SCHAPTER 19

BALANCED SCORECARD: QUALITY AND TIME

19-1 Describe two benefits of improving quality.

Quality costs (including the opportunity cost of lost sales because of poor quality) can be as

19-2 How does conformance quality differ from design quality? Explain.

Design quality refers to how closely the characteristics of a product or service meet the needs

19-3 Name two items classified as prevention costs.

Exhibit 19-1 of the text lists the following six line items in the prevention costs category: design

19-4 Give two examples of appraisal costs.

19-5 Distinguish between internal failure costs and external failure costs.

An internal failure cost differs from an external failure cost on the basis of when the

19-6 Describe three methods that companies use to identify quality problems.

Three methods that companies use to identify quality problems are (a) a control chart, which is a

graph of a series of successive observations of a particular step, procedure, or operation taken at

19-7 “Companies should focus on financial measures of quality because these are the only

measures of quality that can be linked to bottom-line performance.” Do you agree? Explain.

No. It is true that an important advantage of financial measures of quality is that they can be

linked to bottom-line performance, but nonfinancial measures, such as number of defects,

19-1

19-8 Give two examples of nonfinancial measures of customer satisfaction relating to quality.

Examples of nonfinancial measures of customer satisfaction relating to quality include the

following:

1. the number of defective units shipped to customers as a percentage of total units of product

shipped;

2. the number of customer complaints;

19-9 Give two examples of nonfinancial measures of internal-business-process quality.

Examples of nonfinancial measures of internal-business-process quality include the following:

1. the percentage of defective products;

19-10 “When evaluating alternative ways to improve quality, managers need to consider the

fully allocated costs of quality.” Do you agree? Explain.

When evaluating alternative ways to improve quality, managers need to identify the relevant

19-11 Distinguish between customer-response time and manufacturing cycle time.

Customer-response time is how long it takes from the time a customer places an order for a

product or a service to the time the product or service is delivered to the customer.

19-2

19-16 Rector Corporation is examining its quality control program. Which of the following

statements is/are correct?

I. Rework costs should be regarded as a cost of quality when the rework is caused by internal

failure.

II. Prevention costs are costs that are incurred to prevent the sale and production of defective

units.

III.Internal failure costs are costs of failure of machinery on the production line.

1. I, II, and III are correct. 2. II only is correct.

3. I and III only are correct. 4. I only is correct.

SOLUTION

Choice “4” is correct.

This question asks which of a series of statements with respect to quality control is/are correct.

Statement I says that rework costs should be regarded as a cost of quality when the rework is caused by

internal failure. Statement I is correct.

19-17 Six Sigma is a continuous quality improvement methodology that is designed to promote:

1. Improvements for existing products and business processes.

2. Development of new products or business processes.

3. Both existing product/process improvement and new product process development.

4. Statistical evaluation of critical success factors.

SOLUTION

Choice “3” is correct.

Six Sigma is a quality improvement program that is used both to improve current products or processes

and to develop new products or processes.

19-4

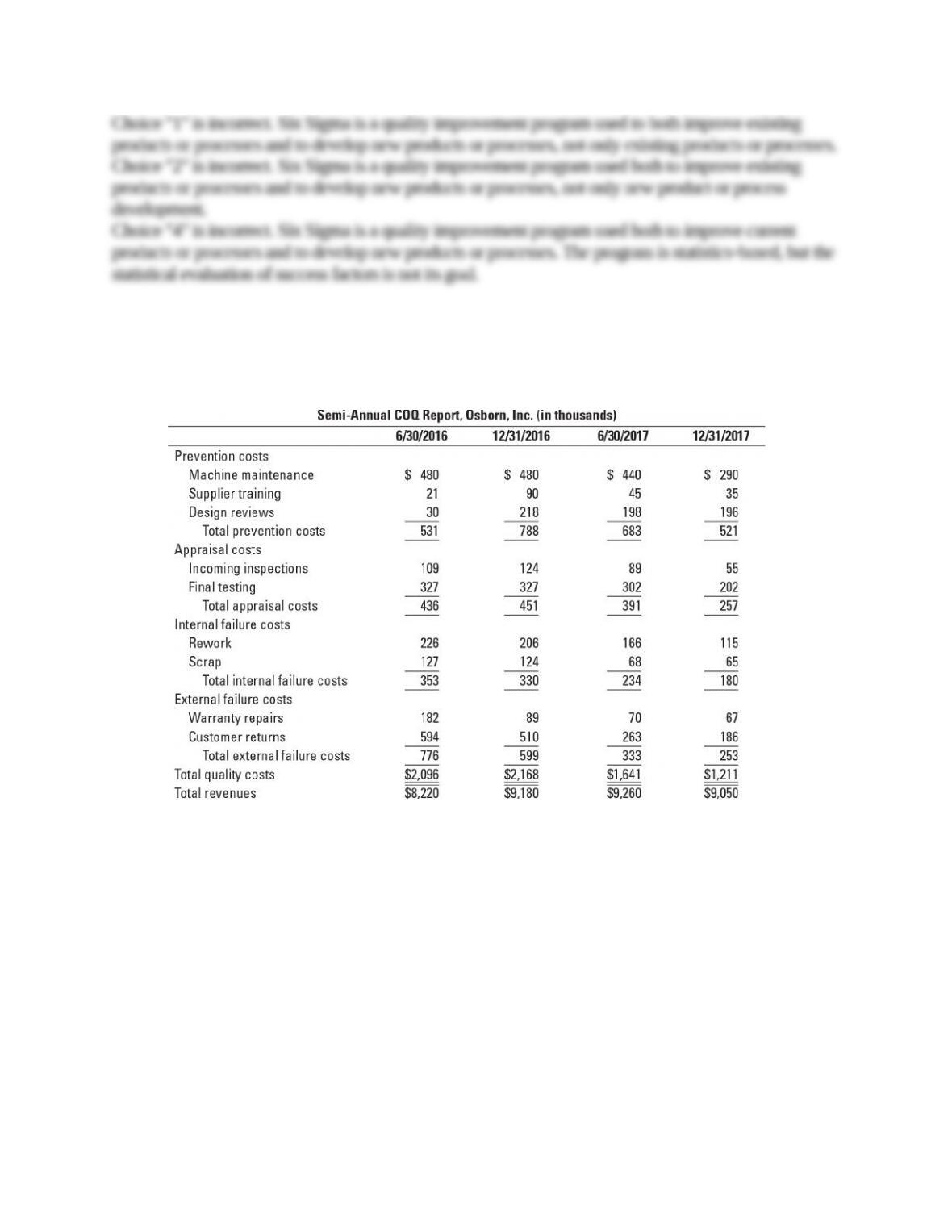

19-18 Costs of quality. (CMA, adapted) Osborn, Inc., produces cell phone equipment. Amanda

Westerly, Osborn’s president, implemented a quality-improvement program that has now been in

operation for 2 years. The cost report shown here has recently been issued.

Required:

1. For each period, calculate the ratio of each COQ category to revenues

and to total quality costs.

2. Based on the results of requirement 1, would you conclude that Osborn’s

quality program has been successful? Prepare a short report to present your

case.

3. Based on the 2015 survey, Amanda Westerly believed that Osborn had to

improve product quality. In making her case to Osborn management, how

might Westerly have estimated the opportunity cost of not implementing the

quality-improvement program?

SOLUTION

(30 min.) Costs of quality.

19-5

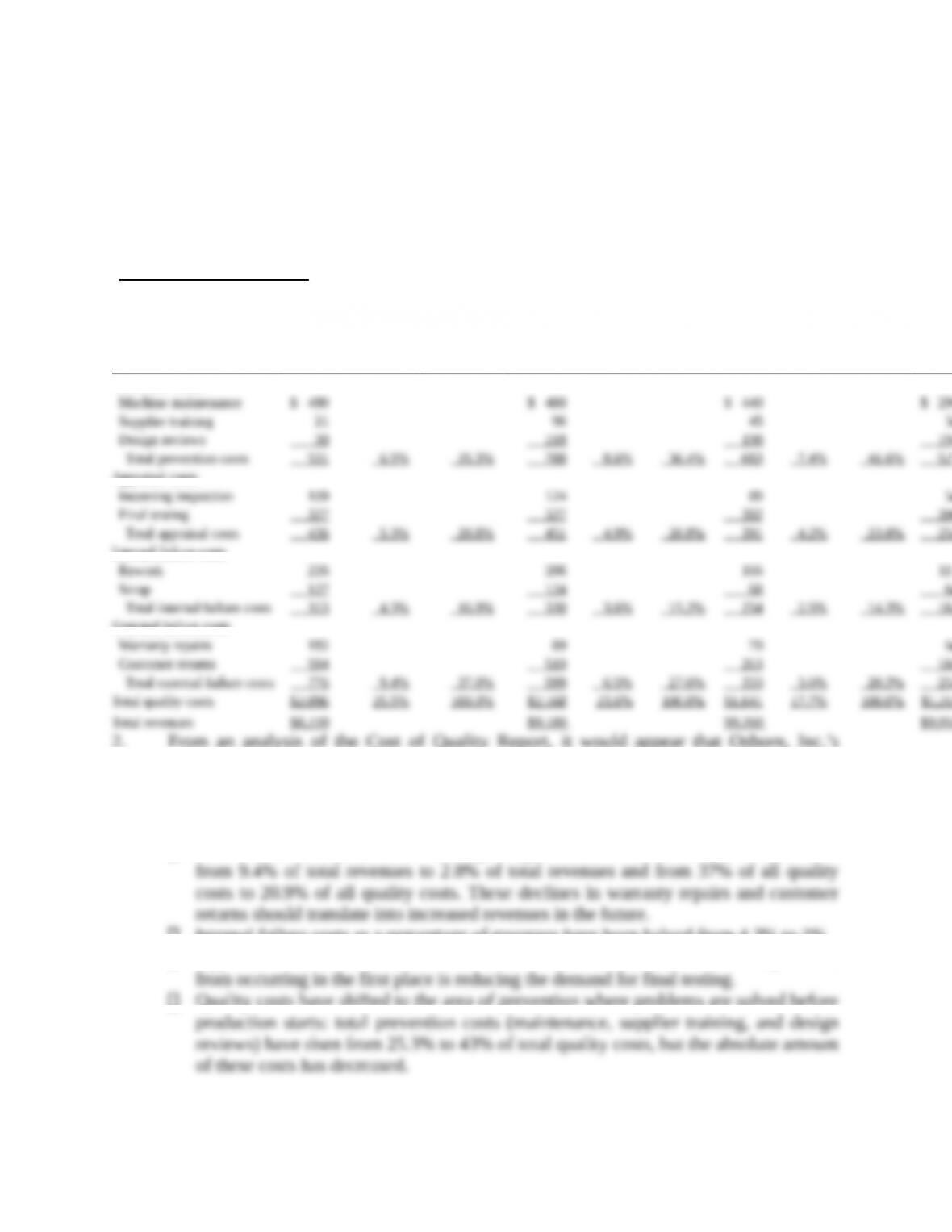

1. The ratios of each COQ category to revenues and to total quality costs for each period are

as follows:

Osborn, Inc.: Semi-Annual Costs of Quality Report

(in thousands)

6/30/2016 12/31/2016 6/30/2017

Actual

% of

Revenues

% of Total

Quality

Costs Actual

% of

Revenues

% of Total

Quality

Costs Actual

% of

Revenues

% of Total

Quality

Costs Actual

(2) = (3) = (5) = (6) = (8) = (9) =

(1) (1) ÷ $8,220 (1) ÷ $2,096 (4) (4) ÷ $9,180 (4) ÷ $2,168 (7) (7) ÷ $9,260 (7) ÷ $1,641 (10)

Prevention costs

Appraisal costs

Internal failure costs

External failure costs

2. From an analysis of the Cost of Quality Report, it would appear that Osborn, Inc.’s

program has been successful because

Total quality costs as a percentage of total revenues have declined from 25.5% to

13.4%.

External failure costs, those costs signaling customer dissatisfaction, have declined

Internal failure costs as a percentage of revenues have been halved from 4.3% to 2%.

Appraisal costs have decreased from 5.3% to 2.8% of revenues. Preventing defects

Quality costs have shifted to the area of prevention where problems are solved before

19-6

Because of improved designs, quality training, and additional preproduction

Production does not have to spend an inordinate amount of time with customer

3. To estimate the opportunity cost of not implementing the quality program and to help her

make her case, Amanda Westerly could have assumed that

Opportunity costs are not recorded in accounting systems because they represent the results of

19-19 Costs of quality analysis. Adirondack Company makes chairs for outside living spaces.

The company has been working on improving quality over the last year and wants to evaluate

how well it has done on costs-of-quality (COQ) measures. Here are the results:

Required:

1. Identify the costs-of-quality category (prevention, appraisal, internal failure, and external

failure) for each of these costs.

2. Prepare a COQ report by calculating the costs of quality for each category and the ratio of

each COQ category to revenues and total quality costs.

SOLUTION

(25 min.) Costs of quality analysis.

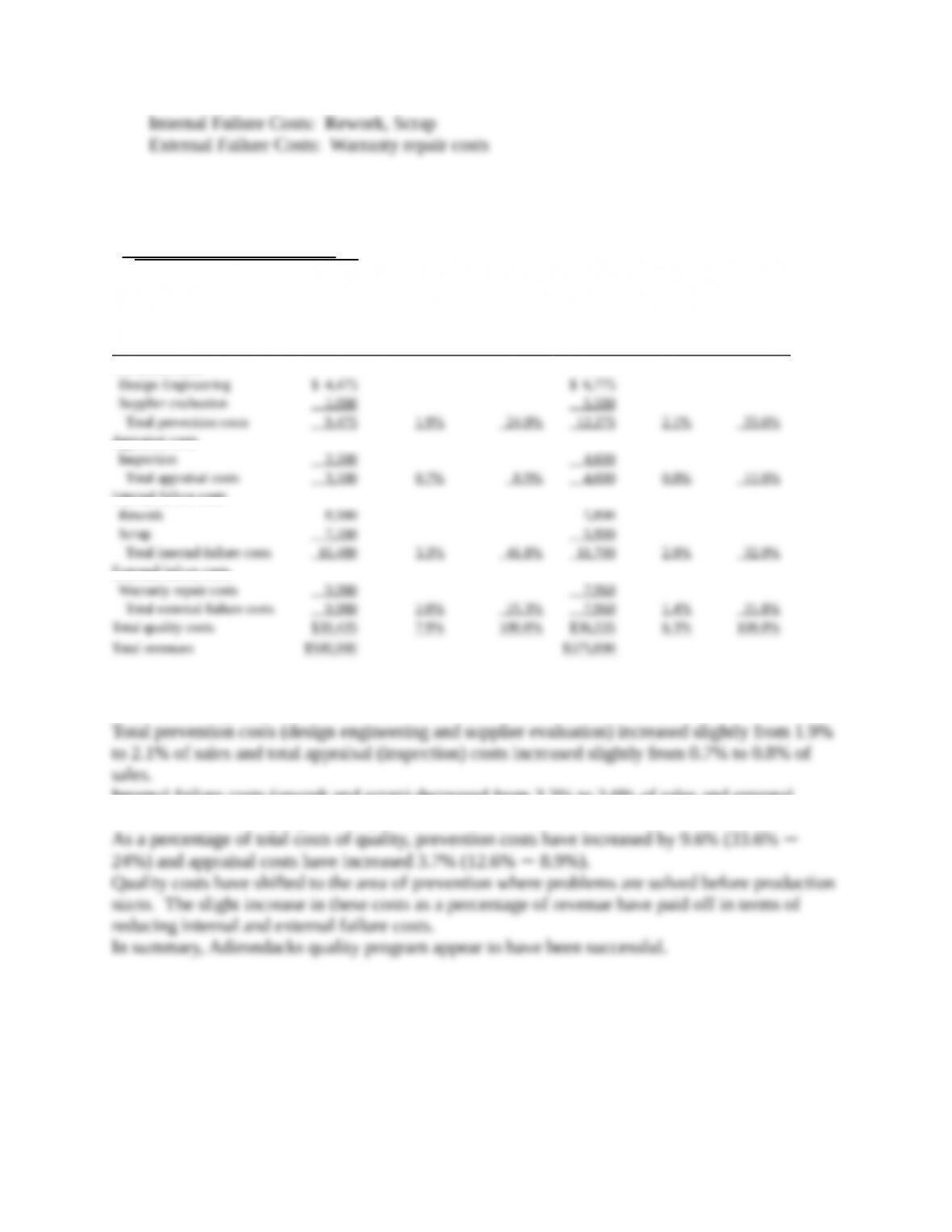

1. Prevention Costs: Design Engineering, Supplier Evaluations

Appraisal Costs: Inspection

19-7

2.

2016 2017

Actual

% of

Revenues

% of Total

Quality

Costs Actual

% of

Revenues

% of Total

Quality Costs

(2) = (3) = (5) = (6) =

(1) (1) ÷ $500,000 (1) ÷ $39,435 (4) (4) ÷ $575,000 (4) ÷ $36,535

Prevention costs

Appraisal costs

Internal failure costs

External failure costs

3. The cost of quality report indicates the following:

Total costs of Quality decreased from 7.9% of sales to 6.3% of sales.

Internal failure costs (rework and scrap) decreased from 3.3% to 2.0% of sales and external

failure costs (warranty repair costs) decreased from 2.0% to 1.4% of sales

19-20 Costs-of-quality analysis. Safe Travel produces car seats for children from newborn to 2

years old. Safe Travel’s only problem with its car seats was stitching in the straps. The problem

can usually be detected and repaired during an internal inspection. Inspection costs $5.00 per car

seat, and repairs cost $1.00 per car seat. All 200,000 car seats were inspected last year, and 5%

were found to have problems with the stitching. Another 1% of the 200,000 car seats had

problems with the stitching, but the internal inspection did not discover them. Defective units

19-8

that were sold and shipped to customers are shipped back to Safe Travel and repaired. Shipping

costs are $8.00 per car seat, and repair costs are $1.00 per car seat. Negative publicity will result

in a loss of future contribution margin of $100 for each external failure.

Required:

1. Identify total costs of quality by category (appraisal, internal failure, and external failure).

2. Safe Travel is concerned with the high up-front cost of inspecting all 200,000 units. It is

considering an alternative internal inspection plan that will cost only $3.00 per car seat

inspected. During the internal inspection, the alternative technique will detect only 3.5% of

the 200,000 car seats that have stitching problems. The other 2.5% will be detected after the

car seats are sold and shipped. What are the total costs of quality for the alternative

technique?

3. What factors other than cost should Safe Travel consider before changing inspection

techniques?

SOLUTION

(20 min.) Costs of quality analysis.

1. Appraisal cost = Inspection cost

Internal failure cost = Rework cost

Out of pocket external failure cost = Shipping cost + Repair cost

Opportunity cost of external failure = Lost future profits

2. Quality control costs under the alternative inspection technique:

19-9

3. In addition to the lower costs under the alternative inspection plan, Safe Travel should

consider a number of other factors:

a. There could easily be serious reputation effects if the percentage of external failures

increases by 250% (from 1% to 2.5%). This rise in external failures may lead to costs

greater than $100 per failure due to lost profits.

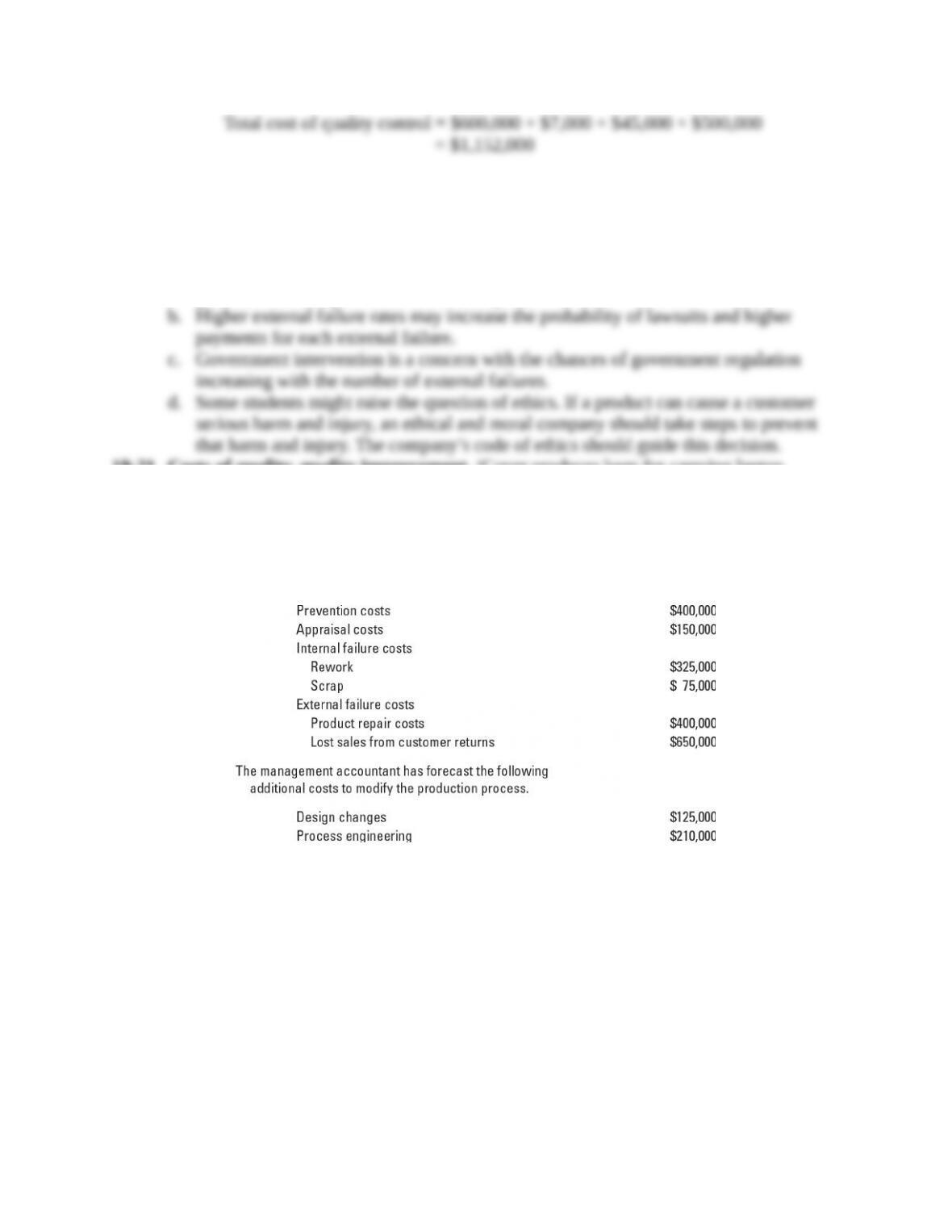

19-21 Costs of quality, quality improvement. iCover produces bags for carrying laptop

computers. iCover sells 1,000,000 units each year at a price of $20 per unit and a contribution

margin of 40%.

To respond to customer complaints, iCover’s mangers want to modify the production

processes to produce higher-quality products.

The current costs of quality are as follows:

Required:

1. Which costs of quality category are managers focusing on? Why?

2. If the improvements result in a 55% decrease in product repair costs and a 70% decrease in

lost sales from customer returns, what is the impact on the overall COQ and the company’s

operating income? What should iCover do? Explain.

3. Calculate prevention, appraisal, internal failure, and external failure costs as a percentage of

total quality costs and as a percentage of sales before and after the change in the production

process. Comment briefly on your results.

19-10