In relevant-cost analysis, managers should not consider all variable as relevant and all

fixed costs as irrelevant.

For short-run product-mix decisions, managers should focus on minimizing total fixed

costs.

Absorption costing is a method of inventory costing in which only variable

manufacturing costs are included as inventoriable costs.

Only variable production costs are used when calculating contribution margin.

The accounting procedures in a backflush-costing system strictly adhere to Generally

Accepted Accounting Principles (GAAP).

Scrap is residual material that results from manufacturing a product; it has low total

sales value compared with the total sales value of the product.

Contribution margin = Total revenues – Total manufacturing costs

ISO 9000 developed by the International Organization for Standardization is a set of

five international standards for quality management.

The revenue effect of growth is calculated by multiplying the difference in units sold

(current year minus the previous year) by selling price in the current year.

Adjusted allocation-rate approach restates all amounts in the general and subsidiary

ledgers by using actual rather than budgeted cost rates.

In a graphical display of a cost function, the steepness of a line represents the total

amount of fixed costs.

The net present value method accurately assumes that project cash flows can only be

reinvested at the company’s required rate of return.

In companies that produce masses of identical or similar units of output and

consequently use process-costing systems, it is relatively easy to set standards and use a

standard cost as the cost per equivalent unit.

Variances that are calculated frequently and in a timely manner can provide early

warnings to management so corrective action can be taken.

Normal costing is a method of job costing that allocates an indirect cost based on the

actual indirect-cost rate times the actual quantity of the cost-allocation base.

The income taxes saved as a result of depreciation deductions are irrelevant because

they decrease cash outflows.

The standard error of the estimated coefficient indicates how much the estimated value,

b, is likely to be affected by random factors.

When replacing an old machine with a new machine, the book value of the old machine

is a relevant cost.

When estimating a cost function, cost behavior can be approximated by a linear cost

function within the relevant range.

Depreciation results in income tax cash savings that are equal to the depreciation

expense multiplied by the company’s income tax rate.

The optimal safety-stock level is the quantity of safety stock that minimizes the sum of

annual relevant stockout and ordering costs.

In job-costing systems, abnormal spoilage costs are considered to be inventoriable costs

and normal spoilage costs are not considered to be inventoriable costs and are written

off as costs of the accounting period in which the abnormal spoilage is detected.

Reverse engineering can be used to analyze competitors’ products to determine product

designs and materials and to understand the technologies competitors use.

A budgeting process can facilitate learning in that feedback from budgets can lead to

changes in plans and strategies.

In using high-low method, the slope coefficient is calculated by dividing the difference

between highest and lowest observations of the cost driver by the difference between

costs associated with highest and lowest observations of the cost driver.

The step-down method allocates support department costs to only operating

departments in a sequential manner.

Variable costing is also called direct costing because it considers other

nonmanufacturing direct costs, such as direct marketing costs as inventoriable costs.

One of the risks of using only the variable cost as a base may tempt managers to cut

prices as long as prices are above variable cost.

The production volume variance arises only for variable overhead costs.

Idle time wages consists of the wages paid to all workers (for both direct labor and

indirect labor) in excess of their straight-time wage rates.

In markets with little or no competition, the key factor affecting price is the cost of

production to the company.

The dual cost-allocation method classifies costs into two pools, a budgeted cost pool

and an actual cost pool.

A step cost function is an example of a linear cost function.

Accounting methods for internal reporting purposes are specified by Generally

Accepted Accounting Principles (GAAP).

Equivalent units is a derived measure of output calculated by converting the quantity of

inputs into the amount of completed output that could be produced with that quantity of

input.

In the “make decisions by choosing among alternatives” stage of the capital budgeting

process, a company determines which investment yields the greatest benefit and the

least cost to the organization.

Activity-based management refers to the use of information derived from ABC analysis

to analyze and improve operations.

The rent paid for an already existing facility is an example of a sunk cost.

Firms often conduct multiple inspections to avoid instances of undetected spoiled units

at later stages of the process.

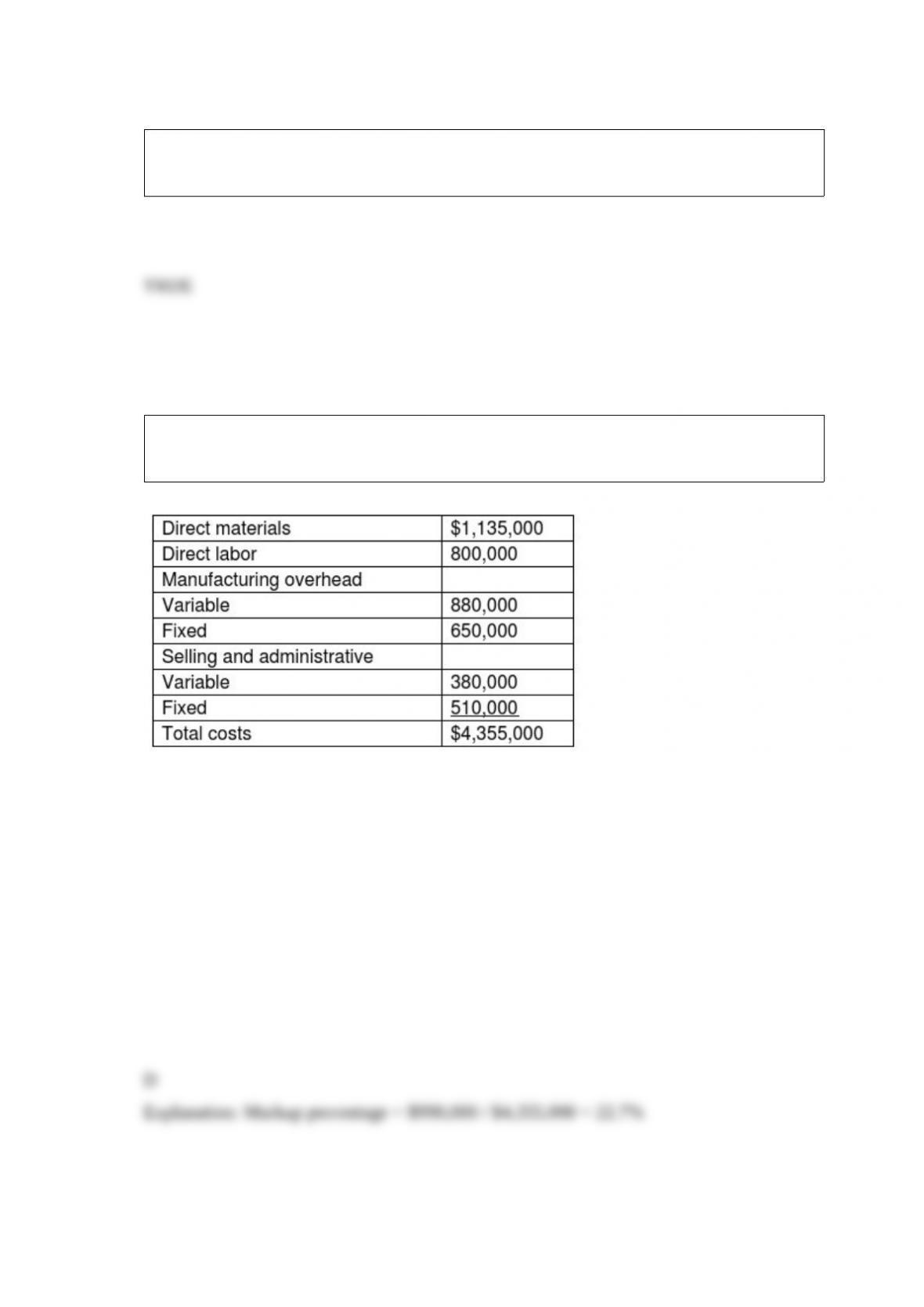

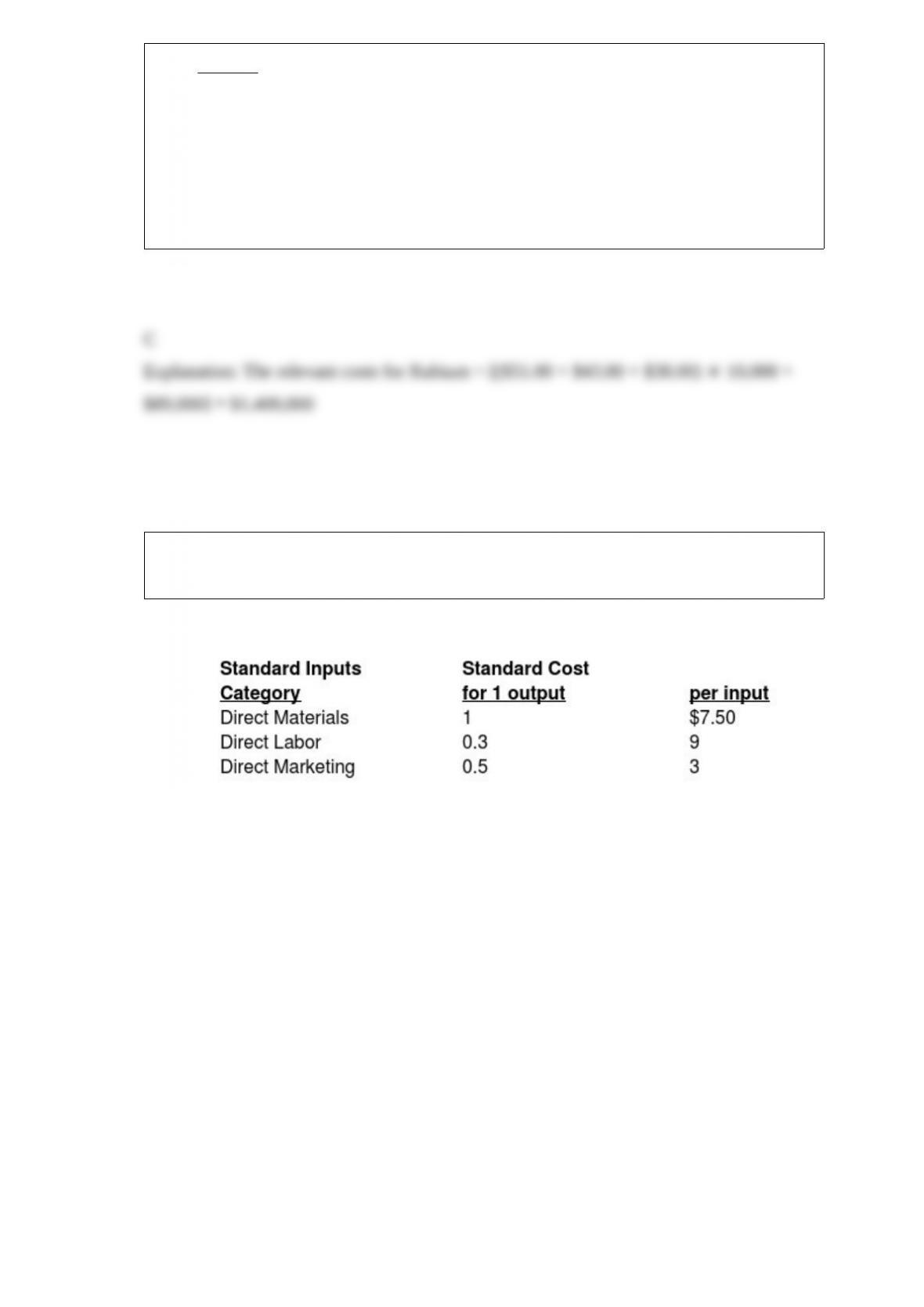

Wilde Corporation budgeted the following costs for the production of its one and only

product for the next fiscal year:

Wilde has an annual target operating income of $990,000.

The markup percentage for setting prices as a percentage of the full cost of the product is

________.

A) 31.9%

B) 36.3%

C) 45.8%

D) 22.7%

Many manufacturing, marketing, and design problems require employees with multiple

skills; therefore, teams are used and the members have the added encouragement of

________.

A) individual incentives

B) management incentives

C) morale incentives

D) team incentives

Put the following steps in order for using the high-low method of estimating a cost

function:

A = Identify the cost function

B = Calculate the constant

C = Calculate the slope coefficient

D = Identify the highest and lowest observed values

A) D C A B

B) C D A B

C) A D C B

D) D C B A

Buildz Corp has been servicing the Production Casting Department for five years.

Beginning next year, the company is adding a Production Molding Department to

compliment the materials produced by the Production Casting Department. As a result,

data center costs are expected to increase from $800,000 per year to $1,000,000 per

year. The Production Molding Department will use 20% of the data center efforts.

Required:

a. Using the stand-alone cost-allocation method, identify the amount of data center cost

that will be allocated to Production Casting and the Production Molding Department

next year.

b. Using the incremental cost-allocation method, identify the amount of data center cost

that will be allocated to Production Casting and the Production Molding Department

next year.

If the sales mix shifts to one unit of Product X and two units of Product Y, then the

breakeven point will ________.

A) increase

B) stay the same

C) decrease

D) will be greater than the original breakeven point

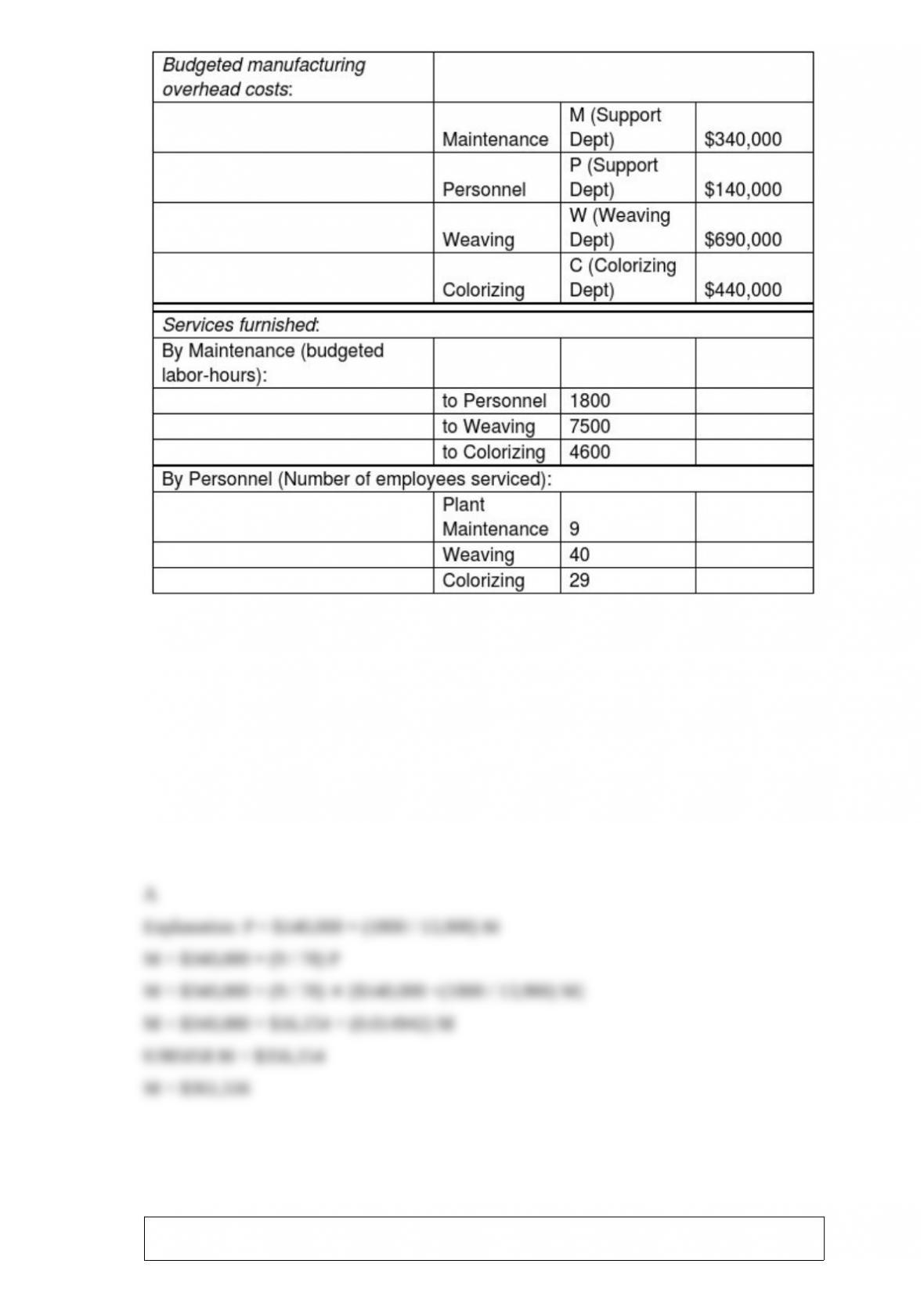

Hugo, owner of Automated Fabric, Inc., is interested in using the reciprocal allocation

method. The following data from operations were collected for analysis:

What is the complete reciprocated cost of the Maintenance Department? (Do not round any

intermediary calculations.)

A) $361,556

B) $356,154

C) $340,000

D) $0

Which purpose of cost allocation is used to encourage sales representatives to push

high-margin products or services?

A) to provide information for economic decisions

B) to motivate managers and other employees

C) to justify costs or compute reimbursement

D) to measure income and assets for reporting to external parties

An unfavorable flexible-budget variance for variable costs may be the result of

________.

A) using more input quantities than were budgeted

B) paying lower prices for inputs than were budgeted

C) selling output at a higher selling price than budgeted

D) selling less quantity compared to the budgeted

Which of the following statements is true of accrual accounting rate of return (AARR)

method and internal rate of return (IRR) method?

A) AARR method calculates the return in absolute terms, whereas IRR method

calculates the result in terms of percentage.

B) The AARR method calculates the return using operating-income numbers after

considering accruals and taxes, whereas the IRR method calculates the return using

after-tax cash flows and the time value of money.

C) The AARR method calculates the return considering the time value of money,

whereas the IRR method calculates the return ignoring the time value of money.

D) The AARR method considers cash flows, whereas the IRR method considers

operating income.

The coefficient of determination is important in explaining variances in estimating

equations. For a certain estimating equation, the unexplained variation was given as

22,000. The total variation was given as 55,000. What is the coefficient of

determination for the equation?

A) 2.50

B) 0.40

C) 0.60

D) 1.40

Which of the following terms is defined as the time required to get equipment, tools,

and materials ready to start production?

A) setup time

B) delivery time

C) manufacturing-cycle time

D) product design time

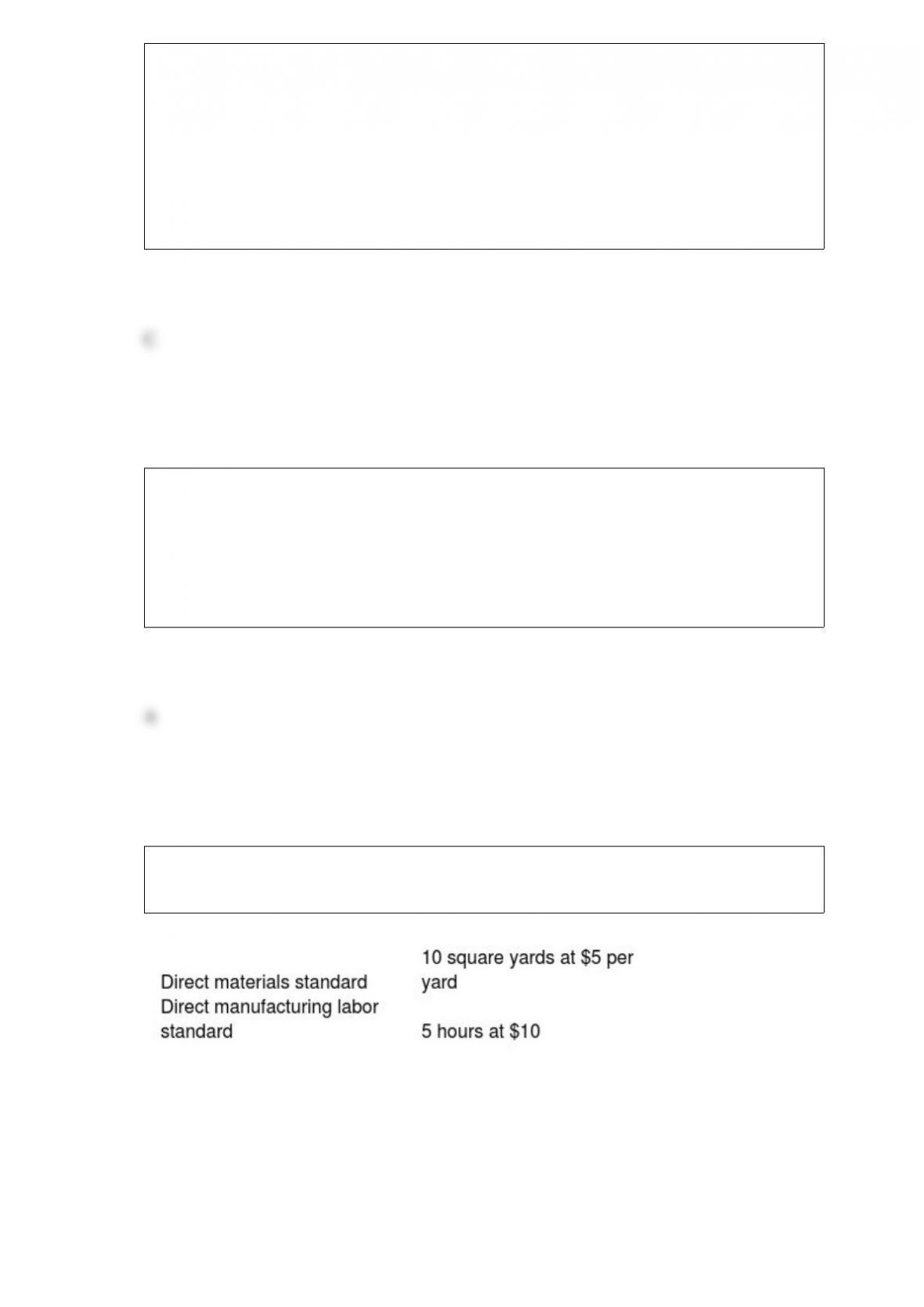

Nancy’s Draperies manufactures curtains. A certain window curtain requires the

following:

During the second quarter, the company made 1,500 curtains and used 14,000 square yards

of fabric costing $72,000. Direct labor totaled 7,600 hours for $83,600.

Required:

a. Compute the direct materials price and efficiency variances for the quarter.

b. Compute the direct manufacturing labor price and efficiency variances for the quarter.

Assume a manufacturing company that has started production in the current year.

Which of the following would result in the highest profit being reported if the company

has 1,000 units of ending inventory?

A) throughput costing

B) variable costing

C) absorption costing

D) standard costing

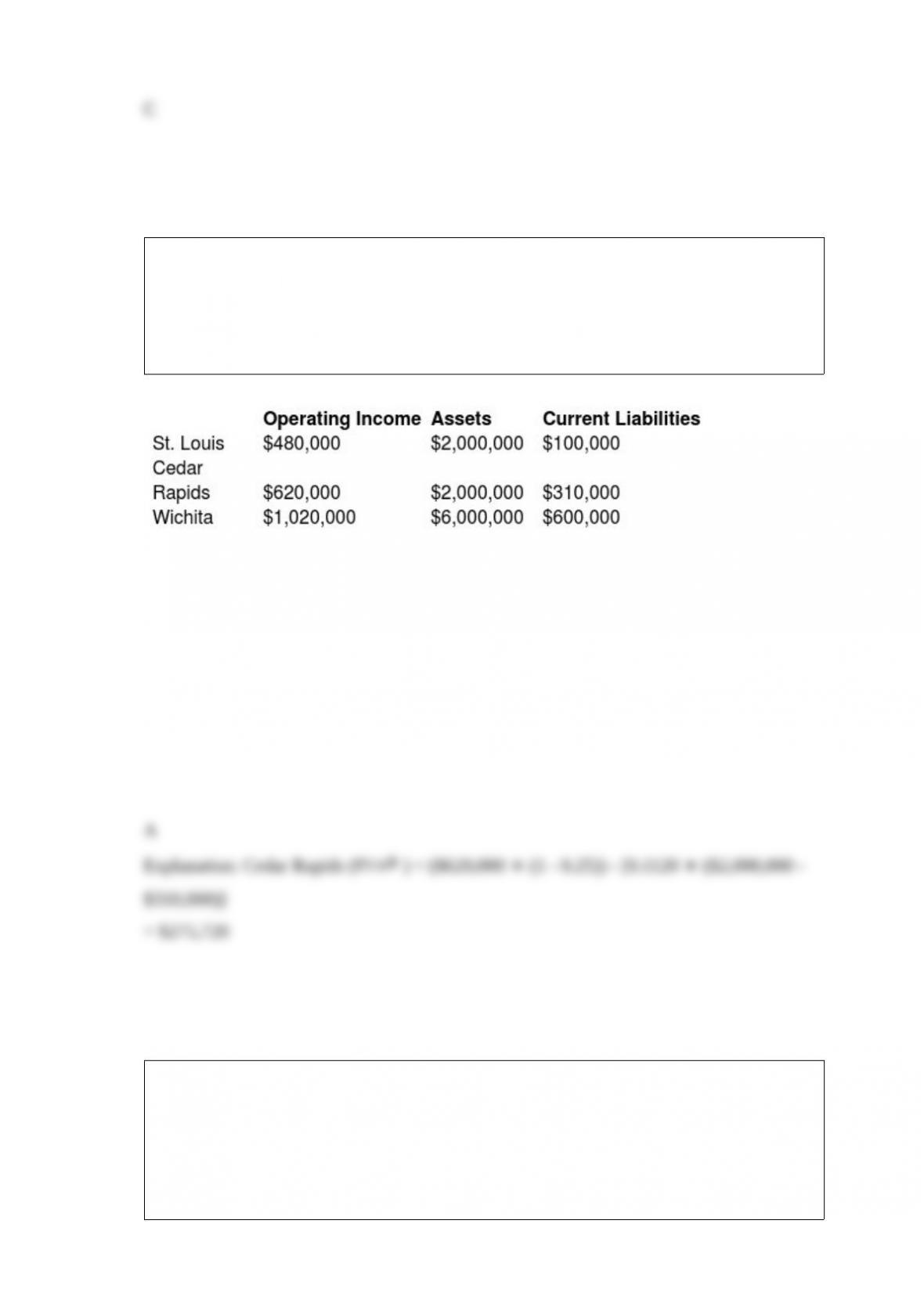

Waldorf Company has two sources of funds: long-term debt with a market and book

value of $5,200,000 issued at an interest rate of 13%, and equity capital that has a

market value of $4,200,000 (book value of $2,400,000). Waldorf Company has profit

centers in the following locations with the following operating incomes, total assets,

and current liabilities. The cost of equity capital is 13%, while the tax rate is 25%.

What is the EVA for Cedar Rapids? (Round intermediary calculations to four decimal

places.)

A) $275,720

B) $465,000

C) $430,720

D) $241,000

More insight into the sales-volume variance can be gained by subdividing it into

________.

A) the sales-mix variance and the sales-quantity variance

B) the market-share variance and the sales-mix variance

C) the flexible-budget variance and the market-size variance

D) the flexible-budget variance and the sales-mix variance

________ is an example of an output unit-level cost in the cost hierarchy.

A) Factory rent expense

B) Building security costs

C) Top management compensation costs

D) Machine depreciation

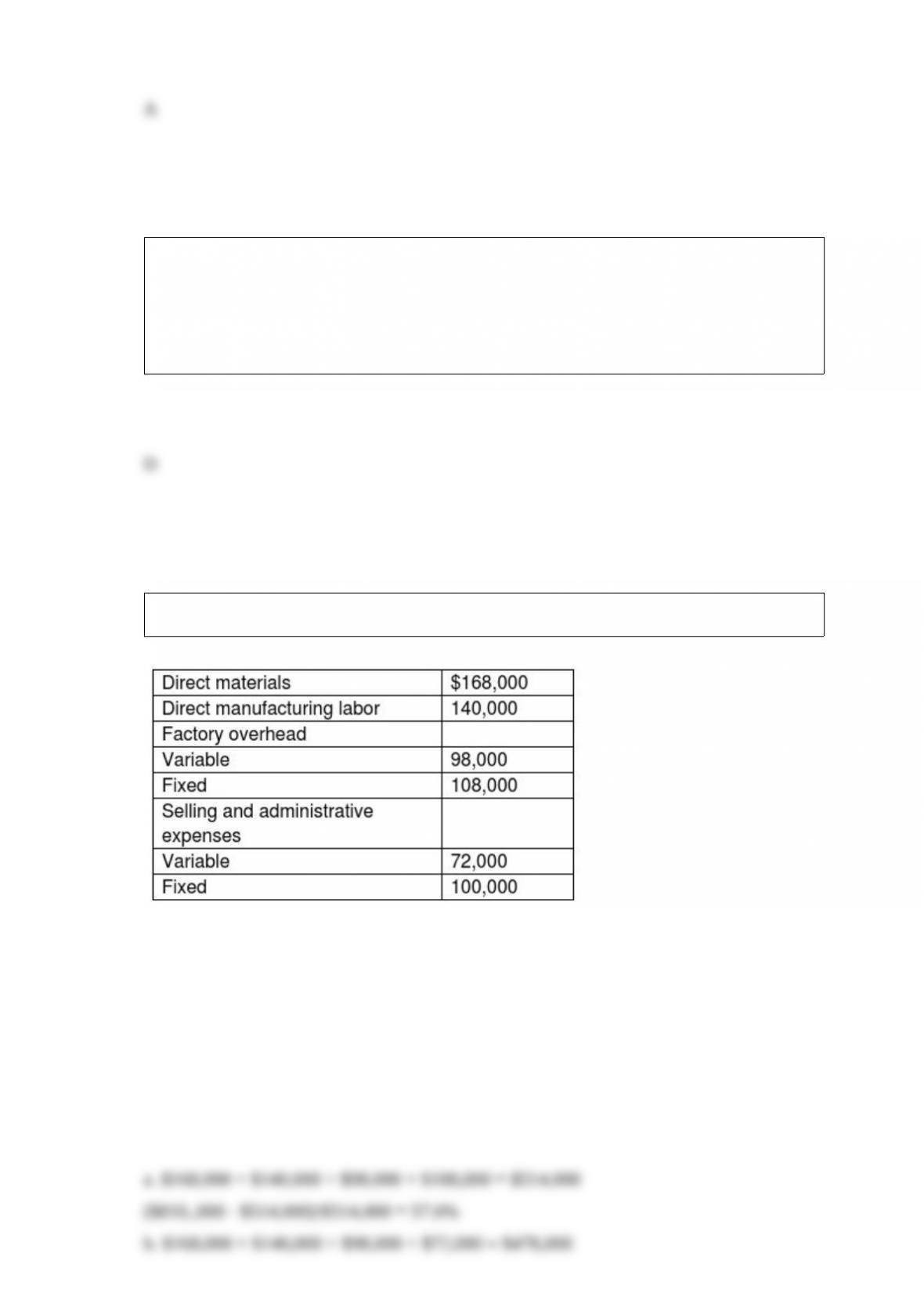

Jackson Company has budgeted sales of $810,000 with the following budgeted costs:

Compute the average markup percentage for setting prices as a percentage of:

a. Total manufacturing costs

b. The variable cost of the product

c. The full cost of the product

d. Variable manufacturing costs

Cost assignment ________.

A) includes future and arbitrary costs

B) associates accumulated costs with certain cost objects

C) is the same as cost accumulation

D) is the difference between budgeted and actual costs

Which of the following differentiates cost accounting and financial accounting?

A) The primary users of cost accounting are the investors, whereas the primary users of

financial accounting are the managers.

B) Cost accounting deals with product design, production, and marketing strategies,

whereas financial accounting deals mainly with pricing of the products.

C) Cost accounting measures only the financial information related to the costs of

acquiring fixed assets in an organization, whereas financial accounting measures

financial and nonfinancial information of a company’s business transactions.

D) Cost accounting measures information related to the costs of acquiring or using

resources in an organization, whereas financial accounting measures a financial position

of a company to investors, banks, and external parties.

Which of the following statements is true of process costing?

A) In the period of rising prices, weighted-average process-costing method will result in

higher operating income as compared to FIFO process-costing method.

B) The operating income and the income tax liability of a company are not affected by

the method of process-costing being followed by the company.

C) In the period of rising prices, weighted-average process-costing method will result in

lower cost of goods sold as compared to FIFO process-costing method.

D) In a period of falling prices, weighted-average process-costing method will result in

a higher income tax liability as compared to FIFO process-costing method.

Process costing is ________.

A) used to enhance employees’ job satisfaction

B) used by businesses to price unique products or identical products produced in

batches

C) used by businesses to price identical products

D) used by businesses when manufacturing goods above normal capacity

Top management at Gifford manufacturing are planning capacity levels and how to

assign capacity costs for an upcoming period. Which of the following factors should be

considered while developing this plan so that proper control can be achieved?

A) The IRS tax implications of such decisions

B) The level of uncertainty of expected costs and demand

C) The GAAP rules requiring absorption costing

D) The requirements of SFAS 151

________ is an example of a total factor productivity measure.

A) The number of units produced per month

B) The number of units produced per machine hour

C) The number of units produced per labor hour

D) The number of units produced per dollar of input cost

Bouchard Company manufactures a product that currently has a full cost of $700. Its

target operating income per unit is $80 and management’s budgets assume that same

target operating income per unit for the foreseeable future. To stay competitive,

Bouchard management believes it must cut its price by 25%. What will be its new target

cost?

A) $700

B) $505.00

C) $585.00

D) $80

For merchandising companies, inventoriable costs include ________.

A) selling expenses

B) shipping (incoming) costs to acquire merchandise

C) distribution costs

D) outgoing freight and handling costs

________ categorizes costs related to customers into different cost pools on the basis of

either different classes of cost drivers or different degrees of difficulty in determining

the cause-and-effect (or benefits-received) relationships.

A) Customer-profitability analysis

B) Customer revenues

C) Customer cost hierarchy

D) Price discounting

Assume the sales mix consists of three units of Product A and one unit of Product B. If

the sales mix shifts to four units of Product A and one unit of Product B, then the

weighted-average contribution margin will ________.

A) increase per unit

B) stay the same

C) decrease per unit

D) cannot be determined from this information

Hartley’s Meat Pies is considering replacing its existing delivery van with a new one.

The new van can offer considerable savings in operating costs. Information about the

existing van and the new van follow:

Existing van New van

Original cost $59,000 $91,000

Annual operating cost $19,500 $11,000

Accumulated depreciation $33,000 —

Current salvage value of the existing van $26,500 —

Remaining life 9 years 9 years

Salvage value in 9 years $ 0 $ 0

Annual depreciation $2,889 $10,111

Sunk costs include ________.

A) the accumulated depreciation of the existing van

B) the original cost of the new van

C) the current salvage value of the existing van

D) the annual operating cost of the new van

The budgeted contribution margin per composite unit for the budgeted sales mix can be

computed by dividing the ________.

A) total budgeted contribution margin by the actual total units

B) total budgeted contribution margin by the total budgeted units

C) actual total contribution margin by the total actual total units

D) actual total contribution margin by the total budgeted units

Which of the following formulas determine cost of goods sold in a manufacturing

entity?

A) Beginning work-in-process inventory + Cost of goods manufactured – Ending

work-in-process inventory = Cost of goods sold

B) Beginning work-in-process inventory + Cost of goods manufactured + Ending

work-in-process inventory = Cost of goods sold

C) Cost of goods manufactured – Beginning finished goods inventory – Ending finished

goods inventory = Cost of goods sold

D) Cost of goods manufactured + Beginning finished goods inventory – Ending finished

goods inventory = Cost of goods sold

Rubium Micro Devices currently manufactures a subassembly for its main product. The

costs per unit are as follows:

Direct materials $51.00

Direct labor 43.00

Variable overhead 38.00

Fixed overhead 33.00

Total $165.00

Crayola Technologies Inc. has contacted Rubium with an offer to sell 10,000 of the

subassemblies for $138.00 each. Rubium will eliminate $89,000 of fixed overhead if it

accepts the proposal. What are the relevant costs for Rubium?

A) $929,000

B) $1,029,000

C) $1,409,000

D) $1,739,000

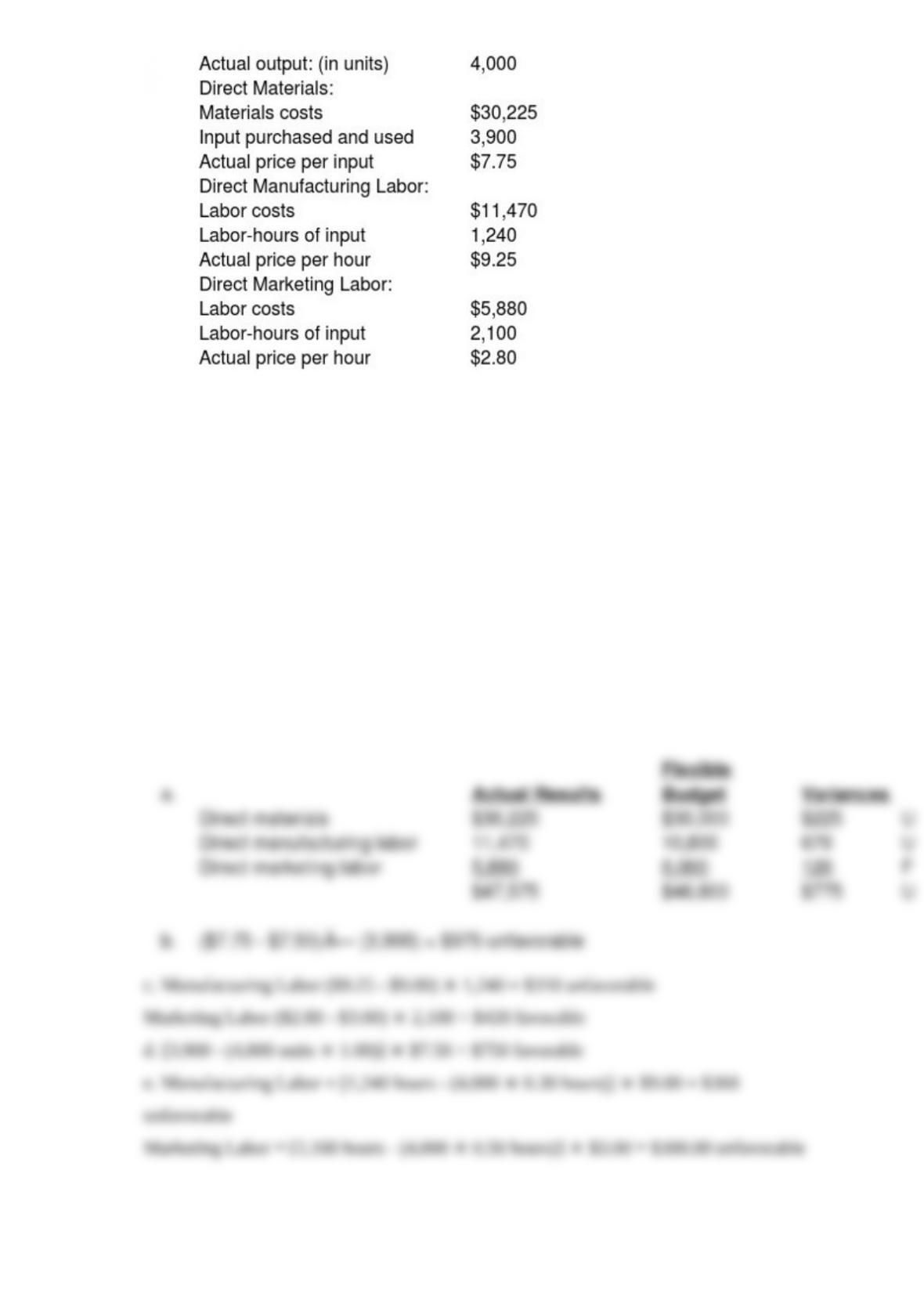

Littrell Company produces chairs and has determined the following direct cost

categories and budgeted amounts:

Actual performance for the company is shown below:

Required:

a. What is the combined total of the flexible-budget variances?

b. What is the price variance of the direct materials?

c. What is the price variance of the direct manufacturing labor and the direct marketing

labor, respectively?

d. What is the efficiency variance for direct materials?

e. What are the efficiency variances for direct manufacturing labor and direct marketing

labor, respectively?

Which of the following statements is true of discretionary costs?

A) They arise from day-to-day operational decisions.

B) They include conversion cost, direct material costs.

C) They have measurable cause-and-effect relationship between output and resources

used.

D) They have high level of uncertainty.

Which of the following statements is true of normal spoilage and abnormal spoilage?

A) Normal spoilage is inherent in a particular production process, whereas abnormal

spoilage is not inherent in a particular production process.

B) Abnormal spoilage arises even when the process is carried out in an efficient

manner, whereas normal spoilage does not arise when the process is carried out in an

efficient manner.

C) Normal spoilage is usually regarded as avoidable and controllable, whereas

abnormal spoilage is unavoidable and uncontrollable.

D) The costs of normal spoilage are recorded as a loss as a separate line item in an

income statement, whereas costs of abnormal spoilage are included as a component of

the costs of good units manufactured.

Tony Manufacturing produces a single product that sells for $80. Variable costs per unit

equal $50. The company expects total fixed costs to be $82,000 for the next month at

the projected sales level of 2,800 units. In an attempt to improve performance,

management is considering a number of alternative actions. Each situation is to be

evaluated separately. Suppose that management believes that a 14% reduction in the

selling price will result in a 14% increase in sales. If this proposed reduction in selling

price is implemented ________.

A) operating income will decrease by $23,990

B) operating income will increase by $7,370

C) operating income will decrease by $31,360

D) operating income will increase by $23,990

Explain the procedure how overhead indirect costs become a part of work-in process

inventory.

Explain what is meant by sensitivity analysis in budgeting, and discuss how managers

might use sensitivity analysis in practice.

Van Meter Fig Company has substantial fluctuations in its production costs because of

the seasonality of figs.

Would you recommend an actual or budgeted allocation base? Why? Would you

recommend calculating monthly, seasonal, or annual allocation rates? Why?

What are the three types of manufacturing cost?

Harriet has been reviewing the accounting system for her company and she is very

concerned about the accounting for spoilage. It appears that spoilage is accounted for

only at the end of the processing cycle. While this concept is acceptable in general,

Harriet believes that a better method can be found to properly account for the spoilage

when it occurs. She believes that there must be something better than the

weighted-average method of accounting for spoilage. She would like the company to

use a method that provides closer tracking of the spoilage with the accounting for the

spoilage.

Required:

Discuss the problems Harriet is having with the accounting system.

Neon Company manufactured 2,500 units during April with a total overhead budget of

$55,000. However, while manufacturing the 2,500 units the microcomputer that

contained the month’s cost information broke down. With the computer out of

commission, the accountant has been unable to complete the variance analysis report.

The information missing from the report is lettered in the following set of data:

Variable overhead:

Standard cost per unit: 1.2 labor hour at $10 per hour

Actual costs: $26,250 for 2,250 hours

Flexible budget: a

Total flexible-budget variance: b

Variable overhead spending variance: c

Variable overhead efficiency variance: d

Fixed overhead:

Budgeted costs: e

Actual costs: f

Flexible-budget variance: $200 favorable

Required:

Compute the missing elements in the report represented by the lettered items.

A company is considering buying a product at $15 per unit, the in-house manufacturing

of the same product is $17. The fixed cost per unit is $3 is included in the $17 in-house

product manufacturing cost. What should the company do in this scenario?

Why is decentralization costly?

What are five features of a just-in-time manufacturing system?

How does cost-based transfer price method help managers to determine transfer prices?

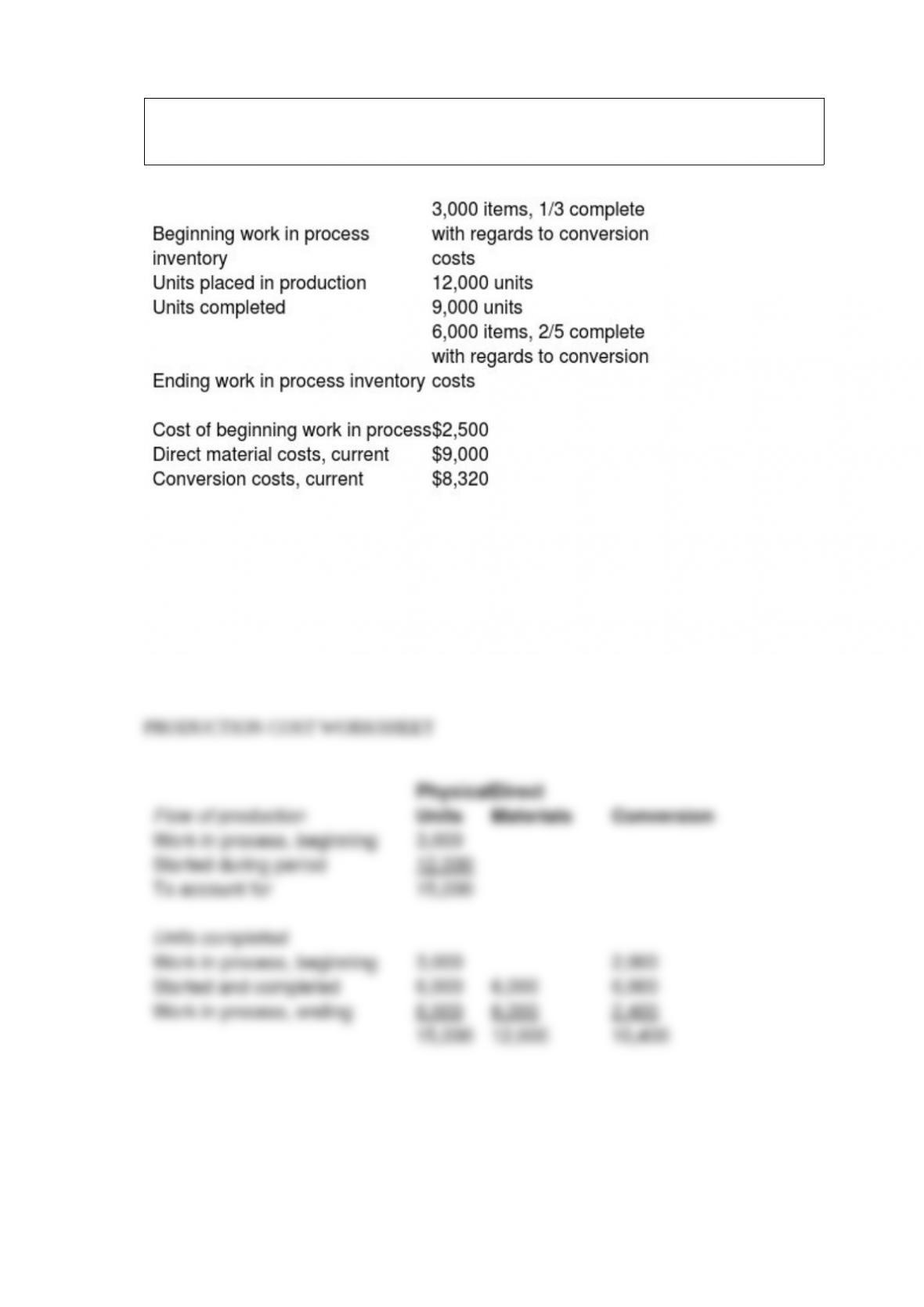

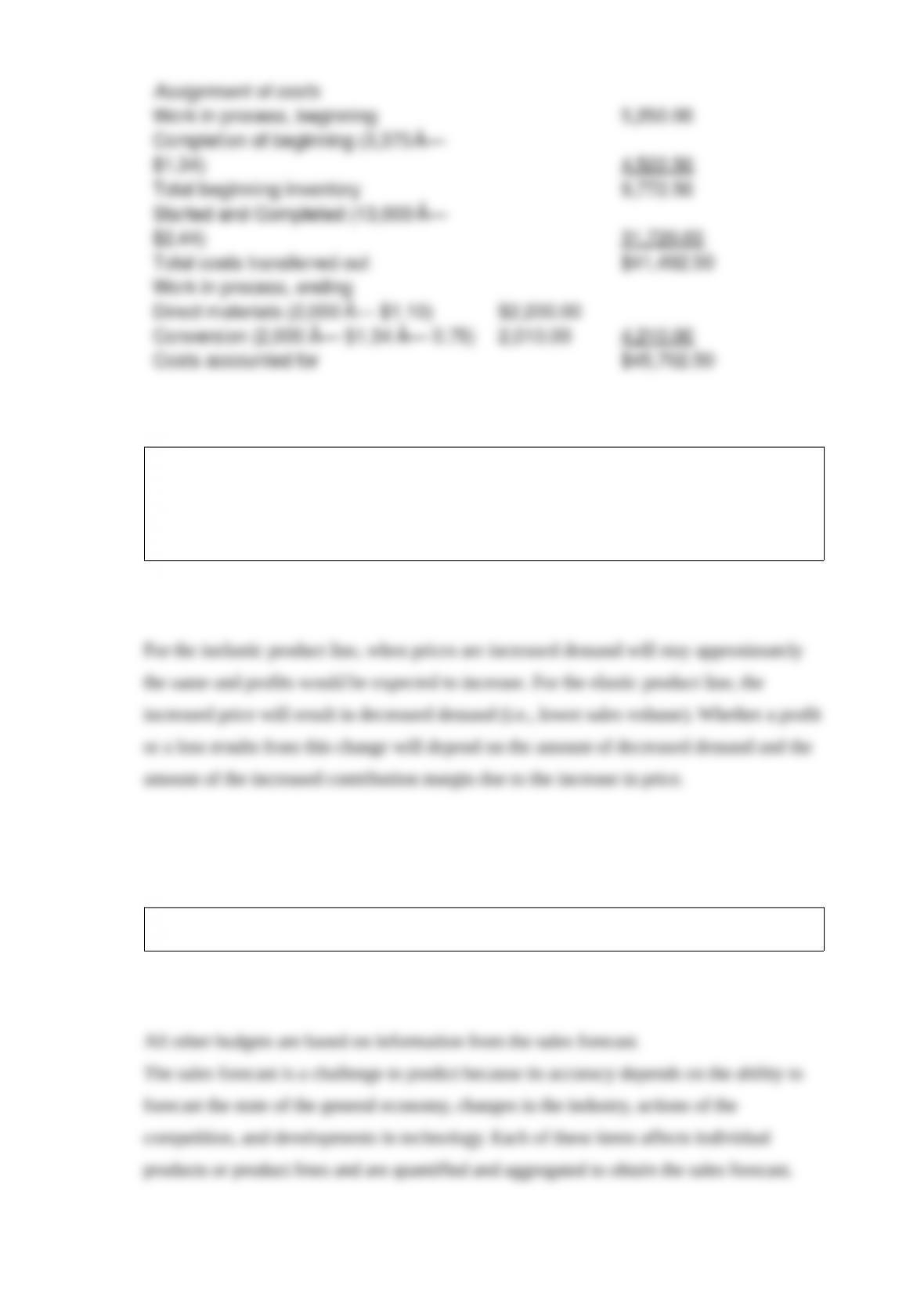

Shining Star Company uses an automated process to clean and polish its souvenir items.

For March, the company had the following activities:

Direct materials are placed into production at the beginning of the process and conversion

costs are incurred evenly throughout the process.

Required:

Prepare a production cost worksheet using the FIFO method.

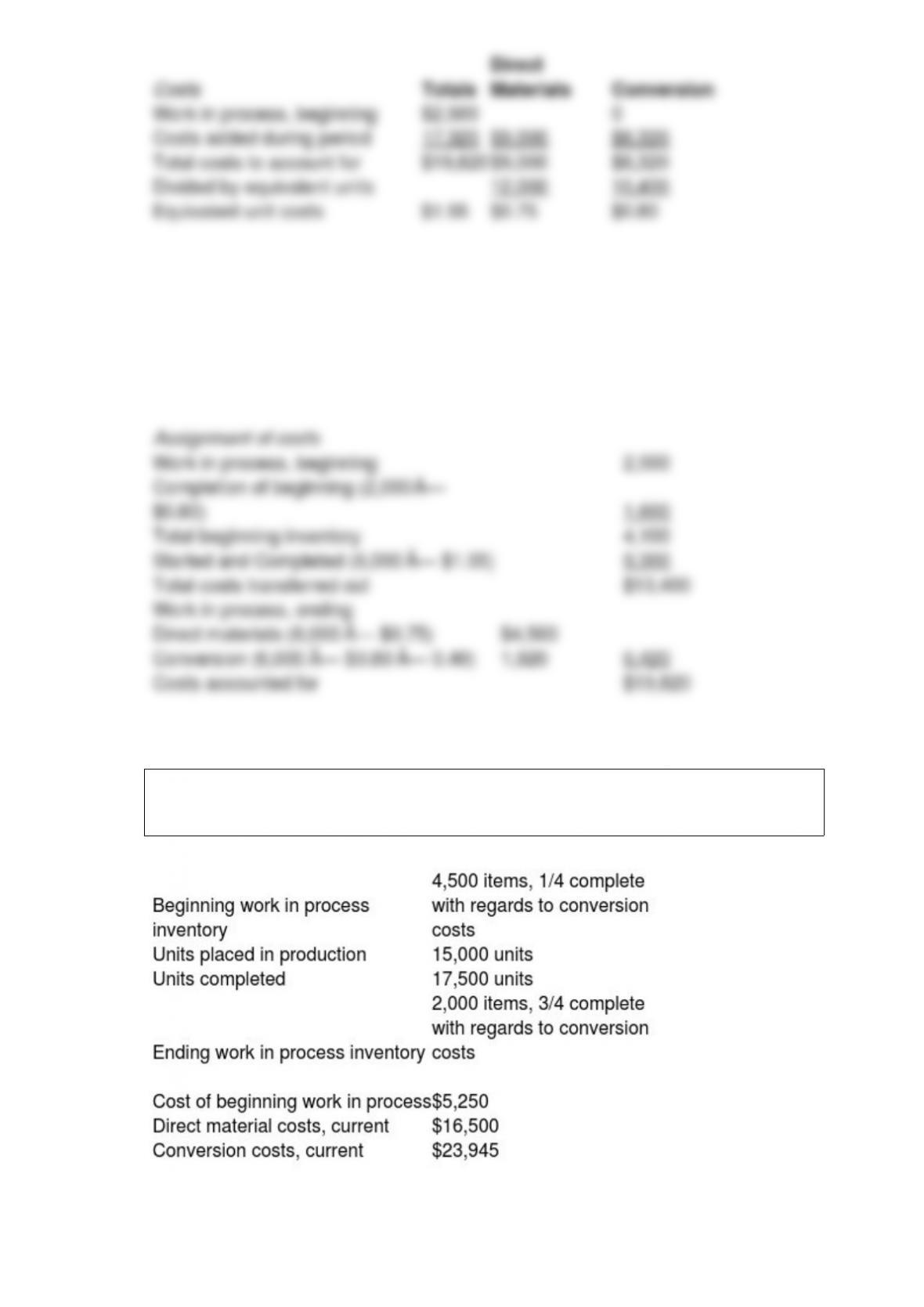

Pet Products Company uses an automated process to manufacture its pet replica

products. For June, the company had the following activities:

Direct materials are placed into production at the beginning of the process and conversion

costs are incurred evenly throughout the process.

Required:

Prepare a production cost worksheet using the FIFO method.

Clark Manufacturing offers two product lines, IN2 and EL5. The demand of the IN2

product line is inelastic, while the demand of the EL5 product line is very elastic. If

Clark initiates a price increase for both product lines, how will customer demand

change? How will the price increase affect operating profits?

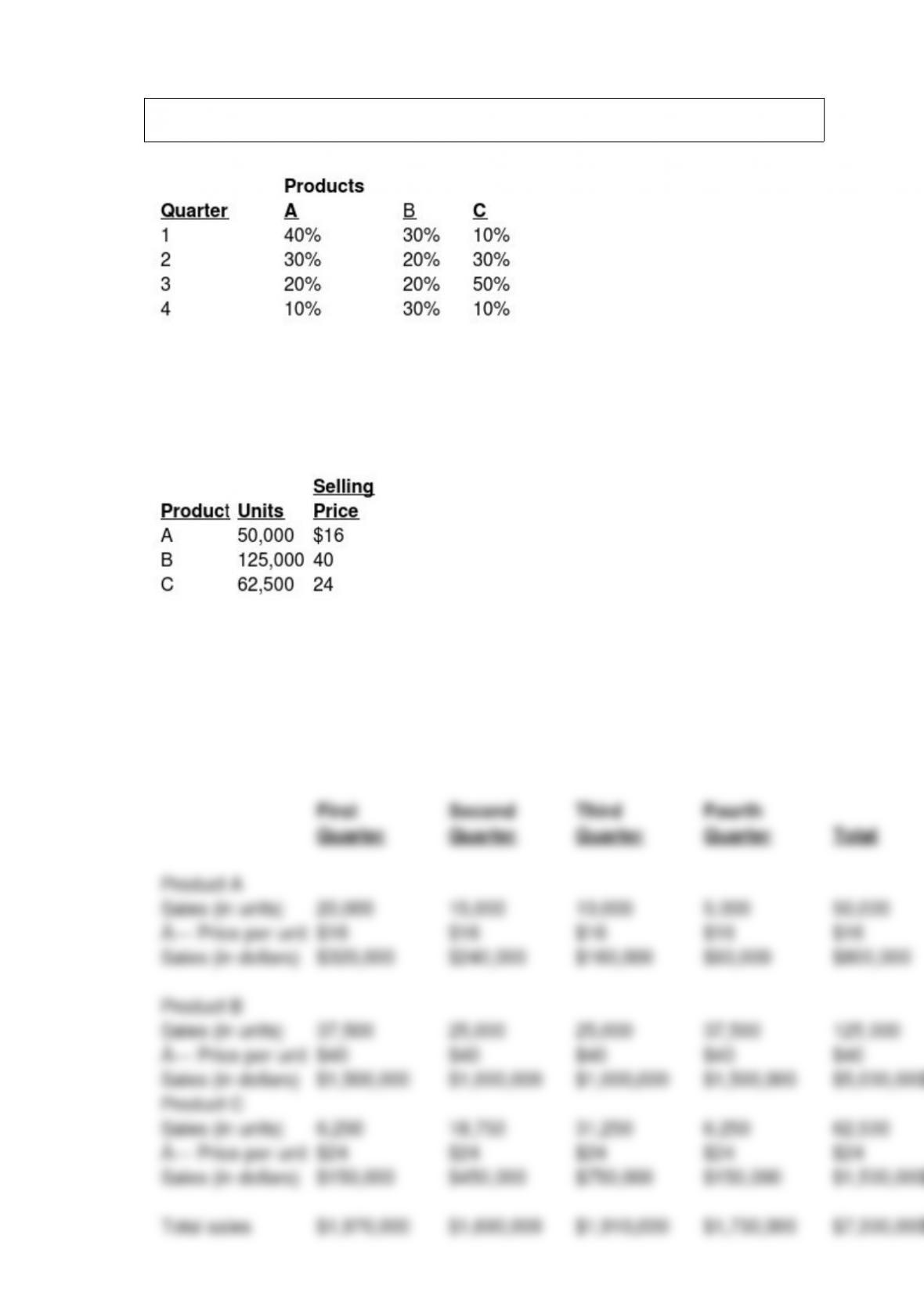

Discuss the importance of the sales forecast and items that influence its accuracy.

Prescher Company sells three products with the following seasonal sales pattern:

The annual sales budget shows forecasts for the different products and their expected

selling price per unit to be as follows:

Required:

Prepare a sales budget, in units and dollars, by quarters for the company for the coming

year.