CHAPTER 14

COST ALLOCATION, CUSTOMER-PROFITABILITY

ANALYSIS, AND SALES-VARIANCE ANALYSIS

14-1 “I’m going to focus on the customers of my business and leave cost-allocation issues to

my accountant.” Do you agree with this comment by a division president? Explain.

Disagree. Cost accounting data plays a key role in many management planning and control

14-2 Why is customer-profitability analysis an important topic for managers?

14-3 How can a company track the extent of price discounting on a customer-by-customer

basis?

Companies that separately record (a) the list price and (b) the discount have sufficient

14-4 “A customer-profitability profile highlights those customers a company should drop to

improve profitability.” Do you agree? Explain.

No. A customer profitability profile highlights differences in the current period’s profitability

14-5 Give examples of three different levels of costs in a customer-cost hierarchy.

Five categories in a customer cost hierarchy are identified in the chapter. The examples given

relate to the Provalue Division of Astel Computers used in the chapter:

●Customer output-unit-level costs—costs of activities to sell each unit (computer) to a

●Customer batch-level costs—costs of activities that are related to a group of units

14-1

●Customer-sustaining costs—costs of activities to support individual customers, regardless

●Distribution-channel costs—costs of activities related to a particular distribution channel

●Division-sustaining costs—costs of division activities that cannot be traced to individual

14-6 What information does the whale curve provide?

14-7 “A company should not allocate all of its corporate costs to its divisions.” Do you agree?

Explain.

Disagree. In general, companies have three choices regarding the allocation of corporate costs to

divisions: allocate all corporate costs, allocate some corporate costs (those “controllable” by the

14-8 What criteria might managers use to guide cost-allocation decisions? Which are the

dominant criteria?

Exhibit 14-8 lists four criteria used to guide cost allocation decisions:

1. Cause and effect.

The cause-and-effect criterion and the benefits-received criterion are the dominant criteria when

14-9 “Once a company allocates corporate costs to divisions, these costs should not be

reallocated to the indirect-cost pools of the division.” Do you agree? Explain.

Disagree. If corporate costs allocated to a division can be reallocated to the indirect cost pools of

14-2

14-10 “A company should not allocate costs that are fixed in the short run to customers.” Do

you agree? Explain briefly.

Disagree. A company will frequently allocate costs that are fixed in the short run to customers to

14-11 How should a company decide on the number of cost pools it should use to allocate costs

to divisions, channels, and customers?

When allocating costs to divisions, channels, and customers, companies must construct cost

If each cost category has a cause-and-effect or benefits-received relationship with a different

14-12 Show how managers can gain insight into the causes of a sales-volume variance by

subdividing the components of this variance.

Using the levels approach introduced in Chapter 7, the sales-volume variance is a Level 2

14-13 How can the concept of a composite unit be used to explain why an unfavorable total

sales-mix variance of contribution margin occurs?

The total sales-mix variance arises from differences in the budgeted contribution margin of the

14-14 Explain why a favorable sales-quantity variance occurs.

14-15 How can the sales-quantity variance be decomposed further?

The sales-quantity variance can be decomposed into (a) a market-size variance (which arises

14-3

14-16 Flexible-budget variance, sales-quantity, market-size, and market-share variance.

The actual contribution margin per unit will impact the following sales variance:

a. Flexible-budget variance

b. Market-size variance

c. Market-share variance.

d. Sales-quantity variance

SOLUTION

Choice “a” is correct. The flexible-budget variance takes into account the difference between the

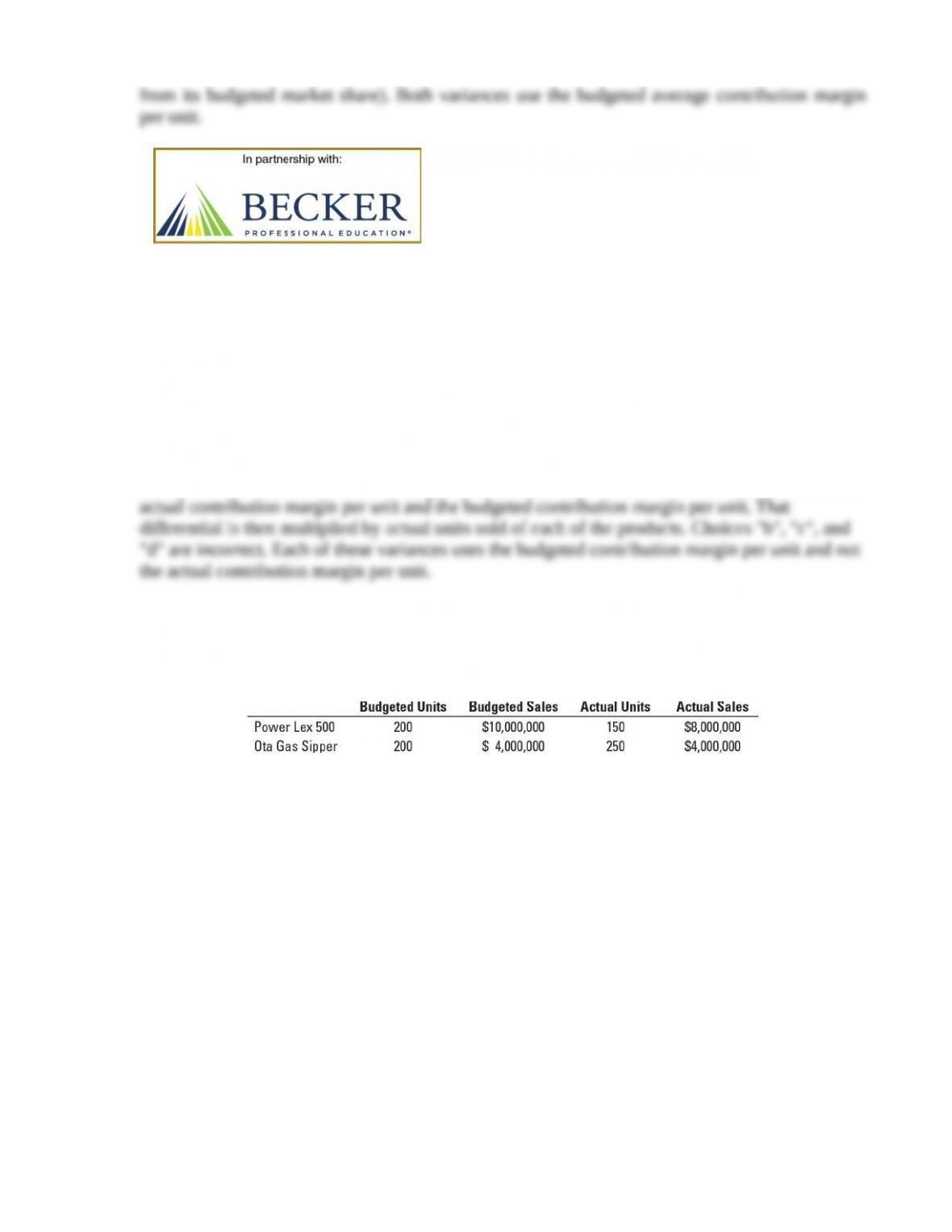

14-17 Sales-volume, sales-mix, and sales-quantity variance. Lexota, Inc., an auto

manufacturer, reported the following budgeted and actual sales of its vehicles during September,

Year 2:

The budgeted contribution margin is 20% for both vehicle types. Which of the following

statements is true concerning the sales variances for Lexota, Inc. for September, Year 2?

a. The sales-volume variance for the company is favorable.

b. The sales-quantity variance for the company is unfavorable.

c. The budgeted variable cost for each vehicle type is the same.

d. The sales-mix variance for the company is unfavorable.

14-4

SOLUTION

Choice “d” is correct. The sales mix variance evaluates the impact of the company’s departure

from the planned mix of product sales. Since the contribution margin percentage of both products

is the same and the company sold more of the low price Ota Gas Sippers and less of the high

14-18Cost allocation in hospitals, alternative allocation criteria. Harold Monette vacationed

at Lake Tahoe last winter. Unfortunately, he broke his ankle while skiing and spent two days at

the Sierra University Hospital. Monette’s insurance company received a $4,950 bill for his

two-day stay. One item that caught Monette’s attention was a $10.60 charge for a roll of cotton.

Monette is a salesman for Johnson & Johnson and knows that the cost to the hospital of the roll

of cotton is between $2.45 and $3.25. He asked for a breakdown of the $10.60 charge. The

accounting office of the hospital sent him the following information:

Monette believes the overhead charge is outrageous. He comments, “There was nothing I could

do about it. When they come in and dab your stitches, it’s not as if you can say, ‘Keep your

cotton roll. I brought my own.’”

Required:

1. Compute the overhead rate Sierra University Hospital charged on the cotton roll.

2. What criteria might Sierra use to justify allocation of the overhead items b–i in the preceding

list? Examine each item separately and use the allocation criteria listed in Exhibit 14-8 (page

572) in your answer.

3. What should Monette do about the $10.60 charge for the cotton roll?

14-5

SOLUTION

(15-20 min.) Cost allocation in hospitals, alternative allocation criteria.

million for retail customers. The company’s annual corporate-sustaining costs, such as salary for

top management and general-administration costs are $48 million. There is no cause-and-effect

or benefits-received relationship between any cost-allocation base and corporate-sustaining costs.

That is, Enviro-Tech could save corporate-sustaining costs only if the company completely shuts

down.

Required:

1. Calculate customer-level operating income using the format in Exhibit 14-3.

2. Prepare a customer-cost hierarchy report, using the format in Exhibit 14-6.

3. Enviro-Tech’s management decides to allocate all corporate-sustaining costs to distribution

channels: $38 million to the wholesale channel and $10 million to the retail channel. As a

result, distribution channel costs are now $71 million ($33 million + $38 million) for the

wholesale channel and for the retail channel. Calculate the distribution-channel-level

operating income. On the basis of these calculations, what actions, if any, should

Enviro-Tech’s managers take? Explain.

4. How might Enviro-Tech use the new cost information from its activity-based costing system

to better manage its business?

SOLUTION

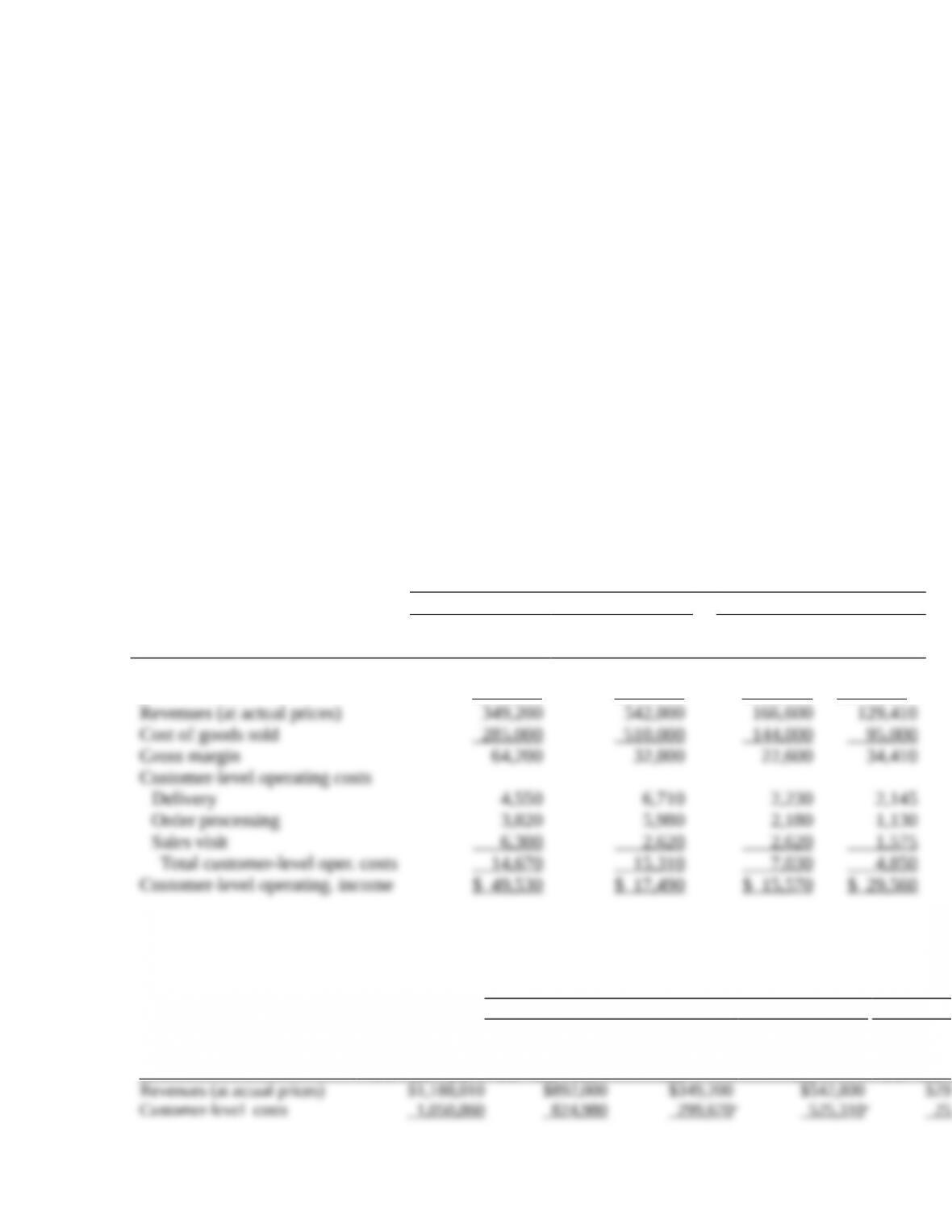

(30 min.) Customer profitability, customer-cost hierarchy.

1. All amounts in thousands of U.S. dollars

Wholesale Retail

North America South America Green Global

Wholesaler Wholesaler Energy Power

Revenues at list prices $375,000 $590,000 $175,000 $130,000

Price discounts 25 ,800 47 ,200 8 ,400 590

2 . Customer Distribution

Channels

(all amounts in $000s)

Wholesale Customers

Total Total North America South America Total

(all customers) Wholesale Wholesaler Wholesaler Retail

(1) = (2) + (5) (2) = (3) + (4) (3) (4) (5) = (6) + (7)

14-7

aCost of goods sold + Total customer-level operating costs from Requirement 1

If corporate costs are allocated to the channels, the retail channel will show an operating profit of

3. Enviro-Tech could use activity-based cost information to better manage its business by

evaluating the customer-level costs and determining which activities are providing a

value to the customer that they are willing to pay for. For example, costs of sales visits

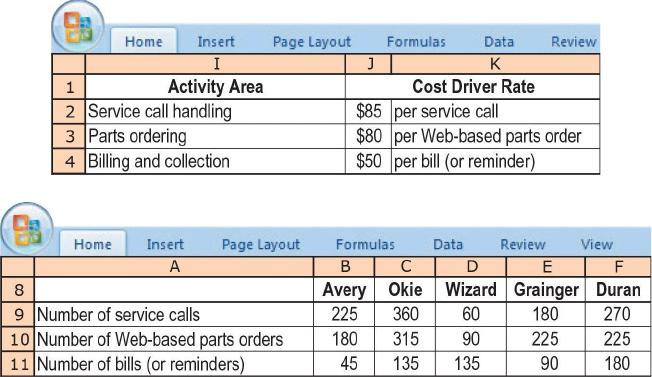

14-20 Customer profitability, service company. Instant Service (IS) repairs printers and

photocopiers for five multisite companies in a tristate area. IS’s costs consist of the cost of

technicians and equipment that are directly traceable to the customer site and a pool of office

overhead. Until recently, IS estimated customer profitability by allocating the office overhead to

each customer based on share of revenues. For 2017, IS reported the following results:

Abby Costa, IS’s new controller, notes that office overhead is more than 10% of total costs, so

she spends a couple of weeks analyzing the consumption of office overhead resources by

14-8

customers. She collects the following information:

Required:

1. Compute customer-level operating income using the new information that Costa has gathered.

2. Prepare exhibits for IS similar to Exhibits 14-4 and 14-5. Comment on the results.

3. What options should IS consider, with regard to individual customers, in light of the new data

and analysis of office overhead?

14-9