SOLUTION

(30 min.) Revenues and production budget.

1.

Selling

Price

Units

Sold

Total

Revenues

12-ounce bottles $0.30 6,000,000a$1,800,000

2. Budgeted unit sales (12-ounce bottles) 6,000,000

Add target ending finished goods inventory 660,000

Deduct beginning finished goods inventory 980,000

3.

Beginning Budgeted Target Budgeted

= +

inventory sales ending inventory production

–

6-27 Budgeting; direct material usage, manufacturing cost, and gross margin. Xander

Manufacturing Company manufactures blue rugs, using wool and dye as direct materials. One

rug is budgeted to use 36 skeins of wool at a cost of $2 per skein and 0.8 gallons of dye at a cost

of $6 per gallon. All other materials are indirect. At the beginning of the year Xander has an

inventory of 458,000 skeins of wool at a cost of $961,800 and 4,000 gallons of dye at a cost of

$23,680. Target ending inventory of wool and dye is zero. Xander uses the FIFO inventory

cost-flow method.

Xander blue rugs are very popular and demand is high, but because of capacity constraints

the firm will produce only 200,000 blue rugs per year. The budgeted selling price is $2,000 each.

There are no rugs in beginning inventory. Target ending inventory of rugs is also zero.

Xander makes rugs by hand, but uses a machine to dye the wool. Thus, overhead costs are

accumulated in two cost pools—one for weaving and the other for dyeing. Weaving overhead is

allocated to products based on direct manufacturing labor-hours (DMLH). Dyeing overhead is

allocated to products based on machine-hours (MH).

There is no direct manufacturing labor cost for dyeing. Xander budgets 62 direct

manufacturing labor-hours to weave a rug at a budgeted rate of $13 per hour. It budgets 0.2

machine-hours to dye each skein in the dyeing process.

6-1

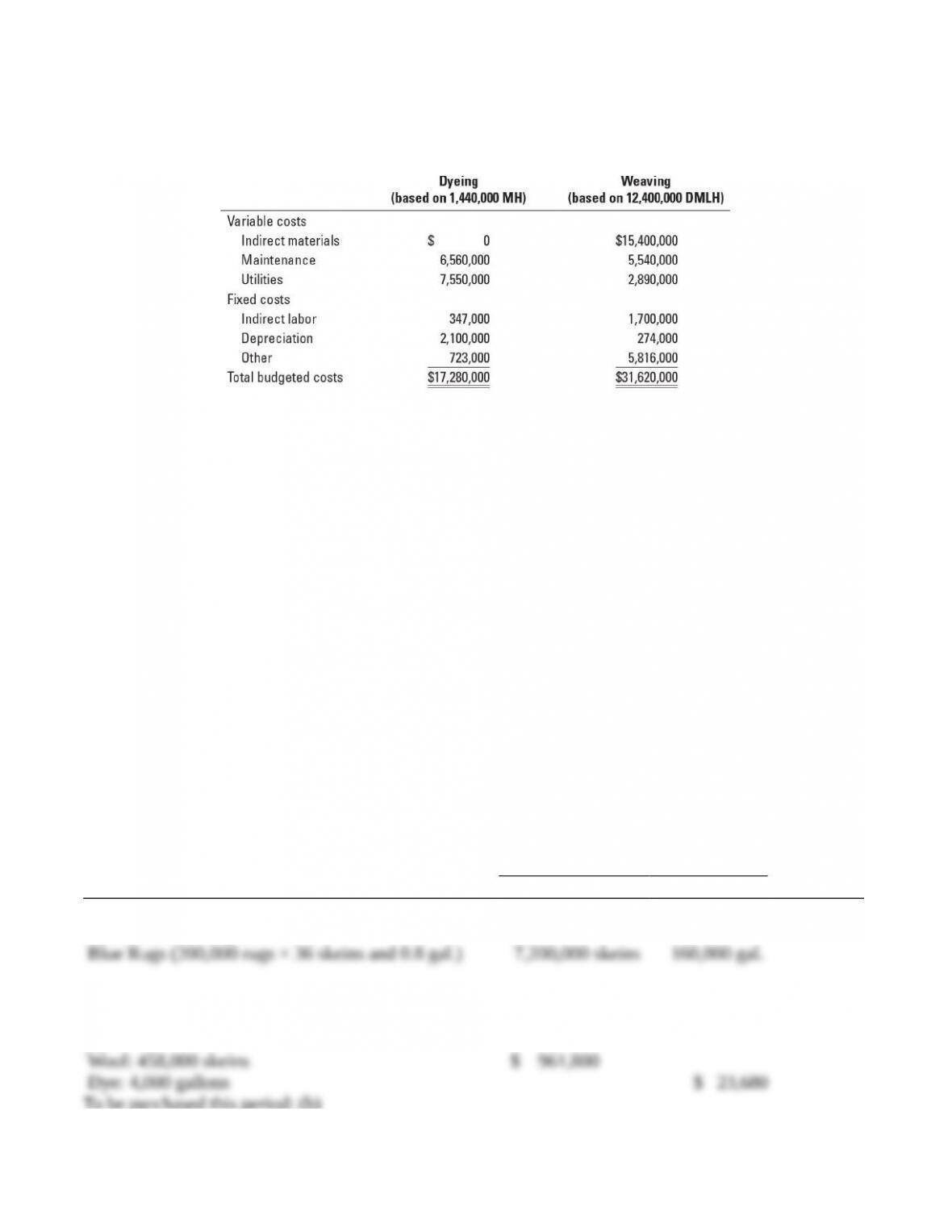

The following table presents the budgeted overhead costs for the dyeing and weaving cost

pools:

Required:

1. Prepare a direct materials usage budget in both units and dollars.

2. Calculate the budgeted overhead allocation rates for weaving and dyeing.

3. Calculate the budgeted unit cost of a blue rug for the year.

4. Prepare a revenues budget for blue rugs for the year, assuming Xander sells (a) 200,000 or

(b) 185,000 blue rugs (that is, at two different sales levels).

5. Calculate the budgeted cost of goods sold for blue rugs under each sales assumption.

6. Find the budgeted gross margin for blue rugs under each sales assumption.

7. What actions might you take as a manager to improve profitability if sales drop to 185,000

blue rugs?

8. How might top management at Xander use the budget developed in requirements 1–6 to

better manage the company?

SOLUTION

(30 min.) Budgeting: direct material usage, manufacturing cost, and gross margin.

1.

Direct Material Usage Budget in Quantity and Dollars

Material

Wool Dye Total

Physical Units Budget

Direct materials required for

Cost Budget

Available from beginning direct materials inventory:

(a)

To be purchased this period: (b)

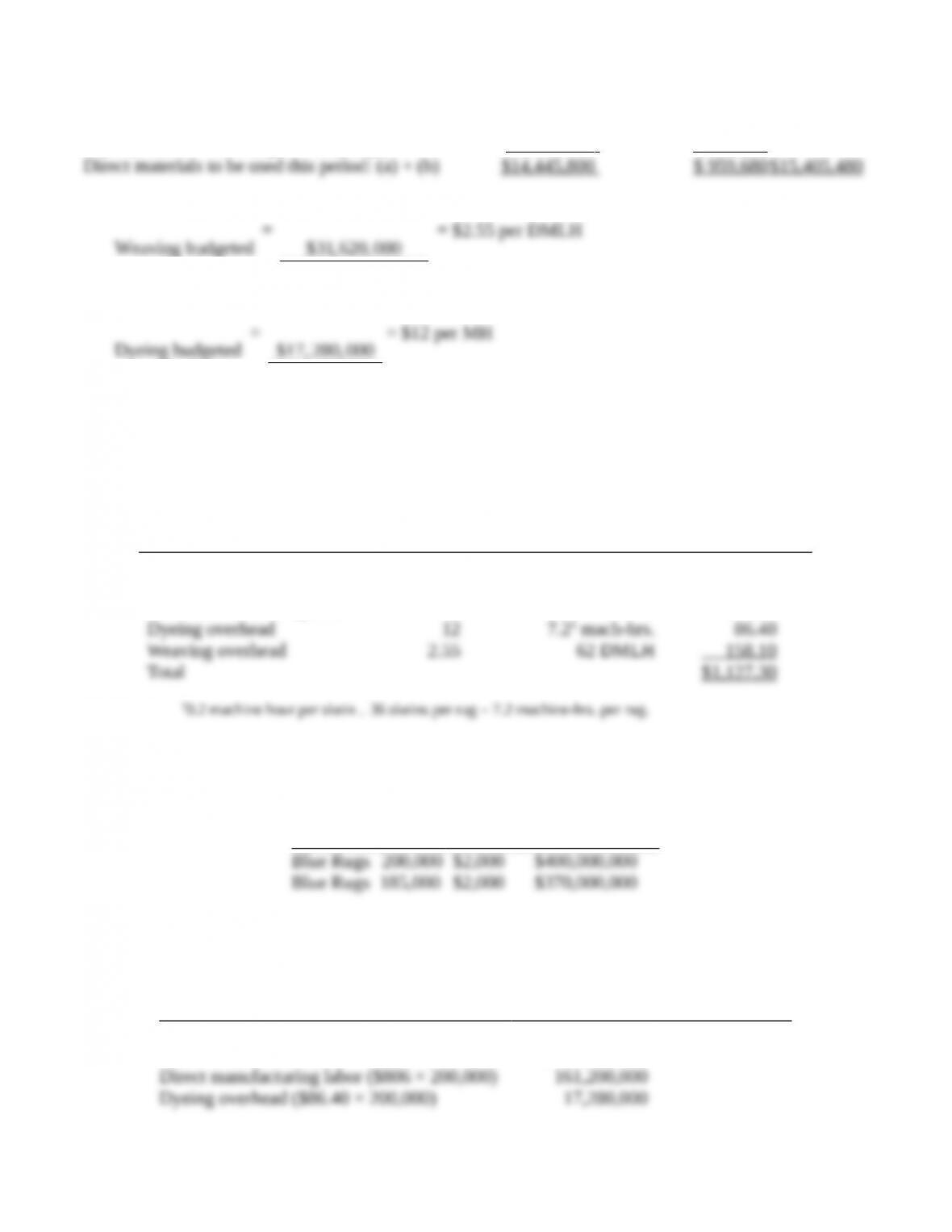

6-2

Wool: (7,200,000 – 458,000) skeins × $2 per skein 13,484,000

Dye: (160,000 – 4,000) gal. × $6 per gal. 936 ,000

2.

Weaving budgeted

overhead rate

=

$31,620,000

12,400,000 DMLH

= $2.55 per DMLH

Dyeing budgeted

overhead rate

=

$17, 280, 000

1, 440,000 MH

= $12 per MH

3.

Budgeted Unit Cost of Blue Rug

Cost per

Unit of Input

Input per

Unit of

Output Total

Wool $ 2 36 skeins $ 72.00

Dye 6 0.8 gal. 4.80

Direct manufacturing labor 13 62 hrs. 806.00

10.2 machine hour per skein

´

4.

Revenue Budget

Units

Selling

Price Total Revenues

5a.

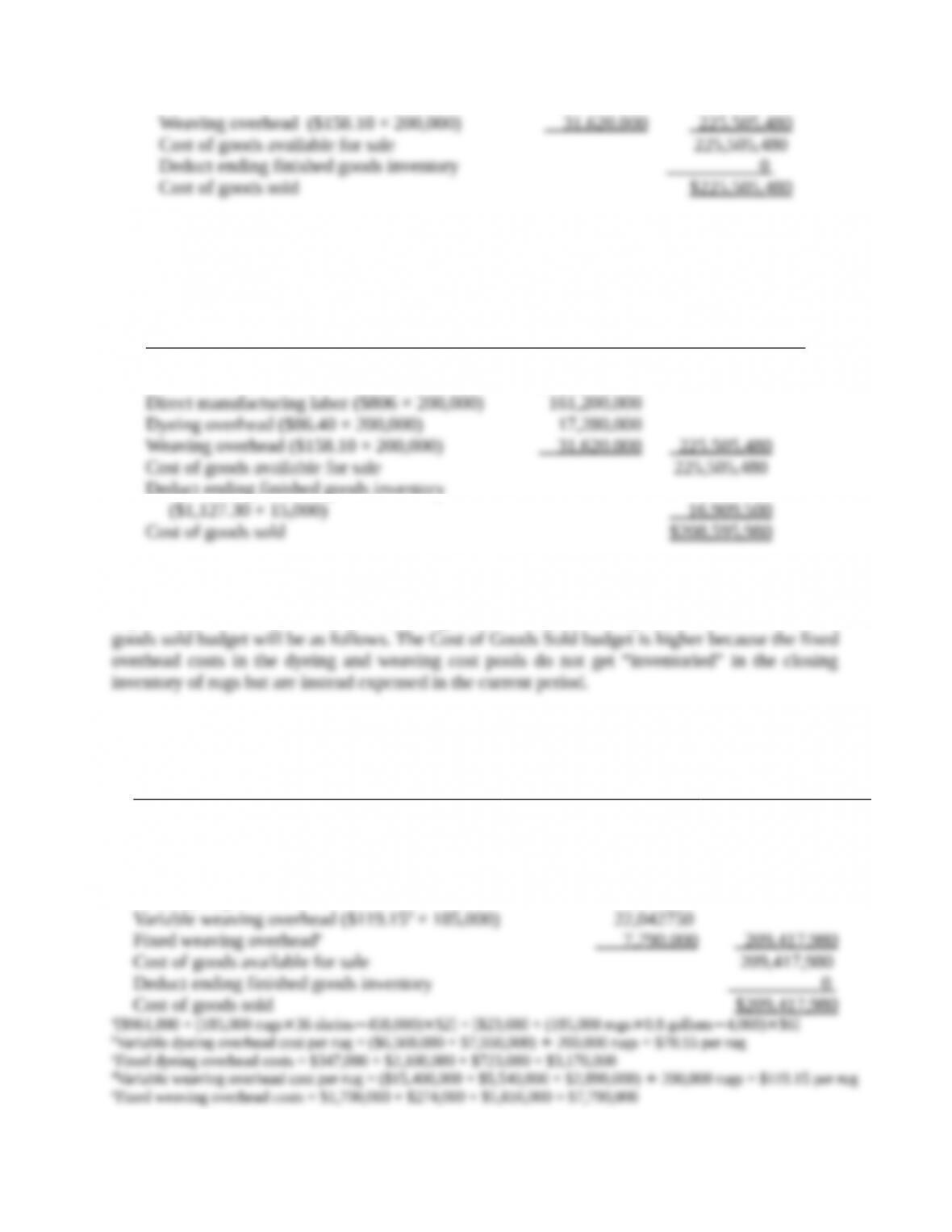

Sales = 200,000 rugs

Cost of Goods Sold Budget

From Schedule Total

Beginning finished goods inventory $ 0

Direct materials used $ 15,405,480

6-3

5b.

Sales = 185,000 rugs

Production = 200,000 rugs

Cost of Goods Sold Budget

From Schedule Total

Beginning finished goods inventory $ 0

Direct materials used $ 15,405,480

Deduct ending finished goods inventory

Some students assume that Xander will produce only 185,000 rugs to match 185,000 rugs that ar

expected to be sold and carry no finished good inventory of the rugs. In this case the Cost of

Sales = 185,000 rugs

Cost of Goods Sold Budget for Producing 185,000 rugs

From Schedule Total

Beginning finished goods inventory $ 0

Direct materials useda$ 14,253,480

Direct manufacturing labor ($806 × 185,000) 149,110,000

Variable dyeing overhead ($70.55b × 185,000) 13,051,750

Fixed dyeing overheadc 3,170,000

6-4

6.

200,000 rugs sold

185,000 rugs sold

200,000 rugs produced

185,000 rugs sold

185,000 rugs produced

Revenue $400,000,000 $370,000,000 $370,000,000

7. If sales drop to 185,000 blue rugs, Xander should look to reduce fixed costs and produce

8. Top management can look for ways to increase (stretch) sales and improve quality,

efficiency, and input prices to reduce costs in each cost category such as direct materials, direct

6-28 Budgeting, service company. Ever Clean Company provides gutter cleaning services to

residential clients. The company has enjoyed considerable growth in recent years due to a

successful marketing campaign and favorable reviews on service-rating Web sites. Ever Clean

owner Joanne Clark makes sales calls herself and quotes on jobs based on length of gutter

surface. Ever Clean hires college students to drive the company vans to jobs and clean the

gutters. A part-time bookkeeper takes care of billing customers and other office tasks. Overhead

is allocated based on direct labor-hours (DLH).

Joanne Clark estimates that her gutter cleaners will work a total of 1,000 jobs during the year.

Each job averages 600 feet of gutter surface and requires 12 direct labor-hours. Clark pays her

gutter cleaners $15 per hour, inclusive of taxes and benefits. The following table presents the

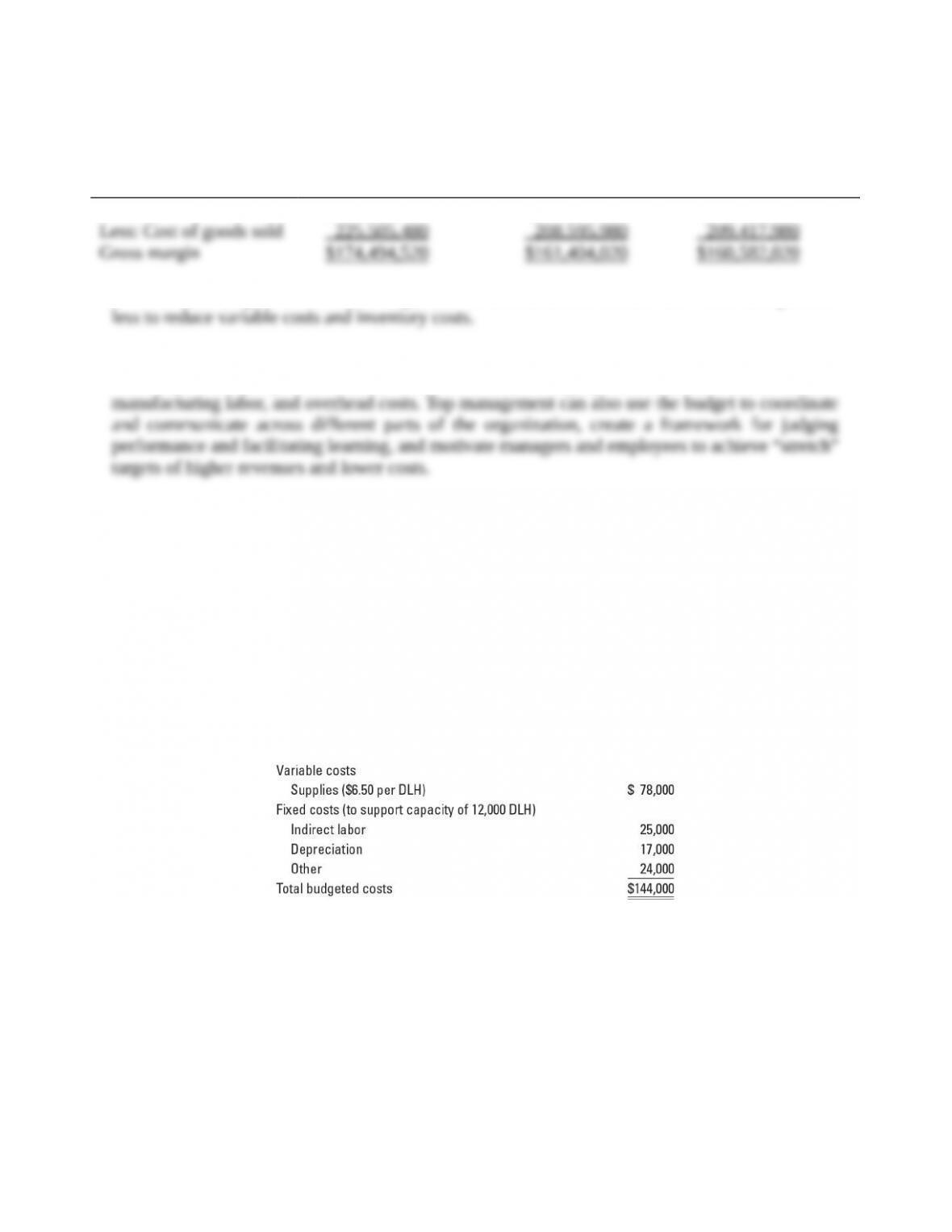

budgeted overhead costs for 2018:

Required:

1. Prepare a direct labor budget in both hours and dollars.

2. Calculate the budgeted overhead allocation rate based on the budgeted quantity of the cost

drivers.

3. Calculate the budgeted total cost of all jobs for the year and the budgeted cost of an average

600-foot gutter-cleaning job.

4. Prepare a revenues budget for the year, assuming that Ever Clean charges customers $0.60 per

square foot.

6-5

5. Calculate the budgeted operating income.

6. What actions can Clark take if sales should decline to 900 jobs annually?

SOLUTION

(20 min.) Budgeting: service company.

1.

Direct Labor Budget in Hours and Dollars

Total

Hours Budget

Direct labor hours required

Cost Budget

2.

Budgeted overhead rate =

$60,000

25,000 miles

$144,000

12,000 DLH

= $12 per DLH

3.

Budgeted Total Cost and Average Cost of 600-Foot Gutter-Cleaning Job

Direct labor costs $180,000

Overhead costs 144,000

Total costs of 1,000 jobs $324,000

4.

Revenue Budget

Feet of Gutter Surface Price per Foot Total Revenues

5. Operating Income Budget

1,000 jobs

Revenue $360,000

6. The following table shows Ever Clean’s profitability if sales decline to 900 jobs.

6-6

Revenue (900 jobs 600 sq. ft. 0.60/sq. ft. $324,000

$ 25 ,800

If revenue should fall to 900 jobs, Clark should examine the company’s fixed overhead costs to

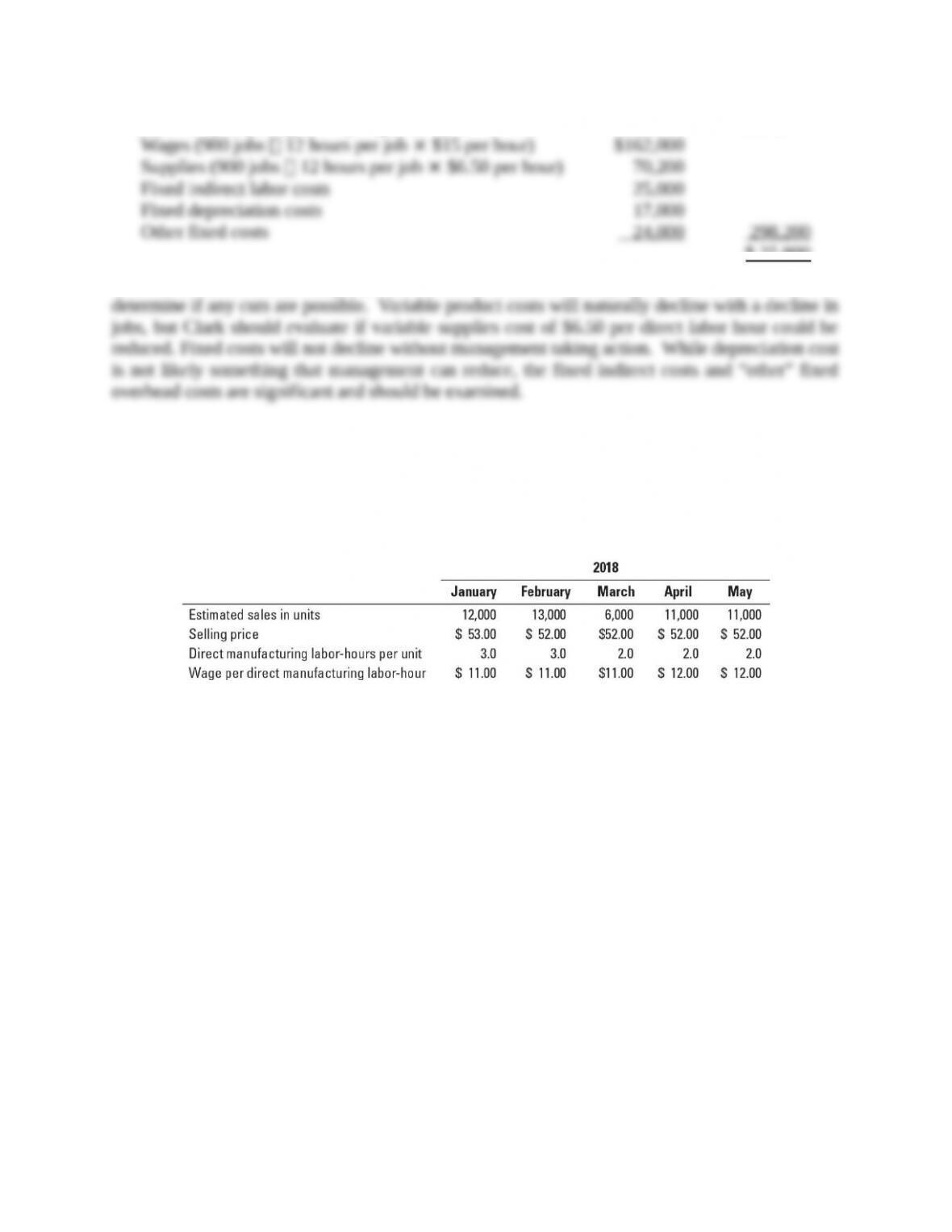

6-29 Budgets for production and direct manufacturing labor. (CMA, adapted) DeWitt

Company makes and sells artistic frames for pictures of weddings, graduations, and other special

events. Ron Bahar, the controller, is responsible for preparing DeWitt’s master budget and has

accumulated the following information for 2018:

In addition to wages, direct manufacturing labor-related costs include pension contributions of

$0.40 per hour, worker’s compensation insurance of $0.10 per hour, employee medical insurance

of $0.50 per hour, and Social Security taxes. Assume that as of January 1, 2018, the Social

Security tax rates are 7.5% for employers and 7.5% for employees. The cost of employee

benefits paid by DeWitt on its direct manufacturing employees is treated as a direct

manufacturing labor cost.

DeWitt has a labor contract that calls for a wage increase to $12 per hour on April 1, 2018.

New labor-saving machinery has been installed and will be fully operational by March 1, 2018.

DeWitt expects to have 16,000 frames on hand at December 31, 2017, and it has a policy of

carrying an end-of-month inventory of 100% of the following month’s sales plus 50% of the

second following month’s sales.

Required:

1. Prepare a production budget and a direct manufacturing labor cost budget for DeWitt Company

by month and for the first quarter of 2018. You may combine both budgets in one schedule.

The direct manufacturing labor cost budget should include labor-hours and show the details for

each labor cost category.

2. What actions has the budget process prompted DeWitt’s management to take?

6-7

3. How might DeWitt’s managers use the budget developed in requirement 1 to better manage the

company?

SOLUTION

(15-25 min.) Budgets for production and direct manufacturing labor.

DeWitt Company

Budget for Production and Direct Manufacturing Labor

for the Quarter Ended March 31, 2018

January February March Quarter

Budgeted sales (units) 12,000 13,000 6,000 31,000

Add target ending finished goods

Deduct beginning finished goods

inventory (units) 16,000 16,000 11,500 16,000

Direct manufacturing labor-hours

Total hours of direct manufacturing

Direct manufacturing labor costs:

Pension contributions

Workers’ compensation insurance

Employee medical insurance

Social Security tax (employer’s share)

2. The budget process would prompt DeWitt’s management to look for ways to reduce finished

goods inventories, the manufacturing labor hours needed to produce each unit both before and

6-8

3. We already see one example of a decision that DeWitt’s management took based on the

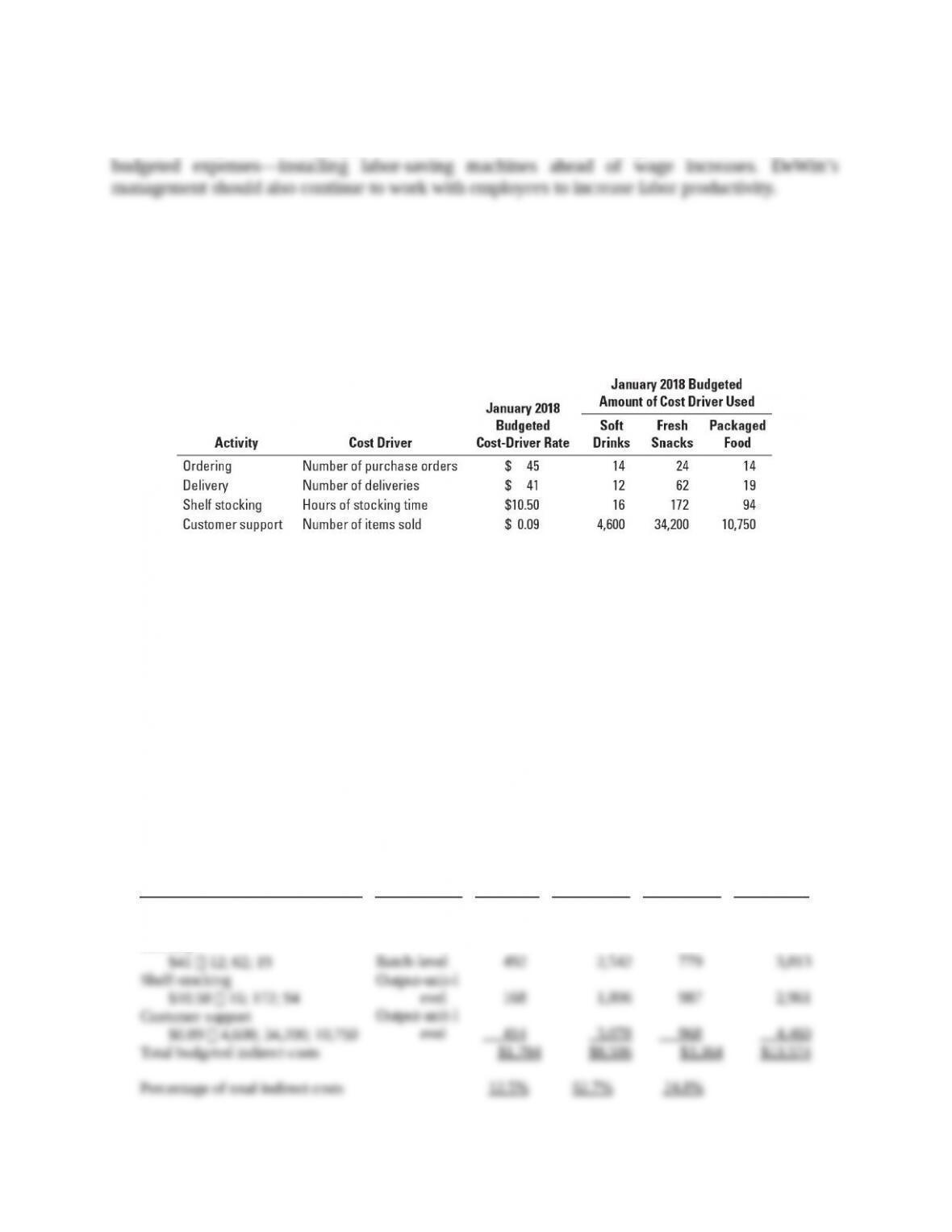

6-30 Activity-based budgeting. The Jerico store of Jiffy Mart, a chain of small neighborhood

convenience stores, is preparing its activity-based budget for January 2018. Jiffy Mart has three

product categories: soft drinks (35% of cost of goods sold [COGS]), fresh produce (25% of

COGS), and packaged food (40% of COGS). The following table shows the four activities that

consume indirect resources at the Jerico store, the cost drivers and their rates, and the cost-driver

amount budgeted to be consumed by each activity in January 2018.

Required:

1. What is the total budgeted indirect cost at the Jerico store in January 2018? What is the total

budgeted cost of each activity at the Jerico store for January 2018? What is the budgeted

indirect cost of each product category for January 2018?

2. Which product category has the largest fraction of total budgeted indirect costs?

3. Given your answer in requirement 2, what advantage does Jiffy Mart gain by using an

activity-based approach to budgeting over, say, allocating indirect costs to products based on

cost of goods sold?

SOLUTION

(20–30 min.) Activity-based budgeting.

1.

Activity

Cost

Hierarchy

Soft

Drinks

Fresh

Snacks

Packaged

Food Total

Ordering

$45 14; 24; 14

Delivery

Batch-level

$ 630

$1,080

$ 630

$ 2,340

6-9

2. Refer to the last row of the table in requirement 1. Fresh snacks, which represents the

smallest portion of COGS (25%), is the product category that consumes the largest share (62.7%)

3. An ABB approach recognizes how different products require different mixes of support

activities. The relative percentage of how each product area uses the cost driver at each activity

area is:

Activity

Cost

Hierarchy

Soft

Drinks

Fresh

Snacks

Packaged

Food Total

By recognizing these differences, Jiffy Mart’s managers are better able to budget for different

unit sales levels and different mixes of individual product-line items sold. Using a single cost

driver (such as COGS) assumes homogeneity in the use of indirect costs (support activities)

6-31 Kaizen approach to activity-based budgeting (continuation of 6-30). Jiffy Mart has a

Kaizen (continuous improvement) approach to budgeting monthly activity costs for each month of

2018. Each successive month, the budgeted cost-driver rate decreases by 0.4% relative to the

preceding month. So, for example, February’s budgeted cost-driver rate is 0.996 times January’s

budgeted cost-driver rate, and March’s budgeted cost-driver rate is 0.996 times the budgeted

February rate. Jiffy Mart assumes that the budgeted amount of cost-driver usage remains the same

each month.

Required:

1. What are the total budgeted cost for each activity and the total budgeted indirect cost for

March 2018?

2. What are the benefits of using a Kaizen approach to budgeting? What are the limitations of

this approach, and how might Jiffy Mart management overcome them?

6-10