A direct cost of one cost object cannot be an indirect cost of another cost object.

The net realizable value (NRV) method allocates joint costs to joint products produced

during the accounting period on the basis of their relative NRV—final sales value plus

separable costs.

When rework is normal and NOT attributable to a specific job, the costs of rework are

charged to manufacturing overhead and are spread, through overhead allocation, over

all jobs.

The customer perspective under the balanced scorecard approach would include

measures on cost reduction.

The product or service transferred between subunits of an organization is called an

intermediate product.

Fixed cost per unit falls with an increase in production volume.

Rework labor time is considered an overhead cost and not a direct labor cost.

Allocating joint costs to individual products can be helpful for litigation settlement

purposes in which the costs of joint products or services are key inputs.

The cost of breakage and obsolescence are relevant incremental costs of carrying

inventory.

Management will most likely behave the same way if a department is structured as a

cost center or if the same department is structured as a profit center.

Practical capacity rather than master-budget volume is a better way to price product and

avoid downward demand spiral.

A production cost worksheet is used to summarize total costs to account for, compute

cost per equivalent unit, and assign total costs to units completed and to units in ending

work-in-process.

Uniformly assigning the costs of resources to cost objects when those resources are

actually used in a nonuniform way is called activity based costing.

When faced with a potential ethical conflict, the managerial accountant should first

consult IMA ethics counselor.

Overhead costs allocated to the sales office and individual customers are always

relevant when deciding whether to drop a customer.

Misinterpretation of data can arise when fixed costs are reported on a per unit basis.

Both, the standard-costing method and FIFO, assumes that the earliest equivalent units

in beginning work in process are completed first.

Productivity describes the relationship between different quantities of inputs consumed

and the quantities of output produced.

In estimating a cost function using quantitative analysis, the dependent variable is the

factor used to predict the independent variable.

Actual costing helps managers get information earlier and take corrective measures to

improve labor efficiency.

The costs related to buildings (such as rent and insurance), equipment (such as lease

payments or straight-line depreciation), and salaried labor in a factory are all examples

of cost items that would be part of the fixed overhead budget.

Budgeting includes only the financial aspects of the plan and NOT any nonfinancial

aspects such as the number of physical units manufactured or the hours that the direct

laborers are expected to work.

When forecasting fixed costs, managers should concentrate on total lump-sum costs

instead of unitized fixed overhead costs.

Rolling budgets help in reducing budgetary slack.

Activity-based budgeting would permit the use of multiple drivers and multiple cost

pools in the budgeting process.

If there are non-uniform cash flows (cash flows that differ from year-to-year), payback

period is calculated by dividing net initial investment by uniform increase in annual

future cash flows.

If Option 1 costs $120 and Option 2 costs $90, then the differential cost is $30.

When budgeted cost-allocation rates are used, variations in actual usage by one division

affect the costs allocated to other divisions.

A company should use the same denominator level capacity for all the budgets and

other purposes so as to facilitate comparability and avoid misrepresentation.

To calculate the breakeven point in a multiproduct situation, one must assume that the

sales mix of the various products remains constant.

When using the cause-and-effect criterion, cost drivers are selected as the cost

allocation bases.

The broader the cost object definition (i.e., plant versus product), the more confident the

manager will be about the accuracy of the direct cost amounts.

Although unit costs are regularly used in financial reports and for making product mix

and pricing decisions, managers should think in terms of total costs rather than unit

costs for making decisions.

The formal management control system includes the shared values, loyalties, and

mutual commitments among members of the organization.

Which of the following is true of price bidding with the federal government?

A) the price can only cover direct costs

B) the price can only cover direct costs and marketing costs

C) the price is based on costs that include fully allocated manufacturing and design

costs but not include marketing costs

D) the price can include only fixed manufacturing costs and design costs but not

include marketing costs

Managers can reduce capacity-based fixed costs by measuring and managing ________.

A) unused capacity

B) variable costs

C) engineered costs

D) discretionary costs

Which of the following is a cost driver for a company’s human resource costs?

A) the number of employees in the company

B) the number of job applications processed

C) the number of units sold

D) the square footage of the office space used by the human resource department

In multiproduct situations, when sales mix shifts toward the product with the lowest

contribution margin then ________.

A) total revenues will increase

B) interest cost will decrease

C) total contribution margin will increase

D) operating income will decrease

Using residual income as a measure of performance rather than return on investment

promotes goal congruence because residual income ________.

A) places importance on the reduction of underperforming assets

B) calculates a percentage return rather than an absolute return

C) concentrates on maximizing an absolute amount of dollars

D) concentrates on maximizing the return on sales

Which of the following is the mathematical expression for calculating manufacturing

cycle efficiency (MCE)?

A) MCE = Manufacturing cycle time Value-added manufacturing time

B) MCE = Manufacturing time Value-added manufacturing time

C) MCE = Value-added manufacturing time Manufacturing cycle time

D) MCE = Value-added manufacturing time Manufacturing time

Assume the following:

WIP, beginning 4500 units (100% complete as to direct materials, 40% complete as to

conversion costs)

Started 12,500 units during the period

Total spoilage is 800 with normal spoilage is calculated to be 350 units

Completed and transferred out during the period 10,000 units

WIP, ending 6200 units (100% complete as to direct materials, 50% complete as to

conversion costs)

Spoiled units 800 and inspection happens when the process is 30% complete

All materials are added at the start of the process

Under the weighted average method, would would be the equivalent units of work done

for the period?

A) 9405

B) 10,000

C) 6200

D) 13,340

Crandle Manufacturers Inc. is approached by a potential customer to fulfill a

one-time-only special order for a product similar to one offered to domestic customers.

The company has excess capacity. The following per unit data apply for sales to regular

customers:

Variable costs:

Direct materials $140

Direct labor 100

Manufacturing support 105

Marketing costs 55

Fixed costs:

Manufacturing support 175

Marketing costs 65

Total costs 640

Markup (50%) 320

Targeted selling price $960

For Crandle Manufacturers Inc., what is the minimum acceptable price of this special

order?

A) $400

B) $320

C) $480

D) $640

Sandra Clothing Company has invested $51,000,000 in its business. The target rate of

return for the company is 12%. It has long-term assets of $23,000,000. Cost of debt for

the company is 8%. It expects to sell 12,000 units in the upcoming year. What will be

the target operating income per unit for Sandra Clothing Company?

A) $153

B) $230

C) $340

D) $510

Which of the following is an assumption of linear programming?

A) Average variable costs remain constant throughout the year.

B) Opportunity costs are irrelevant in decision making.

C) Few sunk costs are relevant in decision making.

D) All costs are either variable or fixed for a single cost driver.

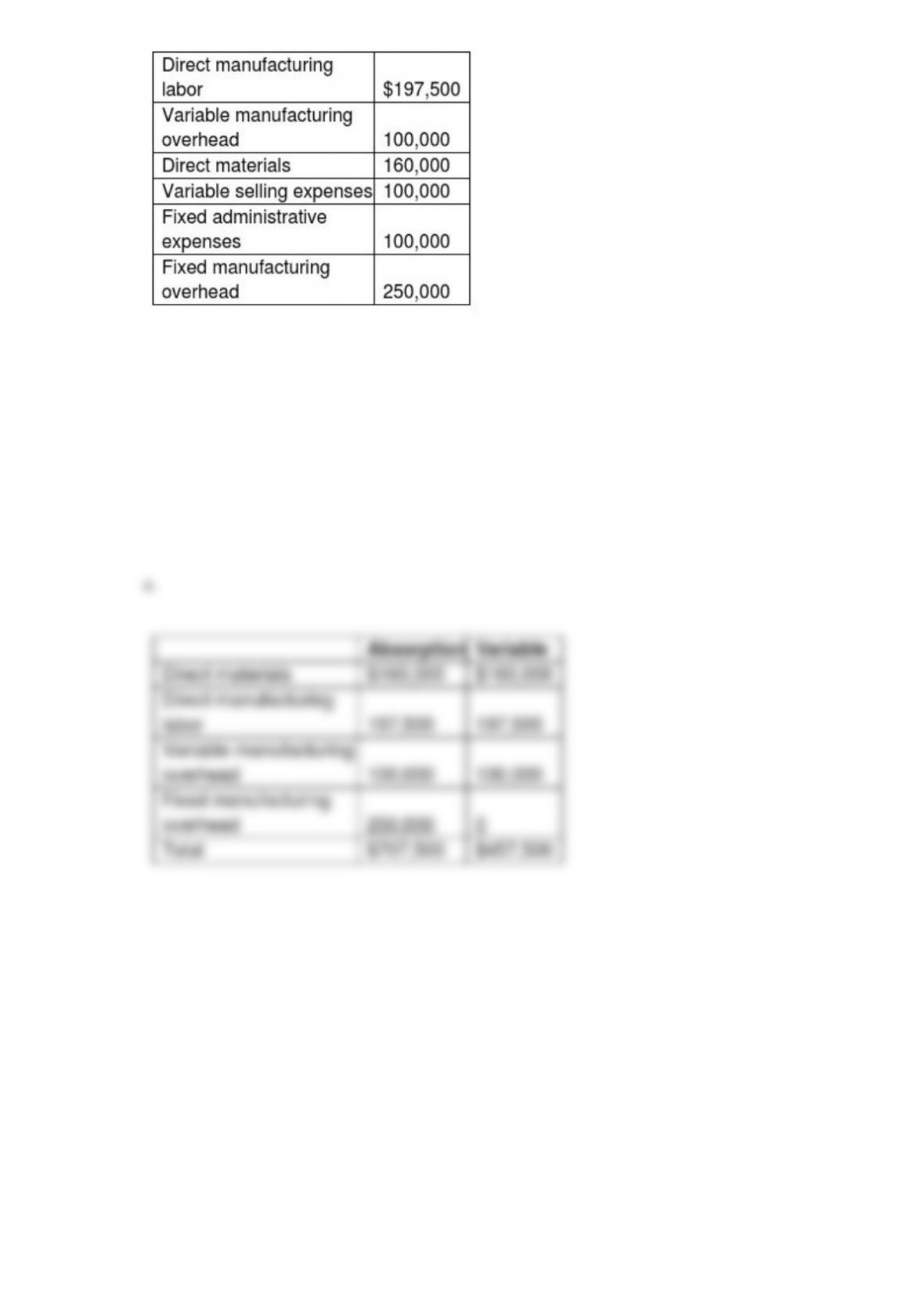

For 2017, Rockford, Inc., had sales of 150,000 units and production of 200,000 units.

Other information for the year included:

There was no beginning inventory.

Required:

a. Compute the ending finished goods inventory under both absorption and variable

costing.

b. Compute the cost of goods sold under both absorption and variable costing.

The Robinson Corporation manufactures automobile parts. During the year, the

company sold $5,600,000 of parts that had a cost of $3,200,000. At year end, these are

the balances for cost of goods sold and its manufacturing overhead accounts:

Cost of goods sold $3,200,000

Manufacturing overhead allocated $1,400,000

Manufacturing overhead control $1,495,000

What would be the correct journal entry to close out the overhead accounts assuming

that the write-of to cost of goods sold approach is used?

A) Manufacturing overhead control $1,495,000

Cost of goods sold $95,000

Manufacturing overhead allocated $1,400,000

B) Sales $5,600,000

Cost of goods sold $3,200,000

Gross profit $2,400,000

C) Finished goods $95,000

Manufacturing overhead allocated $1,400,000

Manufacturing overhead control $1,495,000

D) Cost of goods sold $95,000

Manufacturing overhead allocated $1,400,000

Manufacturing overhead control $1,495,000

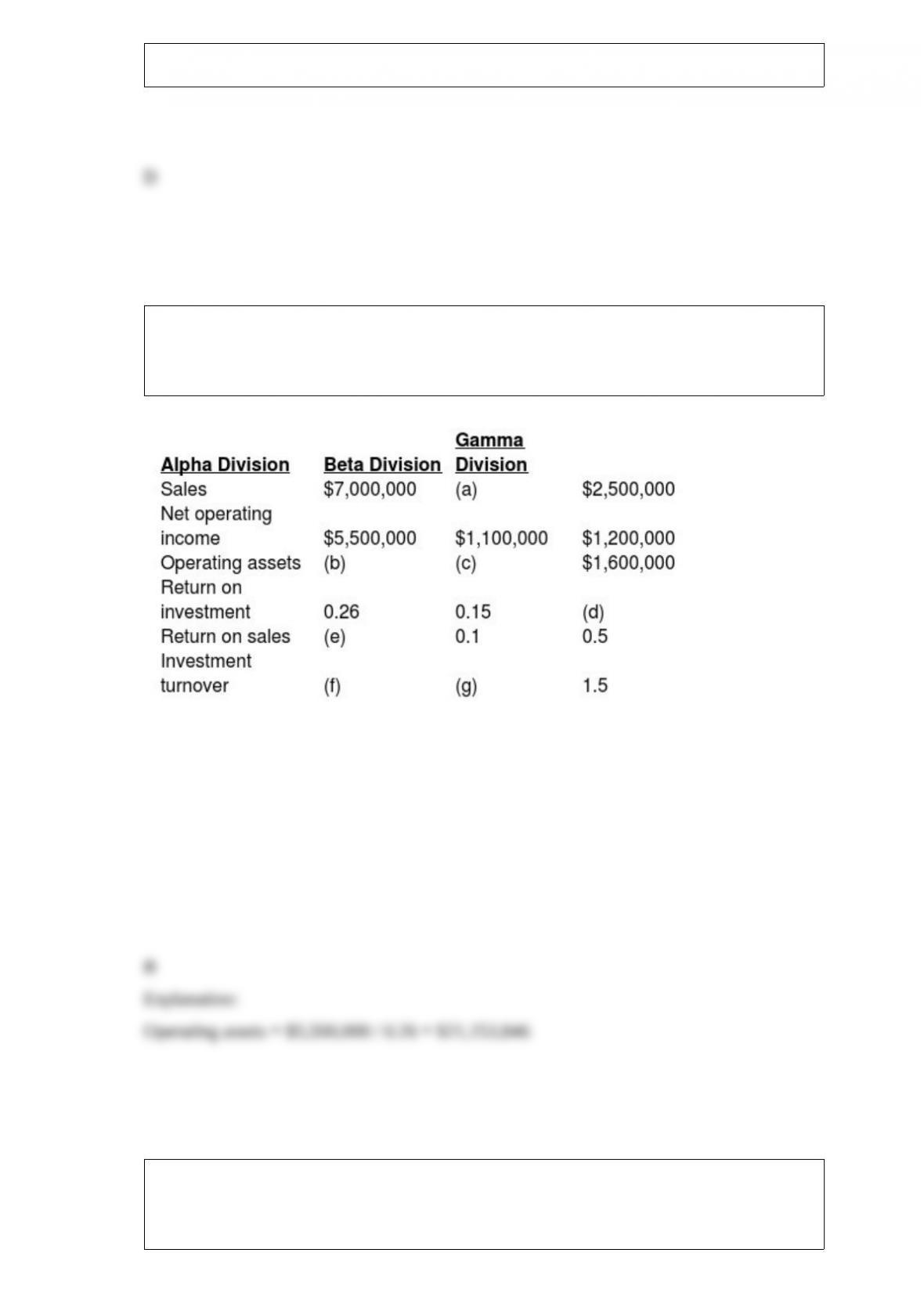

The top management at Amore Corp, a manufacturer of computer games, is attempting

to recover from a flood that destroyed some of their accounting records. The main

computer system was also severely damaged. The following information was salvaged:

What is the value of the operating assets belonging to the Alpha Division (b)?

A) $12,500,000

B) $21,153,846

C) $26,923,077

D) $1,820,000

In setting prices for products and services, managers may attempt to charge what the

customer is willing to pay however, too high a price may ________.

A) deter a customer from purchasing a product and seek alternatives

B) increase demand and demand for the product

C) indicate supply is too plentiful

D) decrease a competitor’s market share

Which cost-allocation criterion is most likely to subsidize poor performers at the

expense of the best performers?

A) the fairness or equity criterion

B) the benefits-received criterion

C) the ability to bear criterion

D) the cause-and-effect criterion

Which of the following journal entries can happen only under the production method of

recording byproducts?

A) Work in Process

Finished Goods – Byproduct

Accounts Payable

B) Cash or Accounts Receivable

Revenues – Main product

C) Byproduct Inventory

Finished Goods – Main product

Work in Process

D) Cash or Accounts Receivable

Revenues – Byproduct

SaleCo sells 8,400 units resulting in $120,000 of sales revenue, $35,000 of variable

costs, and $45,000 of fixed costs. The contribution margin percentage is ________.

A) 62.5%

B) 70.83%

C) 33.33%

D) 29.17%

In the manufacturing sector, ________.

A) only variable costs are subtracted to determine gross margin

B) fixed overhead costs are subtracted to determine gross margin

C) fixed overhead costs are subtracted to determine contribution margin

D) all operating costs are subtracted to determine contribution margin

A single indirect-cost rate distorts product costs because ________.

A) there is an assumption that all support activities affect all products in a uniform way

B) it recognizes specific activities that are required to produce a product

C) competitive pricing is ignored

D) it assumes all costs are product costs

Which of the following is an objective of value engineering?

A) to reduce cost by eliminating all value-added activities

B) to streamline and add non-value added activities

C) to reduce the total cost of the product

D) to understand competitors’ product design

Which of the following efforts would most likely yield the greatest re-engineering

benefits?

A) focusing on a single activity to determine if it is necessary

B) decreasing quantity of output produced to increase total factor productivity

C) increasing costs of all inputs used to increase total factor productivity

D) focusing on entire processes and elimination of unnecessary activities and task

High Tech Manufacturing Inc., incurred total indirect manufacturing labor costs of

$490,000. The company is labor intensive. Total labor hours during the period were

4,100. Using qualitative analysis, the manager and the management accountant

determine that over the period the indirect manufacturing labor costs are mixed costs

with only one cost driver–labor-hours. They separated the total indirect manufacturing

labor costs into costs that are fixed ($120,000 based on 8,600 hours of labor) and costs

that are variable ($370,000) based on the number of labor-hours used. The company has

estimated 7,300 labor hours during the next period.

Which of the following represents the correct linear cost function?

A) y = $370,000 + $43.02X

B) y = $120,000 + $119.51X

C) y = $120,000 + $90.24X

D) y = $370,000 + $56.98X

A manufacturer estimates that it will incur variable indirect costs for the month of

October of $70,000 and $30,000 of fixed costs. The company uses direct labor hours to

calculate the predetermined overhead rate and predicted that 3,000 direct labor hours

would be used in October. Actual direct labor hours amounted to 3,200.

Required:

A) What is the variable predetermined indirect rate for October?

B) What is the fixed predetermined indirect cost rate for October?

C) What is the total allocation rate per direct labor hour for October?

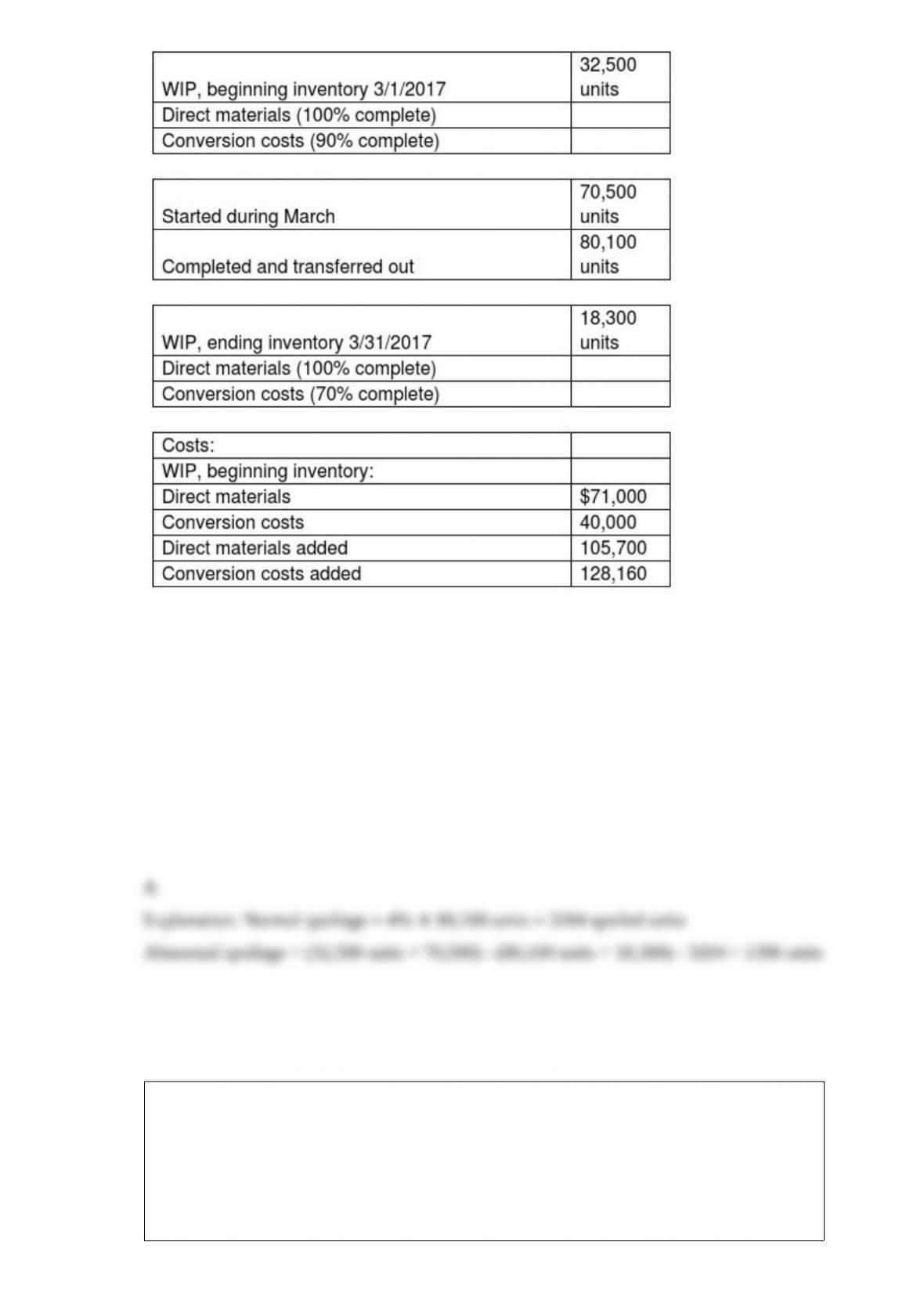

Verer Custom Carpentry manufactures chairs in its Processing Department. Direct

materials are included at the inception of the production cycle and must be bundled in

single kits for each unit. Conversion costs are incurred evenly throughout the

production cycle. Inspection takes place as units are placed into production. After

inspection, some units are spoiled due to undetectable material defects. Spoiled units

generally constitute 4% of the good units. Data provided for March 2017 are as follows:

What are the normal and abnormal spoilage units, respectively, for March when using

FIFO?

A) 3204 units; 1396 units

B) 1968 units; 1420 units

C) 9749 units; 1540 units

D) 530 units; 2032 units

Which of the following is a stage of the capital-budgeting process that tracks realized

cash flows and compares those against estimated numbers?

A) implement the decision, evaluate performance, and learn stage

B) make predictions stage

C) identify projects stage

D) make decisions by choosing among alternatives stage

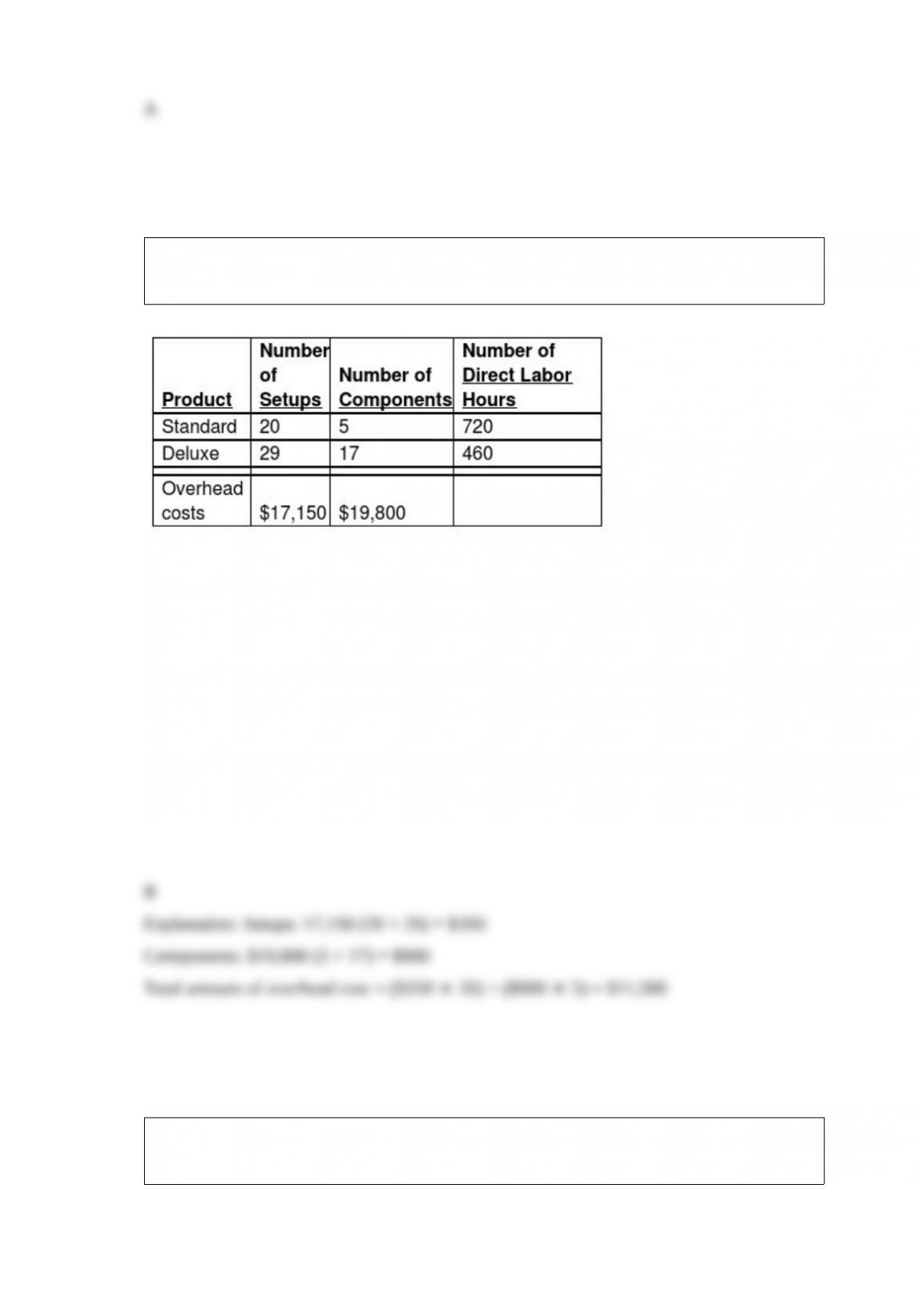

North Street Corporation manufactures two models of motorized go-carts, a standard

and a deluxe model. The following activity and cost information has been compiled:

Number of setups and number of components are identified as activity-cost drivers for

overhead. Assuming an activity-based costing system is used, what is the total amount of

overhead cost assigned to the standard model? (Do not round interim calculations. Round

the final answer to the nearest whole dollar.)

A) $18,475

B) $11,500

C) $19,750

D) $25,450

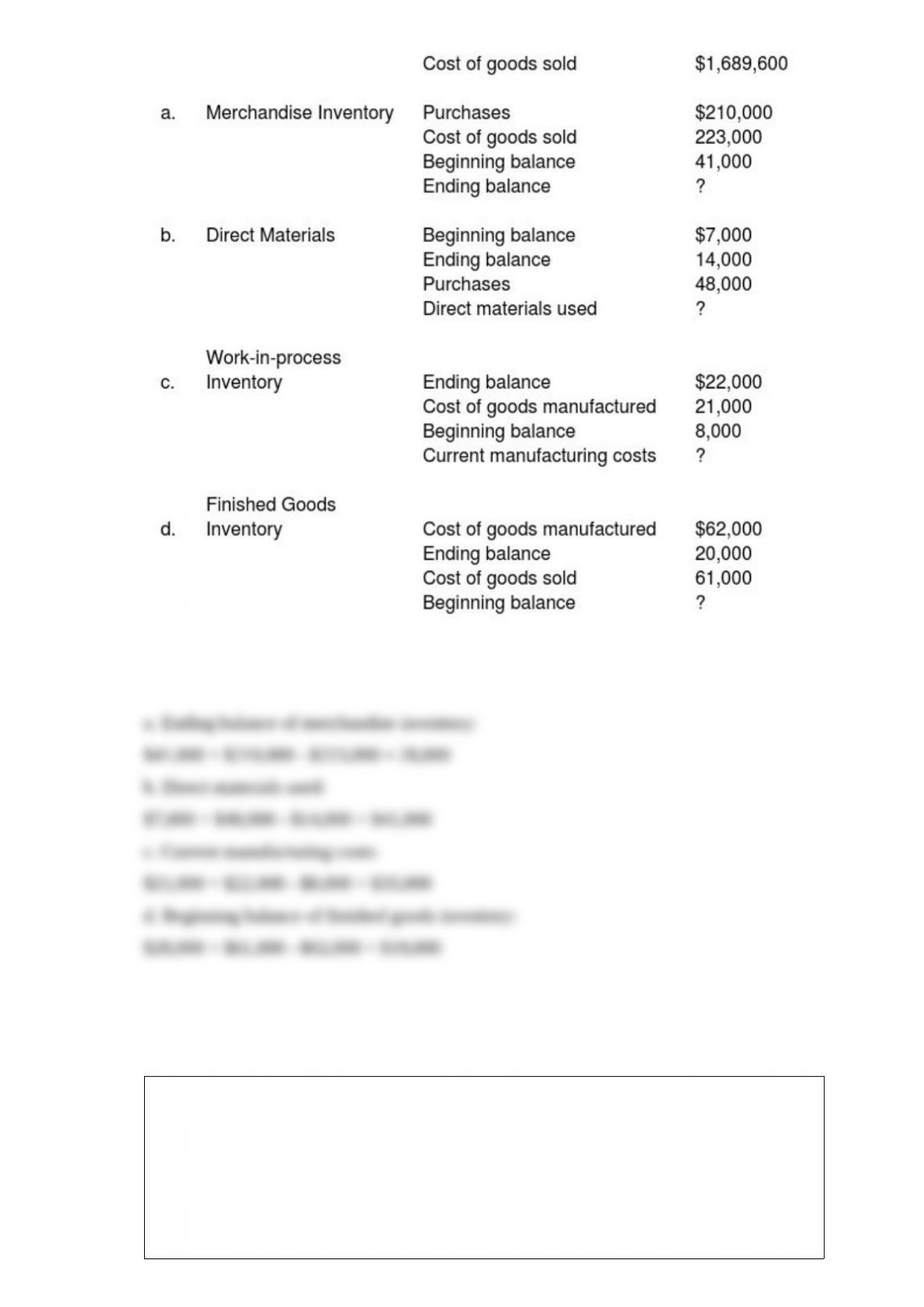

Using the following information find the unknown amounts. Assume each set of

information is an independent case.

In which order are the following developed? First to last:

A = Production budget

B = Direct materials costs budget

C = Budgeted income statement

D = Revenues budget

A) ABDC

B) DABC

C) DCAB

D) CABD

Gross margin is ________.

A) sales revenue less variable costs

B) sales revenue less cost of goods sold

C) contribution margin less fixed costs

D) contribution margin less variable costs

Ambinu Flower Company provides flowers and other nursery products for decorative

purposes in medium to large sized restaurants and businesses. The company has been

investigating the purchase of a new specially equipped van for deliveries. The van has a

value of $133,750 with a six-year life. The expected additional cash inflows are

$52,500 per year. What is the payback period for this investment?

A) 1.5 years

B) 2.5 years

C) 6 years

D) 3.5 years