Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

SOLUTION

(25 min.) Cost-plus, target return on investment pricing.

´

2.

* solve backwards for revenues

Selling price =

$4,800,000

400,000 cases =

$12 per case.

Markup % on full cost

Full cost = $2,000,000 + $1,600,000 = $3,600,000

Unit cost = $3,600,000 ÷ 400,000 cases = $9.00 per case

Markup % on full cost =

$12 - $9

$9 =

33.33%

3.

Budgeted Operating Income

For the year ending December 31, 20xx

Revenues ($13

´

360,000 cases*)

$4,680,000

Variable costs ($5

´

360,000 cases)

´

Return on investment =

$1, 280,000

$10,000,000 =

12.8%

13-1

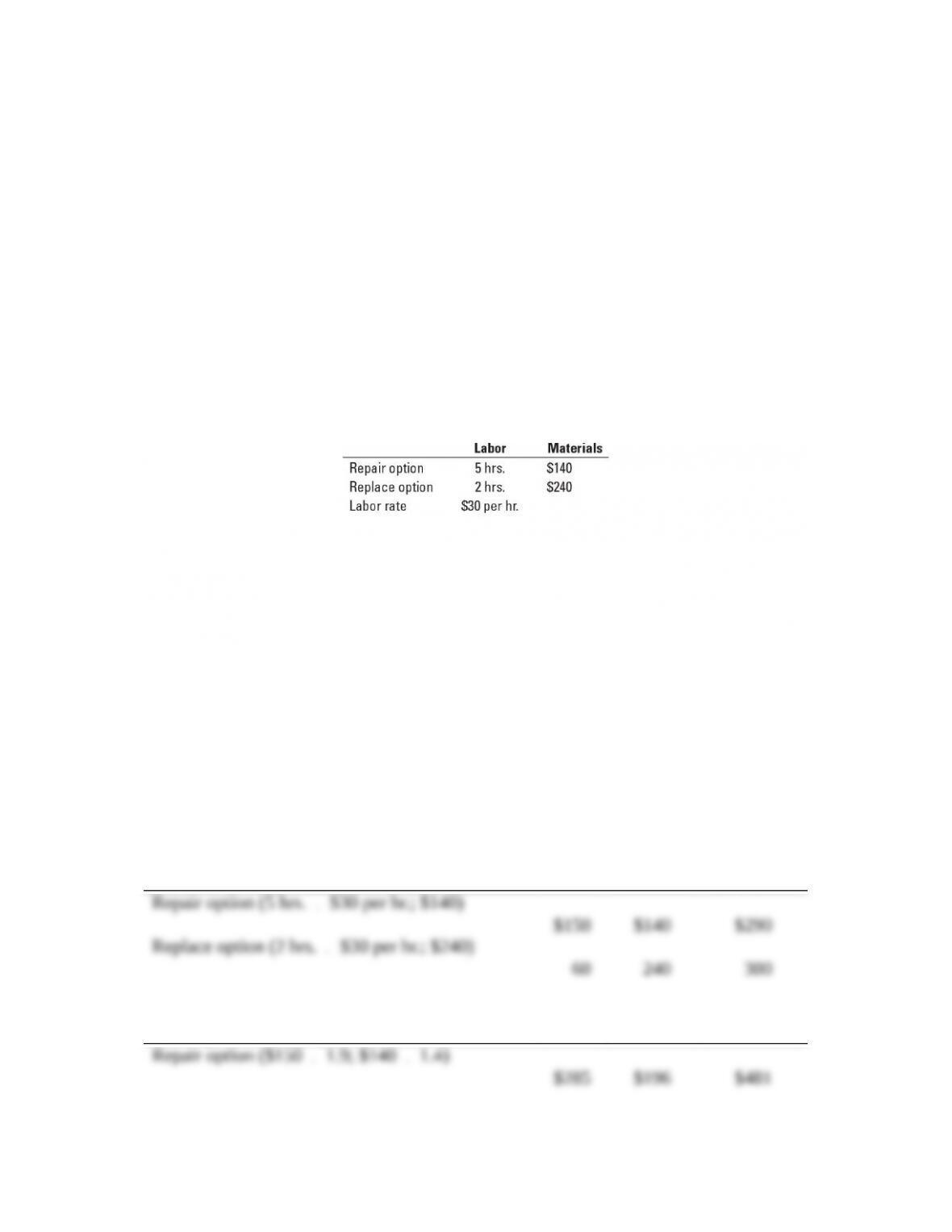

PRICE (90% markup on labor cost; 40%

markup on materials) Labor Materials Total Price

13-2

2. If the repair and replace options are equally effective, Lee will choose to get the air

conditioning system replaced for $450 (rather than spend $481 on repairing it).

3. C&S Mechanical will earn a greater contribution toward overhead in the repair option

($191 = $481 – $290) than in the replace option ($150 = $450 – $300). Therefore, Anderson will

recommend the repair option to Lee, which is not the one she would prefer. Recognizing this

The ethical course of action would be to honestly present both options to Lee and have

13-31 Cost-plus and market-based pricing. Georgia Temps, a large labor contractor, supplies

contract labor to building-construction companies. For 2017, Georgia Temps has budgeted to

supply 84,000 hours of contract labor. Its variable costs are $13 per hour, and its fixed costs are

$168,000. Roger Mason, the general manager, has proposed a cost-plus approach for pricing

labor at full cost plus 20%.

Required:

1. Calculate the price per hour that Georgia Temps should charge based on Mason’s proposal.

2. The marketing manager supplies the following information on demand levels at different

prices:

Georgia Temps can meet any of these demand levels. Fixed costs will remain unchanged for

all the demand levels. On the basis of this additional information, calculate the price per hour

that Georgia Temps should charge to maximize operating income.

3. Comment on your answers to requirements 1 and 2. Why are they the same or different?

SOLUTION

13-3

(25 min.) Cost-plus and market-based pricing.

1. Georgia Temps’ full cost per hour of supplying contract labor is

2. Contribution margins for different prices and demand realizations are as follows:

Price per Hour

(1)

Variable Cost

per Hour

(2)

Contribution

Margin per

Hour

(3) = (1) – (2)

Demand in

Hours

(4)

Total

Contribution

(5) = (3) × (4)

Fixed costs will remain the same regardless of the demand realizations. Fixed costs are,

therefore, irrelevant because they do not differ among the alternatives.

The table above indicates that Georgia Temps can maximize contribution margin

($444,000) and operating income by charging a price of $19 per hour.

3. The cost-plus approach to pricing in requirement 1 does not explicitly consider the effect

of prices on demand. The approach in requirement 2 models the interaction between price and

demand and determines the optimal level of profitability using concepts of relevant costs. The

13-32 Cost-plus and market-based pricing. (CMA, adapted) Precision Laboratories

evaluates the reaction of materials to extreme increases in temperature. Much of the

company’s early growth was attributable to government contracts, but recent growth has come

from expansion into commercial markets. Two types of testing at Precision are Heat Testing

(HTT) and Arctic-Condition Testing (ACT). Currently, all of the budgeted operating costs are

collected in a single overhead pool. All of the estimated testing-hours are also collected in a

single pool. One rate per test-hour is used for both types of testing. This hourly rate is marked

up by 40% to recover administrative costs and taxes and to earn a profit.

13-4

Jeff Boone, Precision’s controller, believes that there is enough variation in the test

procedures and cost structure to establish separate costing rates and billing rates at a 40%

markup. He also believes that the inflexible rate structure the company is currently using is

inadequate in today’s competitive environment. After analyzing the company data, he has

divided operating costs into the following three cost pools:

Jeff Boone budgets 100,000 total test-hours for the coming period. Test-hours is also the cost

driver for labor and supervision. The budgeted quantity of cost driver for setup and facility costs

is 600 setup hours. The budgeted quantity of cost driver for utilities is 9,000 machine-hours.

Jeff has estimated that HTT uses 60% of the test-hours, 20% of the setup-hours, and half the

machine-hours.

Required:

1. Find the single rate for operating costs based on test-hours, and the hourly billing rate for

HTT and ACT.

2. Find the three activity-based rates for operating costs.

3. What will the billing rate for HTT and ACT be based on the activity-based costing structure?

State the rates in terms of test-hours. Referring to both requirements 1 and 2, which rates

make more sense for Precision?

4. If Precision’s competition all charge $19.50 per hour for arctic testing, what can Precision do

to stay competitive?

SOLUTION

Cost-plus and market-based pricing.

´

$300,000

600 setup hours

13-5

Utilities =

$360,000

9,000 machine-hours

= $40 per machine-hour (MH)

3.

HTT ACT Total

Labor and supervision

($5 × 60,000; 40,000 test-hours)1$300,000 $200,000 $ 500,000

Setup and facility cost

($500 × 120; 480 setup-hours)260,000 240,000 300,000

Utilities

($40 × 4,500; 4,500 machine-hours)3 180 ,000

180 ,000 360 ,000

Total cost $540,000 $620,000 $1 ,160,000

Number of testing hours (TH) ÷ 60 ,000 TH ÷ 40 ,000 TH

Cost per testing hour $9.00 per TH $ 15.50 per TH

Mark-up × 1.40 × 1.40

Billing rate per testing hour $ 12.60 per TH $ 21.70 per TH

1100,000 test-hours

´

60% = 60,000 test-hours; 100,000 test-hours

´

40% = 40,000 test-hours

2600 setup-hours × 20% = 120 setup-hours; 600 setup-hours × 80% = 480 setup-hours

39,000 machine-hours × 50% = 4,500 machine-hours; 9,000 machine-hours × 50%

= 4,500 machine-hours

The billing rates based on the activity-based cost structure make more sense. These billing rates

reflect the ways the testing procedures consume the firm’s resources.

4. To stay competitive, Precision Laboratories needs to be more efficient in arctic testing.

Roughly 40% of arctic testing’s total cost

240,000 39%

620,000

æ ö

=

ç ÷

è ø

occurs in setups and facility costs.

Perhaps the setup activity can be redesigned to achieve cost savings. Precision Laboratories

should also look for savings in the labor and supervision cost per test-hour and the total number

of test-hours used in arctic testing, as well as the utility cost per machine-hour and the total

number of machine hours used in arctic testing. This may require redesigning the test,

redesigning processes, and achieving efficiency and productivity improvements.

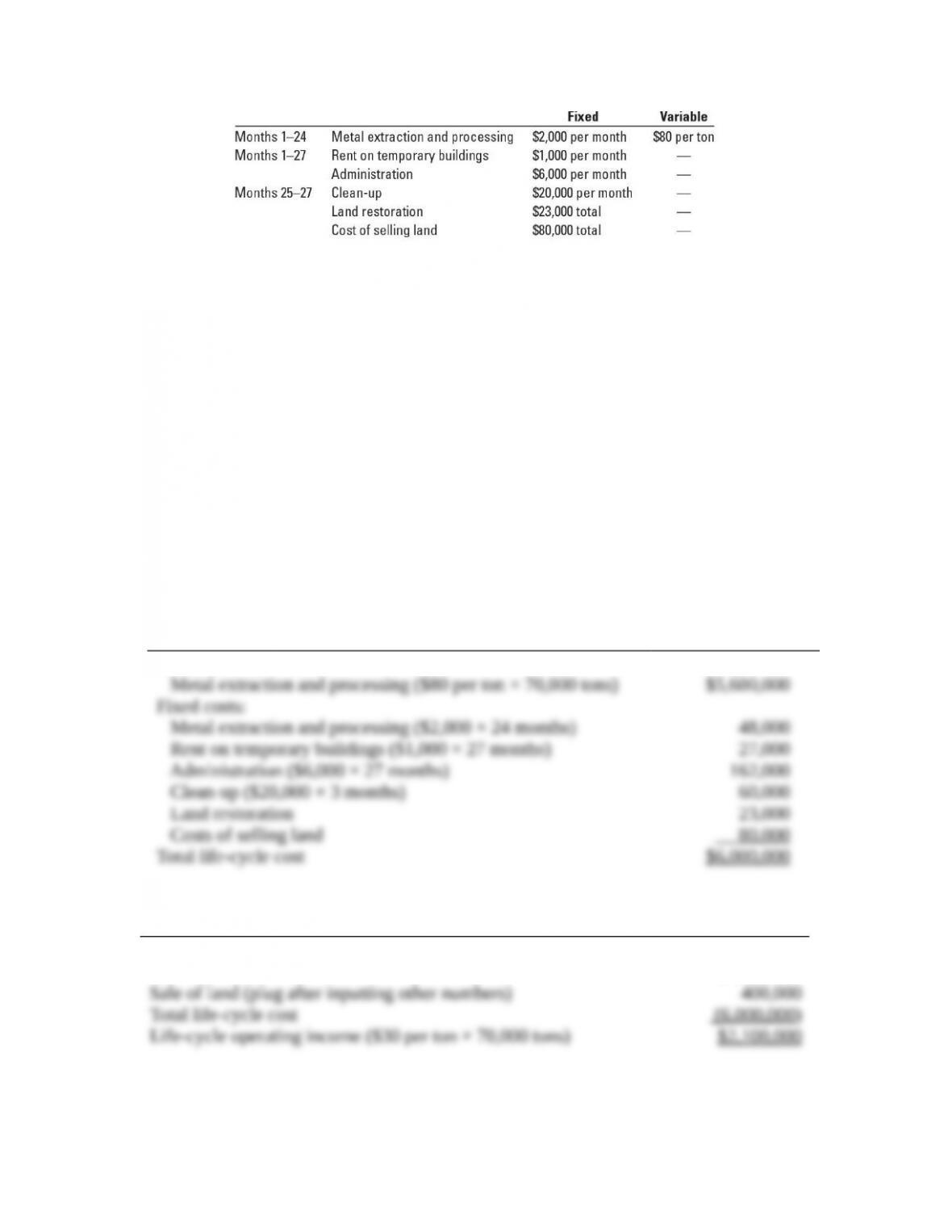

13-33 Life-cycle costing. Maximum Metal Recycling and Salvage receives the opportunity to

salvage scrap metal and other materials from an old industrial site. The current owners of the site

will sign over the site to Maximum at no cost. Maximum intends to extract scrap metal at the site

for 24 months and then will clean up the site, return the land to useable condition, and sell it to a

developer. Projected costs associated with the project follow:

13-6

Required:

Ignore the time value of money.

1. Assuming that Maximum expects to salvage 70,000 tons of metal from the site, what is the

total project life-cycle cost?

2. Suppose Maximum can sell the metal for $110 per ton and wants to earn a profit (before

taxes) of $30 per ton. At what price must Maximum sell the land at the end of the project to

achieve its target profit per ton?

3. Now suppose Maximum can only sell the metal for $100 per ton and the land at $110,000

less than what you calculated in requirement 2. If Maximum wanted to maintain the same

markup percentage on total project life-cycle cost as in requirement 2, by how much would

the company have to reduce its total project life-cycle cost?

SOLUTION

(25–30 min.) Life-cycle costing.

1.

Total Project Life-Cycle Costs

Variable costs:

2.

Projected Life Cycle Income Statement

Revenue ($110 per ton

´

70,000 tons)

$7,700,000

13-7

Mark-up percentage on project life-cycle cost =

Life cycle operating income

Total life-cycle cost

$2,100,000

$6,000,000

=

The company would have to sell the land for $400,000.

3.

$150,000.

Required:

1. If you could charge different prices to business travelers and pleasure travelers, would you?

Show your computations.

2. Explain the key factor (or factors) for your answer in requirement 1.

3. How might Costal Airways implement price discrimination? That is, what plan could the

airline formulate so that business travelers and pleasure travelers each pay the price the

airline desires?

SOLUTION

(30 min.) Airline pricing, considerations other than cost in pricing.

1. If the fare is $600,

a. Coastal Airways would expect to have 225 business and 110 pleasure travelers.

b. Variable costs per passenger would be $65.

Contribution margin from business travelers at prices of $600 and $1,350, respectively,

follow:

Coastal Airways would maximize contribution margin and operating income by charging

business travelers a fare of $1,350.

follow:

Coastal Airways would maximize contribution margin and operating income by charging

pleasure travelers a fare of $600.

Coastal Airways would maximize contribution margin and operating income by a price

differentiation strategy, where business travelers are charged $1,350 and pleasure travelers $600.

In deciding between the alternative prices, all other costs such as fuel costs, allocated

annual lease costs, allocated ground services costs, and allocated flight crew salaries are

irrelevant. Why? Because these costs will not change whatever price Coastal Airways chooses to

charge.

2. The elasticity of demand of the two classes of passengers drives the different demands of

the travelers. Business travelers are relatively price insensitive because they must get to their

destination during the week (exclusive of weekends) and their fares are paid by their companies.

13-9

3. Because business travelers often want to return within the same week, while pleasure

travelers often stay over weekends, a requirement that a Saturday night stay is needed to qualify

13-35 Anti-trust laws and pricing. Global Airlines is a major low-price airline carrier for both

domestic and international travel. The company guarantees the “lowest price” ticket for travel

within the United States. The “lowest price” ticket guarantee does not apply for travel on

Monday mornings and Friday evenings, which are busy travel times for business travelers.

Required:

1. Do these pricing practices of Global Airlines violate any anti-trust laws? Why or why not?

2. Why is Global Airlines not offering a price guarantee for flights on Monday mornings and

Friday evenings? Do you agree with this policy? Explain briefly.

3. What other factors should Global Airlines consider before implementing these pricing

policies?

13-10