Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

SOLUTION EXHIBIT 16-23 (all numbers are in thousands)

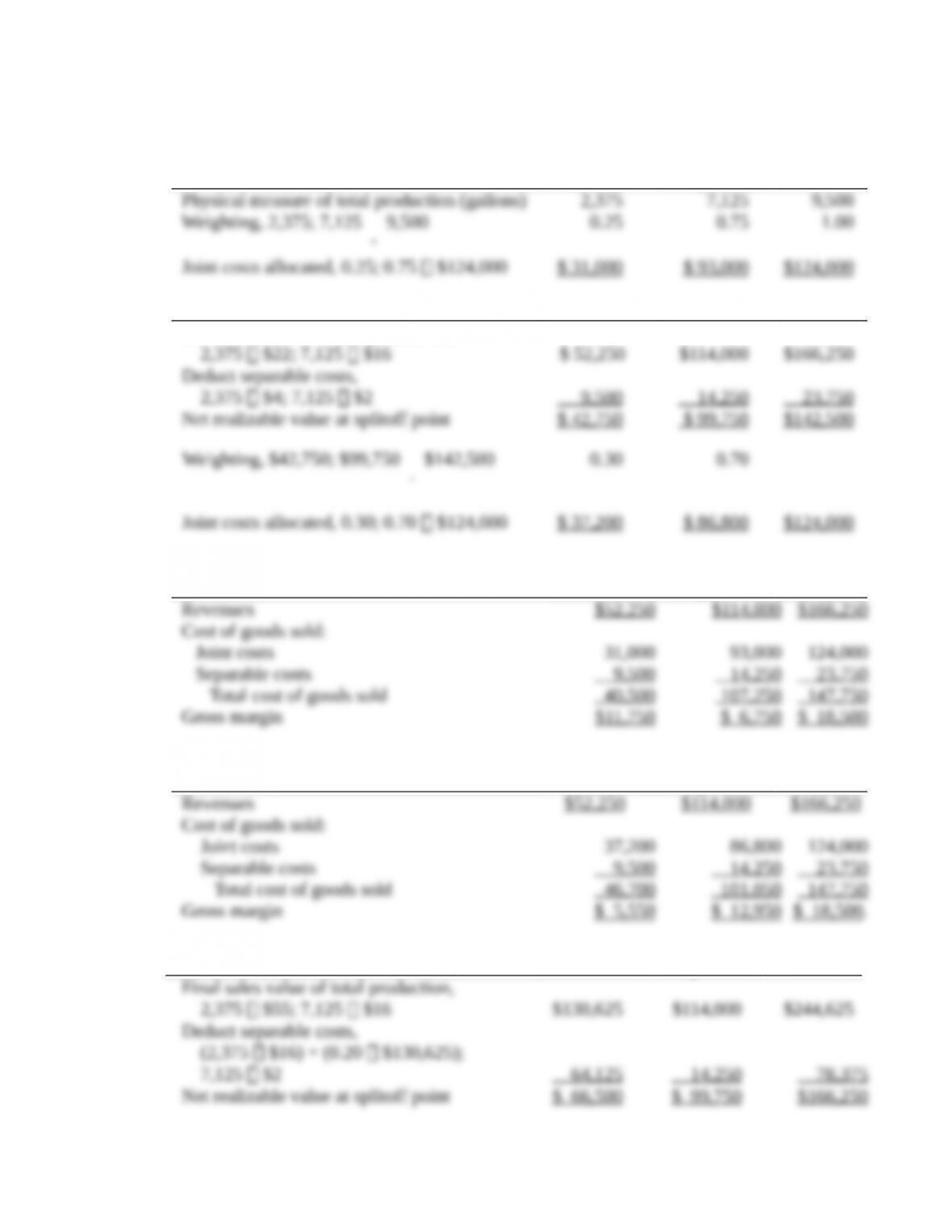

16-24 Alternative joint-cost-allocation methods, further-process decision. The Tempura

Spirits Company produces two products—methanol (wood alcohol) and turpentine—by a joint

process. Joint costs amount to $124,000 per batch of output. Each batch totals 9,500 gallons:

25% methanol and 75% turpentine. Both products are processed further without gain or loss in

volume. Separable processing costs are methanol, $4 per gallon, and turpentine, $2 per gallon.

Methanol sells for $22 per gallon. Turpentine sells for $16 per gallon.

Required:

1. How much of the joint costs per batch will be allocated to methanol and to turpentine,

assuming that joint costs are allocated based on the number of gallons at splitoff point?

2. If joint costs are allocated on an NRV basis, how much of the joint costs will be allocated to

methanol and to turpentine?

3Prepare product-line income statements per batch for requirements 1 and 2. Assume no

beginning or ending inventories.

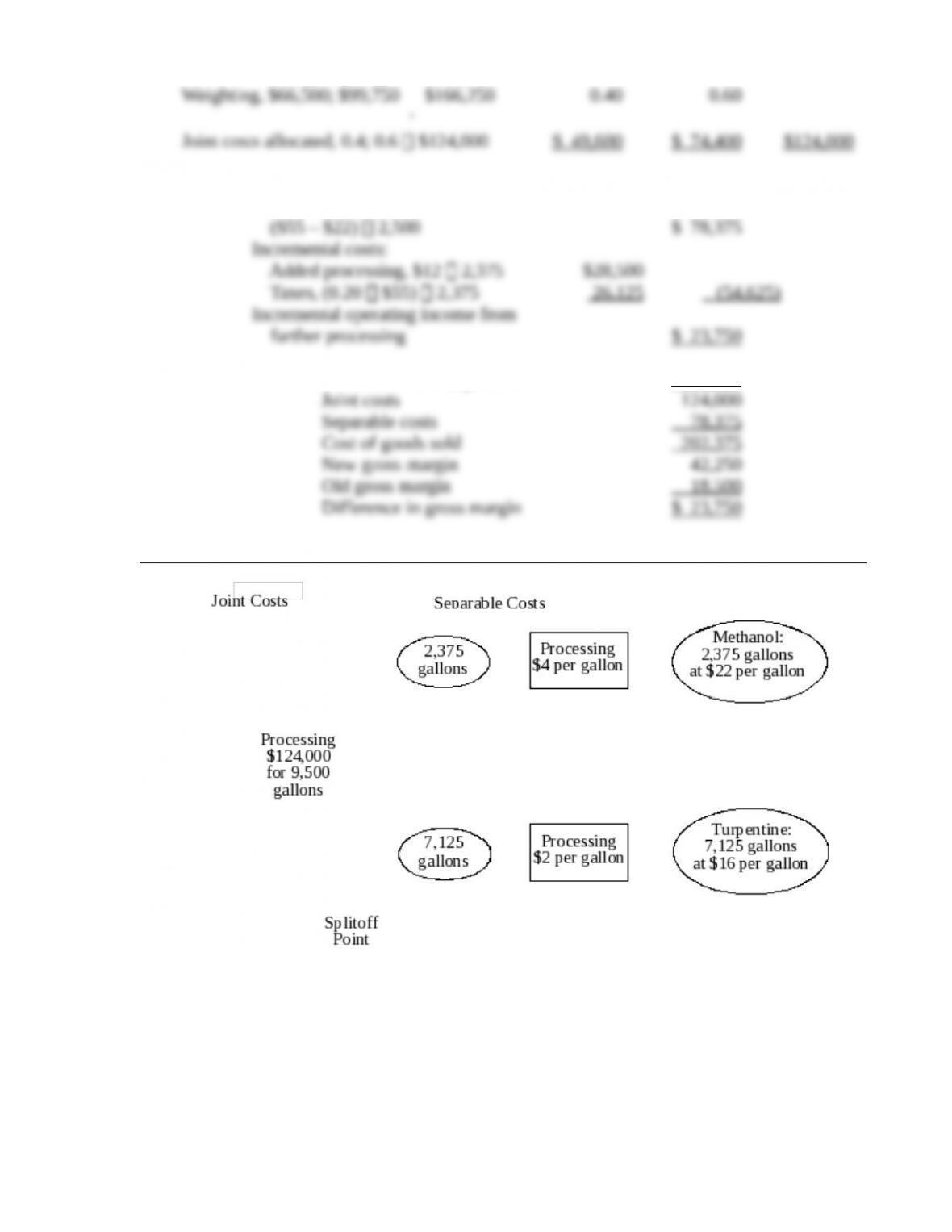

4. The company has discovered an additional process by which the methanol (wood alcohol)

can be made into a pleasant-tasting alcoholic beverage. The selling price of this beverage

would be $55 a gallon. Additional processing would increase separable costs $12 per gallon

(in addition to the $4 per gallon separable cost required to yield methanol). The company

would have to pay excise taxes of 20% on the selling price of the beverage. Assuming no

other changes in cost, what is the joint cost applicable to the wood alcohol (using the NRV

method)? Should the company produce the alcoholic beverage? Show your computations.

SOLUTION

(40 min.) Alternative joint-cost-allocation methods, further-process decision.

A diagram of the situation is in Solution Exhibit 16-24.

1. Methanol Turpentine Total

2. Methanol Turpentine Total

Final sales value of total production,

3. a. Physical-measure (gallons) method:

Methanol Turpentine Total

b. Estimated net realizable value method:

Methanol Turpentine Total

Alcohol Bev. Turpentine Total

An incremental approach demonstrates that the company should use the new process:

Incremental revenue,

Proof: Total sales of both products $244,625

SOLUTION EXHIBIT 16-24

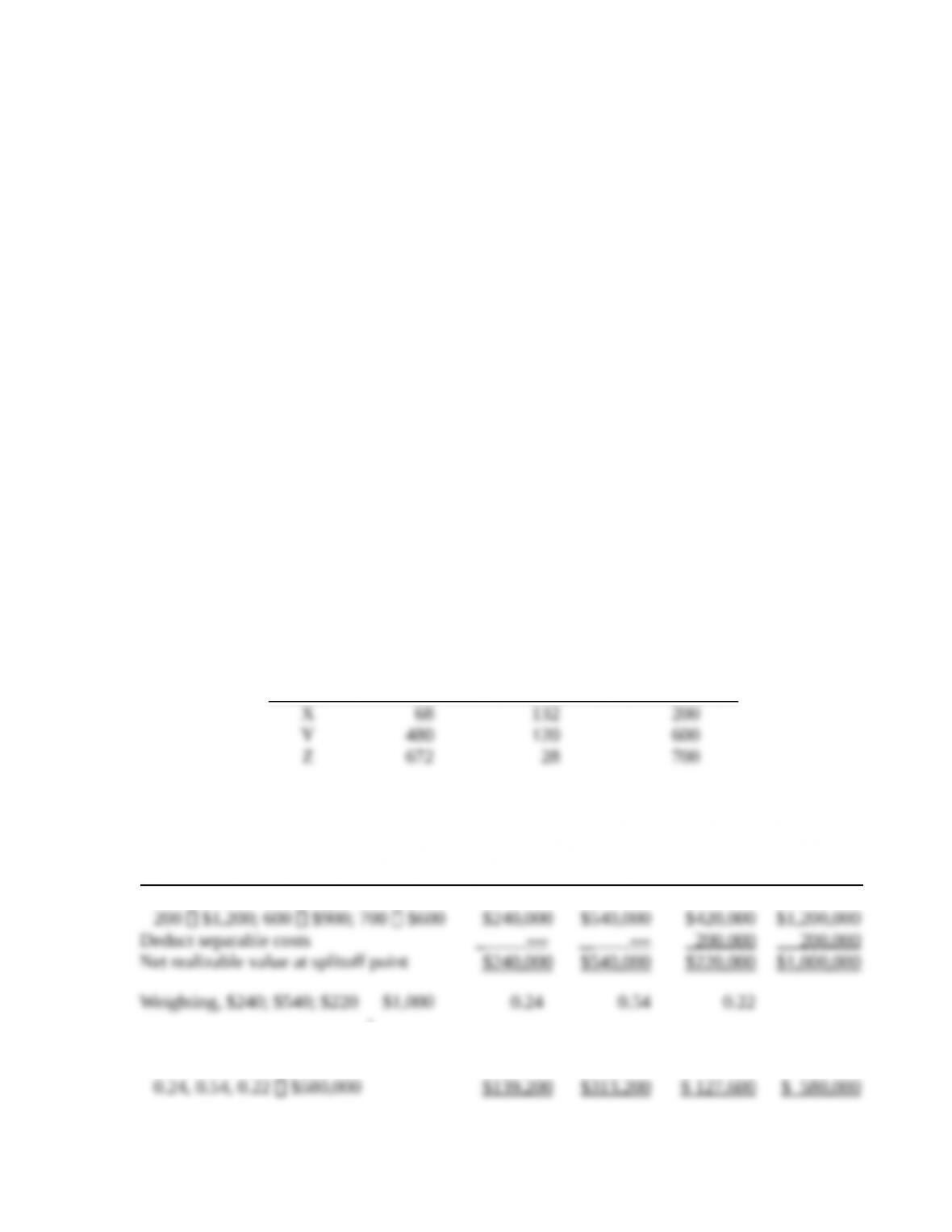

16-25 Alternative methods of joint-cost allocation, ending inventories. The Cook Company

operates a simple chemical process to convert a single material into three separate items, referred

to here as X, Y, and Z. All three end products are separated simultaneously at a single splitoff

point.

Products X and Y are ready for sale immediately upon splitoff without further processing or

any other additional costs. Product Z, however, is processed further before being sold. There is

no available market price for Z at the splitoff point.

The selling prices quoted here are expected to remain the same in the coming year. During

2017, the selling prices of the items and the total amounts sold were as follows:

■X—68 tons sold for $1,200 per ton

■Y—480 tons sold for $900 per ton

■Z—672 tons sold for $600 per ton

The total joint manufacturing costs for the year were $580,000. Cook spent an additional

$200,000 to finish product Z.

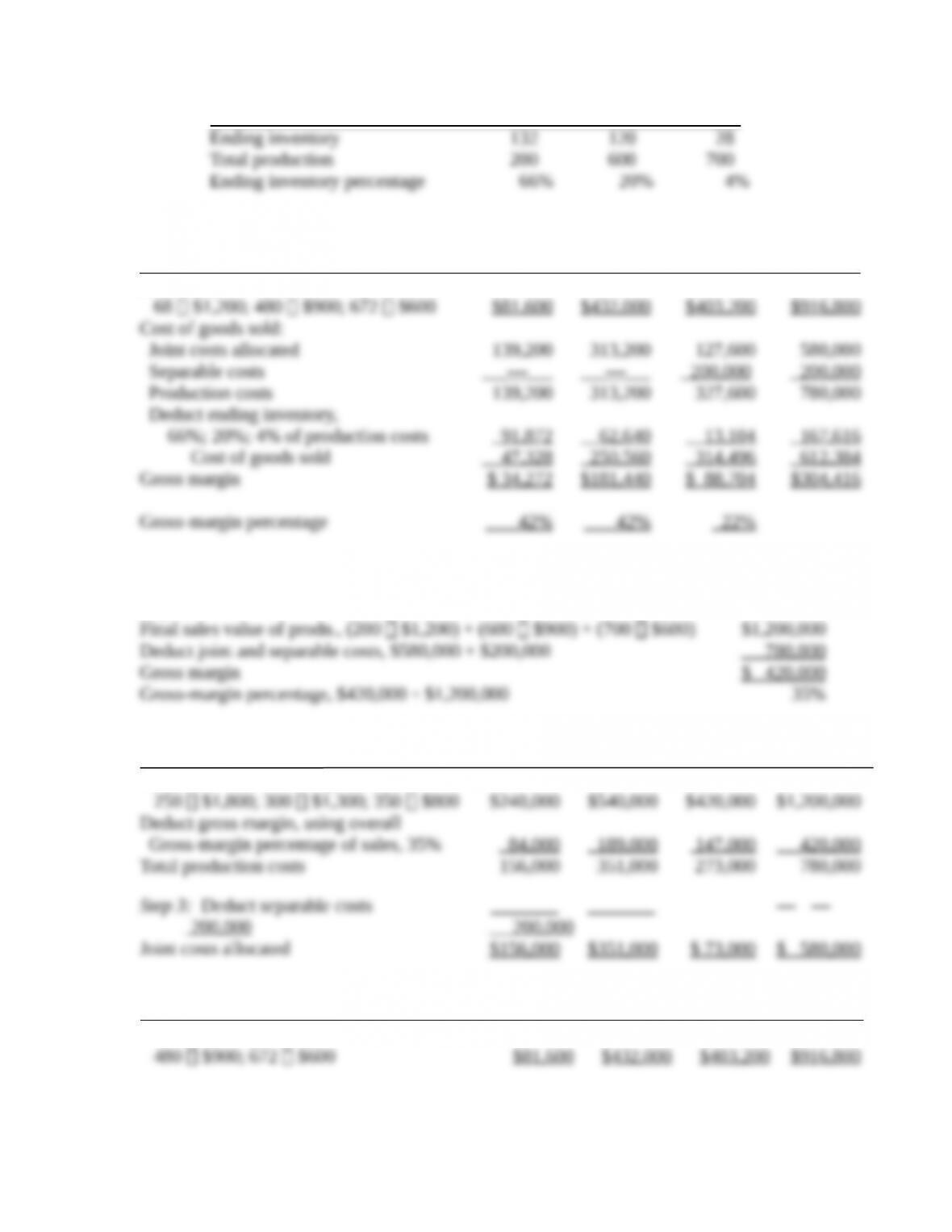

There were no beginning inventories of X, Y, or Z. At the end of the year, the following

inventories of completed units were on hand: X, 132 tons; Y, 120 tons; Z, 28 tons. There was no

beginning or ending work in process.

Required:

1. Compute the cost of inventories of X, Y, and Z for balance sheet purposes and the cost of

goods sold for income statement purposes as of December 31, 2017, using the following

joint-cost-allocation methods:

a. NRV method

b. Constant gross-margin percentage NRV method

2. Compare the gross-margin percentages for X, Y, and Z using the two methods given in

requirement 1.

SOLUTION

(40 min.) Alternative methods of joint-cost allocation, ending inventories.

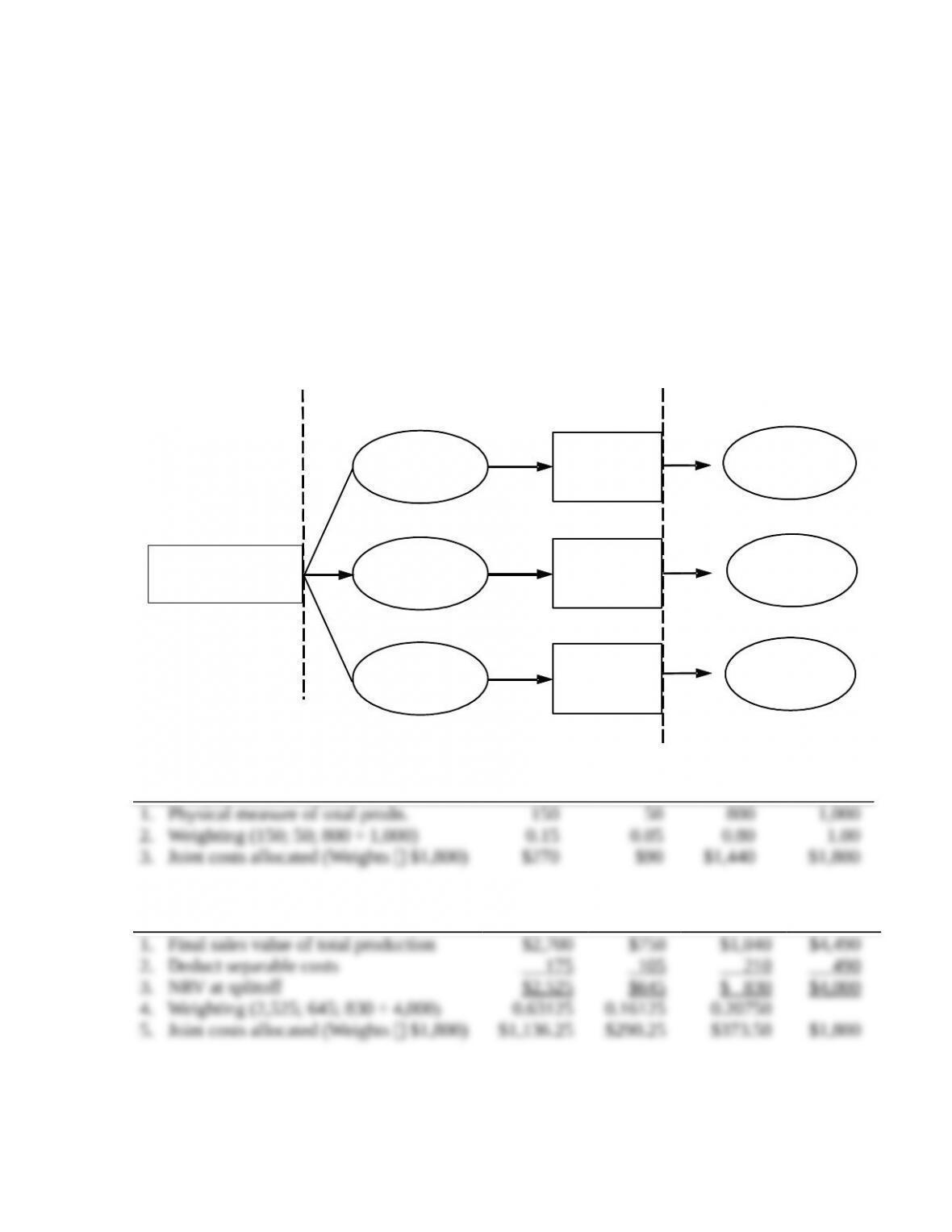

Total production for the year was:

Ending Total

Sold Inventories Production

A diagram of the situation is in Solution Exhibit 16-25.

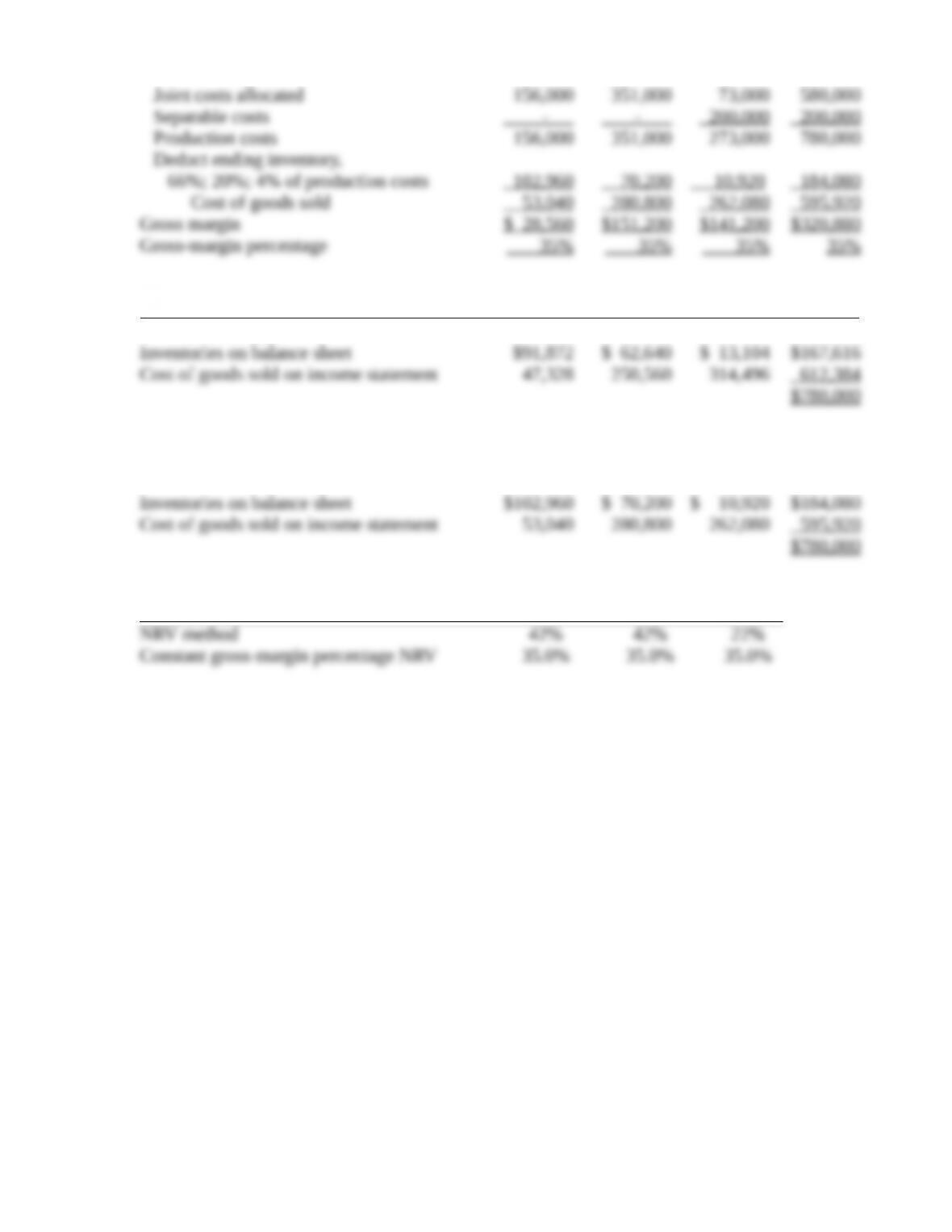

1. a. Net realizable value (NRV) method:

X Y Z Total

Final sales value of total production,

¸

Joint costs allocated,

Ending Inventory Percentages:

X Y Z

Income Statement

X Y Z Total

Revenues,

b. Constant gross-margin percentage NRV method:

Step 1:

Step 2:

X Y Z Total

Final sales value of total production,

Income Statement

X Y Z Total

Revenues, 68 $1,200;

Cost of goods sold:

Summary

X Y Z Total

a. NRV method:

b. Constant gross-margin

percentage NRV method

2.Gross-margin percentages:

X Y Z

SOLUTION EXHIBIT 16-25

Splitoff

Point

Processing

$200000

Product Y:

600 tons at

$900 per ton

Product X:

200 tons at

$1,200 per ton

Joint

Processing

Costs

$580,000

Product Z:

700 tons at

$600 per ton

Joint Costs

Separable Costs

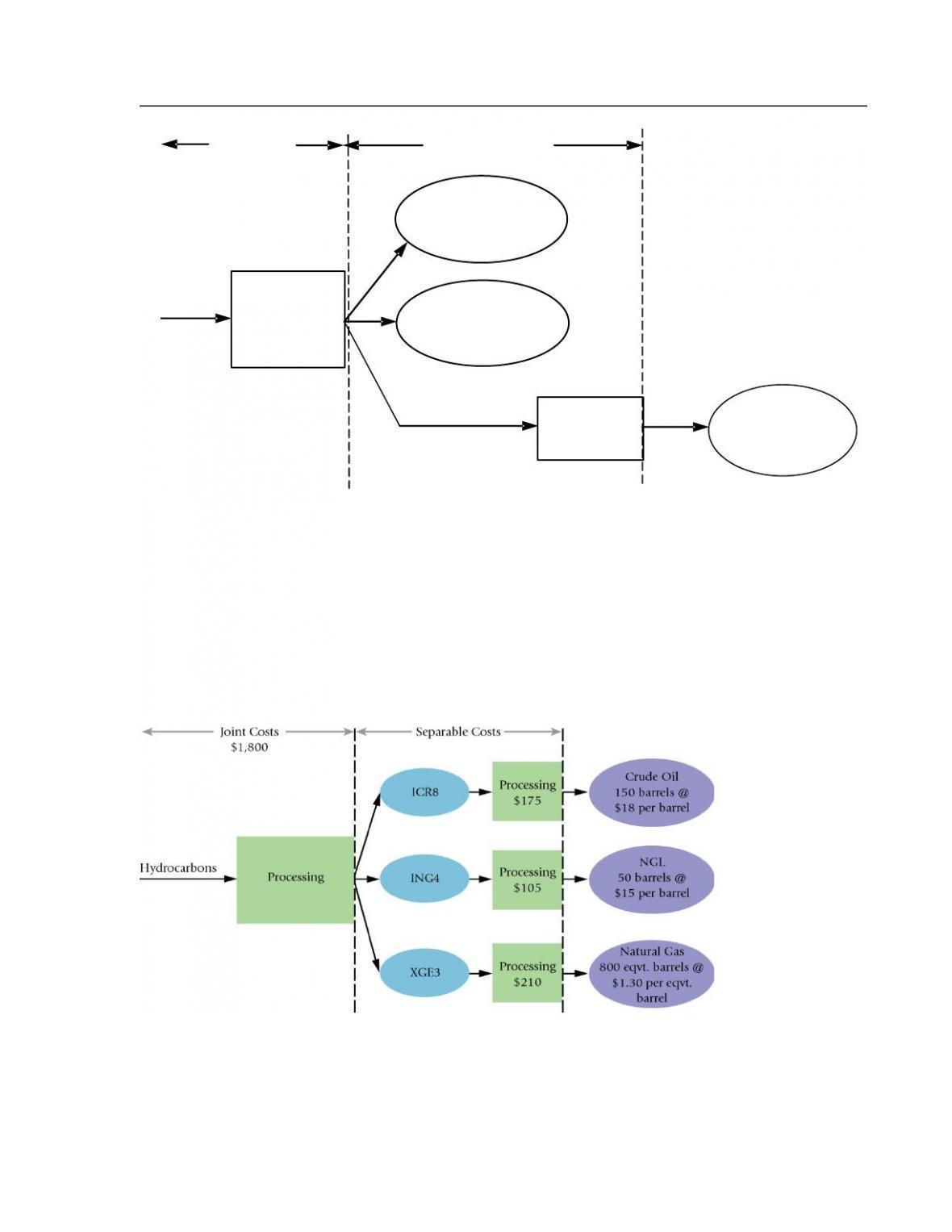

16-26 Joint-cost allocation, process further. Sinclair Oil & Gas, a large energy conglomerate,

jointly processes purchased hydrocarbons to generate three nonsalable intermediate products:

ICR8, ING4, and XGE3. These intermediate products are further processed separately to produce

crude oil, natural gas liquids (NGL), and natural gas (measured in liquid equivalents). An

overview of the process and results for August 2017 are shown here. (Note: The numbers are

small to keep the focus on key concepts.)

A federal law that has recently been passed taxes crude oil at 30% of operating income. No new

tax is to be paid on natural gas liquids or natural gas. Starting August 2017, Sinclair Oil & Gas

must report a separate product-line income statement for crude oil. One challenge facing Sinclair

Oil & Gas is how to allocate the joint cost of producing the three separate salable outputs.

Assume no beginning or ending inventory.

Required:

1. Allocate the August 2017 joint cost among the three products using the following:

a. Physical-measure method

b. NRV method

2. Show the operating income for each product using the methods in requirement 1.

3. Discuss the pros and cons of the two methods to Sinclair Oil & Gas for making decisions

about product emphasis (pricing, sell-or-process-further decisions, and so on).

4. Draft a letter to the taxation authorities on behalf of Sinclair Oil & Gas that justifies the

joint-cost-allocation method you recommend Sinclair use.

SOLUTION

(30 min.) Joint-cost allocation, process further.

Joint Costs =

$1800

ICR8

(Non-Saleable)

ING4

(Non-Saleable)

XGE3

(Non-Saleable)

Processing

$175

Processing

$210

Processing

$105

Crude Oil

150 bbls × $18 / bbl =

$2700

NGL

50 bbls × $15 / bbl =

$750

Gas

800 eqvt bbls ×

$1.30 / eqvt bbl =

$1040

Splitoff

Point

1a. Physical Measure Method

Crude Oil NGL Gas Total

1b. NRV Method

Crude Oil NGL Gas Total

2. The operating-income amounts for each product using each method is:

(a) Physical Measure Method

Crude Oil NGL Gas Total

(b) NRV Method

Crude Oil NGL Gas Total

3. Neither method should be used for product emphasis decisions. It is inappropriate to use

joint-cost-allocated data to make decisions regarding dropping individual products, or pushing

4. Since crude oil is the only product subject to taxation, it is clearly in Sinclair’s best interest to

use the NRV method since it leads to a lower profit for crude oil and, consequently, a smaller tax

16-27 Joint-cost allocation, sales value, physical measure, NRV methods. Tasty Foods

produces two types of microwavable products: beef-flavored ramen and shrimp-flavored ramen.

The two products share common inputs such as noodle and spices. The production of ramen

results in a waste product referred to as stock, which Tasty dumps at negligible costs in a local

drainage area. In June 2017, the following data were reported for the production and sales of

beef-flavored and shrimp-flavored ramen:

Due to the popularity of its microwavable products, Tasty decides to add a new line of products that

targets dieters. These new products are produced by adding a special ingredient to dilute the original

ramen and are to be sold under the names Special B and Special S, respectively. Following are the

monthly data for all the products:

Required:

1. Calculate Tasty’s gross-margin percentage for Special B and Special S when joint costs are

allocated using the following:

a. Sales value at splitoff method

b. Physical-measure method

c. Net realizable value method

2. Recently, Tasty discovered that the stock it is dumping can be sold to cattle ranchers at $5 per

ton. In a typical month with the production levels shown, 3,000 tons of stock are produced

and can be sold by incurring marketing costs of $11,100. Sabrina Donahue, a management

accountant, points out that treating the stock as a joint product and using the sales value at

splitoff method, the stock product would lose about $6,754 each month, so it should not be

sold. How did Donahue arrive at that final number, and what do you think of her analysis?

Should Tasty sell the stock?