CHAPTER 4

JOB COSTING

4-1 Define cost pool, cost tracing, cost allocation, and cost-allocation base.

Cost pool––a grouping of individual indirect cost items.

4-2 How does a job-costing system differ from a process-costing system?

In a job-costing system, costs are assigned to a distinct unit, batch, or lot of a product or service.

4-3 Why might an advertising agency use job costing for an advertising campaign by

PepsiCo, whereas a bank might use process costing to determine the cost of checking account

deposits?

An advertising campaign for Pepsi is likely to be very specific to that individual client. Job

4-4 Describe the seven steps in job costing.

The seven steps in job costing are (1) identify the job that is the chosen cost object, (2) identify

4-5 Give examples of two cost objects in companies using job costing.

Major cost objects that managers focus on in companies using job costing are a product such as a

4-6 Describe three major source documents used in job-costing systems.

Three major source documents used in job-costing systems are (1) job cost record or job cost

sheet, a document that records and accumulates all costs assigned to a specific job, starting when

4-7 What is the advantage of using computerized source documents to prepare job-cost

records?

The main advantages of using computerized source documents for job cost records are the

4-8 Give two reasons why most organizations use an annual period rather than a weekly or

monthly period to compute budgeted indirect-cost rates.

Two reasons for using an annual period to compute budgeted indirect cost rates are:

a. The numerator reason––the longer the time period, the less the influence of seasonal

4-9 Distinguish between actual costing and normal costing.

Actual costing and normal costing differ in their use of actual or budgeted indirect cost rates:

Actual

Costing

Normal

Costing

Direct-cost rates

Indirect-cost rates

Actual rates

Actual rates

Actual rates

Budgeted rates

4-10 Describe two ways in which a house-construction company may use job-cost

information.

A house construction firm can use job cost information (1) to determine the profitability of

4-11 Comment on the following statement: “In a normal-costing system, the amounts in the

Manufacturing Overhead Control account will always equal the amounts in the Manufacturing

Overhead Allocated account.”

The statement is false. In a normal costing system, the Manufacturing Overhead Control account

will not, in general, equal the amounts in the Manufacturing Overhead Allocated account. The

4-12 Describe three different debit entries to the Work-in-Process Control T-account under

normal costing.

Debit entries to Work-in-Process Control represent increases in work in process. Examples of

4-13 Describe three alternative ways to dispose of under- or overallocated overhead costs.

Alternative ways to make end-of-period adjustments to dispose of underallocated or

overallocated overhead are as follows:

(i) Proration based on the total amount of indirect costs allocated (before proration) in

(ii) Proration based on total ending balances (before proration) in work in process,

(iii) Year-end write-off to Cost of Goods Sold

4-14 When might a company use budgeted costs rather than actual costs to compute

direct-labor rates?

A company might use budgeted costs rather than actual costs to compute direct labor rates

4-15 Describe briefly why Electronic Data Interchange (EDI) is helpful to managers.

Modern technology of electronic data interchange (EDI) is helpful to managers because it

4.16Which of the following does not accurately describe the application of job-order costing?

a. Finished goods that are purchased by customers will directly impact cost of goods sold.

b. Indirect manufacturing labor and indirect materials are part of the actual manufacturing costs

incurred.

c. Direct materials and direct manufacturing labor are included in total manufacturing costs.

d. Manufacturing overhead costs incurred is used to determine total manufacturing costs.

SOLUTION

Choice “d” is correct. Total manufacturing costs contains manufacturing costs applied, not actual

manufacturing costs incurred. The application of job order costing may result in over-applied or

underapplied overhead because of differences in applied and actual manufacturing overhead.

a. Choice “a” is incorrect. The finished goods that are purchased reduce the finished goods

4-17 Sturdy Manufacturing Co. assembled the following cost data for job order #23:

What are the total manufacturing costs for job order #23 if the company uses normal job-order

costing?

a. $191,500 b. $193,500

c. $194,500 d. $195,500

SOLUTION

Choice “d” is correct. Total manufacturing costs include direct materials, direct manufacturing

4-18 For which of the following industries would job-order costing most likely not be

appropriate?

a. Small business printing. b. Cereal production.

c. Home construction. d. Aircraft assembly.

SOLUTION

Choice “b” is correct. The cereal products business involves the production of a number of

homogeneous items. As a result, it is more conducive to the use of process costing than job-order

costing.

4-19 ABC Company uses job-order costing and has assembled the following cost data for the

production and assembly of item X:

Based on the above cost data, the manufacturing overhead for item X is:

a. $500 overallocated.

b. $600 underallocated.

c. $500 underallocated

d. $600 overallocated.

SOLUTION

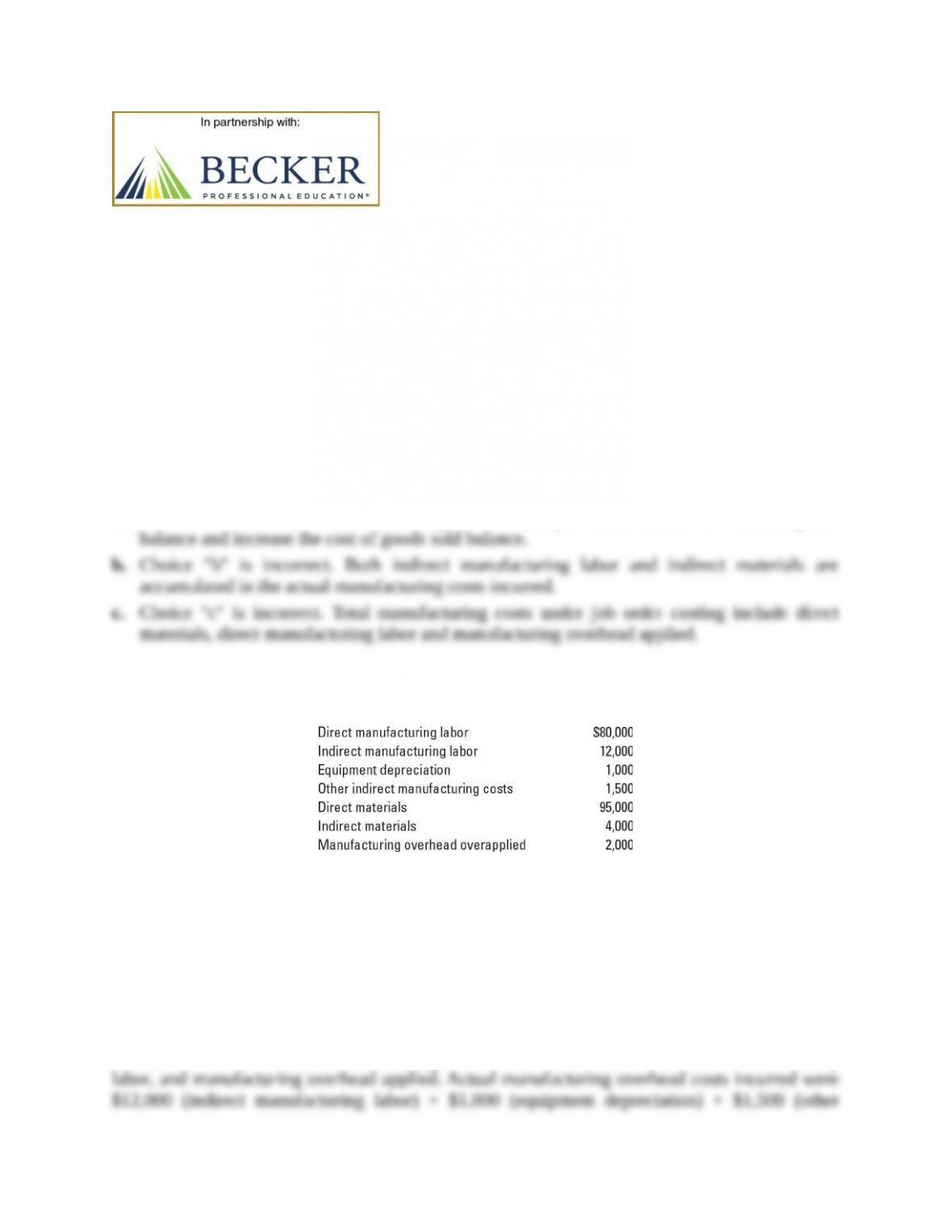

Choice “c” is correct. The actual manufacturing overhead costs incurred includes: $4,000

(indirect manufacturing labor) + $400 (utilities) + $500 (fire insurance) + $6,000 (indirect

materials) + $600 (depreciation on equipment) = $11,500. Because actual manufacturing

overhead costs of $11,500 exceed manufacturing overhead costs applied of $11,000,

manufacturing overhead is underallocated by $500.

4-20 Under Stanford Corporation’s job costing system, manufacturing overhead is applied to

work in process using a predetermined annual overhead rate. During November, Year 1,

Stanford’s transactions included the following:

Stanford had neither beginning nor ending work-in-process inventory. What was the cost of jobs

completed and transferred to finished goods in November 20X1?

Required:

1. $604,000 2. $644,000

3. $620,000 4. $660,000

SOLUTION

Choice “3” is correct.

The question asks about the cost of jobs completed in a particular month. Certain cost

information is provided. Some of this information may not be needed.

4-21 (10 min) Job costing, process costing.

In each of the following situations, determine whether job costing or process costing would

be more appropriate.

SOLUTION

(10 min) Job order costing, process costing.

a. Job costing l. Job costing

b. Process costing m. Process costing

c. Job costing n. Job costing

d. Process costing o. Job costing

e. Job costing p. Job costing

f. Job costing q. Job costing

g. Job costing r. Process costing

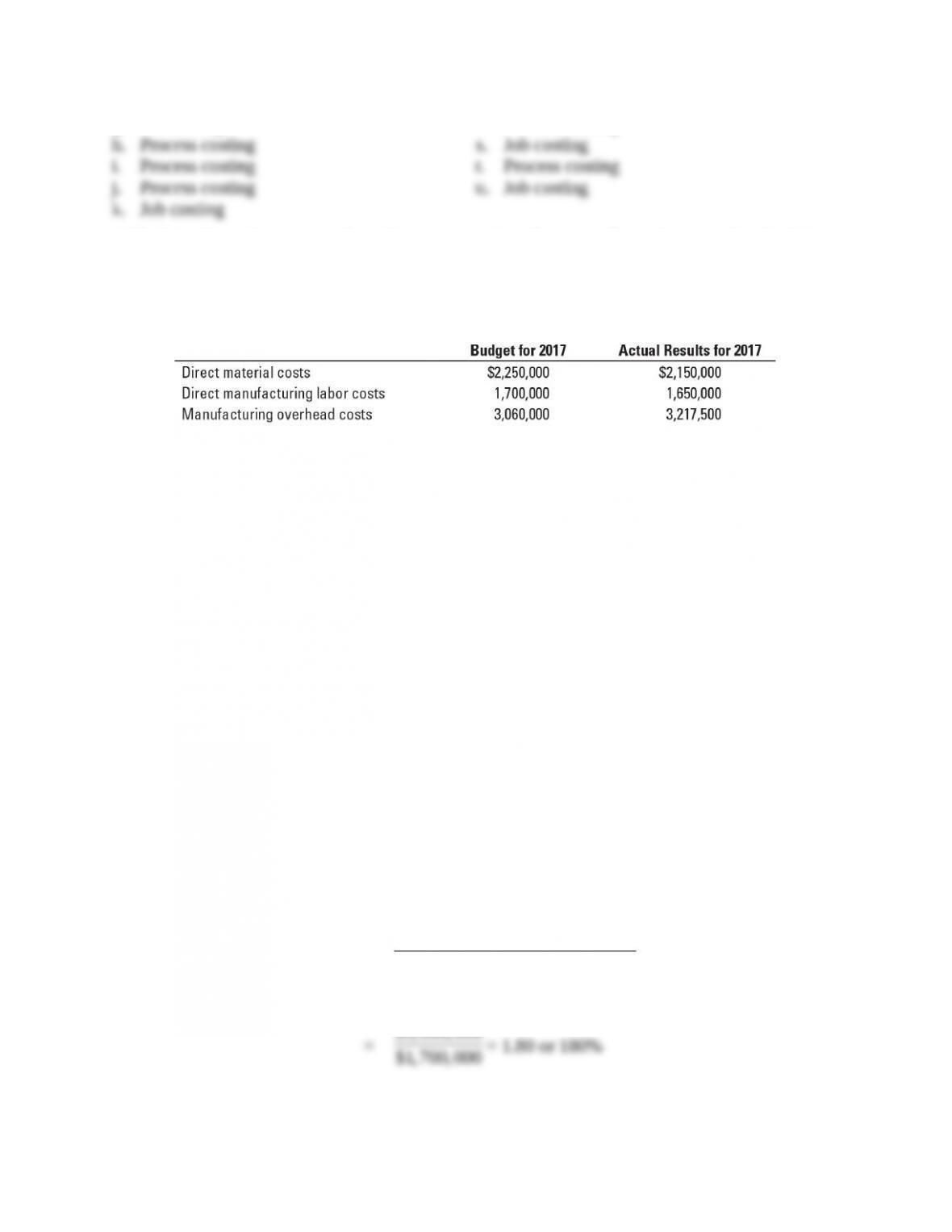

4-22 Actual costing, normal costing, accounting for manufacturing overhead. Dakota

Products uses a job-costing system with two direct-cost categories (direct materials and direct

manufacturing labor) and one manufacturing overhead cost pool. Dakota allocates manufacturing

overhead costs using direct manufacturing labor costs. Dakota provides the following

information:

Required:

1. Compute the actual and budgeted manufacturing overhead rates for 2017.

2. During March, the job-cost record for Job 626 contained the following information:

Direct materials used $55,000

Direct manufacturing labor costs $45,000

Compute the cost of Job 626 using (a) actual costing and (b) normal costing.

3. At the end of 2017, compute the under- or overallocated manufacturing overhead under

normal costing. Why is there no under- or overallocated manufacturing overhead under

actual costing?

4. Why might managers at Dakota Products prefer to use normal costing?

SOLUTION

(20 min.) Actual costing, normal costing, accounting for manufacturing overhead.

1.

Budgeted manufacturing

overhead rate

=

costslabor

ingmanufacturdirect Budgeted

costs overhead

ingmanufactur Budgeted

=

$3,060,000

$1,700,000

= 1.80 or 180%

rate overhead

ingmanufactur ctualA

=

costslabor

ingmanufacturdirect Actual

costs overhead

ingmanufactur Actual

=

$3, 217,500

$1,650,000

= 1.95 or 195%

2. Costs of Job 626 under actual and normal costing follow:

Actual Normal

Costing Costing

Direct materials $ 55,000 $ 55,000

Direct manufacturing labor costs 45,000 45,000

Manufacturing overhead costs

$45,000 1.95; $45,000 1.80 87,750 81,000

Total manufacturing costs of Job 626 $187,750 $181,000

3.

Total manufacturing overhead

allocated under normal costing

=

Actual direct manufacturing

labor costs

Budgeted

overhead rate

Underallocated manufacturing

overhead

=

Actual manufacturing

overhead costs

–

Manufacturing

overhead allocated

There is no under- or overallocated overhead under actual costing because overhead is

4. Managers at Dakota Products might prefer to use normal costing because it enables them

to use the budgeted manufacturing overhead rate determined at the beginning of the year to

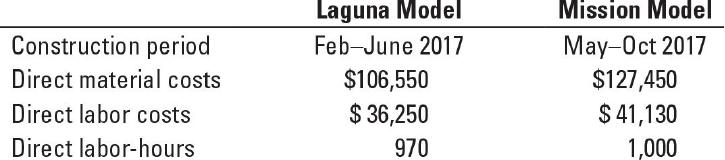

4-23 Job costing, normal and actual costing. Atkinson Construction assembles residential

houses. It uses a job-costing system with two direct-cost categories (direct materials and direct

labor) and one indirect-cost pool (assembly support). Direct labor-hours is the allocation base for

assembly support costs. In December 2016, Atkinson budgets 2017 assembly-support costs to be

$8,800,000 and 2017 direct labor-hours to be 220,000.

At the end of 2017, Atkinson is comparing the costs of several jobs that were started and

completed in 2017.

Direct materials and direct labor are paid for on a contract basis. The costs of each are known

when direct materials are used or when direct labor-hours are worked. The 2017 actual

assembly-support costs were $8,400,000, and the actual direct labor-hours were 200,000.

Required:

1. Compute the (a) budgeted indirect-cost rate and (b) actual indirect-cost rate. Why do they

differ?

2. What are the job costs of the Laguna Model and the Mission Model using (a) normal

costing and (b) actual costing?

3. Why might Atkinson Construction prefer normal costing over actual costing?