1/1/201

7

25,00

0

630,00

0

1/1/201

7

280,00

0

2,900,00

0

1/1/201

7

320,00

0

2,930,00

0

650,00

0

Dir. Man.Lbr 880,00

0

2,900,00

0

12/31/201

7

45,00

0

Dir. Matls. 630,00

0

12/31/201

7

290,00

0

OH Alloc. 1,408,00

0

12/31/201

7

298,00

0

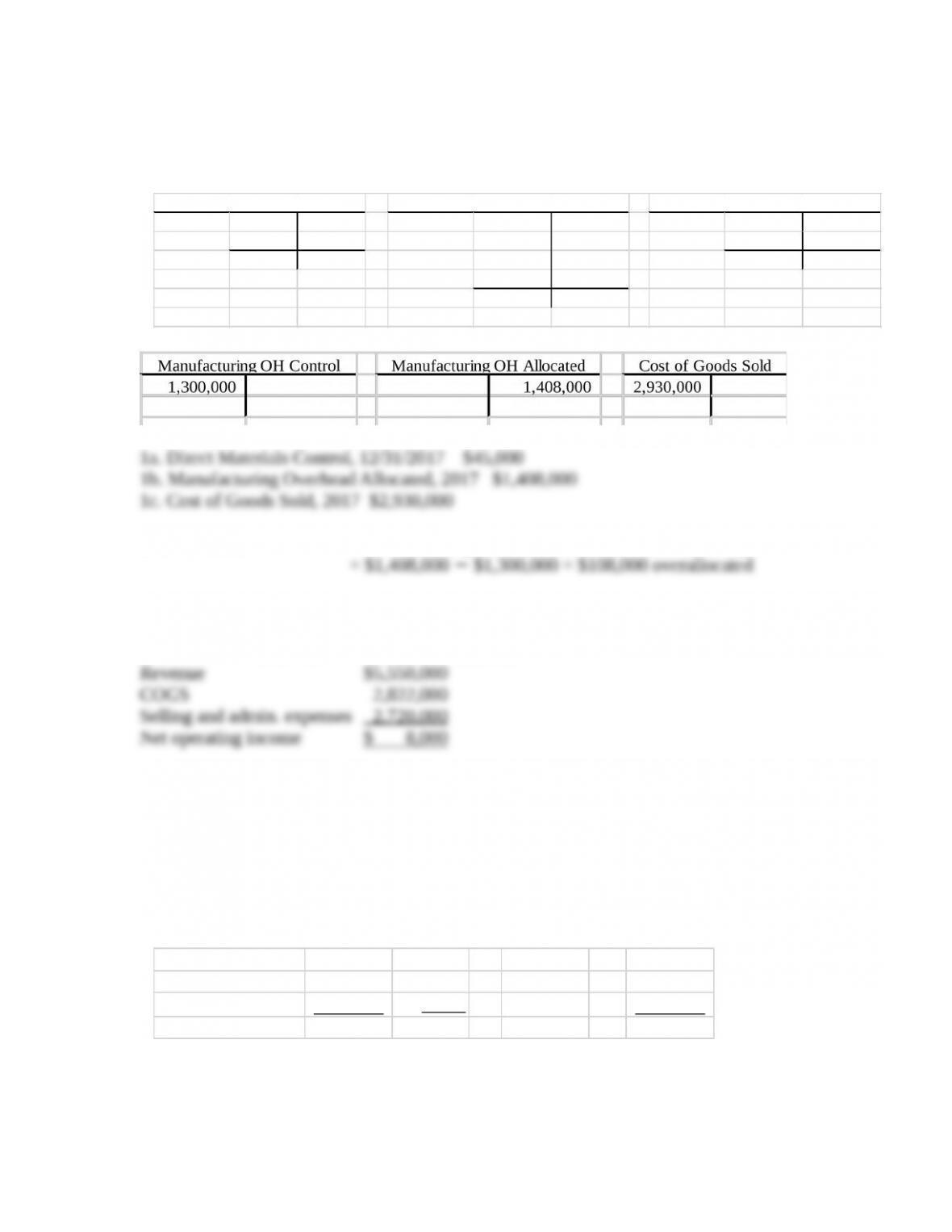

Direct Materials Control Work-in-Process Control Finished Goods Control

WIP Control 298,00

0

$

8.5% ×$108,000

= $ 9,180

Fin. Goods Control 290,00

0

8.2% × 108,00

0

= 8,85

6

Cost of Goods Sold 2,930,00

0

83.3% × 108,00

0

= 89,96

4

3,518,00

0

$ 100% $108,000

SOLUTION

(25-30 min.) Job costing, ethics.

1.

2. Overhead overallocated = Manufacturing overhead allocated – Manufacturing overhead control

3.

a. If the overallocated overhead is closed out to cost of goods sold, COGS decreases by $108,000:

$2,930,000 − $108,000 = $2,822,000

b. If the overallocated overhead is prorated to work in process control, finished goods control,

and cost of goods sold based on ending balances before proration, cost of goods sold will be

adjusted as follows: Proration of

Account $108,000 of

Ending Balance Balance Overallocated Overallocated

Before Proration as a Percent Manufacturing Manufacturing

12/31/2017 of Total Overhead Overhead

(1) (2)=(1)/3,518,000 (3) (4) = (3)×$108,000

$108,000 overallocated overhead × 83.3% = $89,964 is subtracted from COGS

4. While technically the $18,036 difference in adjusted cost of goods sold may have been

Further, Underwood may have been planning for this all along, when he increased the overhead

allocation rate for 2017. The ethical issue is that he may have planned for an overallocation of

4-46 Job costing—service industry. Market Pulse performs market research for consumer

product companies across the country. The company conducts telephone surveys and gathers

consumers together in focus groups to review foods, cleaning products, and toiletries. Market

Pulse uses a normal-costing system with one direct-cost pool, labor, and one indirect-cost pool,

general overhead. General overhead is allocated to each job based on 150% of direct labor cost.

Actual overhead equaled allocated overhead as of April 30, 2017. Actual overhead in May was

$122,000. All costs incurred during the planning stage for a market research job and during the

job are gathered in a balance sheet account called “Jobs in Progress (JIP).” When a job is

completed, the costs are transferred to an income statement account called “Cost of Completed

Jobs (CCJ).” Following is cost information for May 2017:

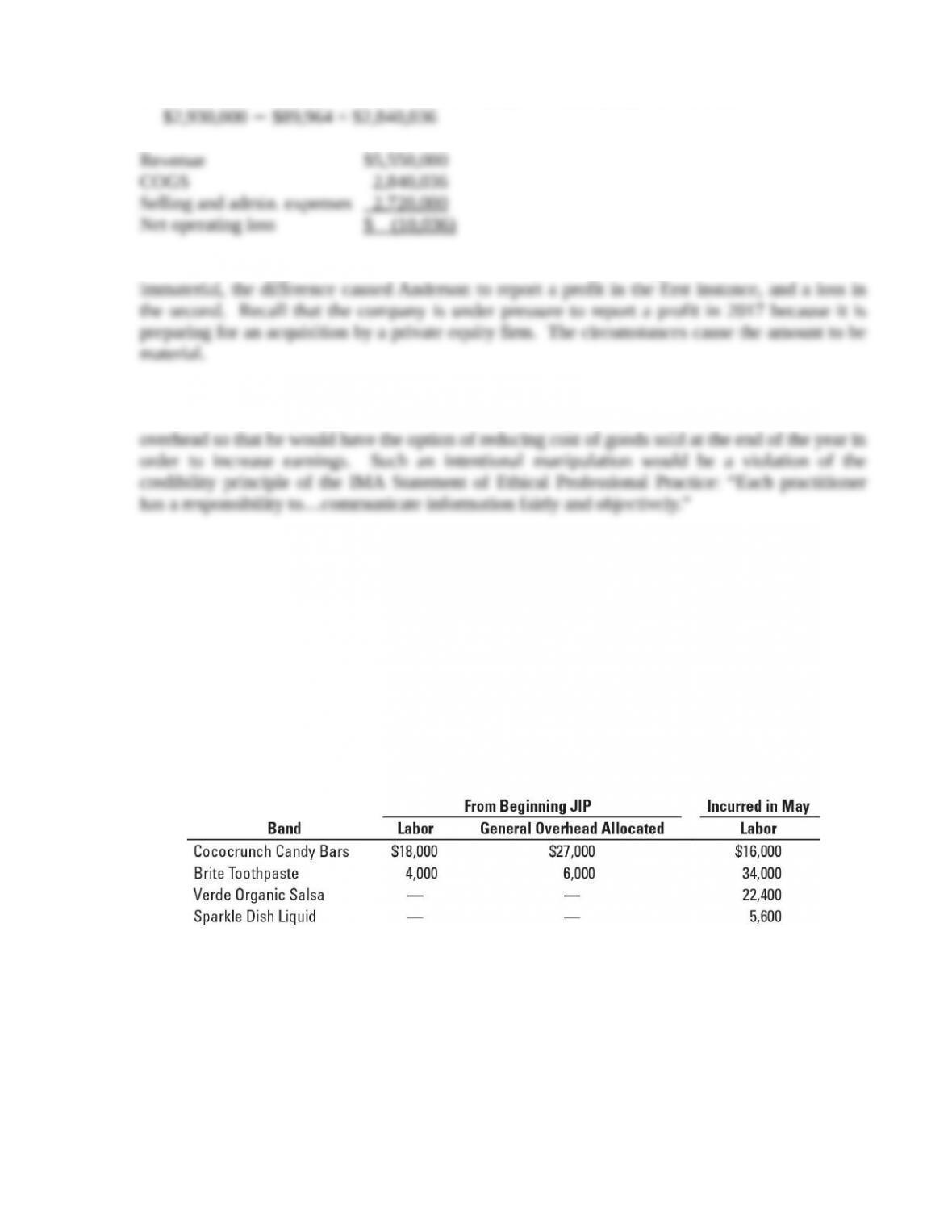

As of May 1, there were two jobs in progress: Cococrunch Candy Bars, and Brite Toothpaste.

The jobs for Verde Organic Salsa and Sparkle Dish Liquid were started during May. The jobs for

Cococrunch Candy Bars and Sparkle Dish Liquid were completed during May.

Required:

1. Calculate JIP at the end of May.

2. Calculate CCJ for May.

3. Calculate under- or overallocated overhead at the end of May.

4. Calculate the ending balances in JIP and CCJ if the under- or overallocated overhead amount

is as follows:

a. Written off to CCJ

b. Prorated based on the ending balances (before proration) in JIP and CCJ

c. Prorated based on the overhead allocated in May in the ending balances of JIP and CCJ

(before proration)

5. Which method would you choose? Explain. Would your choice depend on whether overhead

cost is underallocated or overallocated? Explain.

SOLUTION

(35 min.) Job costing—service industry.

1. Jobs in Process (JIP) May 31, 2017

Brand

Beginning

JIP

Balance

(1)

Direct

Labor Cost

in May

(2)

May Overhead

Allocated

(3) = 150% ×

(2)

Total

(4)

Brite Toothpaste $10,000 $34,000 $51,000 $ 95,000

2. Cost of Jobs Completed (CCJ) in May 2017

Brand

Beginning

JIP

Balance

(1)

Direct

Labor Cost

in May

(2)

May Overhead

Allocated

(3) = 150% × (2)

Total

(4)

Cococrunch Candy Bars $45,000 $16,000 $24,000 $85,000

3. Overhead allocated = $84,600 + $32,400 = $117,000

4a. Underallocated overhead is written off to CCJ

JIP inventory remains unchanged.

Account

May 31, 2017

Balance

(Before Proration)

(1)

Underallocated

Overhead of

$5,000 written

off to Cost of

Completed Jobs

(CCG)

(2)

May 31, 2017

Balance

(After

Proration)

(3) = (1) + (2)

JIP $151,000 $ 0 $151,000

4b. Underallocated overhead prorated based on ending balances (before proration) in JIP and

CCJ

Account

May 31, 2017

Balance

(Before

Proration)

(1)

Account Balance as

a Percent of Total

In JIP and CCJ

(2) = (1) ÷ $250,000

Proration of $5,000

Underallocated

Overhead

(3) = (2)

´

$5,000

May 31, 2017

Balance

(After Proration)

(4) = (1) + (3)

JIP

$ 151,000 0.604

0.604

´

$5,000 = $3,020

$154,020

4c. Underallocated overhead prorated based on May overhead in ending balances

Account

May 31, 2017

Balance

(Before

Proration)

(1)

Overhead

Allocated in

May Included

in May 31, 2017

Balance

(2)

Overhead Allocated

in May Included

in May 31, 2017 as

a Percent of Total

(3) = (2) ÷ $117,000

Proration of $5,000

Underallocated

Overhead

(4) = (3)

´

$5,000

May 31, 2017

Balance

(After Proration)

(5) = (1) + (4)

JIP

0.723

´

$5,000 = $3,615

CCJ

0.277

´

$5,000 = 1,385

5. I would choose the method in 4c (proration based on overhead allocated) because this

Of course, the method chosen affects reported operating income. In the case of

Despite the tax considerations, I would choose proration based on overhead allocated

because it best represents Market Pulse’s performance during a period. I would use the simpler

Try It 4-1 Solution

The solution assumes that Donna Corporation allocates manufacturing overhead costs in its

normal costing system based on direct manufacturing labor-hours.

Budgeted indirect Budgeted annual manufacturing overhead costs

cost rate Budgeted annual quantity of the cost-allocation base

=

Budgeted indirect $960,000

cost rate 32,000 hours

Total manufacturing costs of the 32 Berndale Drive job equals:

Direct manufacturing costs

Try It 4-2 Solution

The solution assumes that Donna Corporation allocates manufacturing overhead costs in its

costing system based on direct manufacturing labor-hours. Although Donna uses a

normal-costing system to manage costs throughout the year, the problem asks you to calculate

actual costs using actual costing at the end of the year. The point of the problem is to illustrate

that companies that use normal costing also use actual costing at the end of the year to evaluate

how well their normal costing systems are working. As the chapter discussion indicates,

companies rarely use actual costing as their main costing system.

Actual manufacturing Actual annual manufacturing overhead costs

overhead rate Actual annual quantity of the cost-allocation base

$992,000

31, 000 direct manufacturing labor-hours

$32 per direct manufacturing

=

=

= labor-hour

Manufacturing overhead costs Actual manufacturing Actual quantity of direct

allocated to 32 Berndale Drive job overhead rate manufacturing labor-hours

$32 per direct manuf. 160 direct manufacturi

labor-hour

= ´

= ´ ng

labor-hours

$5,120=

The cost of the job under actual costing is:

Direct manufacturing costs

Try It 4-3 Solution

The solution assumes that Donna Corporation allocates manufacturing overhead costs in its

normal costing system based on direct manufacturing labor-hours.

Budgeted indirect Budgeted manufacturing overhead costs

cost rate Budgeted annual quantity of the cost-allocation base

=

Budgeted indirect $960,000

cost rate 32,000 hours

(a) Usage of direct materials, $60,000, and indirect materials, $3,000 during April 2017

Work-in-Process Control 60,000

(b) Manufacturing payroll for April 2017: direct labor, $54,000 paid in cash

(c) Other manufacturing overhead costs incurred during April 2017, $76,000, consisting of

■ Supervision and engineering salaries, $50,000 (paid in cash);

■ Plant utilities and repairs $10,000 (paid in cash); and

■ Plant depreciation, $16,000

(d) Allocation of manufacturing overhead to jobs = Budgeted manufacturing overhead rate ×

(e) The sum of all individual jobs completed and transferred to finished goods in April 2017 is

$180,000

(f) Cost of goods sold in April 2017, $175,000

Try It 4-4 Solution

Budgeted indirect Budgeted manufacturing overhead costs

cost rate Budgeted annual quantity of the cost-allocation base

=

Budgeted indirect $960,000

cost rate 32,000 hours

Manufacturing overhead allocated during the year =

Underallocated manufacturing overhead = Actual manufacturing overhead costs – Budgeted

Account

Account

Balance

(Before

Proration

)

(1)

Manufacturing

Overhead in

Each Account

Balance

Allocated in the

Current Year

(Before

Proration)

(2)

Manufacturing

Overhead in

Each Account

Balance

Allocated in the

Current Year as

Percent of Total

(3)=(2)÷$960,00

0

Proration of $62,000

of Underallocated

Manufacturing

Overhead

(4)=(3)×$62,000

Account

Balance

(After

Proration)

(5)=(1)+(4)

Work-in-proce

ss control

$

40,000 $ 14,400 1.5

%0.015 × $62,000 = $ 930 $ 40,930

Finished

60,00