The vertical difference, called the residual term, measures the distance between actual

cost of one period and estimated cost of the next period.

The theory of constraints is more useful for the long-run management of costs since it

takes a long-run

perspective and focuses on improving processes by eliminating non-value-added

activities and reducing the costs of performing value-added activities.

An excessive focus on diagnostic control systems and critical performance variables

can cause an organization to ignore emerging threats and opportunities.

Unlike the payback method, which ignores cash flows after the payback period, the

AARR method considers income earned throughout a project’s expected useful life.

Direct material price variance is likely to be unfavorable if the purchasing manager

switched to a lower-price supplier.

Monopolists can charge prices without limitations as there is no competition for the

product or service the monopolist provides.

In variance analysis, if any single performance measure is underemphasized, managers

will tend to make decisions that will cause the particular performance measure to look

good.

Proration approach restates all amounts in the general and subsidiary ledgers by using

actual rather than budgeted cost rates.

An “economy of scale” function is an example of a linear cost function.

Price discounts must be uniform among all customers.

If a company inspects units only at the end of the production process, the units in

ending work-in-process inventory are not assigned any costs of normal spoilage.

A sunk cost is a relevant cost in a decision making.

As ABC systems get very detailed and more cost pools are created, more allocations are

necessary to calculate activity costs for each cost pool, which increases the chances of

misidentifying the costs of different activity cost pools.

The financial perspective of the balanced scorecard focuses on the profits and value

created for shareholders.

An effective balanced scorecard helps to communicate the strategy to all members of

the organization by translating the strategy into a coherent and linked set of

understandable and measurable operational targets.

Since budgeting is a financial function and mostly an analytical and quantitative

exercise, it generally has no impact on human behavior, motivation and decision

making.

Cost accounting is the process of measuring, analyzing, and reporting financial and

nonfinancial information related to the costs of acquiring or using resources in an

organization.

The production method for recognizing byproducts is simpler and is often used in

practice, primarily because the dollar amounts of byproducts are immaterial.

In variable costing, all nonmanufacturing costs are subtracted from contribution margin.

A linear cost function can only represent fixed cost behavior.

Even in the face of changing conditions, attaining the original budget is critical and is

the only true measure of success.

One assumption frequently made in cost behavior estimation is that changes in total

costs can be explained by changes in the level of a single activity.

Distribution can be a cost-driver for a manufacturing company under ABC system.

Customer life-cycle costs , because they are only budgeted items, do not influence the

prices a company can charge for its products.

Effectiveness is the degree to which a predetermined objective or target is met.

A full-cost formula for pricing does requires that the management accountant performs

a detailed analysis of cost-behavior patterns to separate product costs into variable and

fixed components.

One of the ways to increase capacity is to invest in new equipment, such as flexible

manufacturing systems that can be programmed to switch quickly from producing one

product to producing another.

Separable costs that do not differ between alternatives are irrelevant for decision

making.

The sales quantity variance is the difference between budgeted contribution margin

based on actual units sold of all products at the budgeted mix, and contribution margin

in the flexible budget.

The planning of fixed overhead costs differs from the planning of variable overhead

costs in terms of timing.

Two common operational measures of time are customer-response time and on-time

performance.

For normal costing, even though the indirect-cost rate is based on actual, indirect costs

are allocated to products based on the normal capacity of the cost-allocation base.

The market-share variance is the difference in budgeted contribution margin for actual

market size in units caused solely by actual market share being different from budgeted

market share.

The single cost-allocation method makes no distinction between fixed and variable

costs.

Normal spoilage costs are usually deducted from the costs of good units.

A planned decrease in selling price would be expected to cause an increase in the

quantity sold.

Work-in-process inventory are goods partially worked on but not yet completed.

The best-designed strategies are valuable, whether or not they are effectively

implemented.

Bottom-up budgets entrusts senior managers to prepare budgets and lower-level

managers to execute them.

If a companyʹ‘s breakeven revenue is $1,000 and its budgeted revenue is $1,250, then

its margin of safety percentage is 20%.

River Falls Manufacturing uses a normal cost system and had the following data

available for 2018:

Direct materials purchased on account $159,000

Direct materials requisitioned 85,000

Direct labor cost incurred 133,000

Factory overhead incurred 140,000

Cost of goods completed 285,000

Cost of goods sold 249,000

Beginning direct materials inventory 34,000

Beginning WIP inventory 70,000

Beginning finished goods inventory 55,000

Overhead application rate, as a percent of direct-labor costs 130 percent

The ending balance of direct materials inventory is ________.

A) $108,000

B) $193,000

C) $85,000

D) $119,000

Which of the following is NOT an engineered cost?

A) direct material cost of a major component of the product

B) advertising costs for a new product that the factory will start producing

C) the cost of direct laborers who work in the factory

D) depreciation of all factory tools

Bouvous Corporation had the following information for 2015:

Revenue $400,000

Operating expenses 350,000

Total assets 530,000

What is the return on investment?

A) 9.4%

B) 75.5%

C) 8.6%

D) 10.4%

________ is based on the level of capacity utilization that satisfies average customer

demand over periods generally longer than one year.

A) Practical capacity

B) Theoretical capacity

C) Master-budget capacity utilization

D) Normal capacity utilization

Sparkle Jewelry sells 800 units resulting in $85,000 of sales revenue, $32,000 of

variable costs, and $26,000 of fixed costs.

The number of units that must be sold to achieve $41,000 of operating income is

________.

A) 909 units

B) 393 units

C) 1,012 units

D) 619 units

Expo Manufacturing Inc., is in the process of evaluating a new product using the

following information:

∙ A new transformer has three production runs each year, each with $15,000 in setup

costs.

∙ The new transformer incurred $45,000 in development costs and is expected to be

produced over the next three years.

∙ Direct costs of producing the transformers are $55,000 per run of 5000 transformers

each.

∙ Indirect manufacturing costs charged to each run are $45,000.

∙ Destination charges for each transformer average $2.00.

∙ Customer service expenses average $0.40 per transformer.

∙ The transformers are selling for $20 the first year and will increase by $4 each year

thereafter.

∙ Sales units equal production units each year.

What is the estimated life-cycle operating income for the first year?

A) (126,000)

B) 1,146,000

C) 1,596,000

D) 126,000

Zenith Corporation’s net income is $80,000. What is the return on investment if the

amount of the investment is $510,000?

A) 18.60%

B) 13.56%

C) 15.69%

D) 27.12%

Contribution margin equals ________.

A) revenues minus period costs

B) revenues minus product costs

C) revenues minus variable costs

D) revenues minus fixed costs

For each item below indicate the source documents that would most likely authorize the

journal entry in a job-costing system.

Required:

a. direct materials purchased

b. direct materials used

c. direct manufacturing labor

d. indirect manufacturing labor

e. finished goods control

f. cost of goods sold

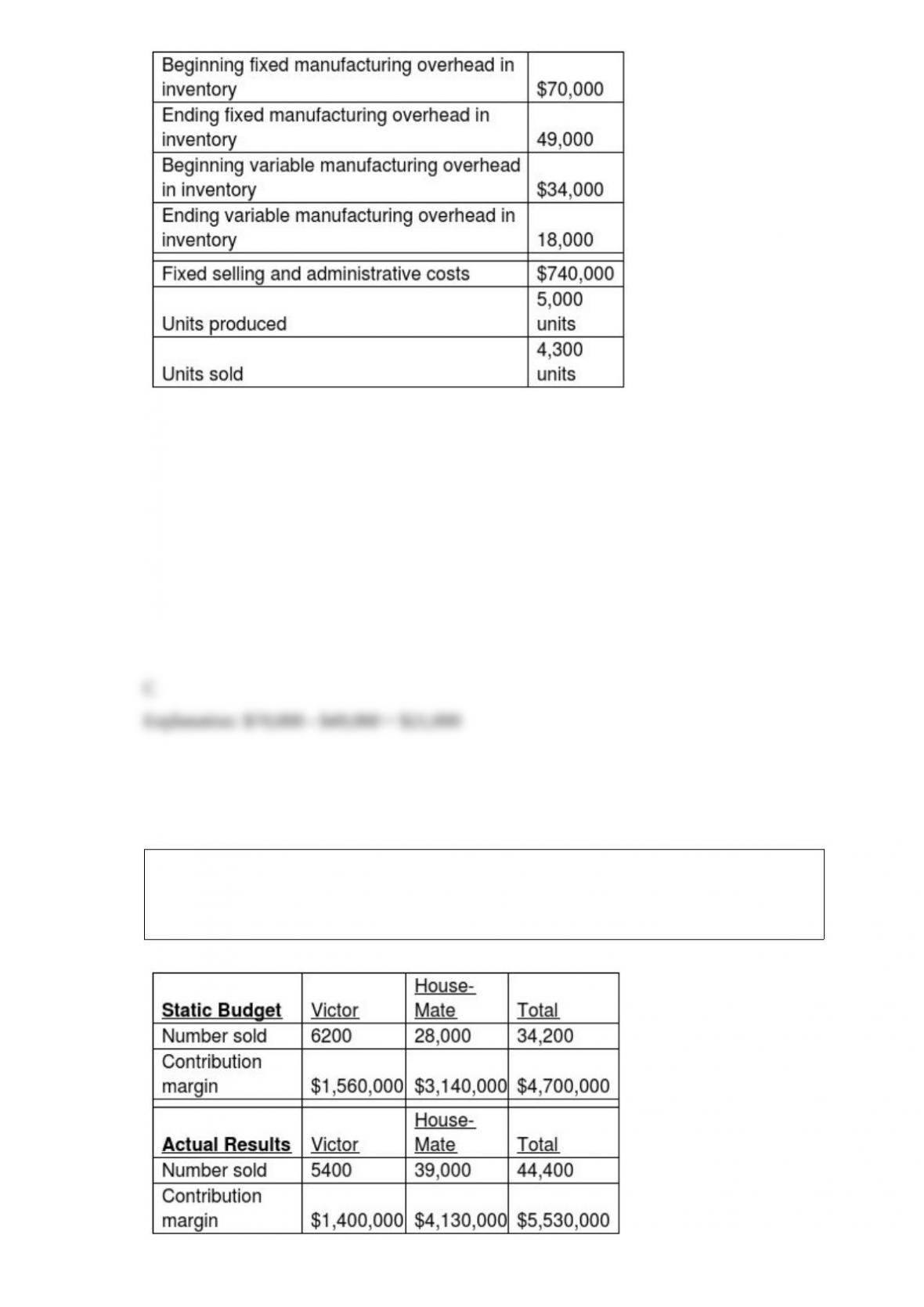

The following information pertains to Stone Wall Corporation:

What is the difference between operating incomes under absorption costing and variable

costing?

A) $3,000

B) $37,000

C) $21,000

D) $10,500

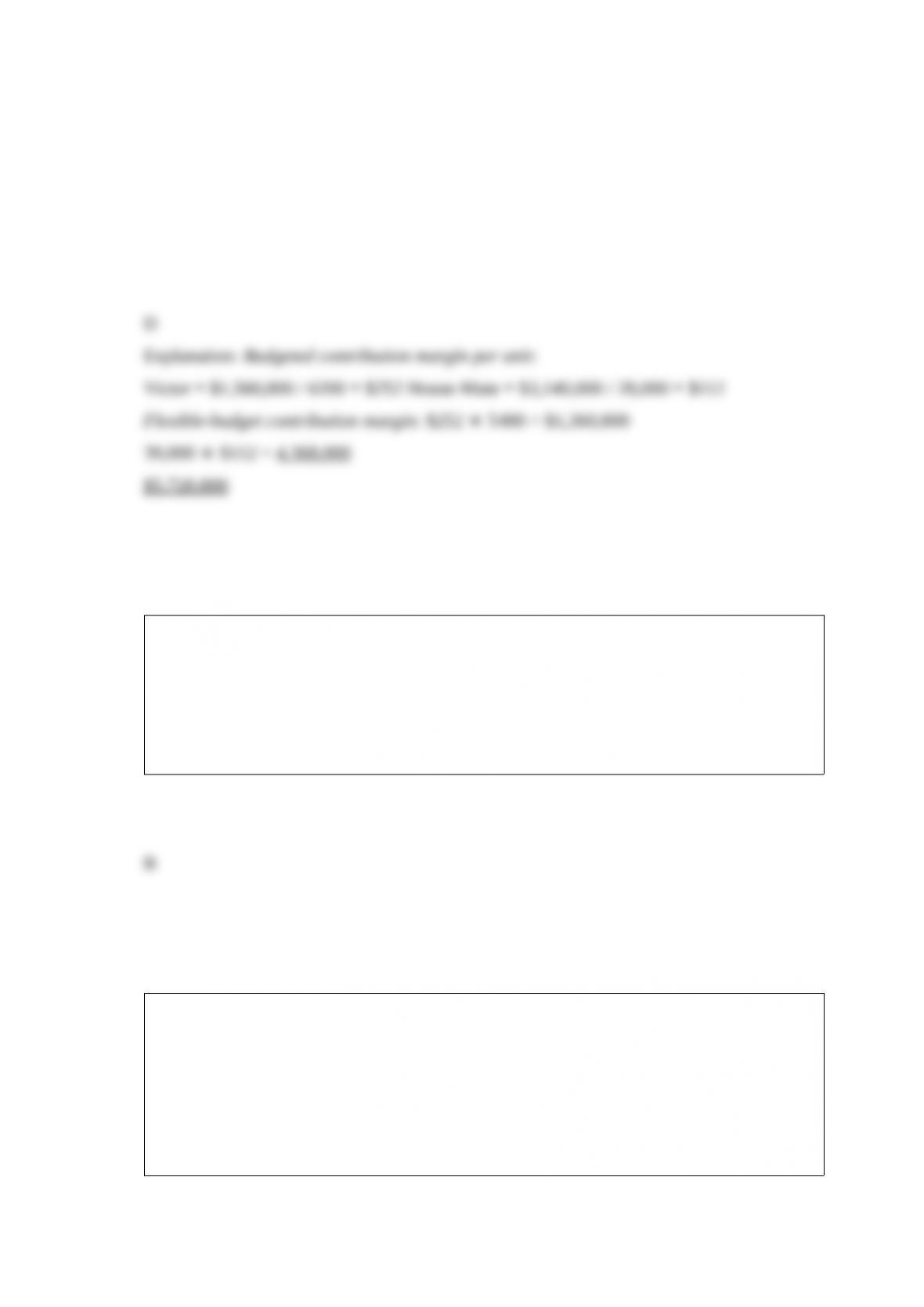

The Fortise Corporation manufactures two types of vacuum cleaners, the Victor for

commercial building use and the House-Mate for residences. Budgeted and actual

operating data for the year 2017 were as follows:

What is the contribution margin for the flexible budget? (Round intermediary calculations

to the nearest dollar.)

A) $1,360,800

B) $4,368,000

C) $4,698,400

D) $5,728,800

Customers making large contributions to the profitability of the company should

________.

A) be treated the same as other customers because all customers are important

B) receive a higher level of attention from the company than less profitable customers

C) be charged higher prices for the same products than less profitable customers

D) not be offered the volume-based price discounts offered to less profitable customers

For a manufacturing company, indirect manufacturing costs would be included in

________.

A) direct materials inventory only

B) merchandise inventory only

C) both work-in-process inventory and finished goods inventory

D) direct materials inventory, work-in-process inventory, and finished goods inventory

accounts

Which of the following statements is true?

A) In a job-costing system, average production cost is calculated for all units produced.

B) In a process-costing system, each unit uses approximately the same amount of

resources.

C) In a job-costing system, overheads are allocated to all units equally.

D) In a process-costing system, individual jobs use different quantities of production

resources.

Which of the following departments would not be considered a service or support

department?

A) assembly

B) information systems

C) shipping

D) plant maintenance

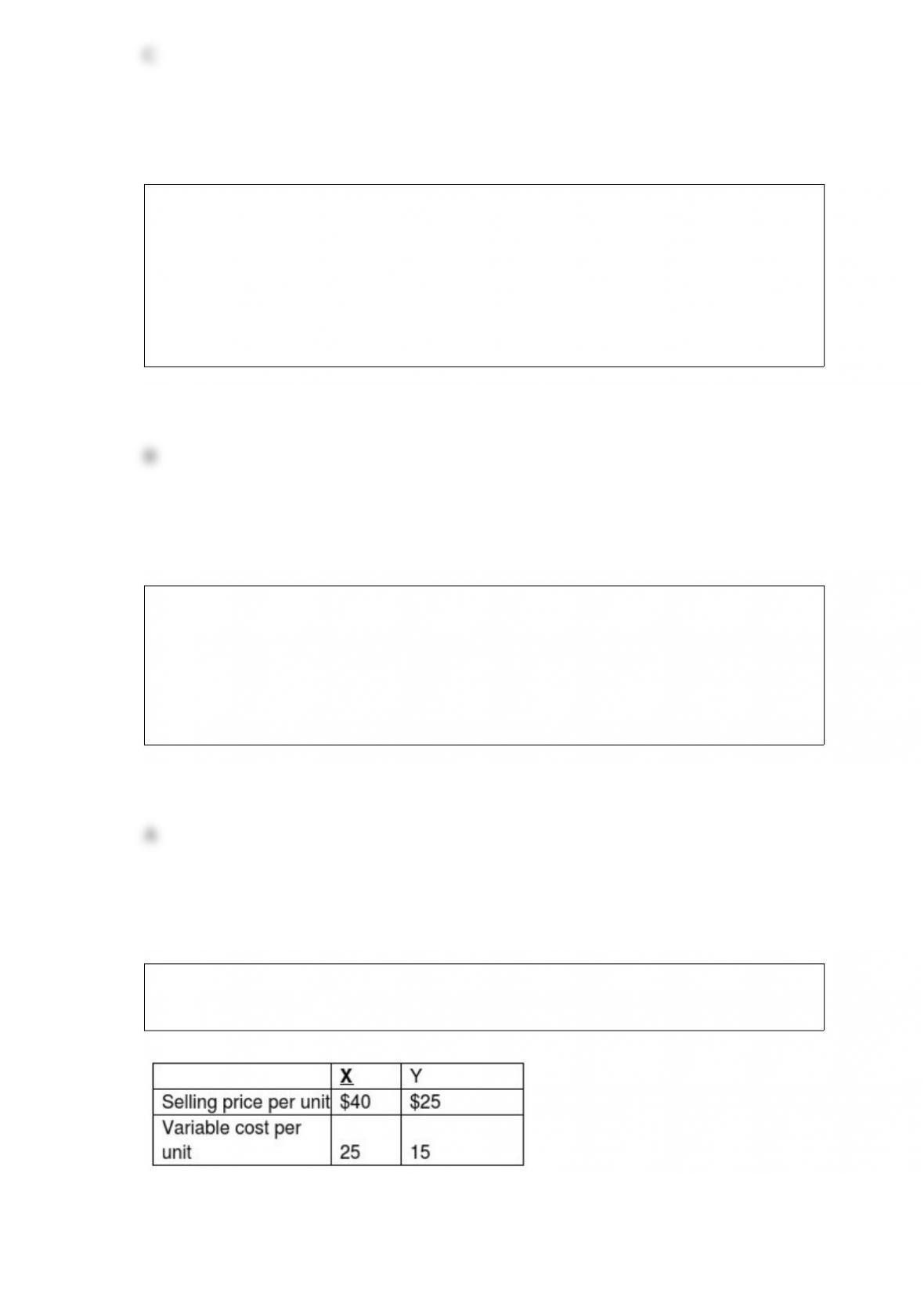

Craylon Manufacturing Company produces two products, X and Y. The following

information is presented for both products:

Total fixed costs are $275,000.

Required:

a. Calculate the contribution margin for each product.

b. Calculate breakeven point in units of both X and Y if the sales mix is 3 units of X for

every unit of Y.

c. Calculate breakeven volume in total dollars if the sales mix is 2 units of X for every 3

units of Y.

Given this change in the cost structure ________.

A) The costing results for chess pieces under the new system depend on the adequacy

and quality of the estimated cost drivers and costs used by the system.

B) Chess pieces have benefited from the new system.

C) Chess pieces are definitely more accurately costed.

D) Chess will now have a lower sales price.

Which of the following best describes transferred-in costs?

A) they are the cost of transferring products from a vendor

B) they are value-added costs that are only considered in the first-in,first out process

costing system

C) costs incurred in a previous department or process that are carried forward as the

product’s cost as that product moves to another department or process in the production

cycle

D) they are the shipping costs related to finished goods that are transported to a

customer’s location

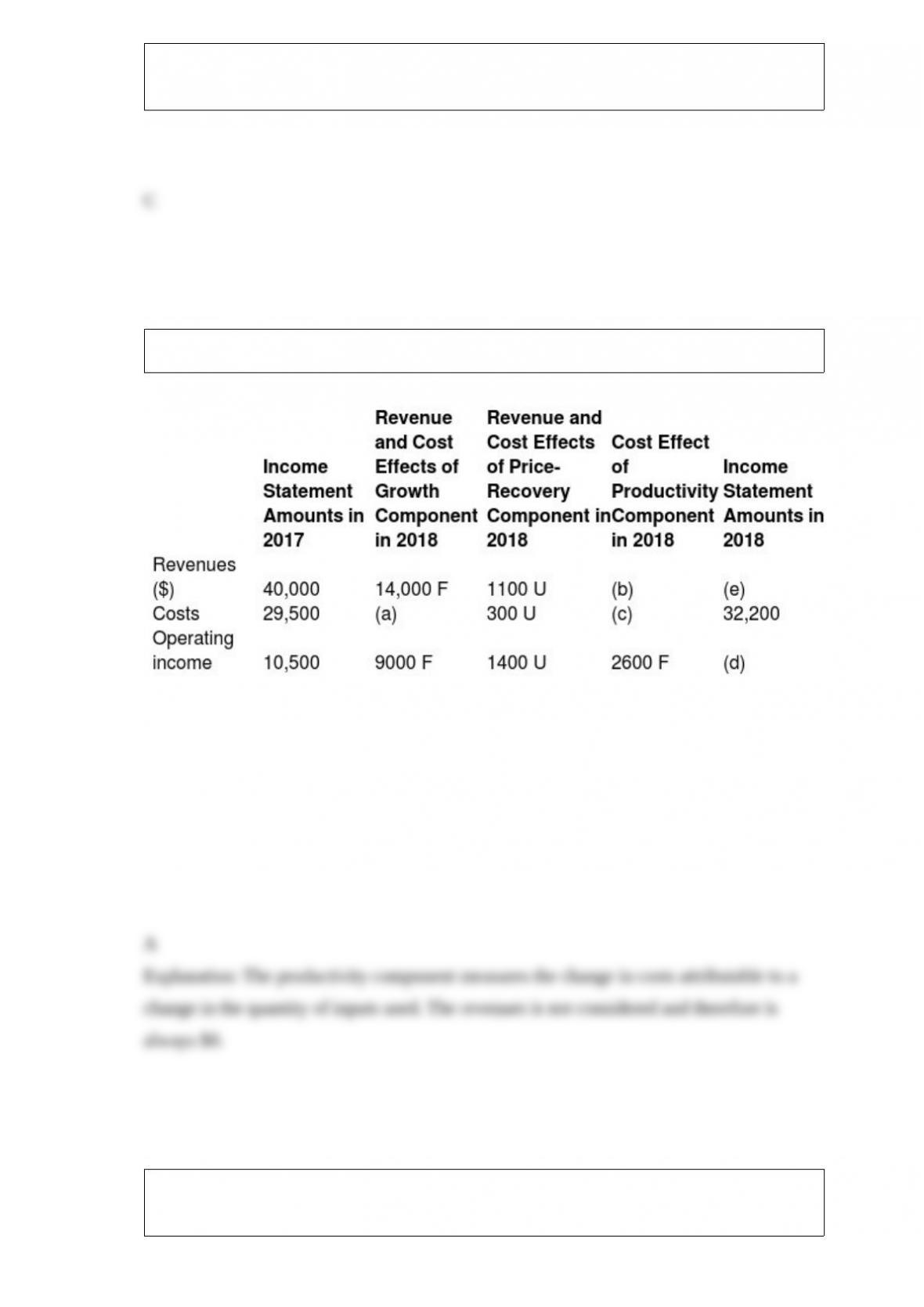

Strategic Analysis of Profitability of King Philip Company:

What is the revenue effect of the productivity component (b)?

A) $0

B) $2600 U

C) $1200 F

D) $2600 F

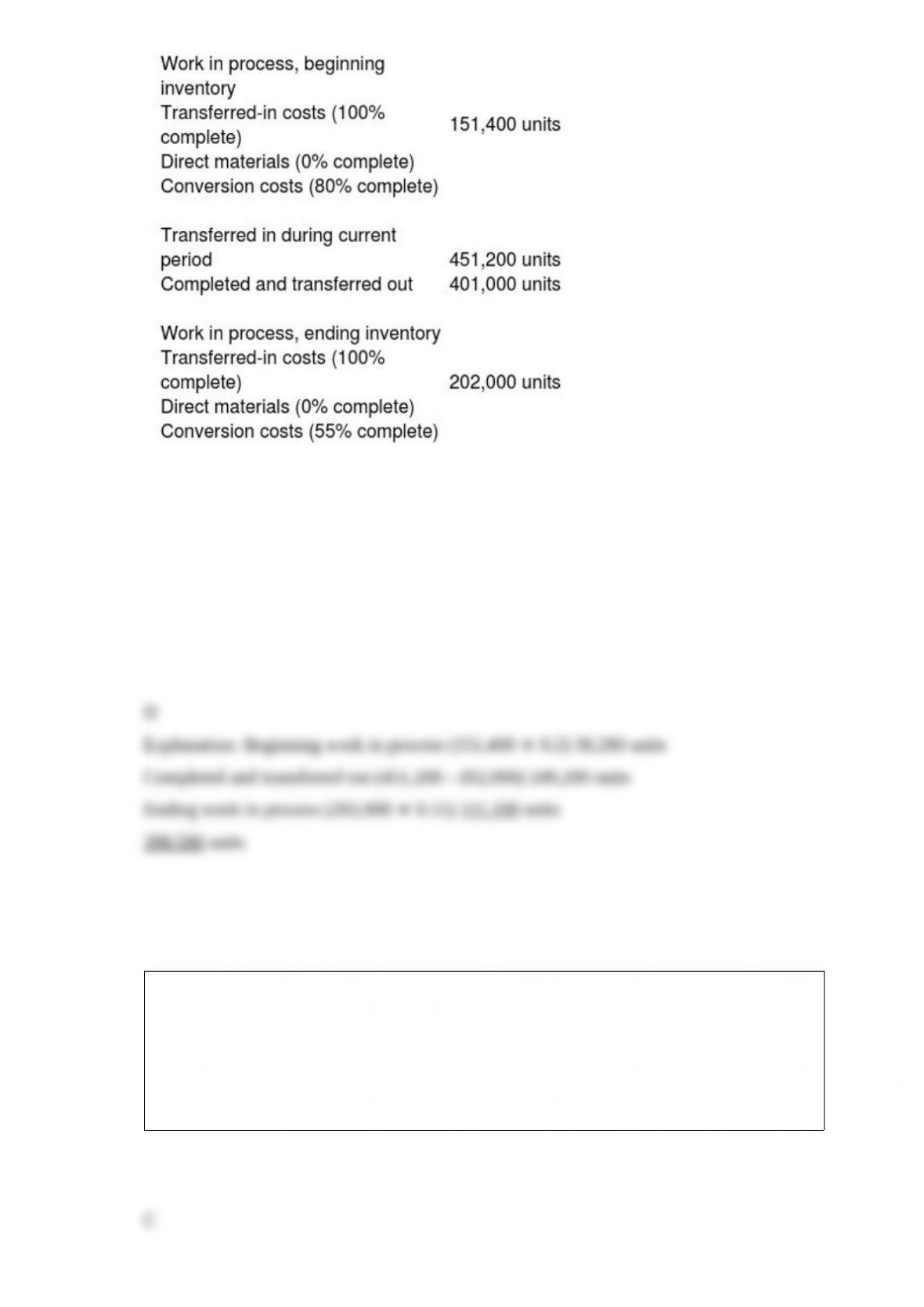

Direct Disk Drive Company operates a computer disk manufacturing plant. Direct

materials are added at the end of the process. The following data were for August 2017:

Calculate equivalent units for conversion costs using the FIFO method.

A) 30,280 units

B) 353,400 units

C) 299,800 units

D) 390,580 units

Market-based transfer prices are helpful when ________.

A) the product is specialized

B) the internal product is different from the products available externally in terms of its

quality

C) the interdependencies of subunits are minimal

D) the markets are not perfectly competitive

Which of the following is a financial budget?

A) budgeted balance sheet

B) cash receivables budget

C) production budget

D) cost of goods sold budget

A ________ is anything for which a measurement of costs is desired.

A) cost-allocation base

B) cost pool

C) cost object

D) cost-application base

Sam’s Structures desires to buy a new crane and accessories to help move and install

modular buildings. The machine sells for $75,000 and requires working capital of

$10,000. Its estimated useful life is six years and it will have a salvage value of

$17,560. Recovery of working capital will be $10,000 at the end of its useful life.

Annual cash savings from the purchase of the machine will be $20,000.

Required:

a. Compute the net present value at a 12% required rate of return.

b. Compute the internal rate of return.

c. Determine the payback period of the investment.

Which of the following is true of responsibility accounting?

A) It is a system that measures the plans, budgets, actions, and actual results of a

responsibility center.

B) It is an arrangement of lines of responsibility and authority within a responsibility

center.

C) It explicitly incorporates continuous improvement and changes due to learning

curve.

D) It examines how a result will change if the original plan is not achieved.

LaCrosse Products has a budget of $903,000 in 2017 for prevention costs. If it decides

to automate a portion of its prevention activities, it will save $80,200 in variable costs.

The new method will require $40,800 in training costs and $100,000 in annual

equipment costs. Management is willing to adjust the budget for an amount up to the

cost of the new equipment. The budgeted production level is 151,000 units.

Appraisal costs for the year are budgeted at $609,000. The new prevention procedures

will save appraisal costs of $50,400. Internal failure costs average $15 per failed unit of

finished goods. The internal failure rate is expected to be 3% of all completed items.

The proposed changes will cut the internal failure rate by one-third. Internal failure

units are destroyed. External failure costs average $58 per failed unit. The company’s

average external failures average 3% of units sold. The new proposal will reduce this

rate by 50%. Assume all units produced are sold and there are no ending inventories.

Management has offered to allow the prevention changes if all changes take place as

anticipated and the amounts netted are less than the cost of the equipment. What is the

net impact of all the changes created by the preventive changes? (Note: numbers shown

as (negatives ) represent net savings and positive numbers represent net cost.)

A) $140,800

B) $(22,650)

C) $(143,820)

D) $(131,370)

When “available time” (i.e., setup-hours) is used to calculate a cost of a resource and to

allocate costs to cost objects , the system is called:

A) job costing

B) process costing

C) hybrid costing

D) time-driven activity based costing

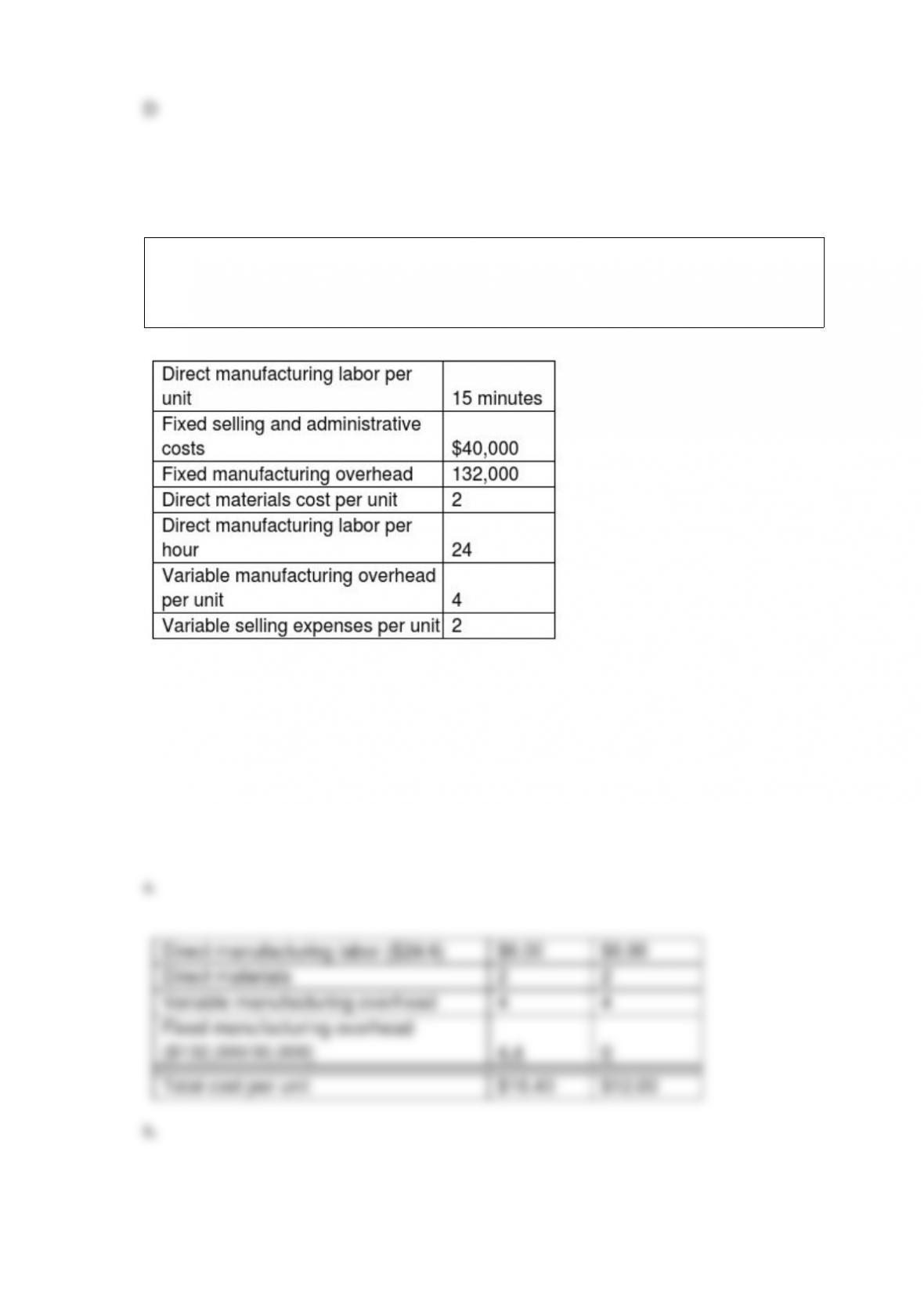

Jarvis Golf Company sells a special putter for $20 each. In March, it sold 28,000 putters

while manufacturing 30,000. There was no beginning inventory on March 1. Production

information for March was:

Required:

a. Compute the cost per unit under both absorption and variable costing.

b. Compute the ending inventories under both absorption and variable costing.

c. Compute operating income under both absorption and variable costing.

Activity-based costing is most likely to yield benefits for companies ________.

A) with complex product design processes that vary significantly from product to

product

B) with operations that remain fairly consistent across product lines

C) in a monopolistic market

D) having nominal percentage of indirect costs

Burgandy Manufacturing produces a single product that sells for $80. Variable costs per

unit equal $35. The company expects total fixed costs to be $90,000 for the next month

at the projected sales level of 2,500 units. In an attempt to improve performance,

management is considering a number of alternative actions. Each situation is to be

evaluated separately. What is the current breakeven point in terms of number of units?

A) 2,000 units

B) 1,125 units

C) 2,572 units

D) 2,046 units

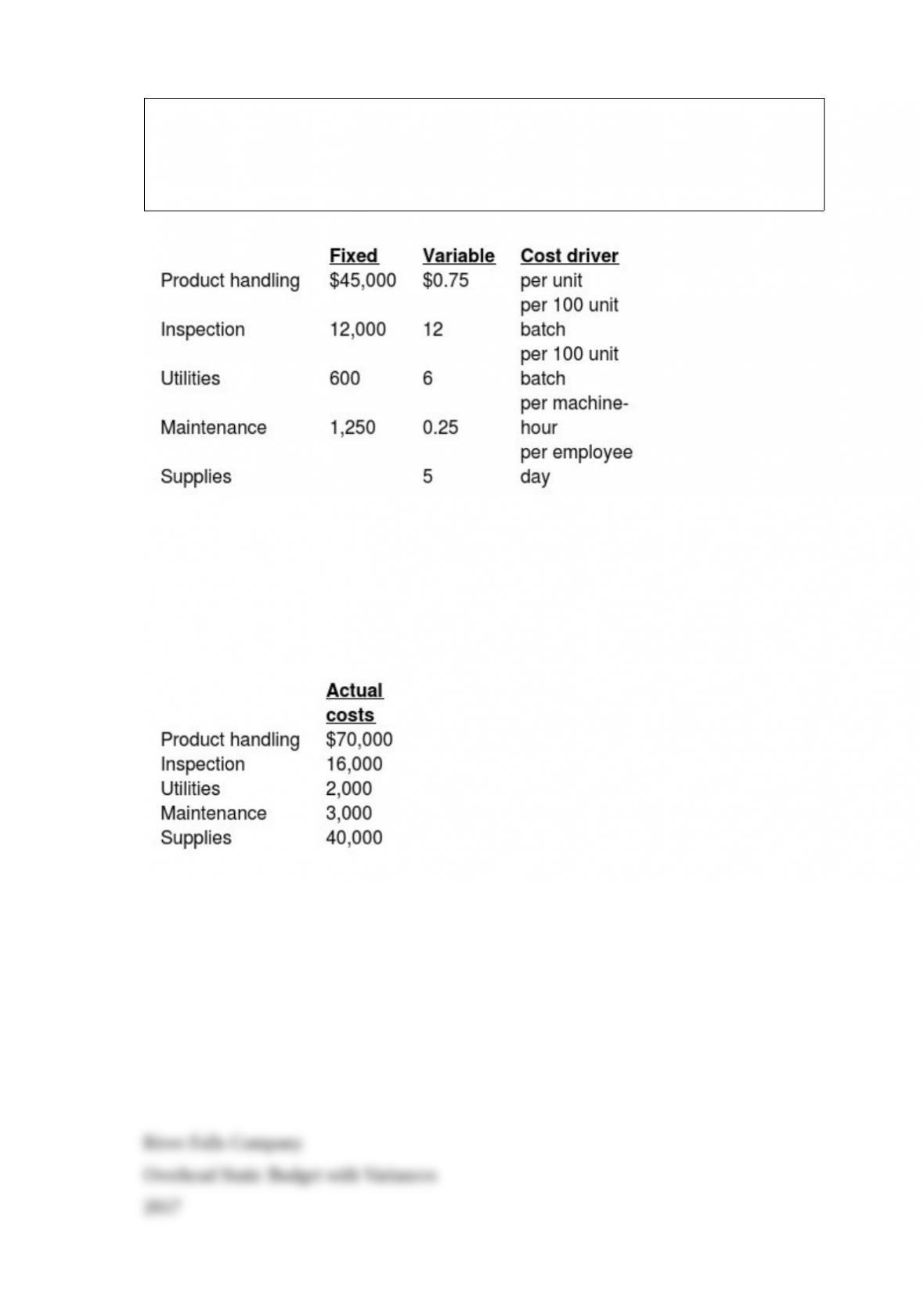

River Falls Company uses a flexible budget for its indirect manufacturing costs. For

2017, the company anticipated that it would produce 27,000 units with 4,800

machine-hours and 8,000 employee days. The costs and cost drivers were to be as

follows:

During the year, the company processed 26,500 units, worked 8,200 employee days, and

had 4,850 machine-hours. The actual costs for 2017 were:

Required:

a. Prepare the static budget using the overhead items above and then compute the

static-budget variances.

b. Prepare the flexible budget using the overhead items above and then compute the

flexible-budget variances.

Norton’s Convenience store has a variable demand. The daily demand ranges from 270

to 330 customers a day who average purchasing 5 items each. The average daily

demand is 300 customers. The convenience store currently operates 12 hours a day.

Each order takes approximately 2 minutes.

Required:

a. What is the average customer waiting time, in minutes?

b. What is the cycle time for an order?

c. Norton has decided that the waiting time is too long and has increased the hours the

store is open to 15 hours. What is the waiting time now?

The Conity Corporation has an Electric Mixer Division and an Electric Lamp Division.

Of a $16,000,000 bond issuance, the Electric Mixer Division used $9,600,000 and the

Electric Lamp Division used $6,400,000 for expansion. Interest costs on the bond

totaled $1,000,000 for the year. What amount of interest costs should be allocated to the

Electric Lamp Division? (Round any intermediary calculations two decimal places and

your final answer to the nearest dollar.)

A) $400,000

B) $600,000

C) $625,000

D) $6,400,000

River Falls Manufacturing uses a normal cost system and had the following data

available for 2018:

Direct materials purchased on account $145,000

Direct materials requisitioned 82,000

Direct labor cost incurred 127,000

Factory overhead incurred 140,000

Cost of goods completed 288,000

Cost of goods sold 248,000

Beginning direct materials inventory 25,000

Beginning WIP inventory 63,000

Beginning finished goods inventory 53,000

Overhead application rate, as a percent of direct-labor costs 125 percent

The ending balance of finished goods inventory is ________.

A) $53,000

B) $40,000

C) $93,000

D) $288,000

When machine-hours are used as an overhead cost-allocation base and annual leasing

costs for equipment unexpectedly increase, the most likely result would be to report

a(n) ________.

A) unfavorable variable overhead spending variance

B) favorable variable overhead efficiency variance

C) unfavorable fixed overhead flexible-budget variance

D) favorable production-volume variance

Jonathan has managed a downtown store in a major metropolitan city for several years.

The firm has ten stores in varying locations. In the past, senior management noticed

Jonathan’s work and he has received very good annual evaluations for his management

of the store.

This year his store has generated steady growth in sales, but earnings have been

deteriorating. After examining the monthly performance report generated by the

company budgeting department, he noticed that increasing fixed costs is causing the

decrease in earnings.

Administrative corporate costs, primarily fixed costs, are allocated to individual stores

each month based on actual sales for that month. Two of these stores are currently

growing at a rapid pace, while four other stores are having operating difficulties.

Required:

From the information presented, what do you think is the cause of Jonathan’s reported

decrease in earnings? How can this be corrected?

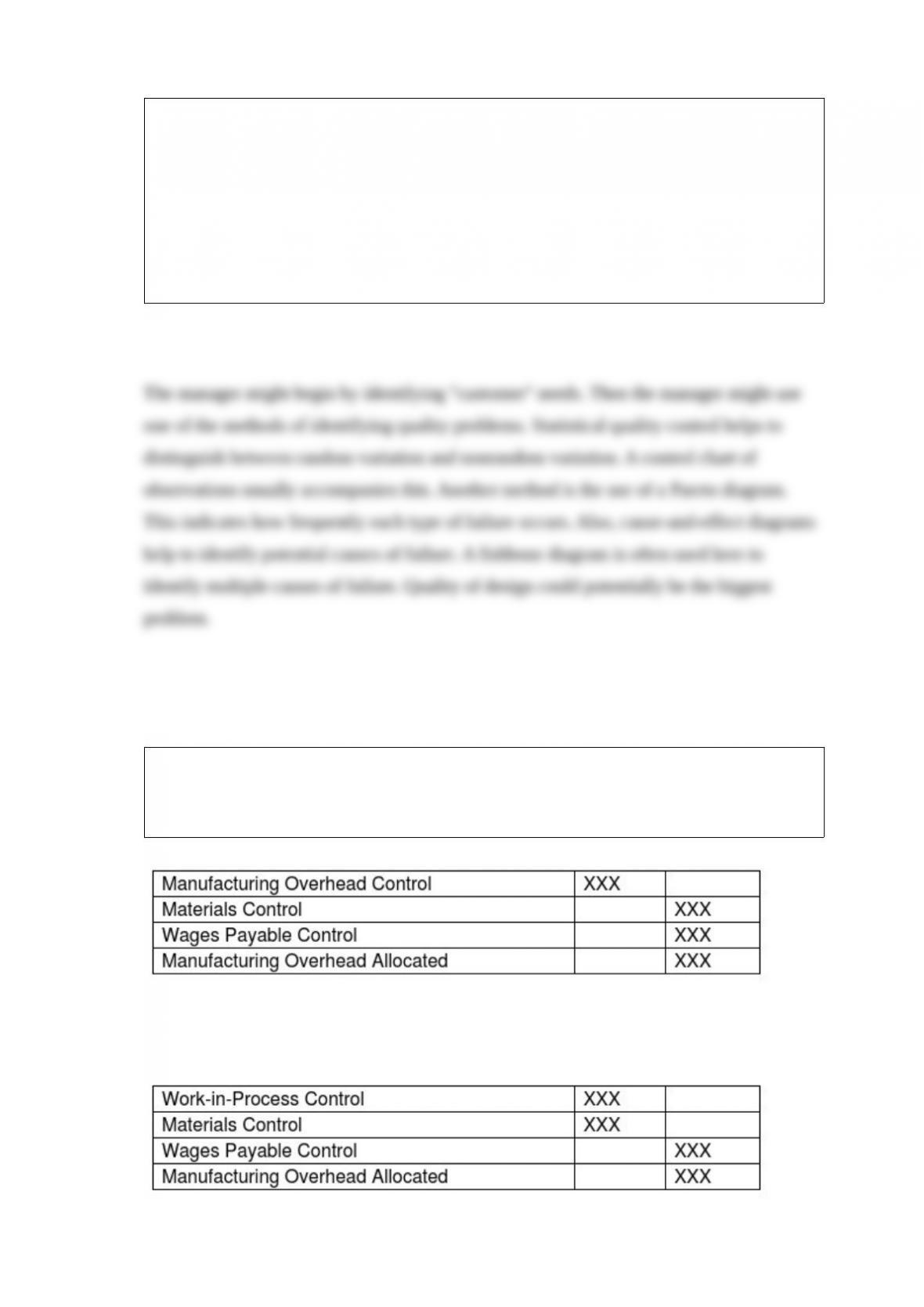

Baby Care Products has just completed a very successful program of improving quality

in its manufacturing operations. The next step is to improve the operations of its

administrative functions, starting with the accounting information system. As the

manager of the accounting operations, you are requested to begin a quality

improvement program.

Required:

What are some possibilities of finding out about the current status of quality in the

accounting system?

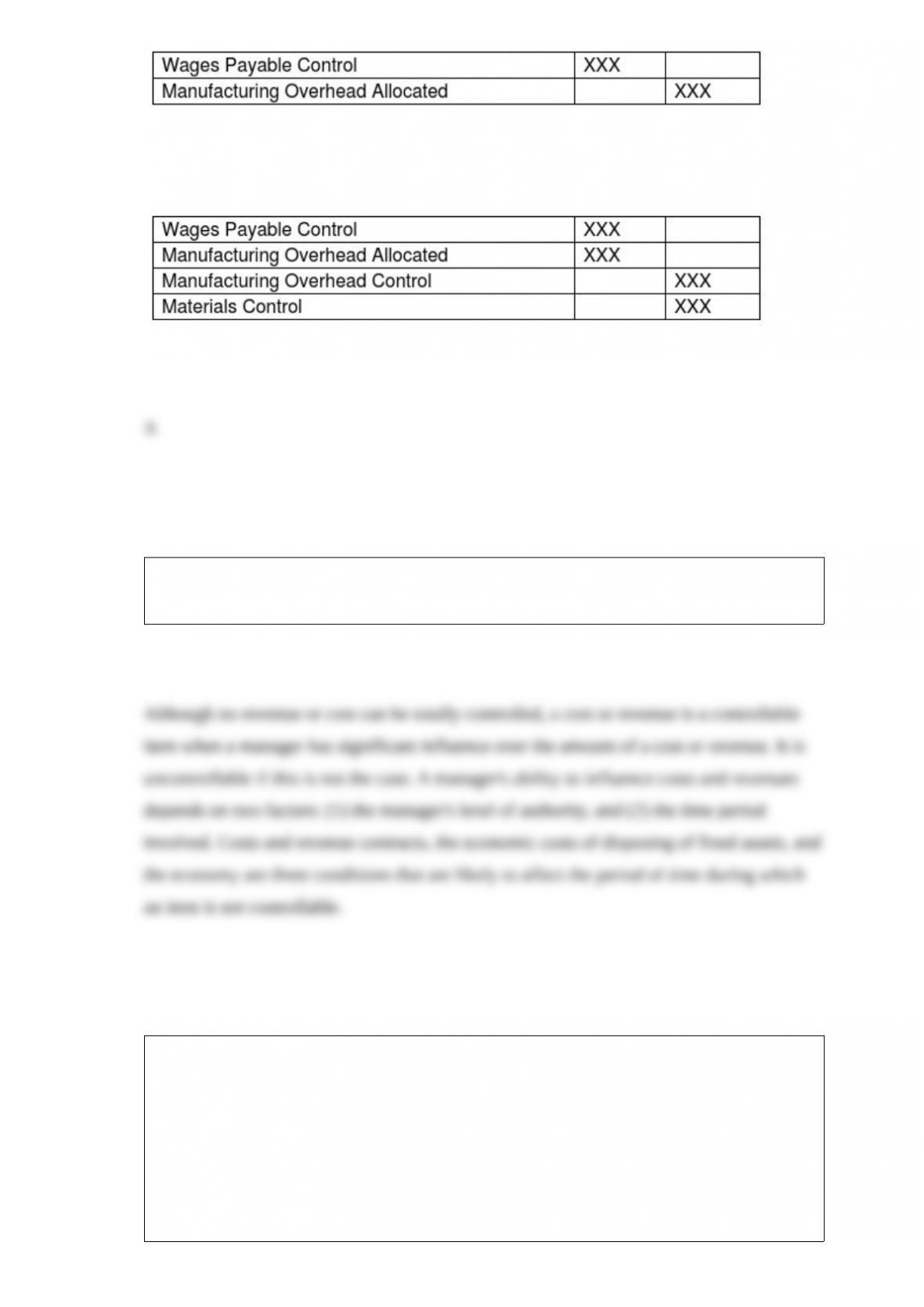

Which of the following entries is correct when the costs of the rework is normal and

common to all the jobs?

A

B)

C)

D)

Distinguish between controllable and uncontrollable aspects of revenue and costs. Can

a manager totally control all revenue and costs? Why or why not?

Shazam Machines produces numerous types of money change machines. All machines

are made in the same production department and many use exactly the same processes.

Because customers have such different demands for the machine characteristics, the

company uses a job-costing system. Unfortunately, some of the production managers

have been upset for the last few months when their jobs were charged with the spoilage

that occurred over an entire processing run of several types of machines. Some of the

best managers have even threatened to quit unless the accounting system is changed.

Required:

What recommendations can you suggest to improve the accounting for spoilage?

Discuss the potential use of nonlinear curves in cost functions and cost analysis. Give

some examples.

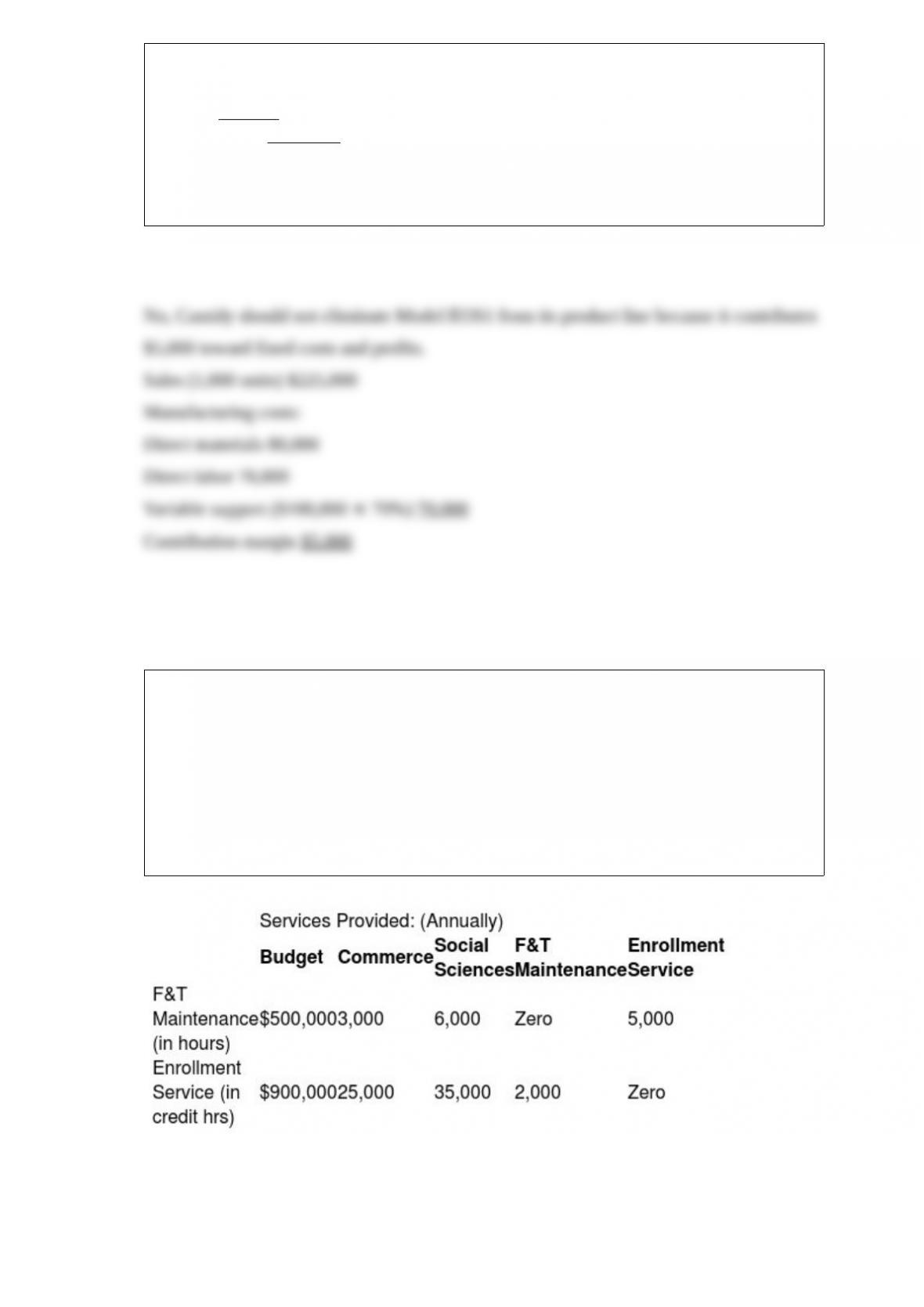

Cassidy Products Inc.is considering eliminating Model EOS1 from its product line

because of losses over the past quarter. The past three months of information for model

EOS1 is summarized below:

Sales (1,000 units) $225,000

Manufacturing costs:

Direct materials 80,000

Direct labor ($15 per hour) 70,000

Support 100,000

Operating loss ($25,000)

Support costs are 70% variable and the remaining 30% is depreciation of special

equipment for model EOS1 that has no resale value.

Should Cassidy eliminate Model EOS1 from its product line? Why or why not?

Marshall University offers only high-tech graduate-level programs. Marshall has two

principal operating departments, Commerce and Social Sciences, and two support

departments, Facility and Technology Maintenance and Enrollment Services. The base

used to allocate facility and technology maintenance is budgeted total maintenance

hours. The base used to allocate enrollment services is number of credit hours for a

department. The Facility and Technology Maintenance budget is $500,000, while the

Enrollment Services budget is $900,000. The following chart summarizes budgeted

amounts and allocation-base amounts used by each department:

Required:

Prepare a schedule which allocates service department costs using the step-down method

with the sequence of allocation based on the highest-percentage support concept. Compute

the total amount of support costs allocated to each of the two principal operating

departments, Commerce and Social Sciences.

Kaiser Company just hired its fourth production manager in three years. All three

previous managers had quit because they could not get the company above the

break-even point, even though sales had increased somewhat each year. The company

was operating at about 60 % of plant capacity. The flatware industry was growing, so

increased sales were not out of the question.

I. R. Thinking took the job as manager of the production division with a very attractive

salary package. After interviewing for the position, he proposed a salary and bonus

package that would give him a very small salary but a large bonus if he took the

operating income (using absorption costing) above the breakeven point during his very

first year.

Required:

What do you think Mr. Thinking had in mind for increasing the company’s operating

income?

BIG Manufacturing Products has been using FIFO process costing for tracking the costs

of its manufacturing activities. However, in recent months, the system has become

somewhat bogged down with details. It seems that, when the company purchased

Brown Electronics last year, its product lines increased six-fold. This has caused both

the accountants and the suppliers of the information, the line managers, great difficulty

in keeping the costs of each product line separate. Likewise, the estimation of the

completion of ending work-in-process inventories and the associated costs has become

very cumbersome. The chief financial officer of the company is looking for ways to

improve the reporting system of product costs.

Required:

What can you recommend to improve the situation?

Discuss the three methods to dispose of production volume variance.

Discuss considerations that should be fully taken into account when developing

inventory related relevant costs for use in an economic order quantity (EOQ) model.

What does Section 482 of the U.S. Internal Revenue Code govern?

What is a “common cost”? What are two methods that a manager can use to allocate

common costs to two or more users?

Lean accounting is much simpler than traditional product costing. Why?