SOLUTION

(20–30 min.) Kaizen approach to activity-based budgeting (continuation of 6-30).

1.

Budgeted Cost-Driver Rates

Activity Cost Hierarchy January February March

Ordering

Batch-level

$45.00

$44.82000a

$44.64072b

The March 2018 rates can be used to compute the total budgeted cost for each activity area in

March 2018:

Activity

Cost

Hierarchy

Soft

Drinks

Fresh

Produce

Packaged

Food Total

Ordering

´

Customer support

Total

2. A Kaizen budgeting approach signals management’s commitment to systematic cost

reduction. Compare the budgeted costs from Question 6-30 and 6-31.

Ordering Delivery

Shelf-Stocki

ng

Customer

Support

Exercise 6-30 $2,340 $3,813 $2,961 $4,460

The Kaizen budget number will show unfavorable variances for managers whose activities

One limitation of Kaizen budgeting, as illustrated in this question, is that it assumes small

incremental improvements each month. It is possible that some cost improvements arise from

6-1

A second limitation is the difficulty and challenge of determining the rate of improvement

(0.4% in this example) and whether a constant percentage improvement can be sustained over a

6-32 Responsibility and controllability. Consider each of the following independent

situations for Prestige Fountains. Prestige manufactures and sells decorative fountains for

commercial properties. The company also contracts to service both its own and other brands of

fountains. Prestige has a manufacturing plant, a supply warehouse that supplies both the

manufacturing plant and the service technicians (who often need parts to repair fountains), and

12 service vans. The service technicians drive to customer sites to service the fountains. Prestige

owns the vans, pays for the gas, and supplies fountain parts, but the technicians own their own

tools.

1. In the manufacturing plant, the production manager is not happy with the motors that the

purchasing manager has been purchasing. In May, the production manager stops requesting

motors from the supply warehouse and starts purchasing them directly from a different motor

manufacturer. Actual materials costs in May are higher than budgeted.

2. Overhead costs in the manufacturing plant for June are much higher than budgeted.

Investigation reveals a utility rate hike in effect that was not figured into the budget.

3. Gasoline costs for each van are budgeted based on the service area of the van and the amount

of driving expected for the month. The driver of van 3 routinely has monthly gasoline costs

exceeding the budget for van 3. After investigating, the service manager finds that the driver

has been driving the van for personal use.

4. Regency Mall, one of Prestige’s fountain service customers, calls the service people only for

emergencies and not for routine maintenance. Thus, the materials and labor costs for these

service calls exceeds the monthly budgeted costs for a contract customer.

5. Prestige’s service technicians are paid an hourly wage of $22, regardless of experience or

time with the company. As a result of an analysis performed last month, the service manager

determined that service technicians in their first year of employment worked on average 20%

more slowly than other employees. Prestige bills customers per service call, not per hour.

6. The cost of health insurance for service technicians has increased by 40% this year, which

caused the actual health insurance costs to greatly exceed the budgeted health insurance costs

for the service technicians.

Required:

For each situation described, determine where (that is, with whom) (a) responsibility and (b)

controllability lie. Suggest ways to solve the problem or to improve the situation.

SOLUTION

(15 min.) Responsibility and controllability.

1. (a) Production manager

6-2

(b) Purchasing Manager

The purchasing manager has control of the cost to the extent that he/she is doing the purchasing

and can seek or contract for the best price. The production manager should work with the

2. (a) Production Manager

(b) External Forces

In the case of the utility rate hike, the production manager would be responsible for the costs, but

3. (a) Van 3 driver

(b) Service manager

The driver of each van has the responsibility to stay within budget for the costs of the service

4. (a) Prestige’s service manager

(b) Regency manager

5. (a) Service manager

(b) Service manager

6. (a) Service manager

(b) External forces

6-3

6-33 Responsibility, controllability, and stretch targets. Consider each of the following

independent situations for Sunrise Tours, a company owned by David Bartlett that sells motor

coach tours to schools and other groups. Sunshine Tours owns a fleet of 10 motor coaches and

employs 12 drivers, maintenance technician, 3 sales representatives, and an office manager.

Sunshine Tours pays for all fuel and maintenance on the coaches. Drivers are paid $0.50 per

mile while in transit, plus $15 per hour while idle (time spent waiting while tour groups are

visiting their destinations). The maintenance technician and office manager are both full-time

salaried employees. The sales representatives work on straight commission.

1. When the office manager receives calls from potential customers, she is instructed to handle

the contracts herself. Recently, however, the number of contracts written up by the office

manager has declined. At the same time, one of the sales representatives has experienced a

significant increase in contracts. The other two representatives believe that the office

manager has been colluding with the third representative to send him the prospective

customers.

2. One of the motor coach drivers seems to be reaching his destinations more quickly than any

of the other drivers and is reporting longer idle time.

3. Regular preventive maintenance of the motor coaches has been proven to improve fuel

efficiency and reduce overall operating costs by averting costly repairs. During busy

months, however, it is difficult for the maintenance technician to complete all of the

maintenance tasks within his 40-hour workweek.

4. David Bartlett has read about stretch targets, and he believes that a change in the

compensation structure of the sales representatives may improve sales. Rather than a straight

commission of 10% of sales, he is considering a system where each representative is given a

monthly goal of 50 contracts. If the goal is met, the representative is paid a 12% commission.

If the goal is not met, the commission falls to 8%. Currently, each sales representative

averages 45 contracts per month.

5. Fuel consumption has increased significantly in recent months. David Bartlett is considering

ways to promote improved fuel efficiency and reduce harmful emissions using stretch

environmental targets, where drivers and the maintenance mechanic would receive a bonus if

fuel consumption falls below 90% of budgeted fuel usage per mile driven.

Required:

For situations 1–3, discuss which employee has responsibility for the related costs and the extent

to which costs are controllable and by whom. What are the risks or costs to the company? What

can be done to solve the problem or improve the situation? For situations 4 and 5, describe the

potential benefits and costs of establishing stretch targets.

SOLUTION

6-4

(15 min.) Responsibility, controllability, and stretch targets.

1. The office manager has the responsibility to follow company guidelines and write contracts

2. Each driver is responsible for controlling and keeping an accurate accounting of his or her

3. The maintenance technician is clearly responsible for completing all of the preventative

maintenance. Requiring the technician to work significant overtime will likely decrease his

4. The maintenance technician is clearly responsible for completing all of the preventative

5. Bartlett has designed the stretch target system correctly. Taking advantage of loss aversion,

In establishing “stretch targets,” Bartlett should be sure that there are sufficient potential

5. The drivers are responsible for driving the motor coaches at fuel-efficient speeds on the

highway. The maintenance technician is responsible for maintaining the vehicles to improve

6-5

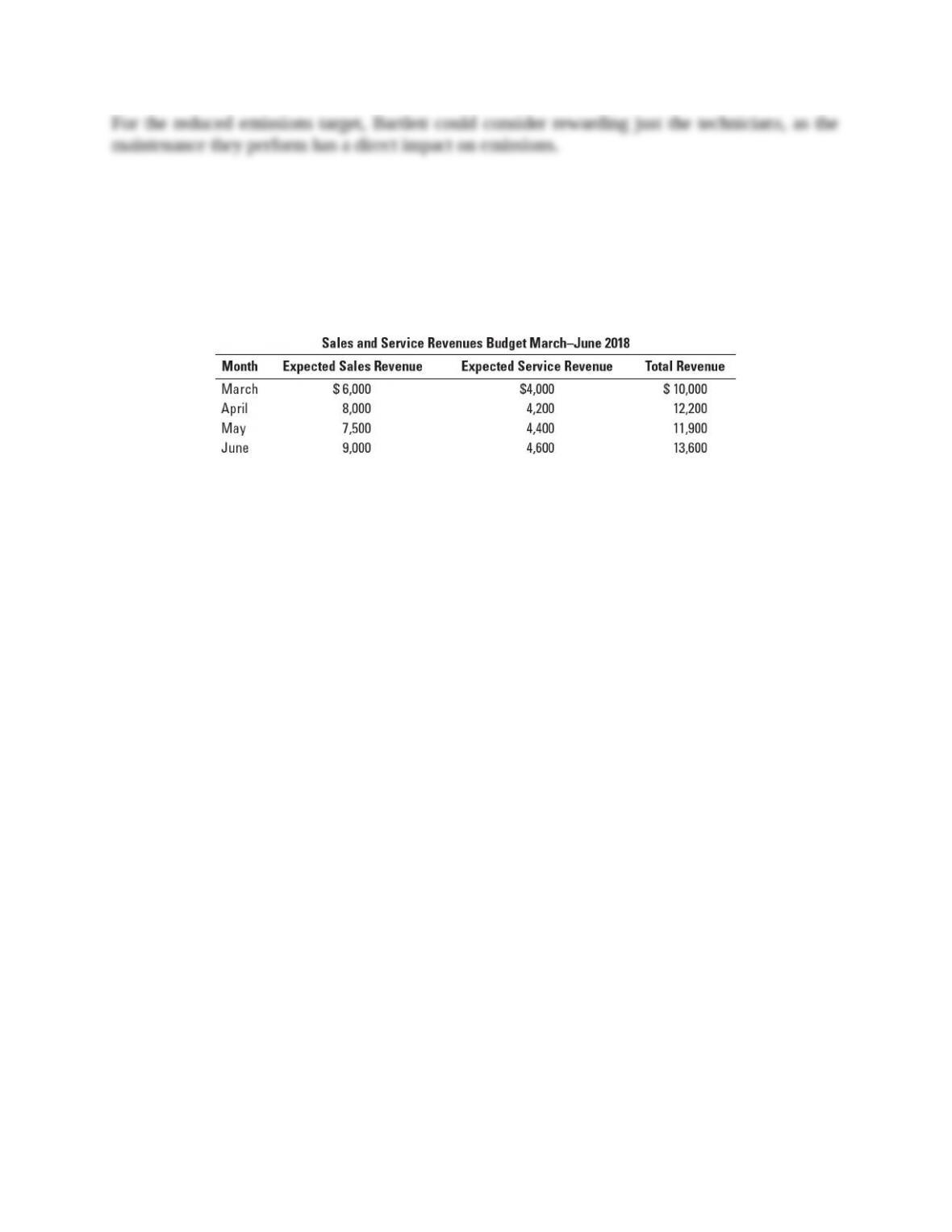

6-34 Cash flow analysis, sensitivity analysis. HealthMart is a retail store selling home oxygen

equipment. HealthMart also services home oxygen equipment, for which the company bills

customers monthly. HealthMart has budgeted for increases in service revenue of $200 each month

due to a recent advertising campaign. The forecast of sales and service revenue for the

March–June 2018 is as follows:

Almost all of the sales revenues of the oxygen equipment are credit card sales; cash sales are

negligible. The credit card company deposits 97% of the revenues recorded each day into

HealthMart’s account overnight. For the servicing of home oxygen equipment, 60% of oxygen

services billed each month is collected in the month of the service, and 40% is collected in the

month following the service.

Required:

1. Calculate the cash that HealthMart expects to collect in April, May, and June 2018 from sales

and service revenues. Show calculations for each month.

2. HealthMart has budgeted expenditures for May of $11,000 and requires a minimum cash

balance of $250 at the end of each month. It has a cash balance on May 1 of $400.

a. Given your answer to requirement 1, will HealthMart need to borrow cash to cover its

payments for May and maintain a minimum cash balance of $250 at the end of May?

b. Assume (independently for each situation) that (1) May total revenues might be 10% lower

or that (2) total costs might be 5% higher. Under each of those two scenarios, show the total

net cash for May and the amount HealthMart would have to borrow to cover its cash

payments for May and maintain a minimum cash balance of $250 at the end of May. (Again,

assume a balance of $400 on May 1.)

3. Why do HealthMart’s managers prepare a cash budget in addition to the revenue, expenses,

and operating income budget? Has preparing the cash budget been helpful? Explain briefly.

SOLUTION

(30 min.) Cash flow analysis, sensitivity analysis.

1. The cash that HealthMart can expect to collect during April, May and June is calculated

below.

6-6

Cash collected in April May June

From sales revenue (credit cards)

From service revenue

2. (a) Beginning balance $400 + Collections $11,595 – Expenditures $11,000 = $995. Yes,

HealthMart will be able to cover the budgeted expenditures and maintain a minimum ending

balance of more than $250.

(b)

Original

numbers

May

Revenues

decrease

10%

May Costs

increase 5%

3. HealthMart’s managers prepare a cash budget in addition to the operating income budget

to plan cash flows to ensure that the company has adequate cash to pay vendors, meet payroll,

and pay operating expenses as these payments come due. HealthMart could be very profitable on

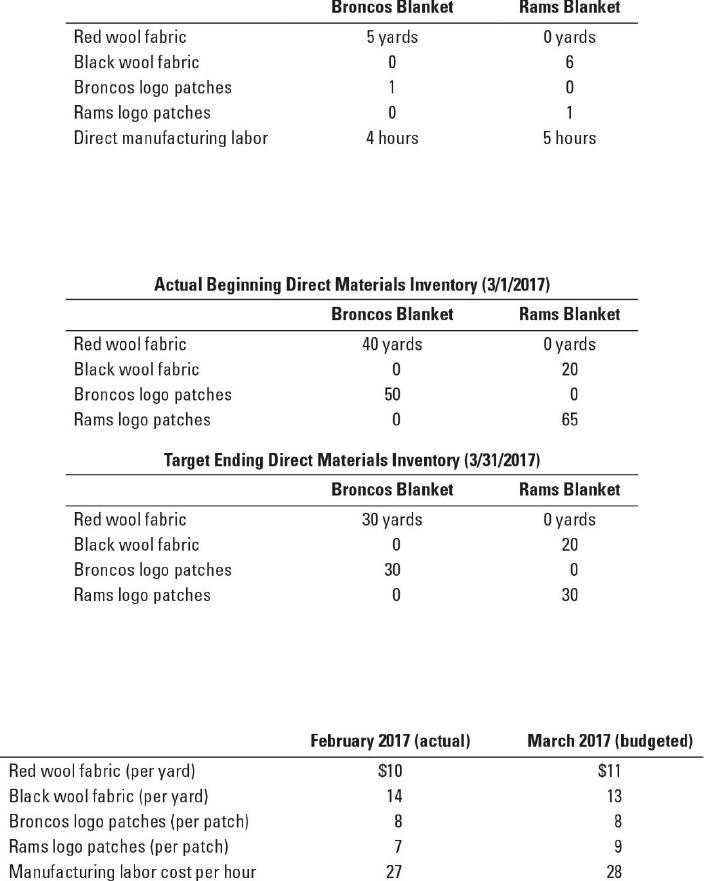

6-35 Budget schedules for a manufacturer. Hale Specialties manufactures, among other

things, woolen blankets for the athletic teams of the two local high schools. The company sews

the blankets from fabric and sews on a logo patch purchased from the licensed logo store site.

The teams are as follows:

6-7

• Broncos, with red blankets and the Broncos logo

• Rams, with black blankets and the Rams logo

Also, the black blankets are slightly larger than the red blankets.

The budgeted direct-cost inputs for each product in 2017 are as follows:

Unit data pertaining to the direct materials for March 2017 are as follows:

Unit cost data for direct-cost inputs pertaining to February 2017 and March 2017 are as follows:

Manufacturing overhead (both variable and fixed) is allocated to each blanket on the basis of

budgeted direct manufacturing labor-hours per blanket. The budgeted variable manufacturing

overhead rate for March 2017 is $17 per direct manufacturing labor-hour. The budgeted fixed

manufacturing overhead for March 2017 is $14,625. Both variable and fixed manufacturing

overhead costs are allocated to each unit of finished goods.

Data relating to finished-goods inventory for March 2017 are as follows:

6-8

Budgeted sales for March 2017 are 140 units of the Broncos blankets and 195 units of the Rams

blankets. The budgeted selling prices per unit in March 2017 are $305 for the Broncos blankets

and $378 for the Rams blankets. Assume the following in your answer:

• Work-in-process inventories are negligible and ignored.

• Direct materials inventory and finished-goods inventory are costed using the FIFO method.

• Unit costs of direct materials purchased and finished goods are constant in March 2017.

Required:

1. Prepare the following budgets for March 2017:

a. Revenues budget

b. Production budget in units

c. Direct material usage budget and direct materials purchases budget

d. Direct manufacturing labor costs budget

e. Manufacturing overhead costs budget

f. Ending inventories budget (direct materials and finished goods)

g. Cost of goods sold budget

2. Suppose Hale Specialties decides to incorporate continuous improvement into its budgeting

process. Describe two areas where it could incorporate continuous improvement into the

budget schedules in requirement 1.

6-9