Discontinuing an unprofitable customer should be solely done on the basis of

profitability.

If the production planners set the budgeted machine hours standards too loose, one

could anticipate there would be a favorable fixed overhead efficiency variance.

A standard price is the minimum price a company will have to pay for a unit of input.

An on-time delivery rate is considered a nonfinancial measure of customer satisfaction.

The weighted average method of process costing assigns the cost of equivalent units

worked on during the current period first to complete beginning inventory, next to start

and complete new units, and finally to units in ending work-in-process inventory.

Using master budget capacity as the denominator level sets the cost of capacity at the

cost of supplying the capacity, regardless of the demand for the capacity.

The design of products, services, and processes component of the supply chain refers to

the detailed planning, engineering, and testing of products and processes.

Increased global competition is placing pressure on companies to reduce costs.

A commitment to a new capital project will always result in an increase in net working

capital.

Indirect manufacturing costs should be allocated equally to each job.

A company’s inventory levels are dependent on a number of variables including the

demand for the product, supplier relationships, and supplier relationships with their

manufacturers.

When inventories are present, classifying spoilage as normal rather than abnormal

results in an decrease in current operating income.

Theoretical capacity is unattainable in the real world.

The balance sheet and income statement are primarily management accounting reports.

Using job costing would not be appropriate in the shipping industry.

In the net present value (NPV) method, pre-tax cash flows should be used instead of

after-tax cash flows.

Return on investment can be calculated by multiplying return on assets by investment

turnover.

The selling price per unit is $25, variable cost per unit $15, and fixed cost per unit is $4

when sales are 10,000 units. If one more unit is sold, operating income will increase by

$6.

Partial productivity and TFP measures work best together because the strengths of one

offset the weaknesses of the other.

A customer cost hierarchy may include customer-sustaining costs.

The chart used to express customer profitability is called the whale curve because it is

backward-bending at the point where customers start to become unprofitable and thus

resembles a humpback.

Management control systems should be designed to support the organizational

responsibilities of individual managers.

Tracking price discounts by customer and by salesperson helps improve customer

profitability.

The breakeven points are the same under both variable costing and absorption costing.

Management accounting information and reports do not have to follow set principles or

rules such as GAAP but should be useful to its audience and meet the cost/benefit test.

Kaizen budgeting does NOT make sense for cost centers.

For optimal planning success it is best if each business function within the value chain

is performed one at a time in sequence.

Computer-based systems, like ERP, help managers budget for all manufacturing costs

but lack the ability to help managers budget for non-manufacturing costs.

Total assets employed includes all assets, regardless of their intended purpose.

The cost-allocation base is a systematic way to link an indirect cost or group of indirect

costs to cost objects.

You can find the breakeven revenues using total revenues, total variable costs, and total

fixed costs; you don’t need unit prices and costs.

The tool crib at a large manufacturing company is responsible for providing tools to the

factory workers on demand. The tool crib has a variable demand. Historically, its

demand has ranged from 220 to 500 small tools per day with an average of 360. Diane,

the tool crib attendant, works eight hours a day, five days a week. Each order is for one

small tool and each small tool takes Diane 1 minute to retrieve from the bins.

Diane has been asked to consider plans to add the retrieval of larger tooling fixtures to

her duties. She anticipates that there would be an average of 10 tooling fixtures per day

requested. Each tooling fixture would take Diane 4 minutes to retrieve.

What is the average waiting time, in minutes, if Diane continues to be the only worker

that would retrieve the small tools as well as the larger tooling fixtures?

A) 0.50 minutes

B) 5.00 minutes

C) 3.25 minutes

D) 160.00 minutes

It is usually difficult to find good cost driver (cause-and-effect relationship) between

________ and a cost allocation base.

A) unit-level costs

B) batch-level costs

C) product-sustaining costs

D) facility-sustaining costs

Maxire Shoes manufactures shoes. All direct materials are included at the inception of

the production process. For March, there were 2,800 units in beginning inventory with a

direct material cost of $1,400. Direct materials totaled $35,000 for the month.

Work-in-process records revealed that 70,000 units were started in March and that

60,000 were finished. When March ended there were 12,800 units in work-in-process.

Normal spoilage of 2% of units finished was incurred. Ending work-in-process units are

complete in respect to direct materials costs. Spoilage is not detected until the process is

complete. Endicott uses the weighted-average method.

Required:

a. What are the direct materials costs assigned to completed good units?

b. What are the direct material amounts allocated to the work-in-process ending

inventory?

Woodruff Flowering Plants provides the following information for the month of May:

For May, Woodruff will report a(n) ________.

A) favorable sales-mix variance

B) unfavorable sales-mix variance

C) favorable market-share variance

D) unfavorable market-share variance

Which of the following statements about the direct/indirect cost classification is true?

A) Indirect costs are always traced.

B) Indirect costs are always allocated.

C) The design of sales target affects the direct/indirect classification.

D) The direct/indirect classification depends on the cost control measures.

Jalbert Incorporated planned to use materials of $11 per unit but actually used materials

of $13 per unit, and planned to make 1,590 units but actually made 1,780 units.

The flexible-budget variance for materials is ________.

A) $3,180 favorable

B) $3,560 unfavorable

C) $3,180 unfavorable

D) $3,560 favorable

Which of the following is an equation of a fixed cost function?

A) y = (a + b)X

B) y = a + bX

C) y = bX

D) y = a

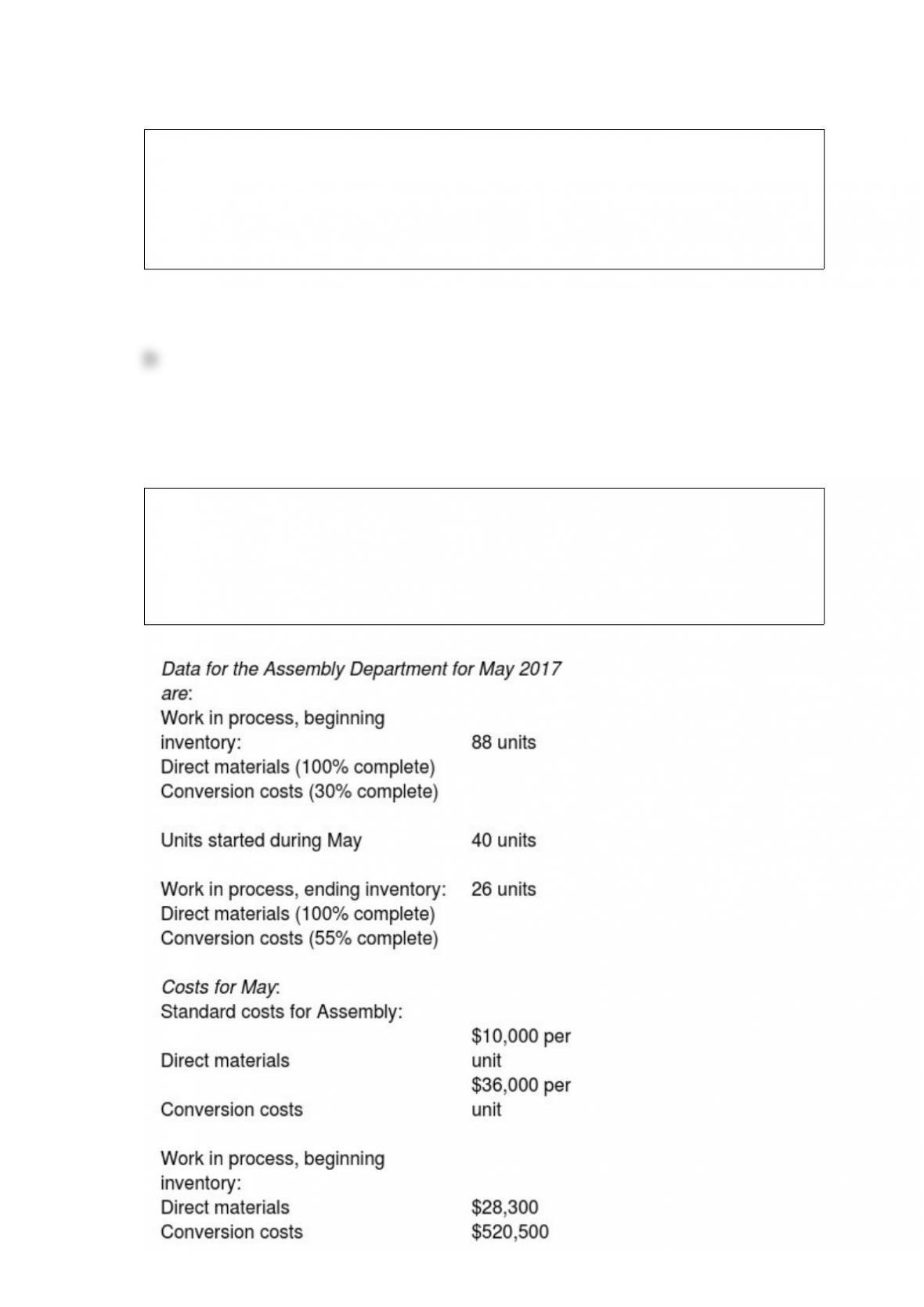

Emerging Dock Company manufactures boat docks on an assembly line. Its standard

costing system uses two cost categories, direct materials and conversion costs. Each

product must pass through the Assembly Department and the Finishing Department.

Direct materials are added at the beginning of the production process. Conversion costs

are allocated evenly throughout production.

What is the balance in ending work-in-process inventory?

A) $514,855

B) $774,800

C) $288,490

D) $175,960

Which of the following is true of net income?

A) Net income is operating income divided by income tax rate.

B) Net income is operating income plus operating revenues minus operating costs

minus income taxes.

C) Net income is operating income plus nonoperating revenues minus nonoperating

costs minus income taxes.

D) Net income is operating income minus nonoperating revenues minus nonoperating

costs minus sales taxes.

The flexible-budget variance for direct cost inputs can be further subdivided into a

________.

A) static-budget variance and a sales-volume variance

B) sales-volume variance and an efficiency variance

C) price variance and an efficiency variance

D) static-budget variance and a price variance

In a company with low operating leverage, ________.

A) fixed costs are more than the contribution margin

B) contribution margin and operating income are inversely related

C) there is a higher possibility of net loss than a higher-leveraged firm

D) less risk is assumed than in a highly leveraged firm

That part of the value chain that includes ordering and shipping the product to retail

outlets is ________.

A) Customer service

B) Production

C) Marketing

D) Distribution

In a cost-benefit approach, managers should spend resources if the ________.

A) marginal costs to the company exceed the marginal benefits

B) expected benefits to the company exceed the expected costs

C) marginal costs to the company equal the marginal benefits

D) expected benefits to the company equal the expected costs

In a noncompetitive environment, the key factor affecting pricing decisions is the

________.

A) customer’s willingness to pay

B) price charged for alternative products

C) information on competitor’s cost structure

D) minimum price acceptable to the firm

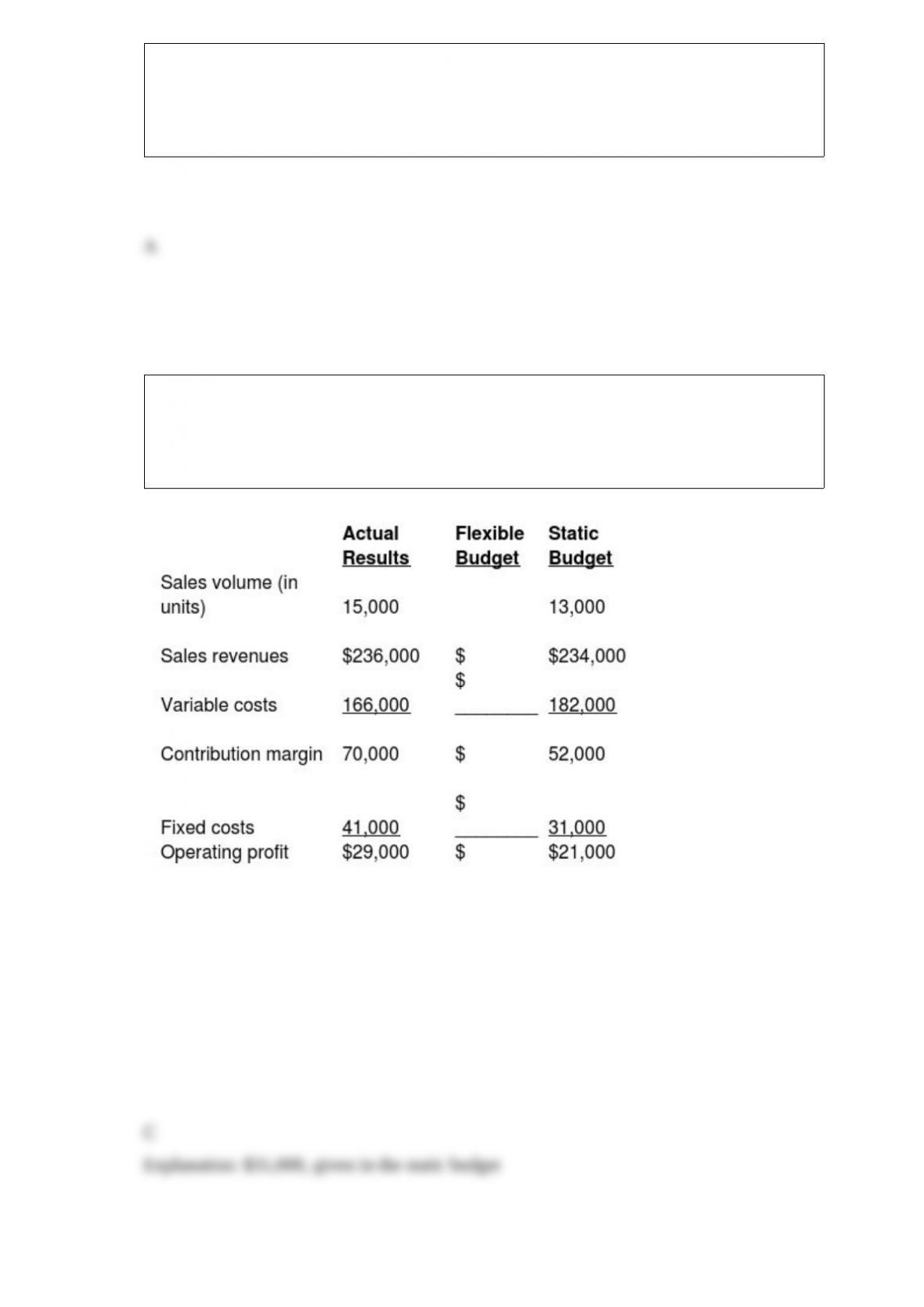

The actual information pertains to the third quarter. As part of the budgeting process,

the Duck Decoy Department of Paralith Incorporated had developed the following static

budget for the third quarter. Duck Decoy is in the process of preparing the flexible

budget and understanding the results.

The flexible budget will report ________ for the fixed costs.

A) $73,923

B) $31,000 Favorable

C) $31,000

D) $10,000 Unfavorable

Timekeeper Corporation has two divisions, Distribution and Manufacturing. The

company’s primary product is high-end watches. Each division’s costs are provided

below:

Manufacturing: Variable costs per unit $1.36

Fixed costs per unit $5.77

Distribution: Variable costs per unit $1.30

Fixed costs per unit $0.50

The Distribution Division has been operating at a capacity of 4,009,000 units a week

and usually purchases 2,004,500 units from the Manufacturing Division and 2,004,500

units from other suppliers at $13.00 per unit.

Assume 110,000 units are transferred from the Manufacturing Division to the

Distribution Division for a transfer price of $8.00 per unit. The Distribution Division

sells the 110,000 units at a price of $18 each to customers. What is the operating

income of both divisions together?

A) $347,600

B) $392,150

C) $997,700

D) $634,700

Assuming previous year’s production capacity was adequate to produce current year

output, the cost effect of growth for fixed costs is calculated by multiplying the

difference between ________ by price per unit of capacity in the previous year.

A) actual units of capacity in current year and actual units of capacity in previous year

B) capacity units required to produce current year output in previous year and the

current year capacity units

C) actual units of capacity in previous year and actual units of capacity in previous year

D) capacity units required to produce previous year output in current year and the

previous year capacity units

The goal of a properly constructed ABC system is to ________.

A) have the most accurate cost system

B) identify more indirect costs

C) develop the best cost system that meets the cost/benefit test

D) have separate allocation rates for each department

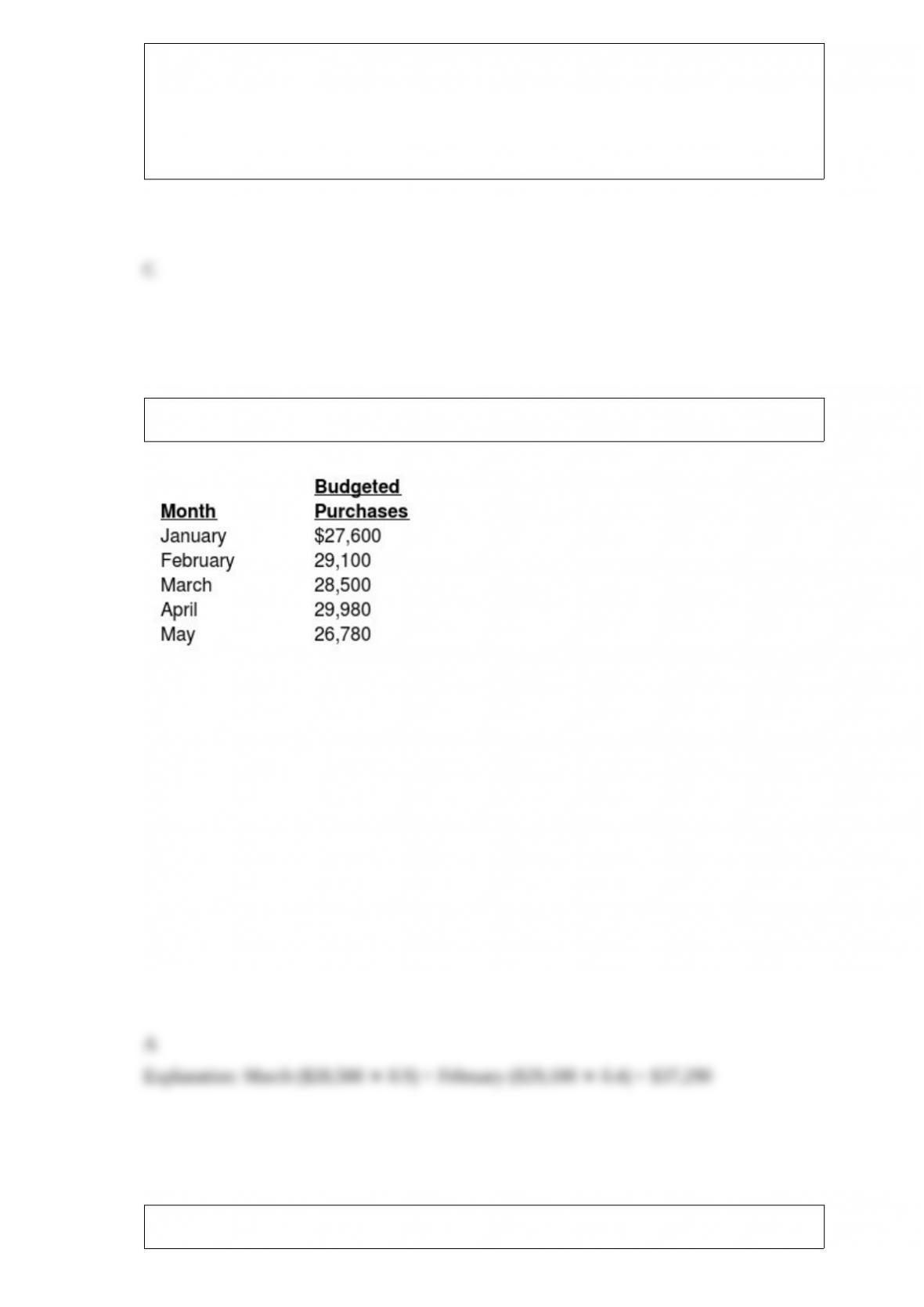

Estate Corp., has the following information:

Purchases are paid for in the following manner:

10% of the purchase amount in the month of purchase

50% of the purchase amount in the month after purchase

40% of the purchase amount in the second month after purchase

What is the expected balance in Accounts Payable as of March 31?

A) $37,290

B) $14,250

C) $2,910

D) $25,650

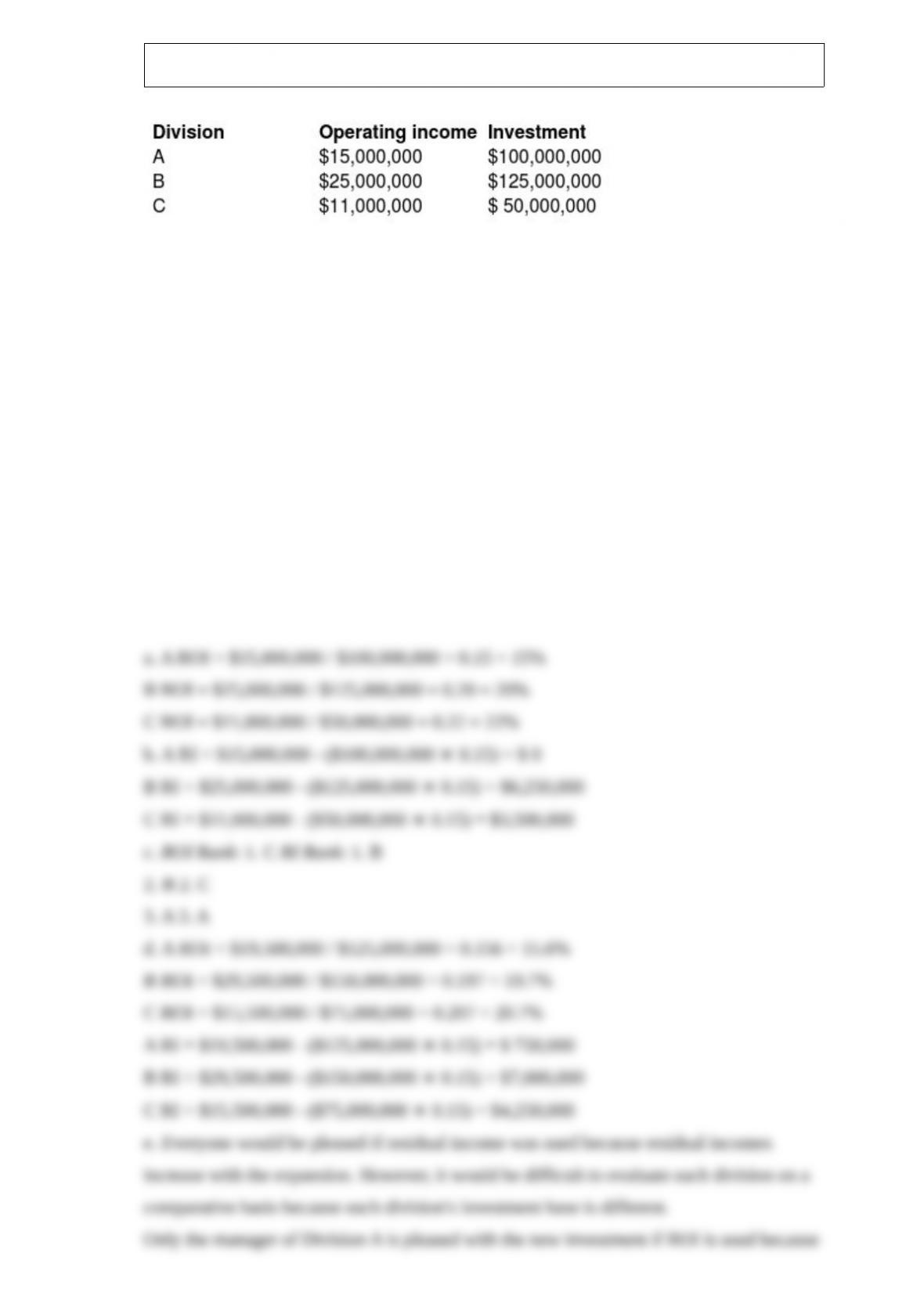

Capital Investments has three divisions. Each division’s required rate of return is 15%.

Planned operating results for 2015 are as follows:

The company is planning an expansion, which will require each division to increase its

investments by $25,000,000 and its income by $4,500,000.

Required:

a. Compute the current ROI for each division.

b. Compute the current residual income for each division.

c. Rank the divisions according to their current ROIs and residual incomes.

d. Determine the effects after adding the new project to each division’s ROI and residual

income.

e. Assuming the managers are evaluated on either ROI or residual income, which divisions

are pleased with the expansion and which ones are unhappy?

Assembly department of Zahra Technologies had 100 units as work in process at the

beginning of the month. These units were 45% complete. It has 200 units which are

20% complete at the end of the month. During the month, it completed and transferred

500 units. Direct materials are added at the beginning of production. Conversion costs

are allocated evenly throughout production. Zahra uses weighted-average

process-costing method. What is the total equivalent units in ending inventory for

assignment of direct materials cost?

A) 100 units

B) 40 units

C) 160 units

D) 200 units

When analyzing the change in operating income, the strategy component of

price-recovery ________.

A) calculations are similar to the efficiency-variance calculations

B) compares the change in output price with the changes in input prices

C) will report a large positive amount when a company has successfully pursued the

cost leadership strategy

D) isolates the change attributed solely to an increase in production efficiencies

After conducting a market research study, Magnificent Manufacturing decided to

produce a new interior door to complement its exterior door line. It is estimated that the

new interior door can be sold at a target price of $250. The annual target sales volume

for interior doors is 28,000. Magnificent has target operating income of 40% of sales.

What is the target operating income?

A) $2,800,000

B) $4,200,000

C) $7,000,000

D) $9,800,000

Transferred-in costs are treated as if they are ________.

A) conversion costs added at the beginning of the process

B) costs of beginning inventory added at the beginning of the process

C) direct labor costs added at the beginning of the process

D) a separate direct material added at the beginning of the process

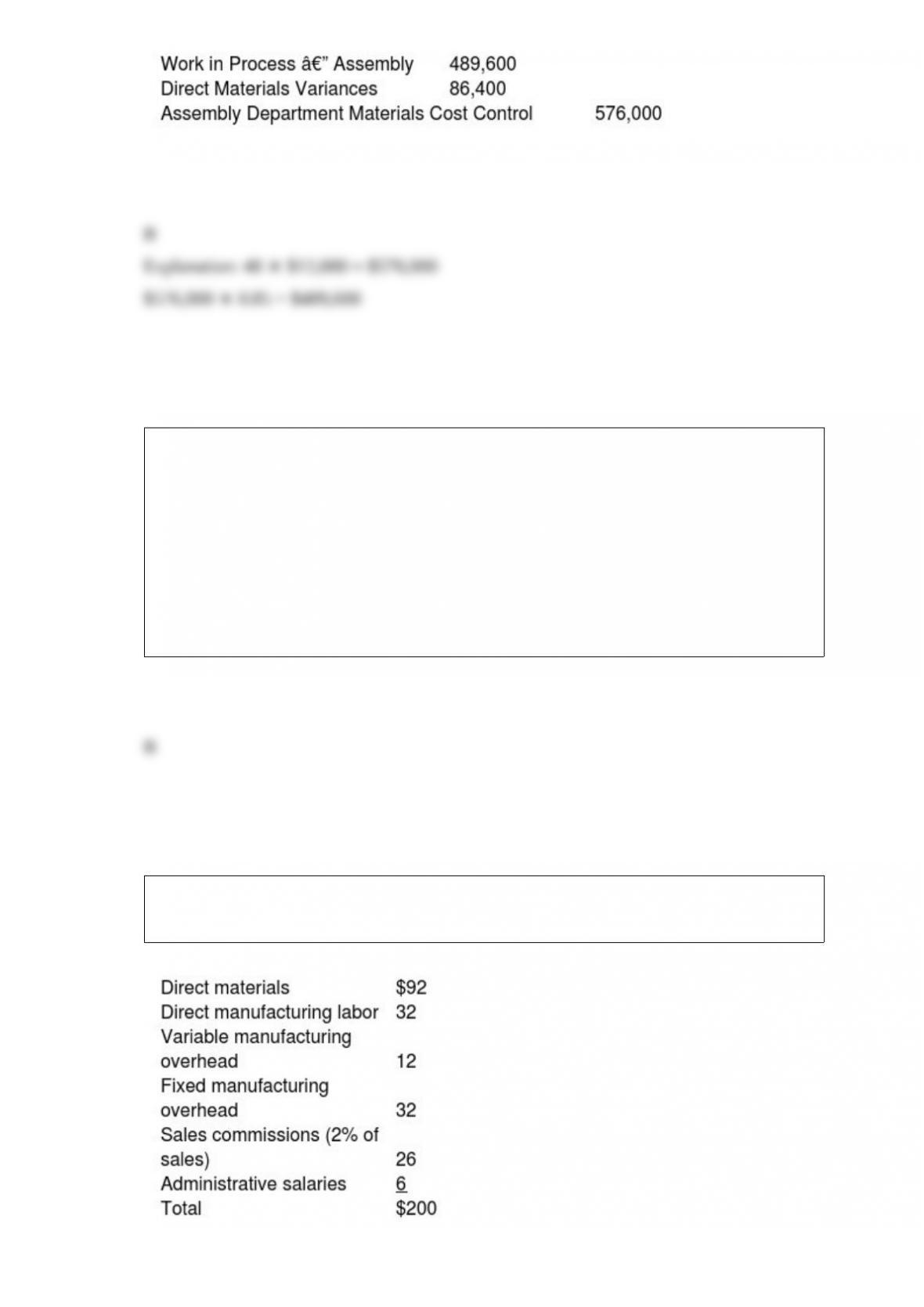

Emerging Dock Company manufactures boat docks on an assembly line. Its standard

costing system uses two cost categories, direct materials and conversion costs. Each

product must pass through the Assembly Department and the Finishing Department.

Direct materials are added at the beginning of the production process. Conversion costs

are allocated evenly throughout production.

Which of the following journal entries records the standard costs of direct materials

assigned to units worked on and total direct materials variances assuming that the

Assembly Department used 15% less materials than expected?

A)

B)

C)

D)

Cost variances should be investigated ________.

A) when they are considered within the “in-control” range as determined by

management

B) when the variance is more than a certain percentage of budgeted costs, as determined

by management

C) even though the cost of investigation exceeds the benefit as determined by

management

D) when the variance is less than a certain percentage of budgeted costs, as determined

by management

The East Company manufactures several different products. Unit costs associated with

Product ORD105 are as follows:

What is the percentage of the total variable costs per unit associated with Product ORD105

with respect to total cost?

A) 81%

B) 68%

C) 84%

D) 71%

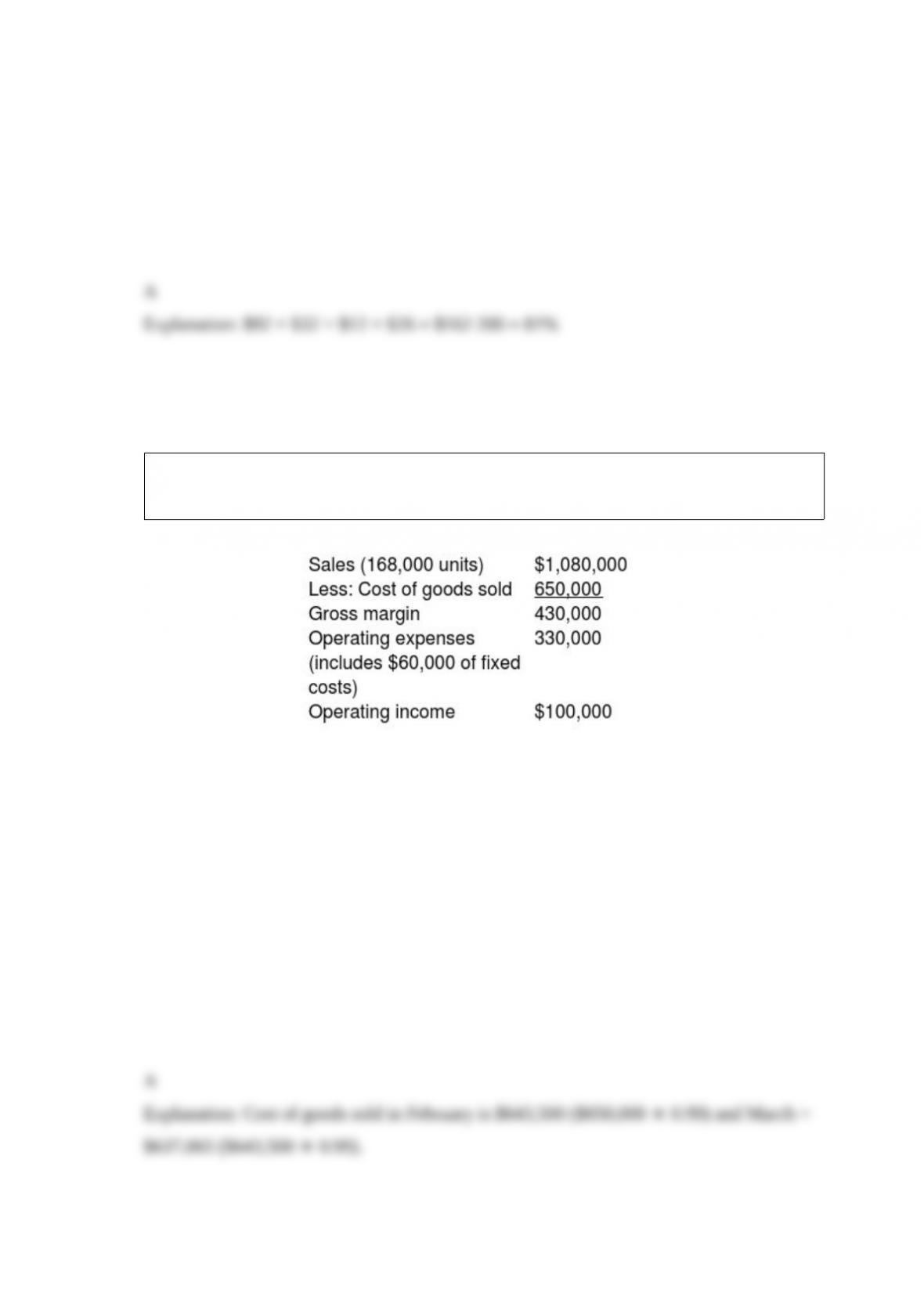

Sherry and John Enterprises are using the kaizen approach to budgeting for 2018. The

budgeted income statement for January 2018 is as follows:

Under the kaizen approach, cost of goods sold and variable operating expenses are

budgeted to decline by 1% per month.

What is budgeted cost of goods sold for March 2018?

A) $637,065

B) $656,500

C) $650,000

D) $643,500

Which of the following would be subtracted from sales while calculating contribution

margin in a variable costing format of an operating income statement?

A) Direct labor in factory

B) Rent on factory building

C) Rent on the headquarters building

D) Sales commission on incremental sales

Total manufacturing costs equal ________.

A) direct materials plus prime costs

B) direct materials plus conversion costs

C) direct manufacturing labor costs plus sunk costs

D) direct manufacturing labor costs plus conversion costs

Which component of strategy measures the reduction in costs attributable to a reduction

in the quantity of inputs used in Year 2 relative to the quantity of inputs that would have

been used in Year 1 to produce the Year 2 output?

A) the growth component

B) the price-recovery component

C) the productivity component

D) the cost leadership component

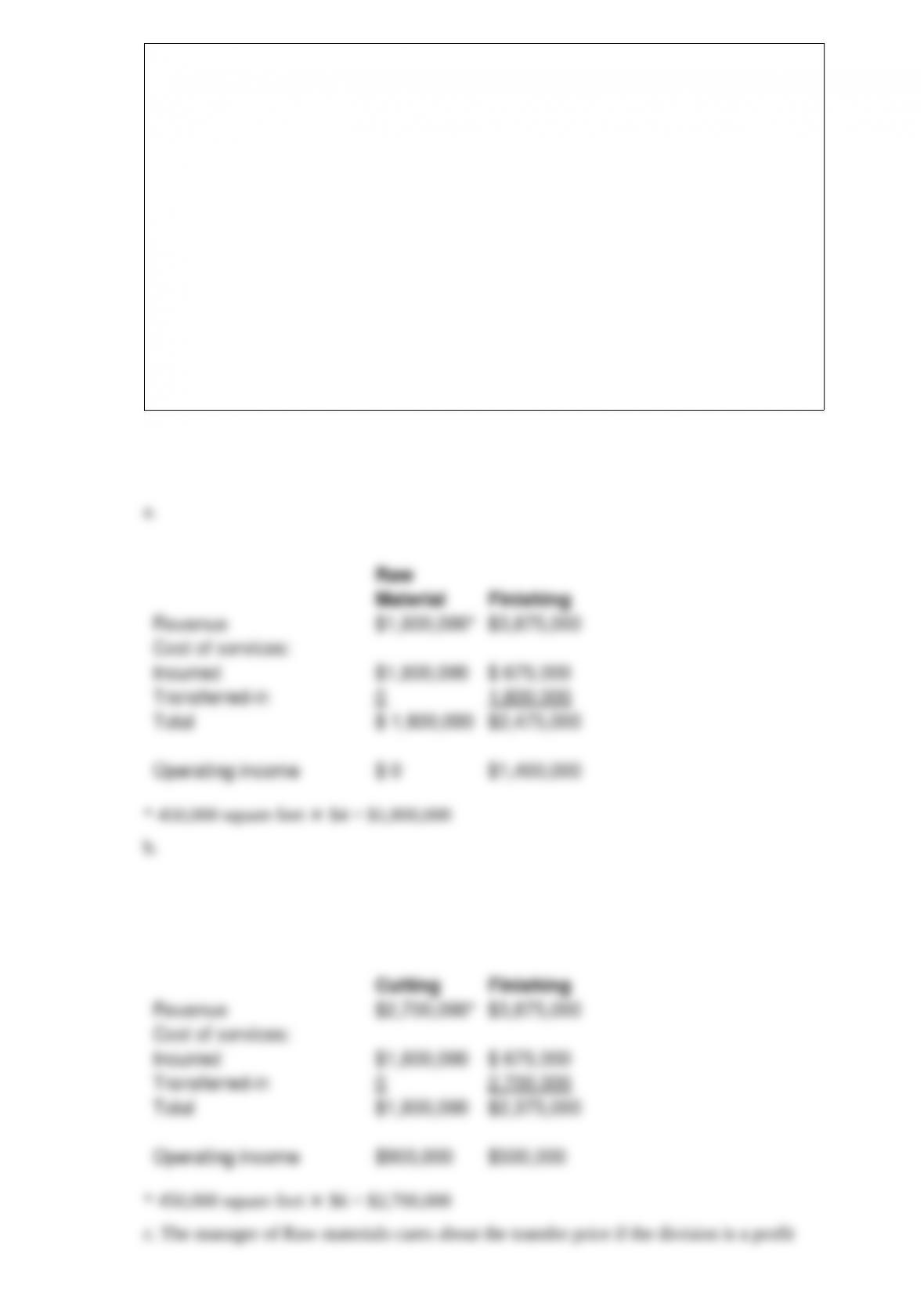

Sandra’s Sheet Metal Company has two divisions. The Raw Material Division prepares

sheet metal at its warehouse facility. The Finishing Division prepares the cut sheet

metal into finished products for the air conditioning industry. No inventories exist in

either division at the beginning of 20X8. During the year, the Raw Material Division

prepared 450,000 square feet of sheet metal at a cost of $1,800,000. All the sheet metal

was transferred to the Finishing Division, where additional operating costs of $1.50 per

square foot were incurred. The 450,000 square feet of finished fabricated sheet metal

products were sold for $3,875,000.

Required:

a. Determine the operating income for each division if the transfer price from Raw

Material to Finishing is at a cost of $4 per square foot.

b. Determine the operating income for each division if the transfer price is $6 per

square foot.

c. Since the Raw Materials Division sells all of its sheet metal internally to the

Finishing Division, does the Raw Materials manager care what price is selected? Why?

Should the Raw Materials Division be a cost center or a profit center under the

circumstances?

Explain capital budgeting and then briefly discuss each of the five stages of a capital

budgeting project?

When a unit has to be reworked, the rework may be classified in three ways. What are

those ways, and how does the accounting for each differ?

Describe the purpose of variance analysis.

What are control charts and how can inferences be drawn from them?

What are the factors that affect the classification of a cost as direct or indirect?

Discuss in brief how easy it is for companies to classify products as main products,

joint products, and byproducts.

List the capital budgeting methods used to analyze financial information.

An important element in designing accounting-based performance measures is choosing

the time horizon of the performance measures. Discuss.

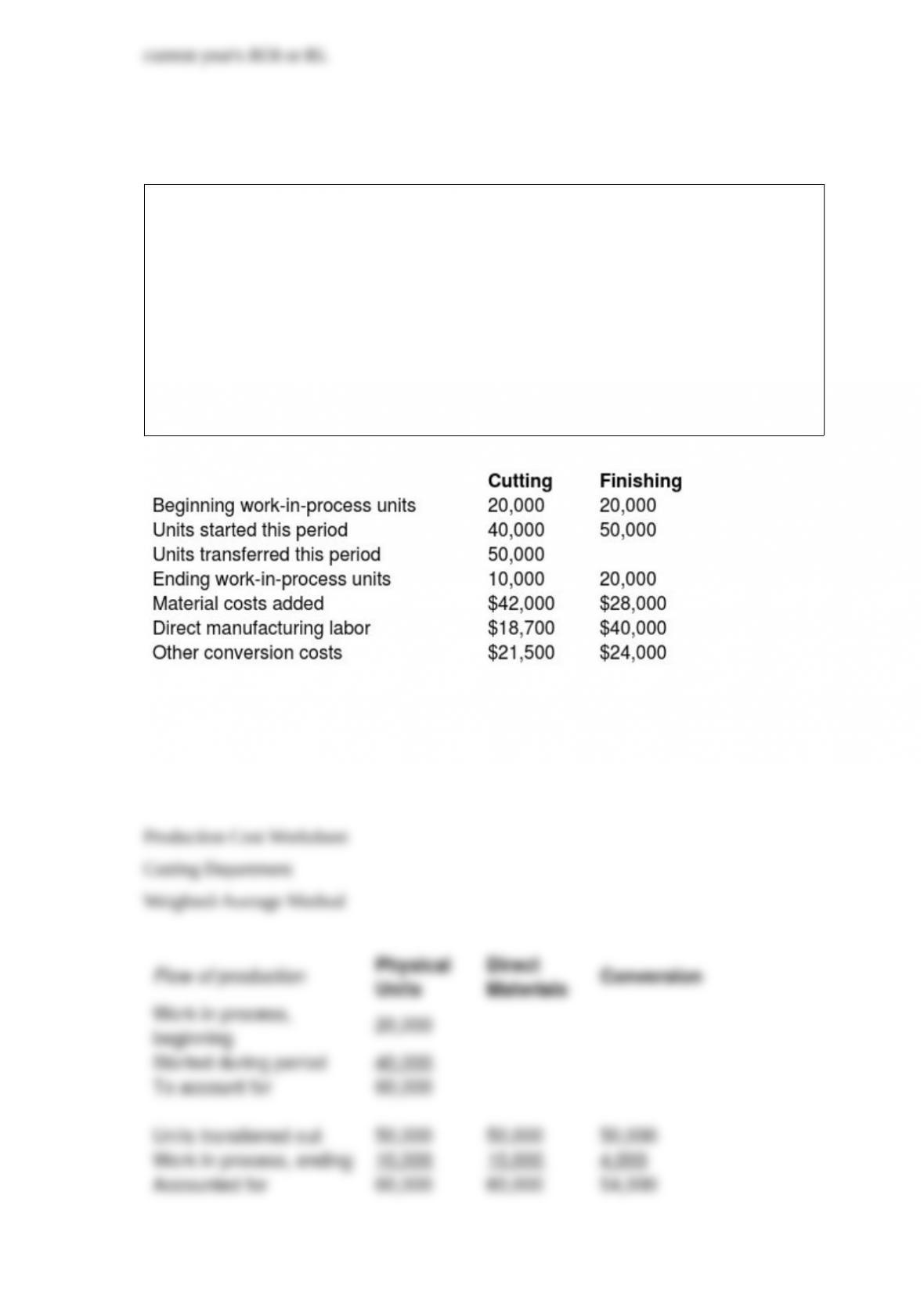

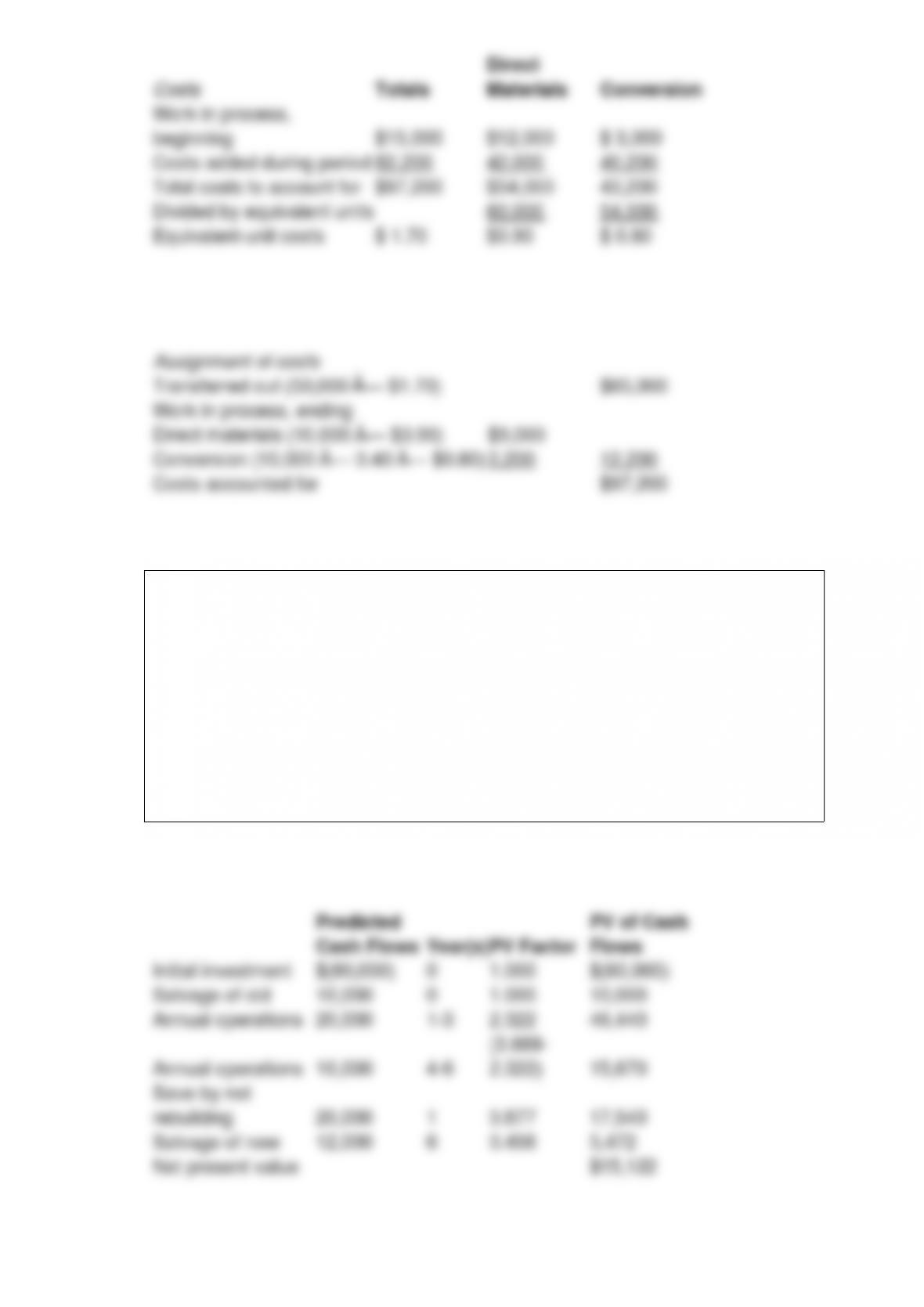

Otylia Manufacturing Company assembles its product in several departments. It has

two departments that process all units. During February, the beginning work in process

in the cutting department was half completed as to conversion, and complete as to direct

materials. The beginning inventory included $12,000 for materials and $3,000 for

conversion costs. Ending work-in-process inventory in the cutting department was 40%

complete. Direct materials are added at the beginning of the process.

Beginning work in process in the finishing department was 75% complete as to

conversion. Beginning inventories included $16,000 for transferred-in costs and

$20,000 for conversion costs. Ending inventory was 25% complete. Additional

information about the two departments follows:

Required:

Prepare a production cost worksheet using weighted-average for the cutting department.

ABC Boat Company is interested in replacing a molding machine with a new improved

model. The old machine has a salvage value of $10,000 now and a predicted salvage

value of $4,000 in six years, if rebuilt. If the old machine is kept, it must be rebuilt in

one year at a predicted cost of $20,000.

The new machine costs $80,000 and has a predicted salvage value of $12,000 at the end

of six years. If purchased, the new machine will allow cash savings of $20,000 for each

of the first three years, and $10,000 for each year of its remaining six-year life.

Required:

What is the net present value of purchasing the new machine if the company has a

required rate of return of 14%?

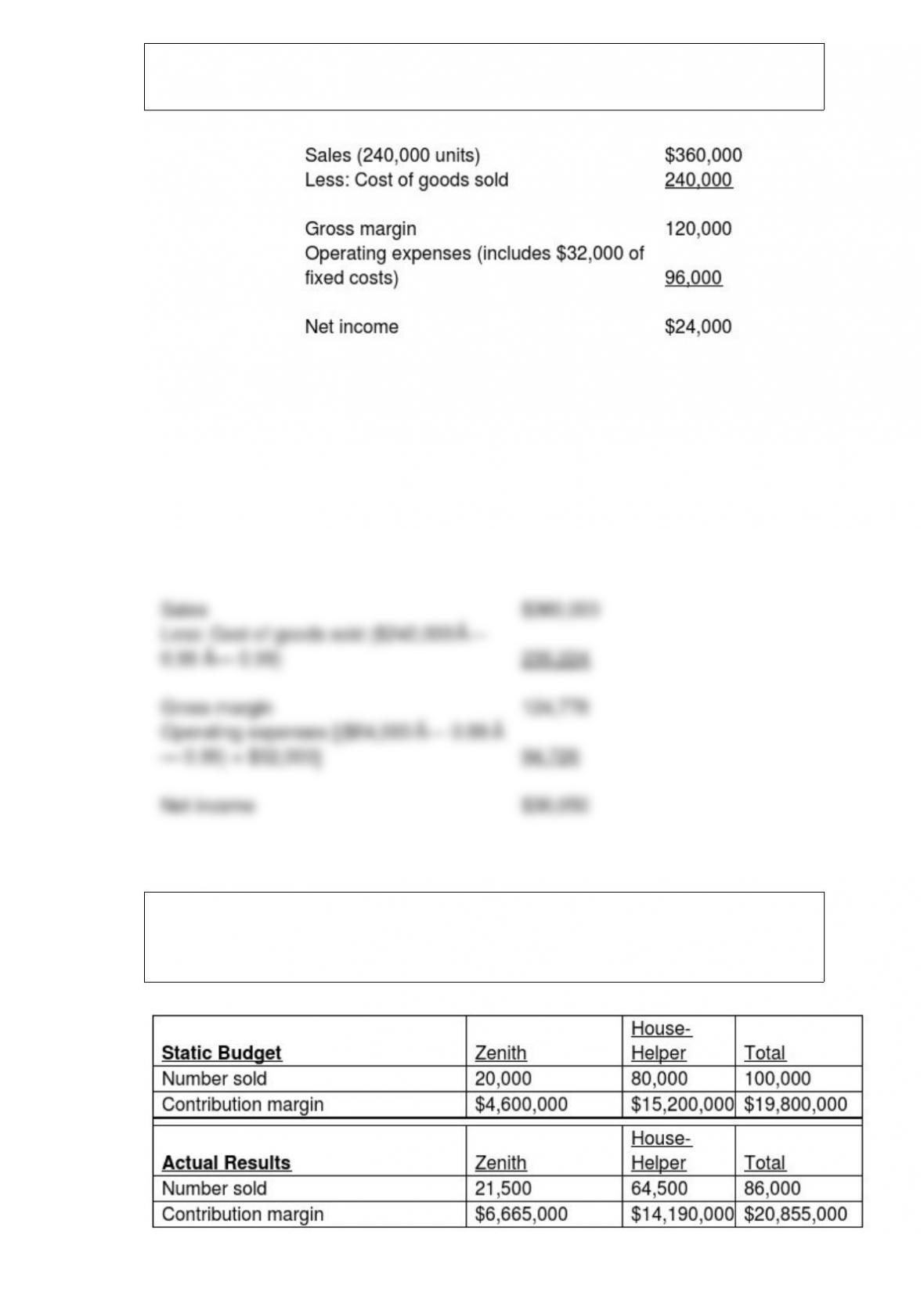

Steve Corporation is using the kaizen approach to budgeting for 2018. The budgeted

income statement for January 2018 is as follows:

Under the kaizen approach, cost of goods sold and variable operating expenses are

budgeted to decline by 1% per month.

Required:

Prepare a kaizen-based budgeted income statement for March of 2018.

The Octova Corporation manufactures two types of vacuum cleaners: the ZENITH for

commercial building use and the House-Helper for residences. Budgeted and actual

operating data for the year 2017 are as follows:

Required:

Compute the sales-mix variance and the sales-quantity variance by type of vacuum

cleaner, and in total. (in terms of the contribution margin)

Define engineered and discretionary costs and give two examples of each.

Generally, companies follow one of two broad strategies: offering a quality product at a

low price, or offering a unique product or service priced higher than the competition. Is

it possible to follow a strategy that is “in the middle”?

When is a company said to be engaged in predatory pricing? What are the primary

conditions to be satisfied to prove predatory pricing?

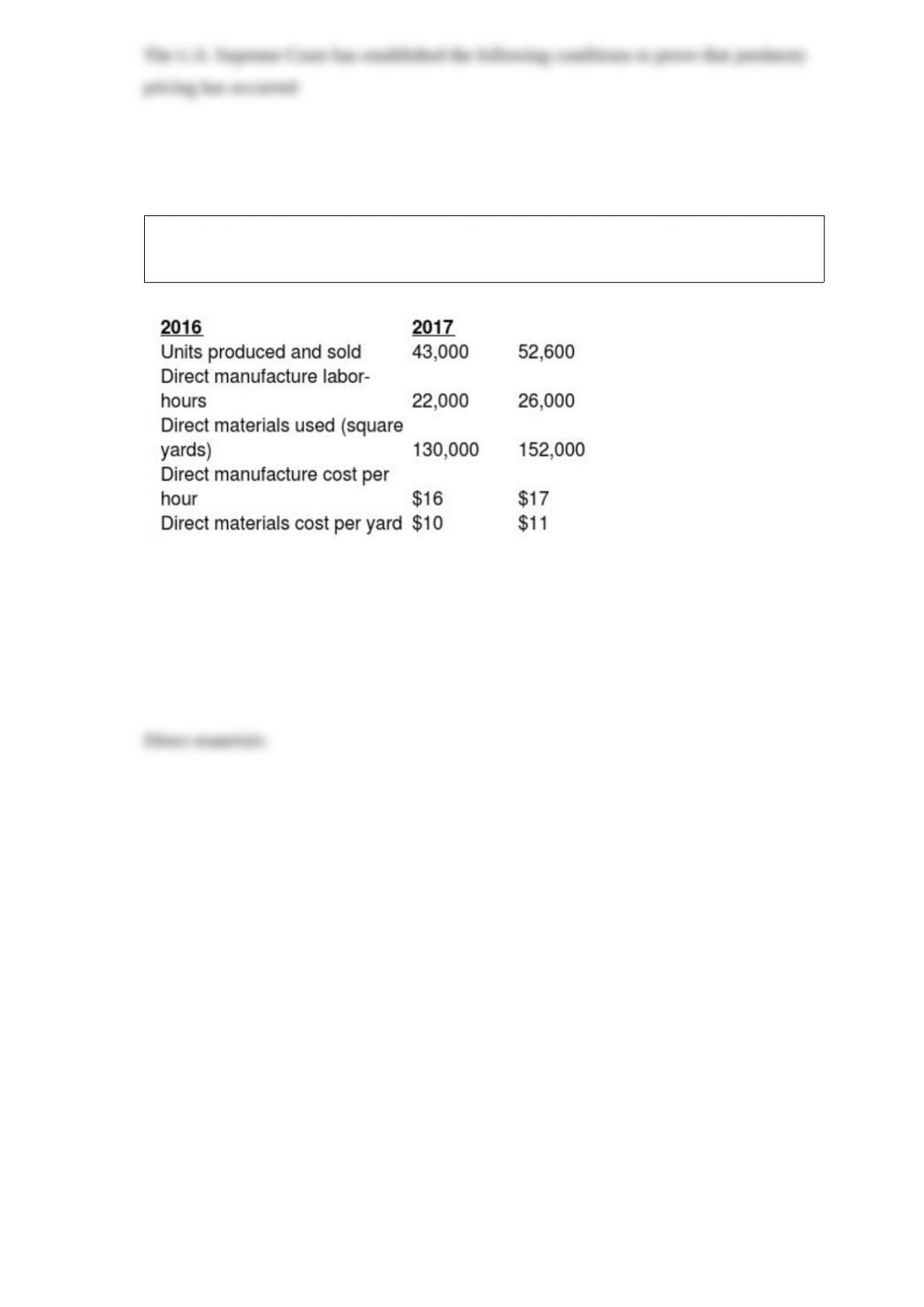

Fairytale Weddings manufactures wedding dresses. The following information relates to

the manufacture of gowns in its Providence plant:

Required:

Prepare an analysis of change in annual costs from 2016 to 2017 including direct materials,

direct manufacturing labor, and total inputs.

What is the difference between a weighted-average method of process costing and a

first-in, first-out method of process costing?

Why would a manager perform customer-profitability analysis?