The benefits of implementing a more-complex cost allocation system are relatively easy

to quantify for application of the cost-benefit approach.

The sales method for recognizing byproducts is conceptually correct because it is

consistent with the matching principle.

Job-costing systems separate costs into cost categories according to when costs are

introduced into the process of manufacture.

Indirect manufacturing costs are also referred to as manufacturing overhead costs or

factory overhead costs.

When production is less than sales, operating income will be the same regardless of

whether variable cost or absorption costing is used.

Two or more support departments whose costs are being allocated can also provide

support to each other and as well as to operating departments.

Rework is an example of a value-added cost.

Incremental revenue is the sum of differential revenues of two alternatives.

A budgeted indirect-cost rate is computed for each cost pool using budgeted indirect

costs and the budgeted quantity of the cost-allocation base.

A lease for a store calls for a base monthly rent of $1,500 up to $10,000 of sales with a

possible additional monthly cost of 2% of sales over $10,000. The rent is a fixed cost

for the month for a relevant range of zero to $10,000 sales.

Effective management control systems should also motivate managers and other

employees.

Management accountants work closely with managers in various departments to

formulate strategies by providing information about the sources of competitive

advantage.

If the selling subunit is operating at capacity, the opportunity cost of transferring a unit

internally rather than selling it externally is equal to the market price minus the variable

cost.

Inventory management is the planning, organizing, and controlling activities that focus

on the flow of materials into, through, and out of the organization.

In a profit center, the manager is accountable for investments, revenues, and costs.

Differential revenue is the additional total revenue from an activity.

The last step in the five-step procedure for process costing with spoilage is to

summarize total costs to account for.

The quantitative analysis method uses a formal mathematical method to identify

cause-and-effect relationships among past data observations.

When using a control chart, the observations outside the upper and lower control limits

are ordinarily regarded as nonrandom and worth investigating.

In successful quality programs, companies decrease costs of quality and, in particular,

internal and external failure costs as a percentage of revenues.

Most computer-based financial planning models have difficulty incorporating

sensitivity (what-if) analysis.

Depreciation allocated to a product line is a relevant cost when deciding to discontinue

that product.

Managers can use variance analysis to make decisions about the mix of products to

make.

Corporate brand advertising and general administration costs are examples of corporate

costs.

In joint costing, the constant gross-margin percentage method recognizes that the profit

margin is not just attributable to the joint process but is also derived from the costs

incurred after split-off.

Scrap and rework are considered to be the same thing by managerial accountants.

The cost of units completed can differ materially between the weighted average and the

FIFO methods of process costing.

A re-design of a product so that it requires fewer components to decrease ordering,

receiving, testing, and inspection costs is an example of value-engineering.

The costs of normal spoilage are typically included as a component of the costs of good

units manufactured.

Return on sales can provide how effectively costs are managed and is part of the

DuPont method of profitability analysis.

Service-sustaining costs are the costs of activities that managers cannot trace to

individual services but that support the organization as a whole.

In a one-time special order situation, if the price offered by the buyer is less than the

absorption cost per unit, the special order may still be profitable since absorption costs

include allocated fixed manufacturing overhead.

South Coast Appliance Store is a small company that has hired you to perform some

management advisory services. The following information pertains to 2017 operations.

Sales (5,600 microwave ovens) $5,600,000

Cost of goods sold 912,800

Store manager’s salary per year 125,000

Operating costs per year 210,000

Advertising and promotion per year 31,520

Commissions (4.5% of sales) 252,000

What were the total fixed costs for 2017?

A) $1,531,320

B) $366,520

C) $335,000

D) $1,164,800

Lazy Guy Corporation manufactured 4,000 chairs during June. The following variable

overhead data relates to June:

What is the variable overhead flexible-budget variance?

A) $2,200 favorable

B) $1,480 favorable

C) $2,200 unfavorable

D) $1,480 unfavorable

The budgeting process is most strongly influenced by ________.

A) the capital budget

B) the budgeted statement of cash flows

C) the sales forecast

D) the production budget

A report showing the actual financial results for a period compared to the budgeted

financial results for that same period would most likely be called a ________.

A) strategic plan

B) management forecast

C) performance report

D) revised plan

Which of the following methods is described as the method that measures the time it

will take to recoup, in the form of future cash inflows, the total dollars invested in a

project?

A) the accrued accounting rate-of-return method

B) the payback method

C) the internal rate-of-return method

D) the book-value method

Which of the following can be a reason for a favorable price variance for direct

materials?

A) a decrease in the price of materials due to an oversupply of materials

B) an unexpected increase in the price of materials

C) less amount of material used during production than planned for actual output

D) workers taking less time to produce the products

Which of the following is a characteristic of a management control system?

A) It gathers key information that aids in the process of making decisions

B) It encourages short-term profit planning

C) Helps managers to act rapidly and with autonomy

D) It deals with coordinating planning across the organization and is not concerned with

behavioral aspects of managing

Line management includes ________.

A) distribution managers

B) human-resource managers

C) information-technology managers

D) management-accounting managers

South Coast Appliance Store is a small company that has hired you to perform some

management advisory services. The following information pertains to 2017 operations.

Sales (5,500 microwave ovens) $5,500,000

Cost of goods sold 962,500

Store manager’s salary per year 150,000

Operating costs per year 220,000

Advertising and promotion per year 18,960

Commissions (3.2% of sales) 176,000

What was the variable cost per unit sold for 2017?

A) $32.00

B) $175

C) $207.00

D) $277.72

Which of the following would be considered the biggest advantage of using practical

capacity to allocate costs?

A) focuses the user’s division with the costs of overused capacity

B) never causes over or under-allocated overhead

C) burdens the user divisions with the costs of unused capacity

D) focuses management’s attention on unused capacity

Which of the following statements is true of the methods for allocating joint costs?

A) The net realizable value method uses the sales value of the units sold during the

accounting period to allocate joint costs.

B) The sales value at split-off method always results in the same gross-margin

percentage for all products.

C) The sales value at split-off method allocates joint costs to each product in proportion

to the sales value of total production.

D) The net realizable value method results in the same joint production cost per unit for

all products.

The primary user of management accounting information is a(n) ________.

A) the controller

B) a shareholder evaluating a stock investment

C) bondholder

D) external regulator

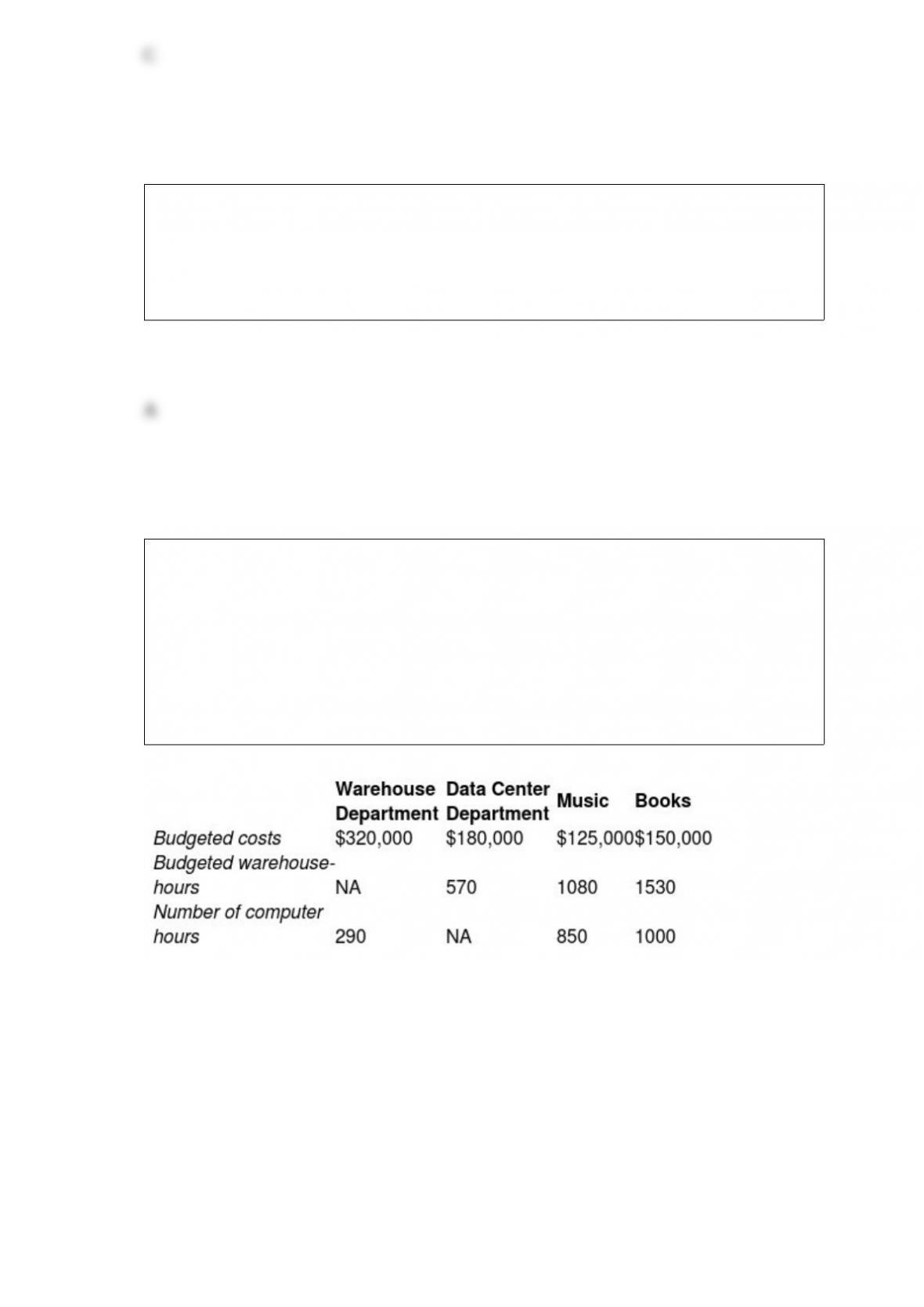

Goldfarb’s Book and Music Store has two service departments, Warehouse and Data

Center. Warehouse Department costs of $320,000 are allocated on the basis of budgeted

warehouse-hours. Data Center Department costs of $180,000 are allocated based on the

number of computer log-on hours. The costs of operating departments Music and Books

are $125,000 and $150,000, respectively. Data on budgeted warehouse-hours and

number of computer log-on hours are as follows:

Production

Support Departments Departments

Using the step-down method, what amount of Data Center Department cost will be

allocated to the Warehouse Department if the service department with the highest

percentage of interdepartmental support service is allocated first? (Round up)

A) $62,182

B) $180,000

C) $24,393

D) $0

A manufacturing plant produces two product lines: golf equipment and soccer

equipment. An example of indirect cost for the soccer equipment line is the ________.

A) material used to make the soccer balls

B) labor to shape the leather used to make the soccer ball

C) material used to manufacture the soccer studs

D) property taxes paid on the land and building (plant)

A company has operating income of $300,000, revenues of $1,500,000, total assets of

$2,000,000 and an ROI of 15%. To improve the ROI, to increase ROI to 20%, which of

the following investment turnovers would need to be achieved?

A) .75

B) 1.5

C) 1

D) 2

Under standard costing, ________.

A) fixed overhead costs are treated as if they are a variable cost

B) fixed overhead costs are treated as if they are a fixed cost

C) variable overhead costs are treated as if they are a fixed cost

D) fixed overhead costs are treated as if they are a sunk cost

Which of the following is a stage of the capital budgeting process in which a firm

obtains funding for the project?

A) make decisions by choosing among alternatives stage

B) identify projects stage

C) obtain information stage

D) implement the decision, evaluate performance, and learn stage

A company manufactures three products, A, B, and C from a single raw material input.

Product C can be sold at the split-off point for total revenues of $60,000 or it can be

processed further at a total cost of $16,000 and then sold for $78,000. Product C:

A) should be sold at the split-off point, rather than processed further.

B) would increase the company’s overall net income by $18,000 if processed further

and then sold.

C) would increase the company’s overall net income by $78,000 if processed further

and then sold.

D) would increase the company’s overall net income by $2000 if processed further and

then sold.

Orange Corporation has budgeted sales of 23,000 units, targeted ending finished goods

inventory of 9,000 units, and beginning finished goods inventory of 6,000 units. How

many units should be produced next year?

A) 38,000 units

B) 32,000 units

C) 26,000 units

D) 23,000 units

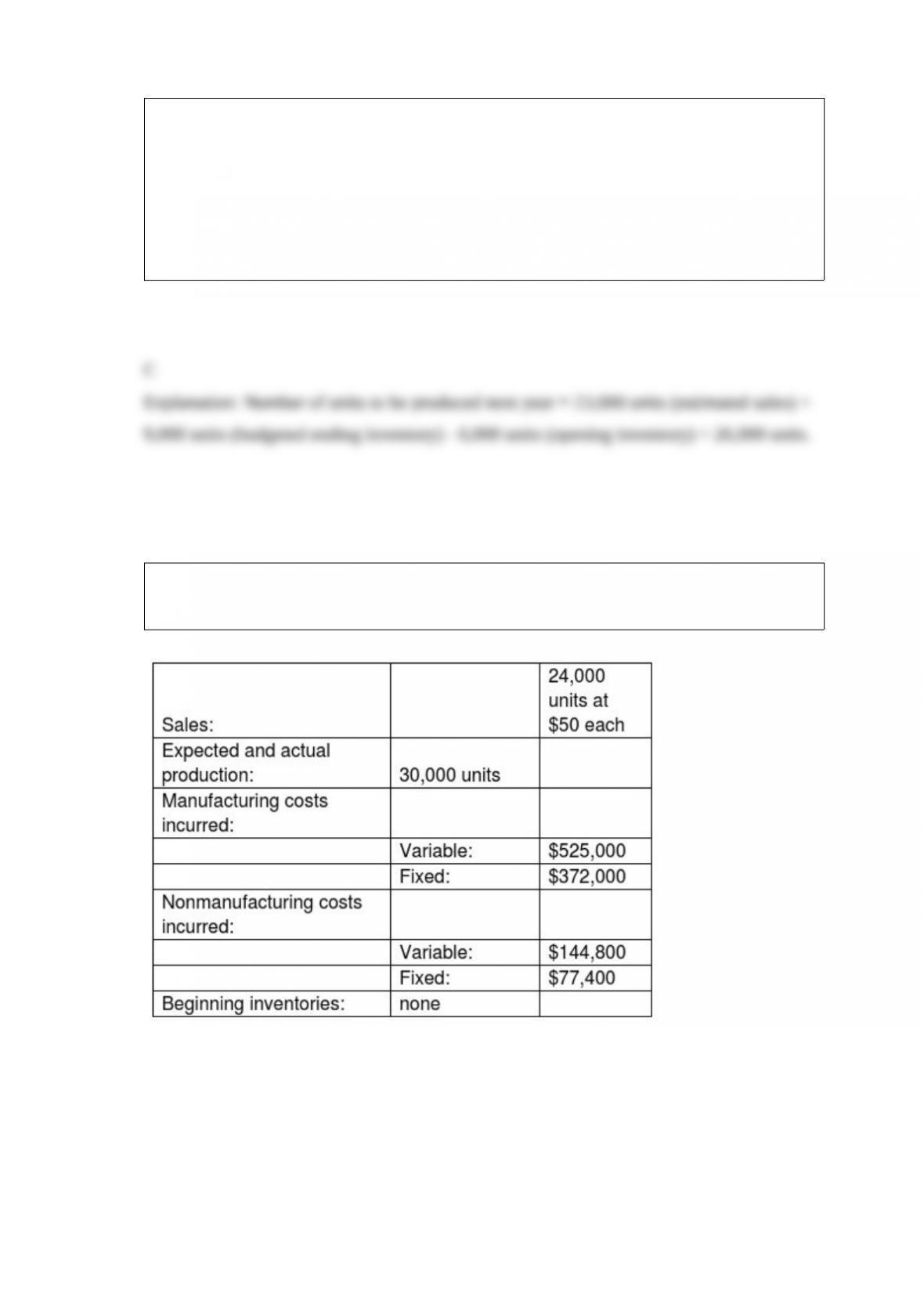

The following data are available for Brennan Soft Toys Company for the year ended

September 30, 2017.

Required:

a. Determine operating income using the variable-costing approach.

b. Determine operating income using the absorption-costing approach.

c. Explain why operating income is not the same under the two approaches.

Pederson Company reported the following:

What is the amount of gross profit margin?

A) $1,750,000

B) $3,150,000

C) $4,725,000

D) $1,575,000

The purpose of the equivalent-unit computation is to ________.

A) convert completed units into the amount of partially completed output units that

could be made with that quantity of input

B) use a common metric to estimate the amount of work done on units in a period

C) predict the future production capabilities of the organization

D) satisfy the GAAP requirements which requires all partially completed goods to be

reported as equivalent-units

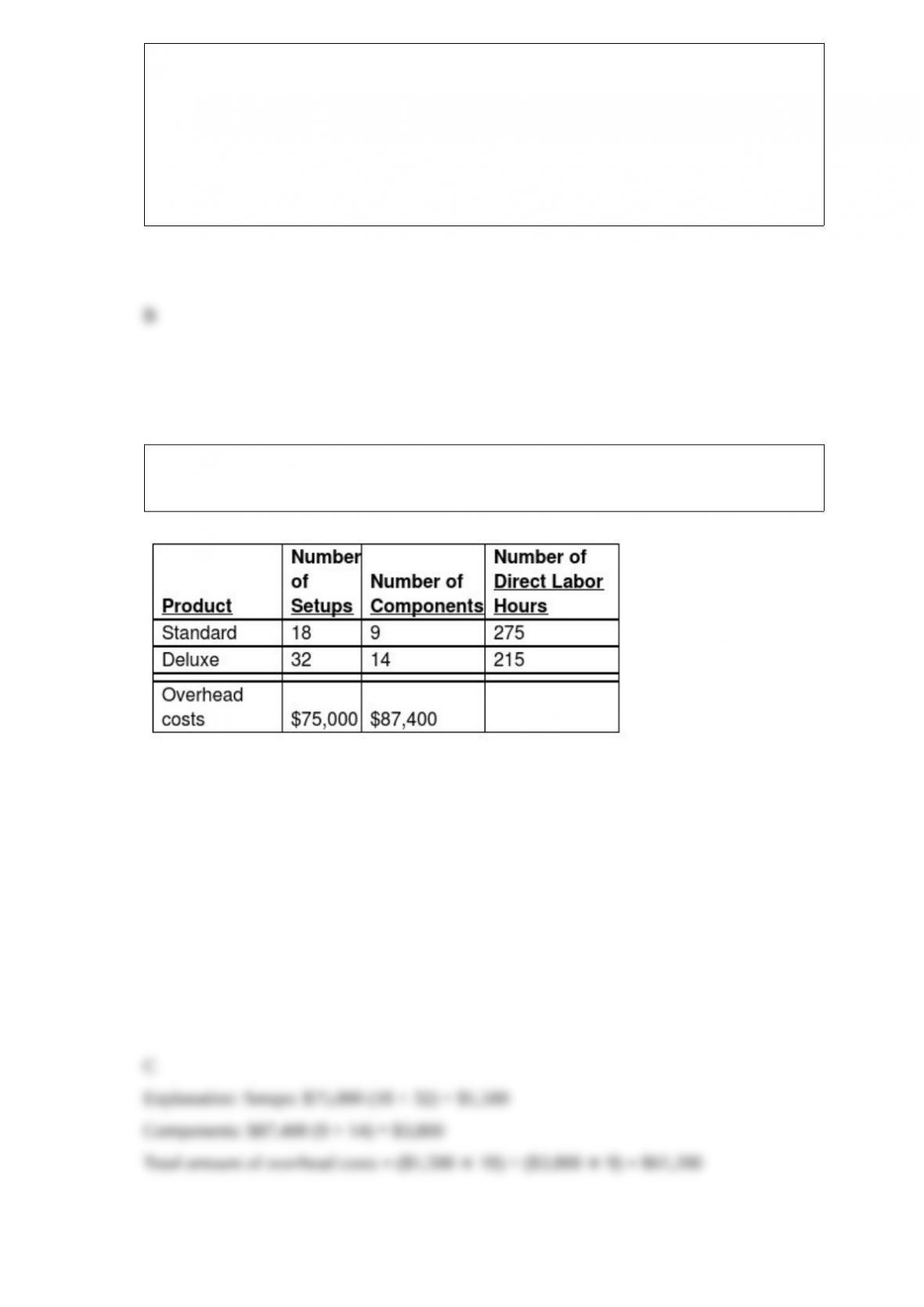

Dartmouth Corporation manufactures two models of office chairs, a standard and a

deluxe model. The following activity and cost information has been compiled:

Number of setups and number of components are identified as activity-cost drivers for

overhead. Assuming an activity-based costing system is used, what is the total amount of

overhead costs assigned to the standard model?

A) $81,200

B) $81,900

C) $61,200

D) $101,200

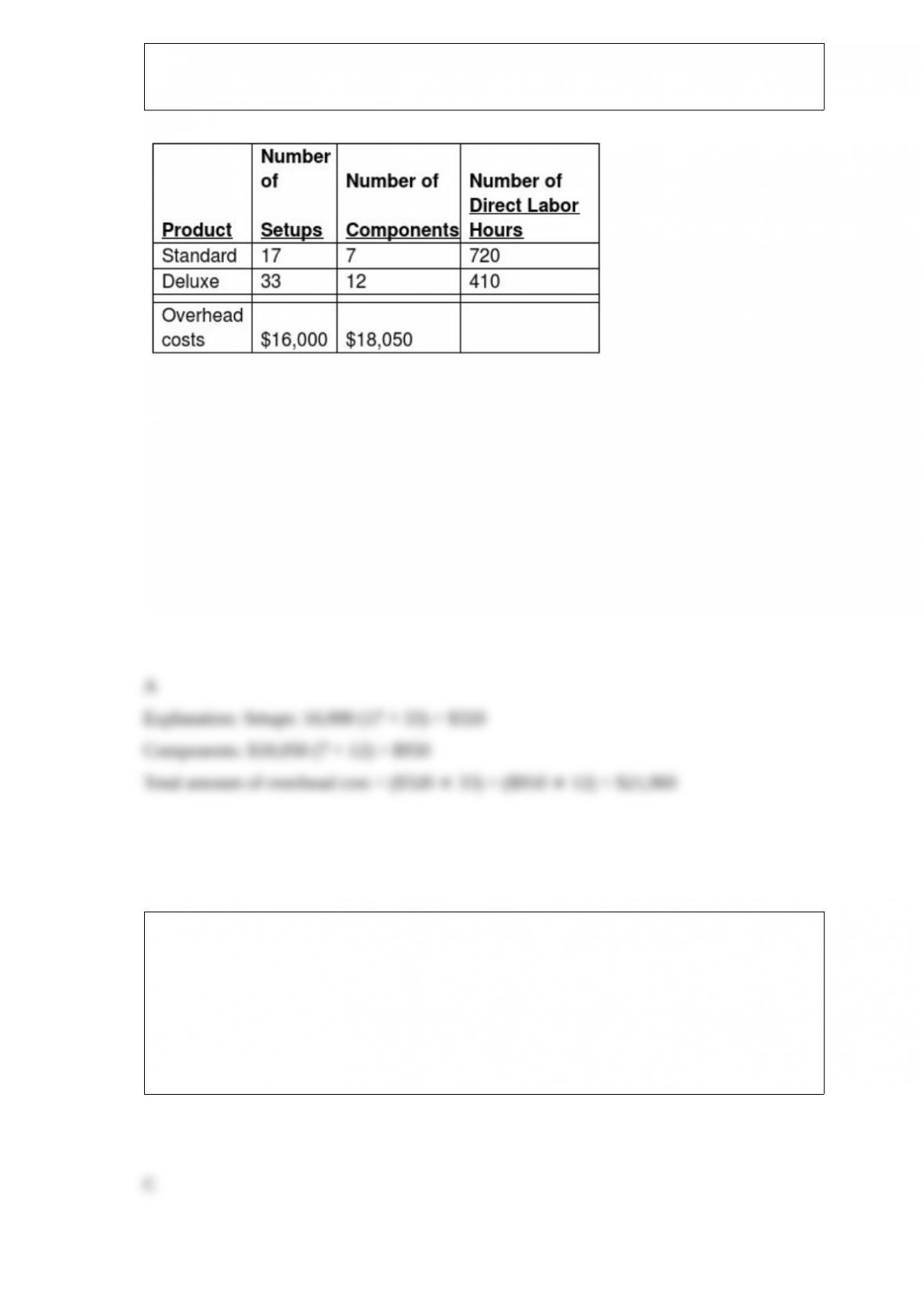

North Street Corporation manufactures two models of motorized go-carts, a standard

and a deluxe model. The following activity and cost information has been compiled:

Number of setups and number of components are identified as activity-cost drivers for

overhead. Assuming an activity-based costing system is used, what is the total amount of

overhead cost assigned to the deluxe model?

A) $21,960

B) $17,025

C) $16,840

D) $17,210

Which of the following statements is true of ABC systems?

A) ABC systems are time-driven cost systems.

B) ABC systems classify some direct costs as indirect costs and some indirect costs as

direct costs.

C) ABC systems provide valuable information to managers beyond accurate product

costs.

D) ABC systems assume all costs are variable costs.

On the assembly floor, Jennifer is paid a regular rate of $25 an hour for straight-time

assuming 8 working hours a day and five working days in a week. She is paid 1.5 times

her regular rate for overtime hours. One week she worked 48 hours.

Required:

a. What is Jennifer’s total compensation for the week?

b. What amount of compensation would be reported as direct manufacturing labor?

c. What amount of compensation would be reported as manufacturing overhead?

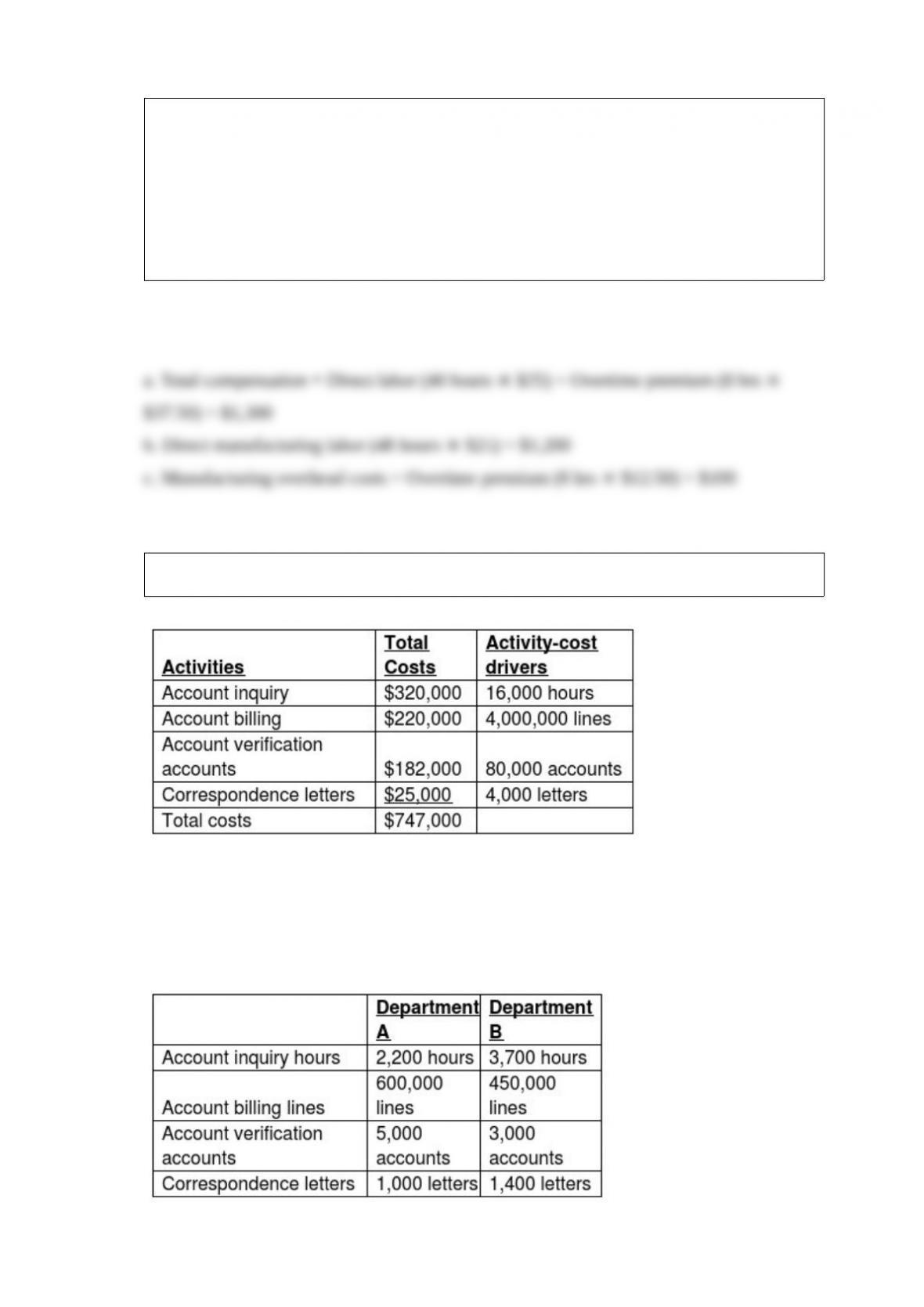

Extreme Manufacturing Company provides the following ABC costing information:

The above activities are used by Departments A and B as follows:

How much of the account billing cost will be assigned to Department B?

A) $220,000

B) $110,000

C) $24,750

D) $33,000

The management accountant for the Chocolate S’more Company has prepared the

following income statement for the most current year:

Chocolate Other Candy Fudge Total

Sales $40,000 $25,000 $35,000 $100,000

Cost of goods sold 26,000 15,000 19,000 60,000

Contribution margin 14,000 10,000 16,000 40,000

Delivery and ordering costs 2,000 3,000 2,000 7,000

Rent (per sq. foot used) 3,000 3,000 2,000 8,000

Allocated corporate costs 5,000 5,000 5,000 15,000

Corporate profit $4,000 $(1,000) $7,000 $10,000

a. Do you recommend discontinuing the Other Candy product line? Why or why not?

b. If the Chocolate product line had been discontinued, corporate profits for the current

year would have decreased by what amount?

Actual (rather than allocated) manufacturing overhead costs are first recorded in the

________.

A) Work-in-Process Control account

B) Finished Goods Control account

C) Manufacturing Overhead Control account

D) Cost of Goods Sold account

Which of the following best describes a step variable-cost function?

A) a step cost function in which cost remains the same over narrow ranges of the level

of activity in each relevant range

B) a step cost function in which cost remains the same over narrow ranges of the level

of activity outside the relevant range

C) step cost function where the cost remains the same over wide ranges of the activity

in each relevant range

D) step cost function where the cost remains the same over wide ranges of the activity

outside the relevant range

The most likely cost driver of distribution costs is the ________.

A) number of parts within the product

B) number of miles driven

C) number of products manufactured

D) number of production hours

Time-series data analysis includes ________.

A) using a variety of time periods to measure the dependent variable of the same entity

(organization, plant, or activity)

B) using the highest and lowest observation for the same entity (organization, plant, or

activity)

C) observing different entities during the same time period for the same entity

(organization, plant, or activity)

D) comparing information in different cost pools for the same entity (organization,

plant, or activity)

Family Furniture sells a table for $900. Its fixed costs are $30,000, while its variable

costs are $600 per table. It currently plans to sell 175 tables this month.

What is the budgeted revenue for the month assuming that Family Furniture sells 175

tables?

A) $52,500

B) $157,500

C) $127,500

D) $105,000

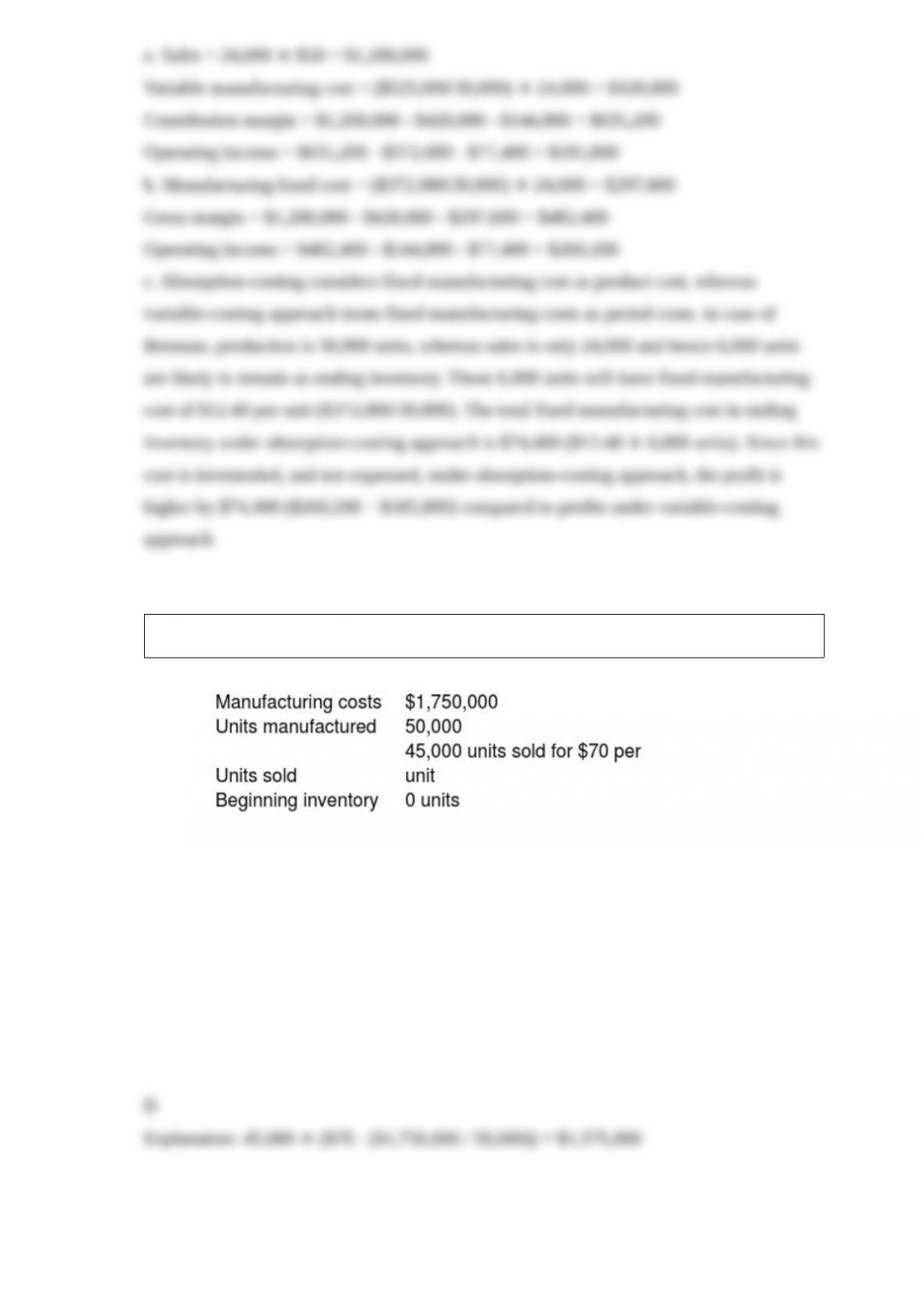

It measures the cost of all manufacturing resources, whether variable or fixed,

necessary to produce inventory.

Universal Works Inc., reports the following information for September sales:

Promotional expenses for September were $1,000.

Required:

If sales double in October, what is the impact on the variable costs?

Silver Company uses one raw material, silver ore, for all of its products. It spends

considerable time getting the silver from the ore before it starts the actual processing of

the finished products, rings, lockets, etc. Traditionally, the company made one product

at a time and charged the product with all costs of production, from ore to final

inspection. However, in recent months, the cost accounting reports have been somewhat

disturbing to management. It seems that some of the finished products are costing more

than they should, even to the point of approaching their retail value. It has been noted

by the accounting manager that this problem began when the company started buying

ore from different parts of the world, some of which require difficult extraction

methods.

Required:

Can you explain how the company might change its accounting system to reflect the

reporting problems better? Are there other problems with the purchasing area?

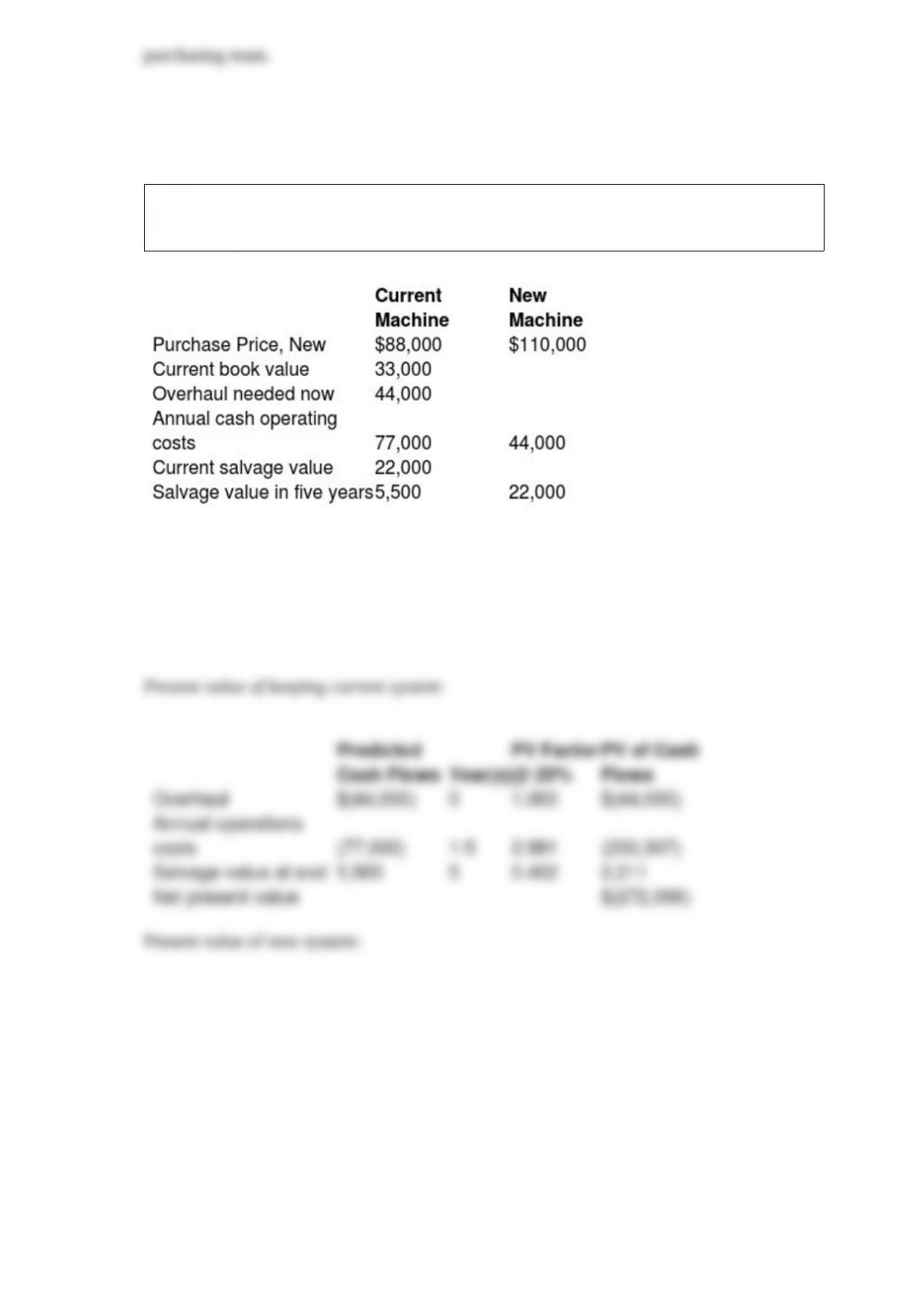

EIF Manufacturing Company needs to overhaul its drill press or buy a new one. The

facts have been gathered, and they are as follows:

Required:

Which alternative is the most desirable with a current required rate of return of 20%?

Show computations, and assume no taxes.

Differentiate between a cost pool and a cost-allocation base.

Explain how the following statement be true: Often the manufacturing overhead control

account (debit) does not equal the manufacturing overhead allocated account (credit).

Explain what revenues and costs are relevant when choosing among alternatives.

Explain the importance of customer-profitability analysis.

Explain why some companies choose not to allocate joint costs to products.

What is the difference between an actual cost system and a normal cost system?

Woody City Manufacturing mills lumber for companies who manufacture furniture. The

main product is finished lumber with a byproduct of wood shavings. The byproduct is

sold to plywood manufacturers. For July, the manufacturing process incurred $412,000

in total costs. Eighty thousand board feet of lumber were produced and sold along with

7,000 pounds of shavings. The finished lumber sold for $6.00 per board foot and the

shavings sold for $0.60 a pound. There were no beginning or ending inventories.

Required:

Prepare an income statement showing the byproduct (1) as a cost reduction during

production, and (2) as a revenue item when sold.

How can a company’s revenues and costs differ across customers?

Describe the major differences between management accounting and financial

accounting for the following:

1. Primary users

2. Focus and emphasis

3. Rules of measurement and reporting

Explain why there is no production-volume variance for variable manufacturing

overhead costs.

A corporation can measure its quality performance by using financial or nonfinancial

measures of quality. Discuss the merits of each method and whether the use of one

precludes the use of the other.

Explain the differences between short-run pricing decisions and long-run pricing

decisions.