

material usage. Therefore, DDC allocates manufacturing overhead to production based upon

pounds of materials used.

At the beginning of 2017, DDC budgeted annual production of 420,000 doorknobs and

adopted the following standards for each doorknob:

Input Cost/Doorknob

Direct materials (brass) 0.3 lb. @ $10/lb. $ 3.00

Direct manufacturing labor 1.2 hours @ $17/hour 20.40

Manufacturing overhead:

Variable $5/lb. × 0.3 lb. 1.50

Fixed $15/lb. × 0.3 lb. 4.50

Standard cost per doorknob $29.40

Actual results for April 2017 were as follows:

Production 29,000 doorknobs

Direct materials purchased 12,400 lb. at $11/lb.

Direct materials used 8,500 lbs.

Direct manufacturing labor 29,200 hours for $671,600

Variable manufacturing overhead $ 65,100

Fixed manufacturing overhead $158,000

Required:

1. For the month of April, compute the following variances, indicating whether each is

favorable (F) or unfavorable (U):

a. Direct materials price variance (based on purchases)

b. Direct materials efficiency variance

c. Direct manufacturing labor price variance

d. Direct manufacturing labor efficiency variance

e. Variable manufacturing overhead spending variance

f. Variable manufacturing overhead efficiency variance

g. Production-volume variance

h. Fixed manufacturing overhead spending variance

2. Can Williams use any of the variances to help explain any of the other variances? Give

examples.

SOLUTION

(35 min.) Flexible-budget variances, review of Chapters 7 and 8.

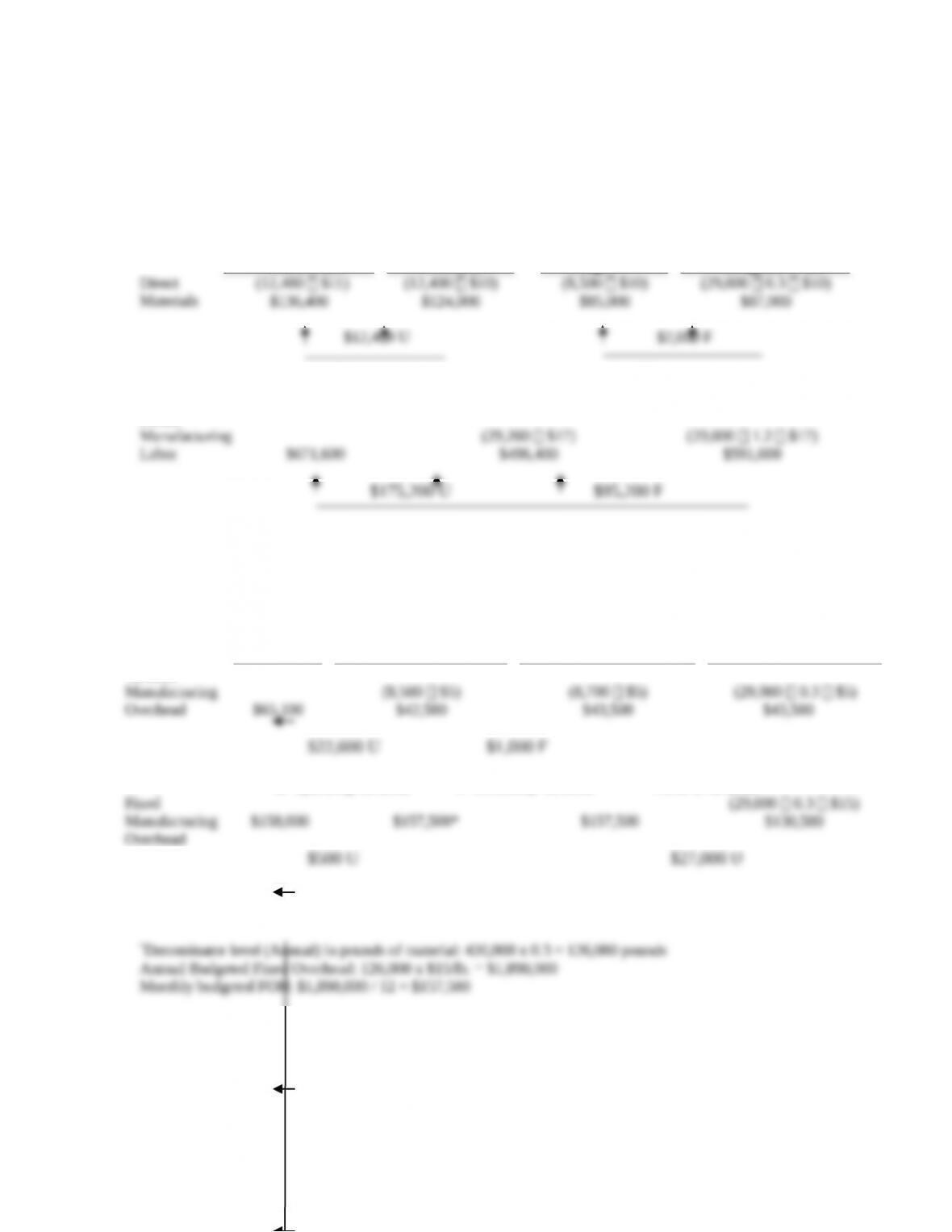

1. Solution Exhibit 8-34 contains a columnar presentation of the variances for Diamond Design

Company (DDC) for April 2017.

SOLUTION EXHIBIT 8-34

Actual Costs

Incurred:

Actual Input Qty.

Actual Input Qty.

´

Budgeted Price

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

× Actual Rate Purchases Usage × Budgeted Price

a. Price variance b. Efficiency variance

Direct

Manufacturing

(29,200 $17)

(29,000 1.2 $17)

c. Price variance d. Efficiency variance

Actual Costs

Incurred

Actual Input Qty.

Budgeted Rate

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

Budgeted Rate

Allocated:

(Budgeted Input Qty.

Allowed for

Actual Output

Budgeted Rate)

Variable

Manufacturing

(8,500 $5)

(8,700 $5)

(29,000 0.3 $5)

e. Spending variance f. Efficiency variance Never a variance

Fixed

(29,000 0.3 $15)

h. Spending variance Never a variance g. Production volume variance

2. The direct materials price variance indicates that DDC paid more for brass than they had

planned. If this is because they purchased a higher quality of brass, it may explain why they

used less brass than expected (leading to a favorable material efficiency variance). In turn, since

variable manufacturing overhead is assigned based on pounds of materials used, this directly led

8-35 Comprehensive variance analysis. Cooking Whiz manufactures premium food

processors. The following are some manufacturing overhead data for Cooking Whiz for the year

ended December 31, 2017:

Manufacturing

Overhead

Actual Results Flexible Budget Allocated

Amount

Variable $ 71,808 $ 80,640 $ 80,640

Fixed 360,672 351,360 368,640

Budgeted number of output units: 915

Planned allocation rate: 2 machine-hours per unit

Actual number of machine-hours used: 1,632

Static-budget variable manufacturing overhead costs: $76,860

Required:

Compute the following quantities (you should be able to do so in the prescribed order):

1. Budgeted number of machine-hours planned

2. Budgeted fixed manufacturing overhead costs per machine-hour

3. Budgeted variable manufacturing overhead costs per machine-hour

4. Budgeted number of machine-hours allowed for actual output produced

5. Actual number of output units

6. Actual number of machine-hours used per output unit

SOLUTION

(30 min.) Comprehensive variance analysis.

1. Budgeted number of machine-hours planned can be calculated by multiplying the number

2. Budgeted fixed MOH costs per machine-hour can be computed by dividing the flexible

3. Budgeted variable MOH costs per machine-hour are calculated as budgeted variable

MOH costs divided by the budgeted number of machine-hours planned:

1. Budgeted number of machine-hours allowed for actual output achieved can be calculated

2. The actual number of output units is the budgeted number of machine-hours allowed for

3. The actual number of machine-hours used per output unit is the actual number of

8-36 Journal entries (continuation of 8-35).

Required:

1. Prepare journal entries for variable and fixed manufacturing overhead (you will need to

calculate the various variances to accomplish this).

2. Overhead variances are written off to the Cost of Goods Sold (COGS) account at the end of

the fiscal year. Show how COGS is adjusted through journal entries.

SOLUTION

(60 min.) Journal entries (continuation of 8-35).

1. Key information underlying the computation of variances is:

Actual

Results

Flexible-Budget

Amount

Static-Budget

Amount

1. Output units (food processors) 960 960 915

2. Machine-hours 1,632 1,920 1,830

3. Machine-hours per output unit 1.70 2.00 2.00

Solution Exhibit 8-36 shows the computation of the variances.

Journal entries for variable MOH, year ended December 31, 2017:

Journal entries for fixed MOH, year ended December 31, 2017:

2. Adjustment of COGS