SOLUTION

(30 min.) Joint-cost allocation, sales value, physical measure, NRV methods.

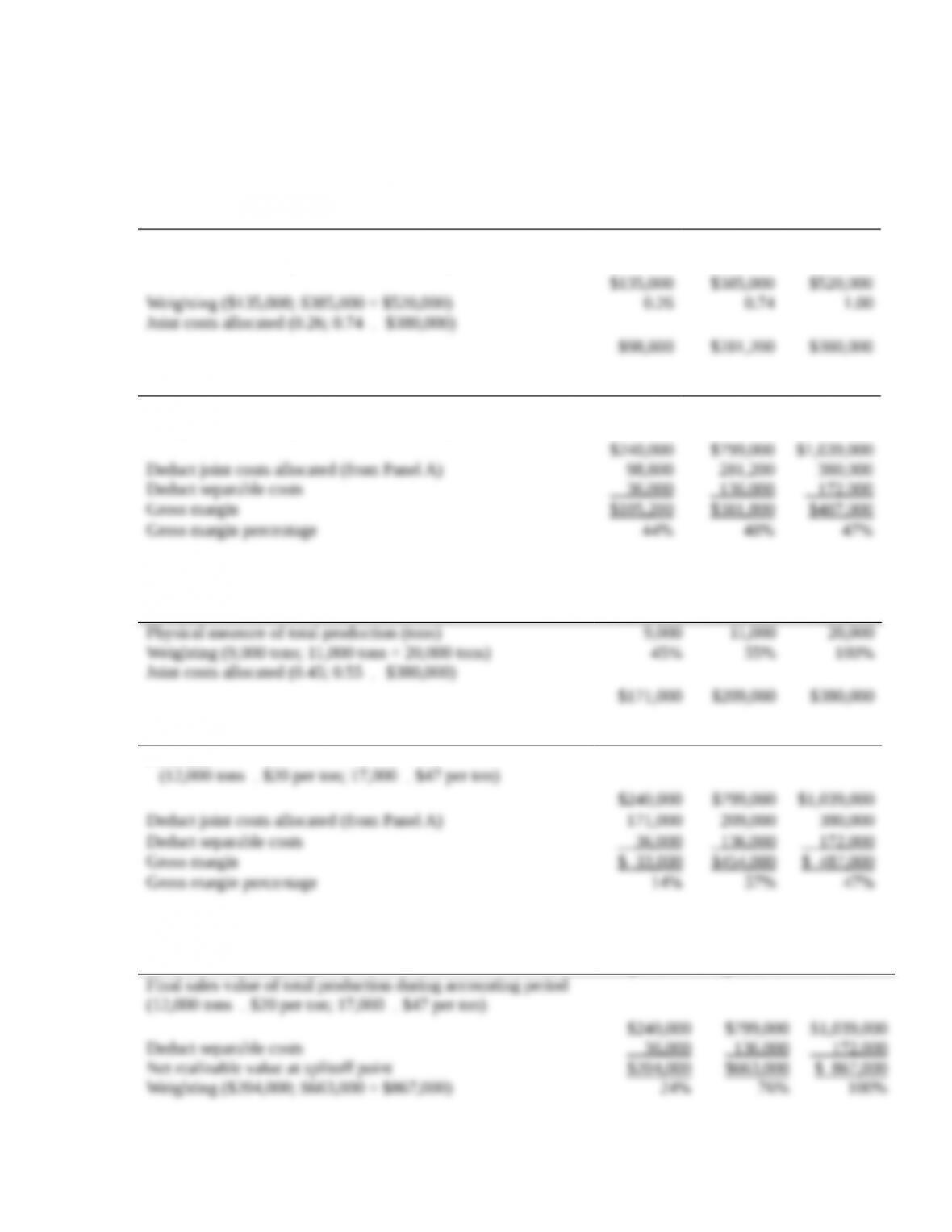

1a.

PANEL A: Allocation of Joint Costs using Sales Value at

Splitoff Method

Special B/

Beef

Ramen

Special S/

Shrimp

Ramen Total

Sales value of total production at splitoff point

(9,000 tons

´

$15 per ton; 11,000

´

$35 per ton)

PANEL B: Product-Line Income Statement for June 2017 Special B Special S Total

Revenues

(12,000 tons

´

$20 per ton; 17,000

´

$47 per ton)

1b.

PANEL A: Allocation of Joint Costs using Physical-Measure

Method

Special B/

Beef

Ramen

Special S/

Shrimp

Ramen Total

PANEL B: Product-Line Income Statement for June 2017 Special B Special S Total

Revenues

1c.

PANEL A: Allocation of Joint Costs using Net Realizable

Value Method Special B Special S Total

´

´

Joint costs allocated (0.24; 0.76

´

$380,000)

PANEL B: Product-Line Income Statement for June 2017 Special B Special S Total

Revenues

(12,000 tons

´

$20 per ton; 17,000

´

$47 per ton)

2. Sabrina Donahue probably performed the analysis shown below to arrive at the net loss

of $6,754 from marketing the stock:

PANEL A: Allocation of Joint Costs using

Sales Value at Splitoff

Special B/

Beef

Ramen

Special S/

Shrimp

Ramen Stock Total

Sales value of total production at splitoff point

´

´

´

´

PANEL B: Product-Line Income Statement

for June 2017 Special B Special S Stock Total

Revenues

(12,000 tons

´

$20 per ton; 17,000

´

$47 per

ton; 3,000

´

$5 per ton)

In this (misleading) analysis, the $380,000 of joint costs are re-allocated between Special B,

Special S, and the stock. Irrespective of the method of allocation, this analysis is wrong. Joint

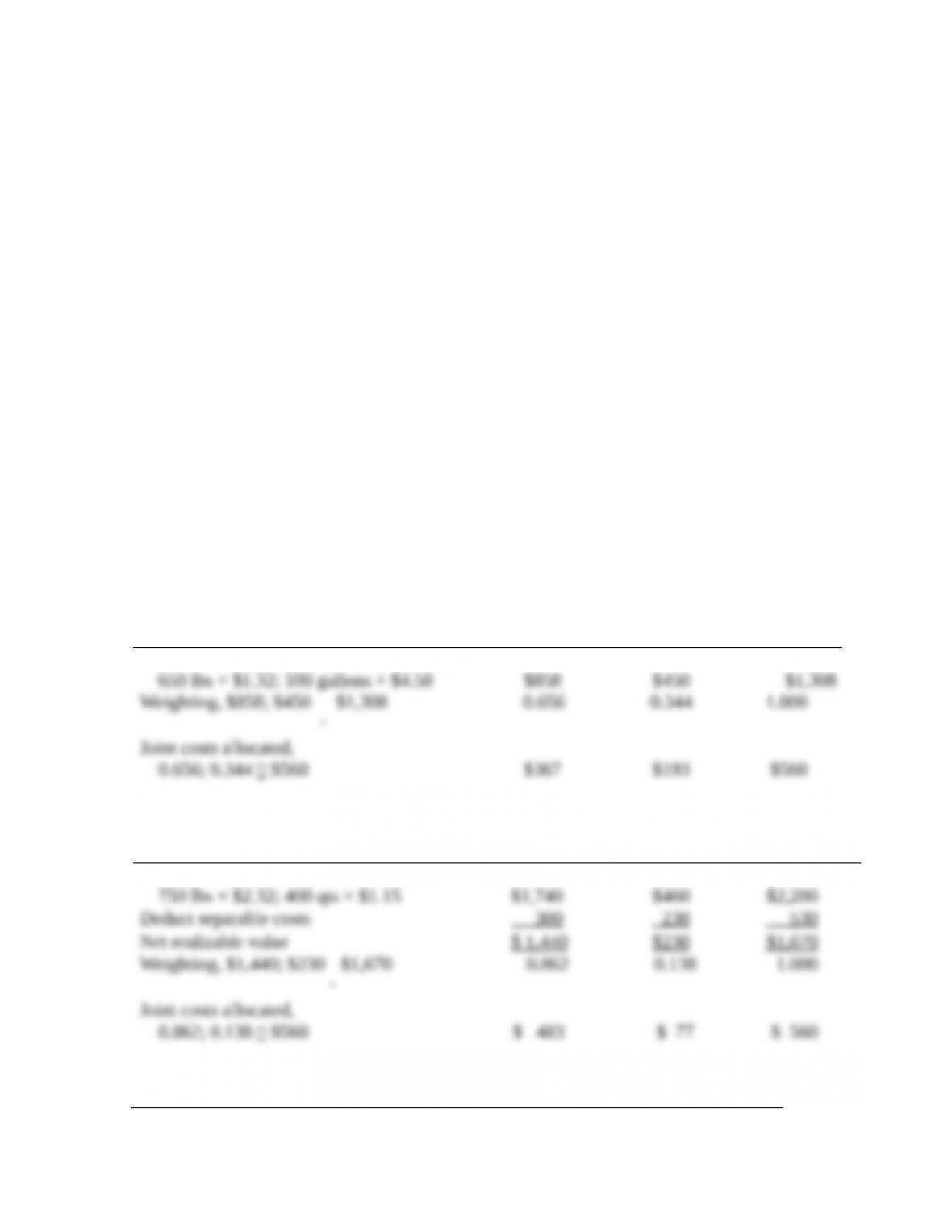

16-28 Joint-cost allocation: Sell immediately or process further. Nervana Soy Products

(NSP) buys soybeans and processes them into other soy products. Each ton of soybeans that NSP

purchases for $350 can be converted for an additional $210 into 650 pounds of soy meal and 100

gallons of soy oil. A pound of soy meal can be sold at splitoff for $1.32 and soy oil can be sold in

bulk for $4.50 per gallon.

NSP can process the 650 pounds of soy meal into 750 pounds of soy cookies at an additional

cost of $300. Each pound of soy cookies can be sold for $2.32 per pound. The 100 gallons of soy

oil can be packaged at a cost of $230 and made into 400 quarts of Soyola. Each quart of Soyola

can be sold for $1.15.

Required:

1. Allocate the joint cost to the soy cookies and the Soyola using the following:

a. Sales value at splitoff method

b. NRV method

2. Should NSP have processed each of the products further? What effect does the allocation

method have on this decision?

SOLUTION

(20 min.) Joint cost allocation: Sell immediately or process further.

1.

a. Sales value at splitoff method:

Soy cookies/

Soy meal

Soyola/

Soy oil

Total

Sales value of total production at splitoff,

b. Net realizable value method:

Soy cookies Soyola Total

Final sales value of total production,

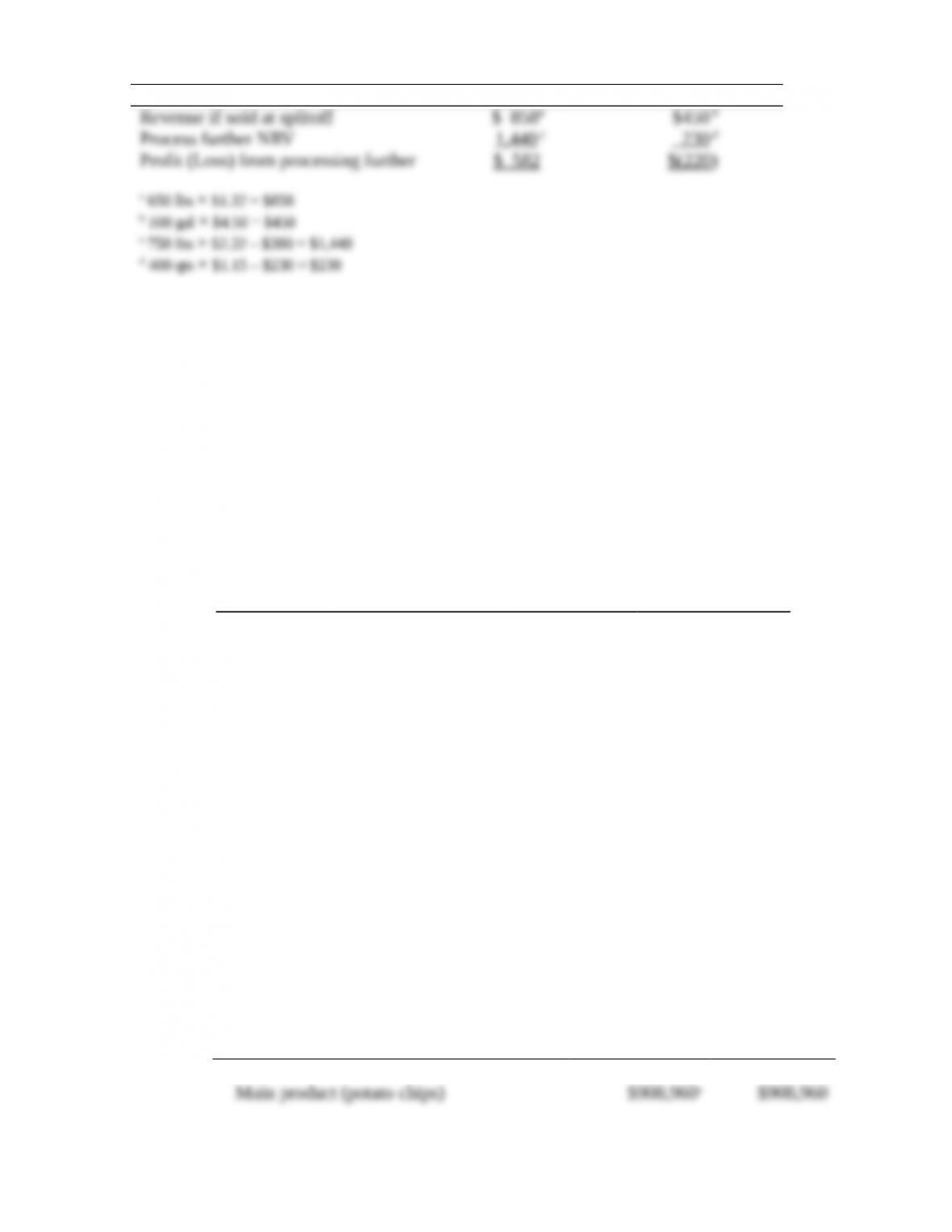

2.

Soy cookies Soyola

/Soy meal /Soy oil

NSP should process the soy meal into soy cookies because that increases profit by $582 ($1,440 –

$858). However, NSP should sell the soy oil as is, without processing it into the form of Soyola,

because profit will be $220 ($450 – $230) higher if they do. Since the total joint cost is the same

under both allocation methods, it is not a relevant cost to the decision to sell at splitoff or process

further.

16-29 Accounting for a main product and a byproduct. (Cheatham and Green, adapted)

Crispy, Inc., is a producer of potato chips. A single production process at Crispy, Inc., yields

potato chips as the main product, as well as a byproduct that can be sold as a snack. Both

products are fully processed by the splitoff point, and there are no separable costs.

For September 2017, the cost of operations is $520,000. Production and sales data are as

follows:

Production (in

pounds)

Sales (in

pounds)

Selling Price per

pound

Potato Chips 46,000 34,960 $26

Byproduct 8,200 5,000 $ 5

There were no beginning inventories on September 1, 2017.

Required:

1. What is the gross margin for Crispy, Inc., under the production method and the sales method

of byproduct accounting?

2. What are the inventory costs reported in the balance sheet on September 30, 2017, for the

main product and byproduct under the two methods of byproduct accounting in requirement

1?

3. Prepare the journal entries to record the byproduct activities under (a) the production method

and (b) the sales method. Briefly discuss the effects on the financial statements.

SOLUTION

(30 min.) Accounting for a main product and a byproduct.

Production

Method

Sales

Method

1. Revenues

Production

Method

Sales

Method

a Ending inventory shown at unrealized selling price.

BI + Production – Sales = EI

3. Byproduct—production method journal entries

i) At time of production:

ii) At time of sale:

For Byproduct

2. Byproduct—sales method journal entries

i) At time of production:

ii) At time of sale:

For Byproduct

16-30 Joint costs and decision making. Jack Bibby is a prospector in the Texas Panhandle. He

has also been running a side business for the past couple of years. Based on the popularity of shows

such as “Rattlesnake Nation,” there has been a surge of interest from professionals and amateurs to

visit the northern counties of Texas to capture snakes in the wild. Jack has set himself up as a

purchaser of these captured snakes.

Jack purchases rattlesnakes in good condition from “snake hunters” for an average of $11 per

snake. Jack produces canned snake meat, cured skins, and souvenir rattles, although he views

snake meat as his primary product. At the end of the recent season, Jack Bibby evaluated his

financial results:

Meat Skins Rattles Total

Sales revenues $33,000 $8,800 $2,200 $44,000

Share of snake

cost

19,800 5,280 1,320 26,400

Processing

expenses

6,600 990 660 8,250

Allocated

overhead

4,400 660 440 5,500

Income (loss) $ 2,200 $1,870 ($ 220) $ 3,850

The cost of snakes is assigned to each product line using the relative sales value of meat,

skins, and rattles (i.e., the percentage of total sales generated by each product). Processing

expenses are directly traced to each product line. Overhead costs represent Jack’s basic living

expenses. These are allocated to each product line on the basis of processing expenses.

Jack has a philosophy of every product line paying for itself and is determined to cut his

losses on rattles.

Required:

1. Should Jack Bibby drop rattles from his product offerings? Support your answer with

computations.

2. An old miner has offered to buy every rattle “as is” for $0.60 per rattle (note: “as is” refers to

the situation where Jack only removes the rattle from the snake and no processing costs are

incurred). Assume that Jack expects to process the same number of snakes each season.

Should he sell rattles to the miner? Support your answer with computations.

SOLUTION

(20 min.) Joint costs and decision making.

1. For analyzing the incremental value generated by rattles as a product line, the allocation

of the cost of the snake (which is a joint cost) is irrelevant since it is sunk. The allocated

2. Jack purchases snakes at a unit cost of $11. Given the total snake cost of $26,400, this

Since the miner is offering just $0.60 per rattle, Jack is better off processing and selling the

rattles on his own.

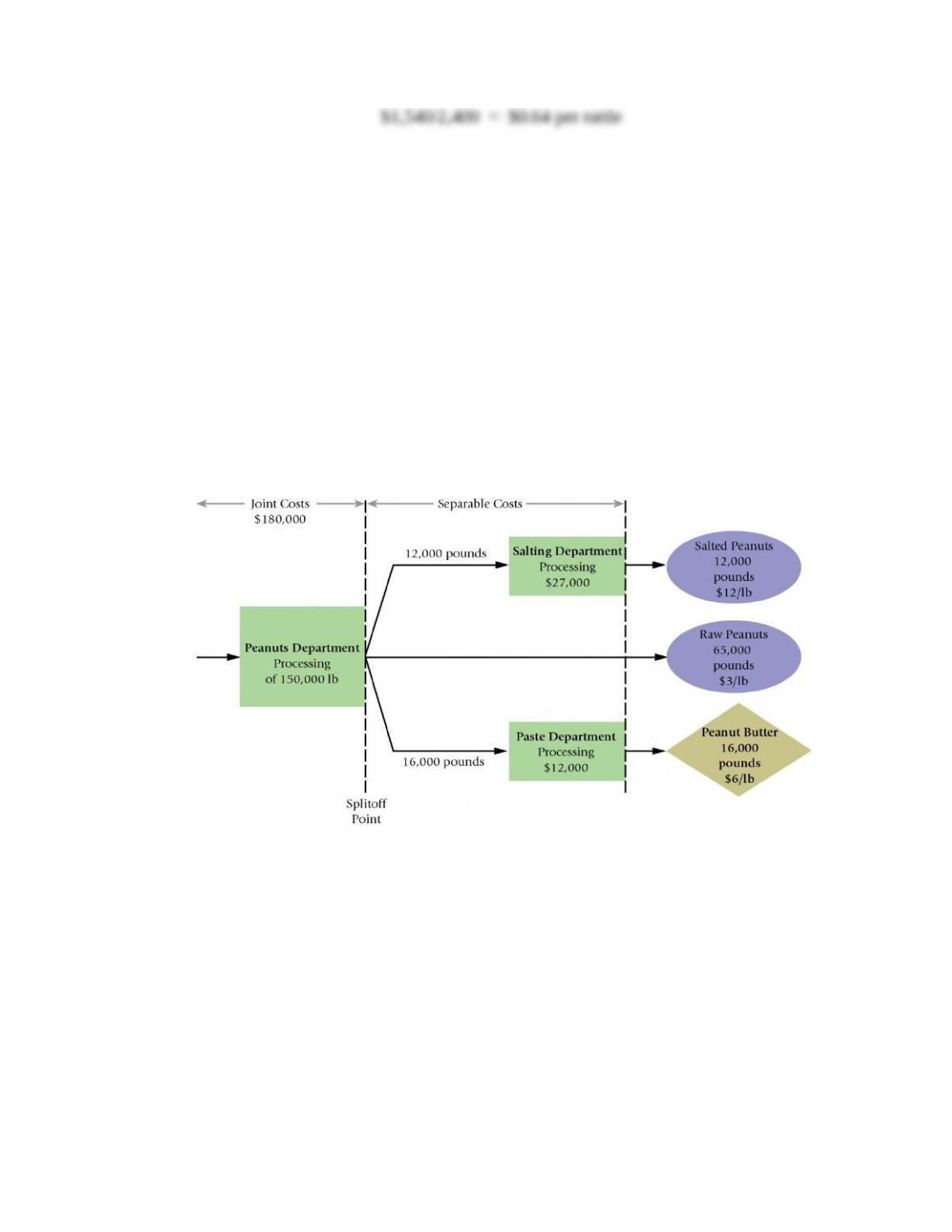

16-31 Joint costs and byproducts. (W. Crum adapted) Royston, Inc., is a large food-processing

company. It processes 150,000 pounds of peanuts in the peanuts department at a cost of $180,000

to yield 12,000 pounds of product A, 65,000 pounds of product B, and 16,000 pounds of product

C.

■ Product A is processed further in the salting department at a cost of $27,000. It yields 12,000

pounds of salted peanuts, which are sold for $12 per pound.

■ Product B (raw peanuts) is sold without further processing at $3 per pound.

■ Product C is considered a byproduct and is processed further in the paste department at a cost

of $12,000. It yields 16,000 pounds of peanut butter, which are sold for $6 per pound.

The company wants to make a gross margin of 10% of revenues on product C and needs to allow

20% of revenues for marketing costs on product C. An overview of operations follows:

Required:

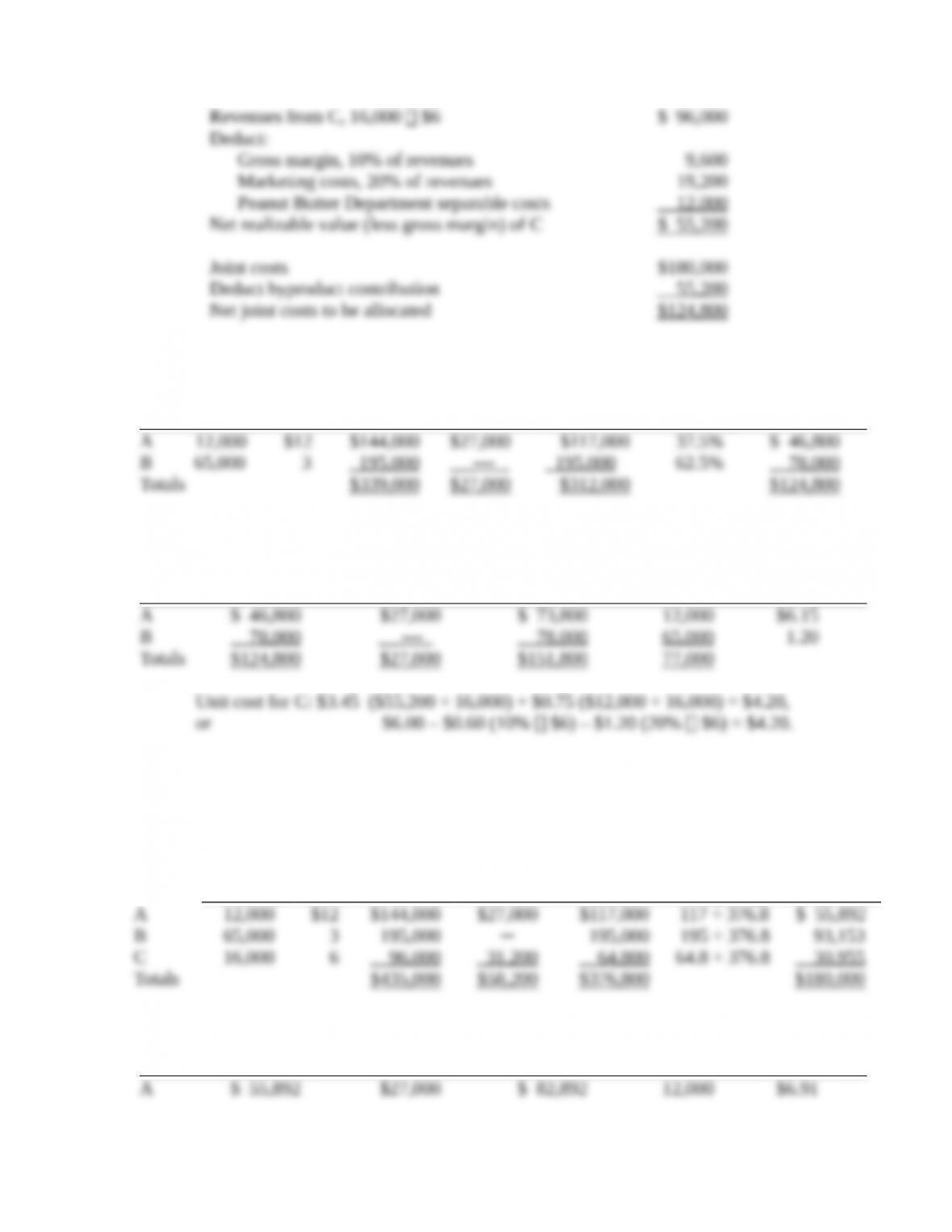

1. Compute unit costs per pound for products A, B, and C, treating C as a byproduct. Use the

NRV method for allocating joint costs. Deduct the NRV of the byproduct produced from the

joint cost of products A and B.

2. Compute unit costs per pound for products A, B, and C, treating all three as joint products

and allocating joint costs by the NRV method.

SOLUTION

(35-45 min.) Joint costs and byproducts.

1. Computing byproduct deduction to joint costs:

Deduct Net

Unit Final Separable Realizable Allocation of

Sales Sales Processing Value at $124,800

Quantity Price Value Cost Splitoff Weighting Joint Costs

Add Separable

Joint Costs Processing

Allocation Costs Total Costs Units Unit Cost

2. If all three products are treated as joint products:

Quantity

Unit

Sales

Price

Final

Sales

Value

Deduct

Separable

Processing

Cost

Net

Realizable

Value at

Splitoff Weighting

Allocation

of

$180,000

Joint

Costs

Add Separable

Joint Costs Processing

Allocation Costs Total Costs Units Unit Cost

Call the attention of students to the different unit “costs” resulting from the two assumptions

about the relative importance of Product C. The point is that costs of individual products depend

heavily on which assumptions are made and which accounting methods and techniques are used.

16-32 Methods of joint-cost allocation, ending inventory. Garden Labs produces a drug used

for the treatment of arthritis. The drug is produced in batches. Chemicals costing $50,000 are

mixed and heated, then a unique separation process extracts the drug from the mixture. A batch

yields a total of 3,000 gallons of the chemicals. The first 2,500 gallons are sold for human use

while the last 500 gallons, which contain impurities, are sold to veterinarians.

The costs of mixing, heating, and extracting the drug amount to $155,000 per batch. The

output sold for human use is pasteurized at a total cost of $130,000 and is sold for $600 per

gallon. The product sold to veterinarians is irradiated at a cost of $20 per gallon and is sold for

$450 per gallon.

In March, Garden, which had no opening inventory, processed one batch of chemicals. It sold

2,000 gallons of product for human use and 300 gallons of the veterinarian product. Garden uses

the net realizable value method for allocating joint production costs.

Required:

1. How much in joint costs does Garden allocate to each product?

2. Compute the cost of ending inventory for each of Garden’s products.

3. If Garden were to use the constant gross-margin percentage NRV method instead, how would

it allocate its joint costs?

4. Calculate the gross margin on the sale of the product for human use in March under the

constant gross-margin percentage NRV method.

5. Suppose that the separation process also yields 300 pints of a toxic byproduct. Garden

currently pays a hauling company $6,000 to dispose of this byproduct. Garden is contacted

by a firm interested in purchasing a modified form of this byproduct for a total price of

$7,000. Garden estimates that it will cost about $35 per pint to do the required modification.

Should Garden accept the offer