Which of the following statements is true of contribution-margin format of the income

statement?

A) It is used for absorption costing.

B) It distinguishes between variable and fixed costs in its format.

C) It distinguishes manufacturing costs from nonmanufacturing costs.

D) It calculates gross margin.

The budgeted direct-labor cost rate includes ________.

A) budgeted total costs in indirect cost pool

B) budgeted total direct-labor costs in the denominator

C) budgeted total direct-labor costs in the numerator

D) budgeted total direct-labor hours in the numerator

For externally reported inventory costs, the Work-in-Process Control account is

increased (debited) by ________.

A) marketing costs

B) allocated plant utility costs

C) the purchase costs of direct and indirect materials

D) customer-service costs

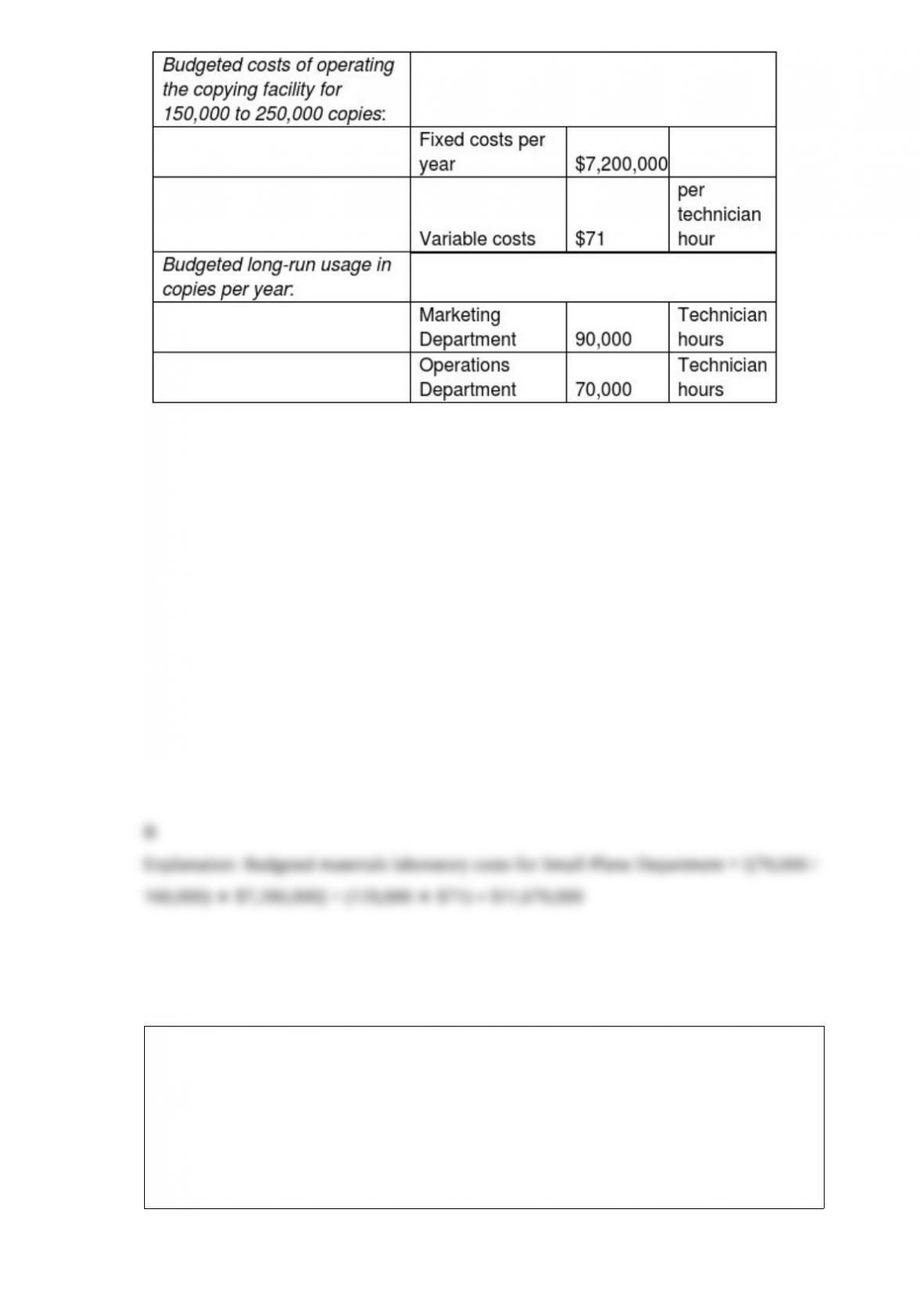

The Speedjet Aircraft Corporation has a central materials laboratory. The laboratory has

only two users, the Large Plane Department and the Small Plane Department. The

following data apply to the coming budget year:

Budgeted amounts are used to calculate the allocation rates.

Actual usage for the year by the Large Plane Department was 80,000 technician hours and

by the Small Plane Department was 120,000 technician hours. If a dual-rate cost-allocation

method is used, what amount of materials laboratory costs will be allocated to the Small

Plane Department? Assume budgeted usage is used to allocate fixed materials laboratory

costs and actual usage is used to allocate variable materials laboratory costs.

A) $13,920,000

B) $11,670,000

C) $10,370,000

D) $8,120,000

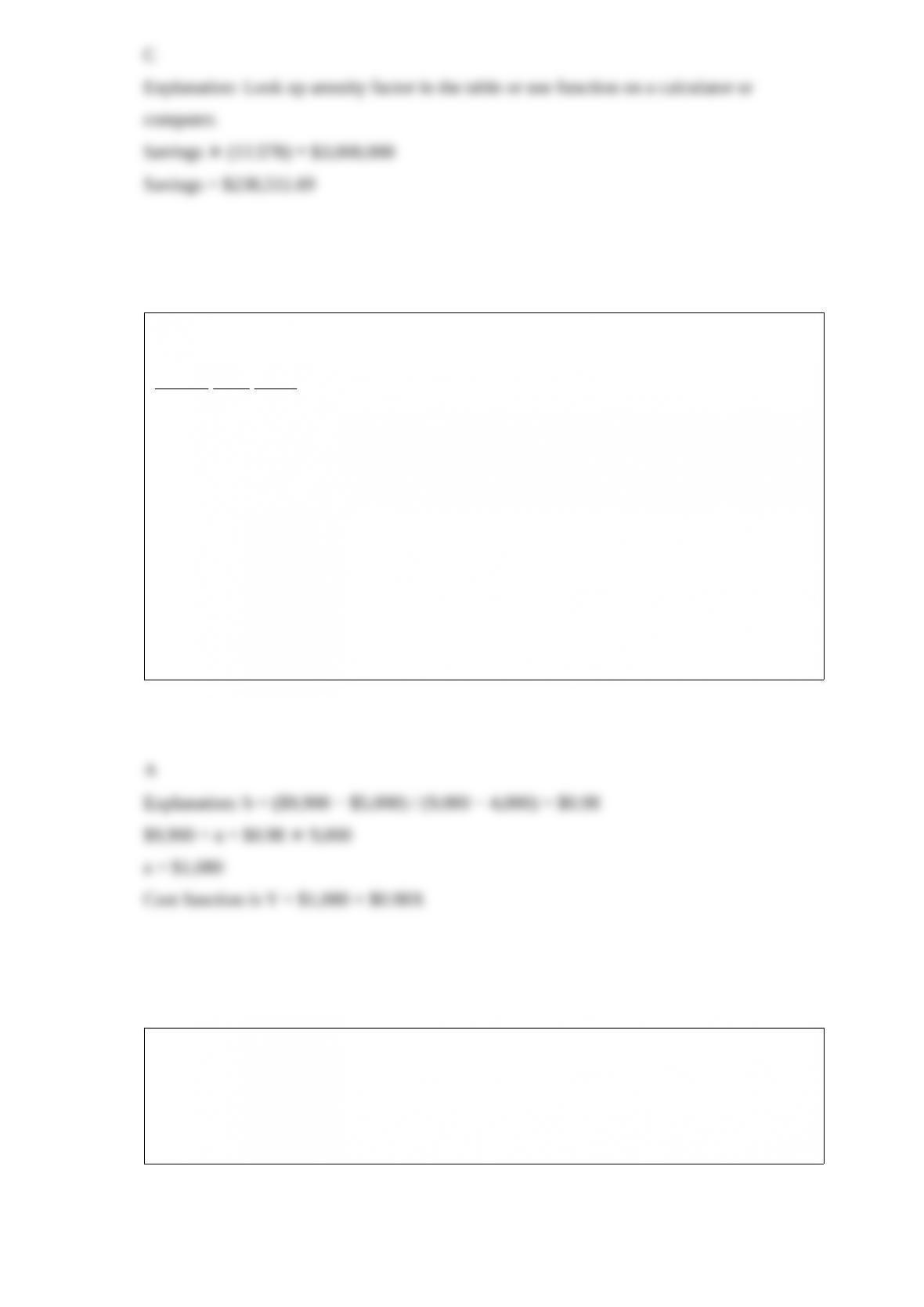

Assume your goal in life is to retire with three million dollars. How much would you

need to save at the end of each year if interest rates average 5% and you have a 10-year

work life?

A) $15,000

B) $1,841,740

C) $238,512

D) $600,000

Presented below are the production data for the first six months of the year for the

mixed costs incurred by Venus Company.

Month Cost Units

January $5,260 4,100

February $5,000 4,000

March $6,810 5,520

April $9,900 9,000

May $5,900 4,960

June $7,390 6,510

Venus Company uses the high-low method to analyze mixed costs.

How would the cost function be stated?

A) y = $1,080 + $0.98X

B) y = $4,900 + $1.25X

C) y = $2,510 + $0.98X

D) y = $9,900 + $1.10X

________ reduces theoretical capacity for unavoidable operating interruptions.

A) Practical capacity

B) Theoretical capacity

C) Master-budget capacity utilization

D) Normal capacity utilization

Manufacturing overhead costs incurred for the month are:

Utilities $45,000

Depreciation on equipment $27,000

Repairs $17,000

Which account is debited assuming utilities and repairs were on account?

A) Manufacturing Overhead Control, 89,000

B) Utilities Overhead Control, 45,000

C) Accumulated Depreciation Control, 27,000

D) Accounts Payable Control, 62,000

In accounting for scrap, which of the following statements is true?

A) Normal scrap is accounted for separately from abnormal scrap.

B) In accounting for scrap, there is no distinction between the scrap attributable to a

specific job and scrap common to all jobs.

C) Initial entries to scrap accounting records are most often made in dollar terms.

D) Scrap records not only help measure efficiency, but also help keep track of scrap,

and so reduce the chances of theft.

Which of the following best describes a bill of materials?

A) It is a document that is prepared by a vendor to invoice a manufacturer for a

purchase of materials

B) It is a document that is used to order materials

C) It is a document that requests materials be removed from the warehouse and put into

production

D) It is a document that identifies how each product is manufactured, specifying

materials and components and the quantities of materials in each finished good

Yellow Mountain Manufacturing factors practical capacity as a denominator to

calculate budgeted fixed overhead. Theoretical capacity is 12,000 units per year with

practical capacity of 9,000 units per year. Budgeted fixed overhead costs were $690,000

and actual overhead costs were $730,000 with actual output of 8,000 units. Which of

the following statements is true?

A) The budgeted cost per unit of supplying the capacity was $86.25

B) The actual cost of supplying capacity was $76.67 per unit

C) The budgeted cost of supplying the capacity was $76.67 per unit

D) The budgeted cost of supplying the capacity was $57.50 per unit.

Management is considering two alternatives. Alternative A has projected revenue per

year of $100,000 and costs of $70,000 while Alternative B has revenue of $100,000 and

costs of $60,000. Both projects require an initial investment of $250,000 of which

$75,000 has already been set aside and will be used as a down payment on the project

that is chosen. There are also other qualitative factors that management must consider

before making a final choice. Which of the following statements is correct about

relevant costs and relevant revenues.

A) The sunk cost of $75,000 is relevant

B) The projected revenues are relevant to the decision

C) The initial investment of $250,000, the projected revenues, and the projected costs

are all relevant

D) The only relevant item are the costs as they differ between alternatives

Mary’s Baskets Company expects to manufacture and sell 30,000 baskets in 2019 for $5

each. There are 4,000 baskets in beginning finished goods inventory with target ending

inventory of 9,000 baskets. The company keeps no work-in-process inventory. What

amount of sales revenue will be reported on the 2019 budgeted income statement?

A) $175,000

B) $150,000

C) $125,000

D) $85,000

If scrap, common to all jobs, is returned to the storeroom, the journal entry is ________.

A) Accounts Receivable

Materials Control

B) Materials Control

Work-in-Process Control

C) Work-in-Process Control

Materials Control

D) Materials Control

Manufacturing Overhead Control

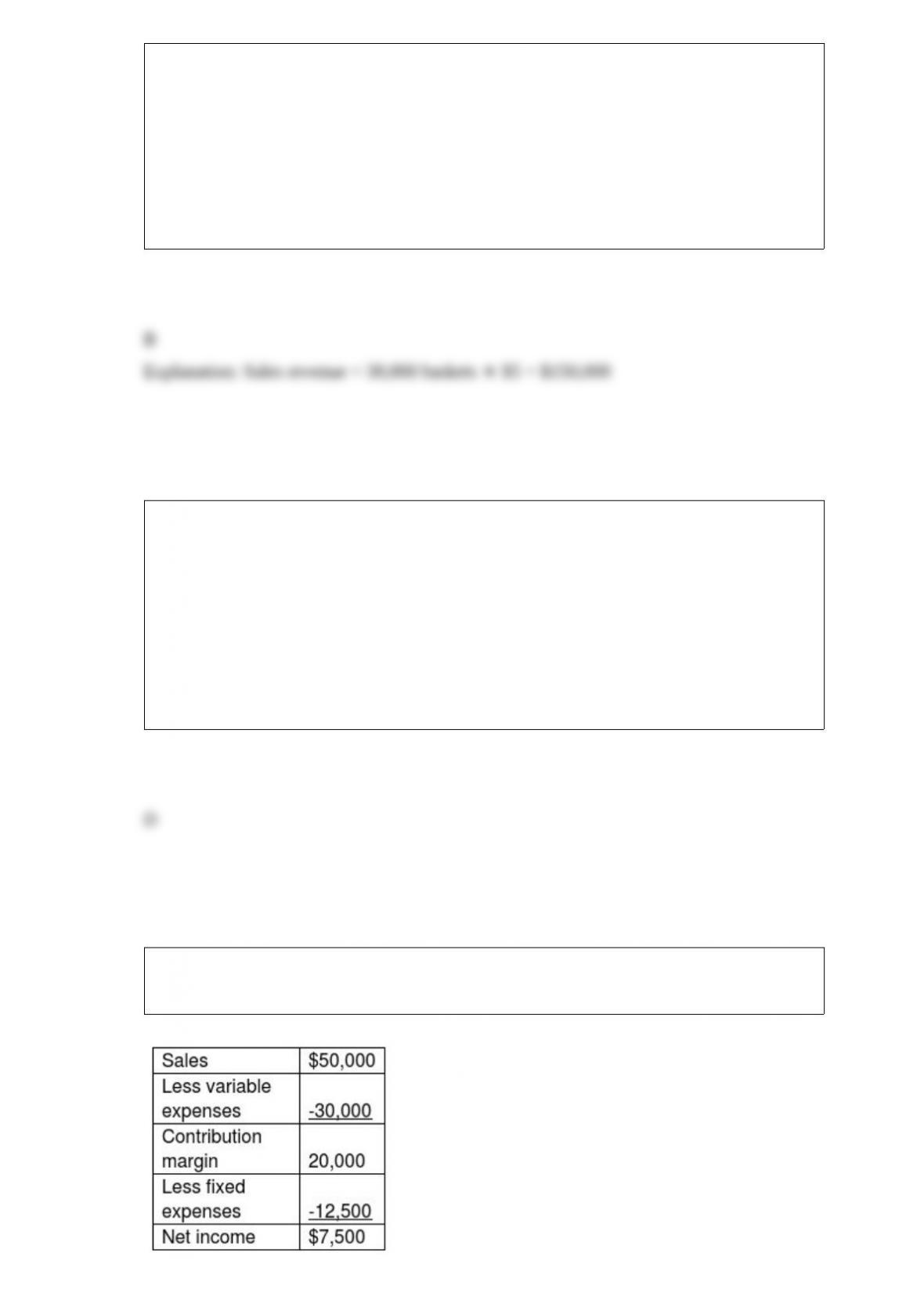

Black Pearl, Inc., sells a single product. The company’s most recent income statement is

given below.

Required:

a. Contribution margin ratio is ________%

b. Breakeven point in total sales dollars is $ ________

c. To achieve $40,000 in operating income, sales must total $ ________

d. If sales increase by $50,000, operating income will increase

by $ ________

e. To achieve a $40,000 after tax income, given a tax rate of

20%, sales must total $________

The following information was gathered for Longview Company for the year ended

December 31, 2018:

Assume that direct labor-hours are the cost-allocation base.

Required:

a. Compute the budgeted factory overhead rate.

b. Compute the factory overhead applied.

c. Compute the amount of over/underapplied overhead.

Elite Stationary employs 20 full-time employees and 10 trainees. Direct and indirect

costs are applied on a professional labor-hour basis that includes both employee and

trainee hours. Following is information for 2018:

Budget Actual

Indirect costs $300,000 $400,000

Annual salary of each employee $200,000 $210,000

Annual salary of each trainee $35,000 $40,000

Total professional labor-hours 20,000 dlh 40,000 dlh

How much should a client be billed in a normal costing system when 1,000 professional

labor-hours are used?

A) $215,000

B) $125,000

C) $130,000

D) $145,000

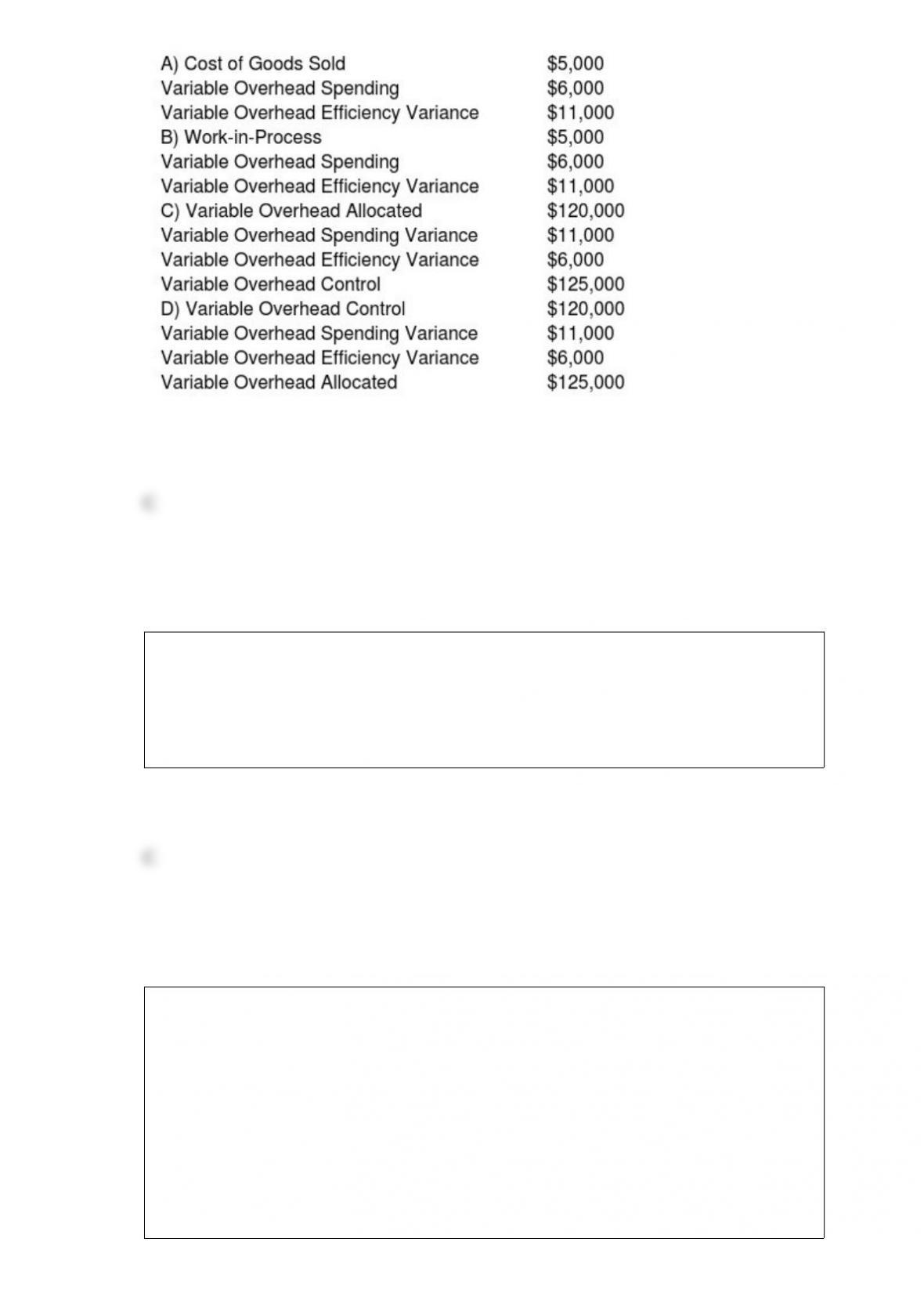

The balances in the variable overhead control account and the variable overhead control

account are $120,000 and $125,000 respectively. The variable overhead spending

variance is $6,000 and the variable overhead efficiency variance is $11,000. Which of

the following entries would be required to record the variances in a standard costing

system?

A variance is ________.

A) the difference between actual fixed cost per unit and standard variable cost per unit

B) the standard units of inputs for one output

C) the difference between an actual result and a budgeted performance

D) the difference between actual variable cost per unit and standard fixed cost per unit

For 2018, Franklin Manufacturing uses machine-hours as the only overhead

cost-allocation base. The estimated manufacturing overhead costs are $340,000 and

estimated machine hours are 40,000. The actual manufacturing overhead costs are

$450,000 and actual machine hours are 50,000. What is the difference between the

budgeted and the actual manufacturing overhead using job costing? (Round interim and

the final answer to the nearest cent.)

A) $2.75

B) $2.20

C) $0.50

D) $2.25

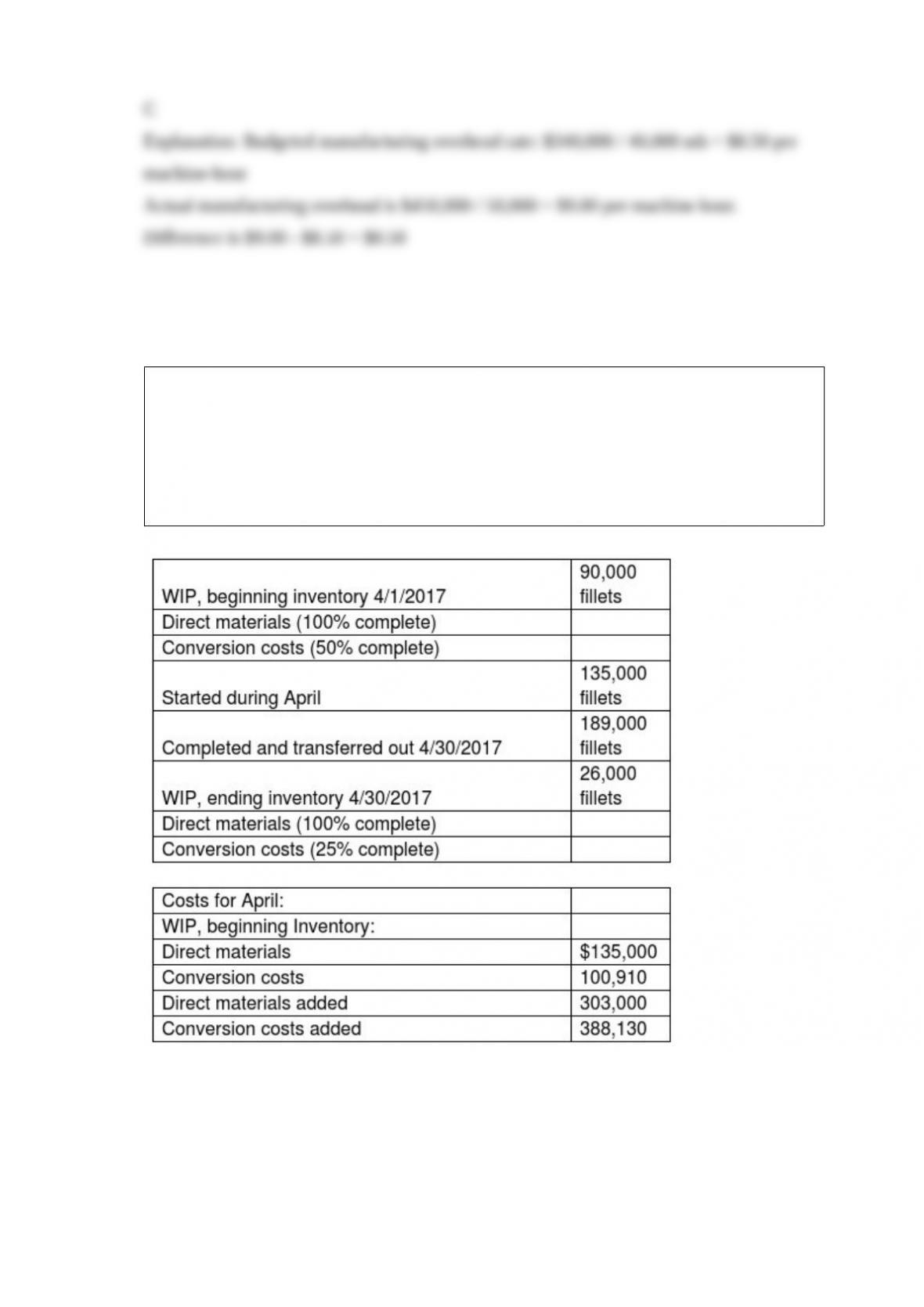

Fish Fillet Incorporated obtains fish and then processes them into frozen fillets and then

prepares the frozen fish fillets for distribution to its retail sales department. Direct

materials are added at the initiation of the cycle. Conversion costs are incurred evenly

throughout the production cycle. Before inspection, some fillets are spoiled due to

undetectable defects. Spoiled fillets generally constitute 4% of the good fillets. Data for

April 2017 are as follows:

What is the amount of direct materials and conversion costs assigned to ending work in

process using the weighted-average process-costing method? (Round any cost per unit

calculations to the nearest cent.)

A) $2025; $42,749

B) $50,700; $15,470

C) $96,730; $101,227

D) $101,227; $25,229

When comparing the operating incomes between absorption costing and variable

costing, and ending finished inventory exceeds beginning finished inventory, it may be

assumed that ________.

A) sales decreased during the period

B) variable cost per unit is more than fixed cost per unit

C) there is a favorable production-volume variance

D) absorption costing operating income exceeds variable costing operating income

Genent’s Preserves currently makes jams and jellies and a variety of decorative jars

used for packaging. An outside supplier has offered to supply all of the needed

decorative jars. For this make-or-buy decision, a cost analysis revealed the following

avoidable unit costs for the decorative jars:

Direct materials $0.56

Direct labor 0.11

Unit-related support costs 0.24

Batch-related support costs 0.30

Product-sustaining support costs 0.53

Facility-sustaining support costs 0.56

Total cost per jar $2.3

The relevant cost per jar is ________.

A) $0.67 per jar

B) $0.91 per jar

C) $1.74 per jar

D) $2.30 per jar

The revenues budget reveals

A) expected cash flows for each product

B) actual unit sales from last year multiplied by the budget period’s expected selling

prices for each product

C) the expected level of unit sales multiplied by expected unit selling prices for

company products

D) the variance of sales from actual for each product

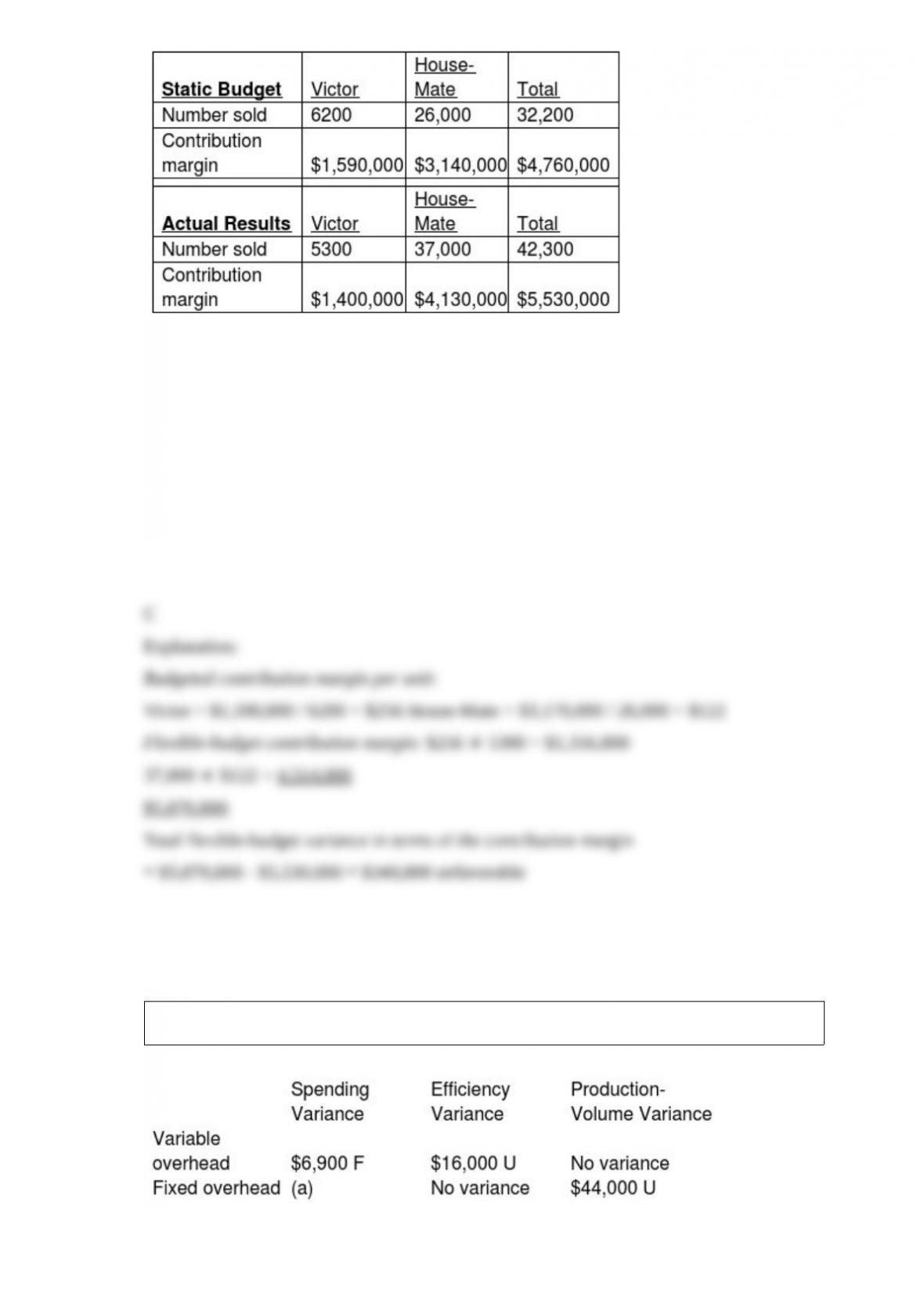

The Fortise Corporation manufactures two types of vacuum cleaners, the Victor for

commercial building use and the House-Mate for residences. Budgeted and actual

operating data for the year 2017 were as follows:

What is the total flexible-budget variance in terms of the contribution margin? (Round

intermediary calculations to the nearest dollar.)

A) $340,800 favorable

B) $1,356,800 favorable

C) $340,800 unfavorable

D) $4,514,000 unfavorable

Skizone Company’s 4-Variance Analysis:

If Skizone’s combined 4-Variance Analysis shows an unfavorable spending variance of

$2,900, what is the fixed overhead spending variance (a)?

A) $9,800 favorable

B) $4,000 unfavorable

C) $9,800 unfavorable

D) $4,000 favorable

Elite Stationary employs 20 full-time employees and 10 trainees. Direct and indirect

costs are applied on a professional labor-hour basis that includes both employee and

trainee hours. Following is information for 2018:

When a normal costing system is used, clients using proportionately more full-time

employees than trainees will ________.

A) be over billed for actual resources used

B) be under billed for actual resources used

C) be billed accurately for actual resources used

D) result in an under allocation of direct costs

Which of the following statements is true of the economic-order-quantity decision

model?

A) It assumes purchasing costs are relevant because the cost per unit changes due to the

quantity ordered.

B) Demand, ordering costs, and carrying costs are all known with certainty.

C) It assumes that stockout costs are relevant even if no stockouts occur.

D) It assumes that ordering costs and carrying costs are irrelevant.

The Duolane Pottery manufactures pottery products. All direct materials are included at

the inception of the production process. For April, there was no beginning inventory in

the processing plant. Direct materials totaled $180,000 for the month. Work-in-process

records revealed that 3,000 tons were started in April and that 2,100 tons were finished;

500 tons were spoiled as expected. Ending work-in-process units are complete in

respect to direct materials costs. Spoilage is not detected until the process is complete.

Required:

a. What is the cost per equivalent unit?

b. What are the costs assigned to completed units?

c. What are the costs transferred out?

d. What are the amounts allocated to the work-in-process ending inventory?

The budgeted indirect-cost rate for each cost pool is computed as ________.

A) budgeted annual indirect costs divided by budgeted annual quantity of cost

allocation base

B) budgeted annual quantity of cost allocation base divided by budgeted annual indirect

costs

C) actual annual indirect costs divided by budgeted annual quantity of cost allocation

base

D) budgeted annual indirect costs divided by budgeted actual quantity of cost allocation

base

Sunk costs are ________.

A) costs incurred as a result of an investment position

B) costs that is the sum of all costs in a particular business function of the value chain

C) the contributions to operating income that is forgone by not using a limited resource

in its next-best alternative use

D) costs that are unavoidable and cannot be changed no matter what action is taken

Colil Computer Systems, Inc., manufactures printer circuit cards. All direct materials

are added at the inception of the production process. During January, the accounting

department noted that there was no beginning inventory. Direct materials of $301,000

were used in production during the month. Work-in-process records revealed that

12,000 card units were started in January, 6000 card units were complete, and 4000 card

units were spoiled as expected. Ending work-in-process card units are complete in

respect to direct materials costs. Spoilage is not detected until the process is complete.

What is the direct material cost assigned to good units completed? (Please round

interim calculations to the nearest cent, and final calculations to the nearest whole

dollar.)

A) $150,480

B) $258,000

C) $100,320

D) $250,800

Customer-satisfaction measures are an example of the ________.

A) goal-congruence approach

B) balanced scorecard approach

C) financial report scorecard approach

D) investment success approach