SOLUTION

(3050 min.) Review of Chapters 7 and 8, 3-variance analysis.

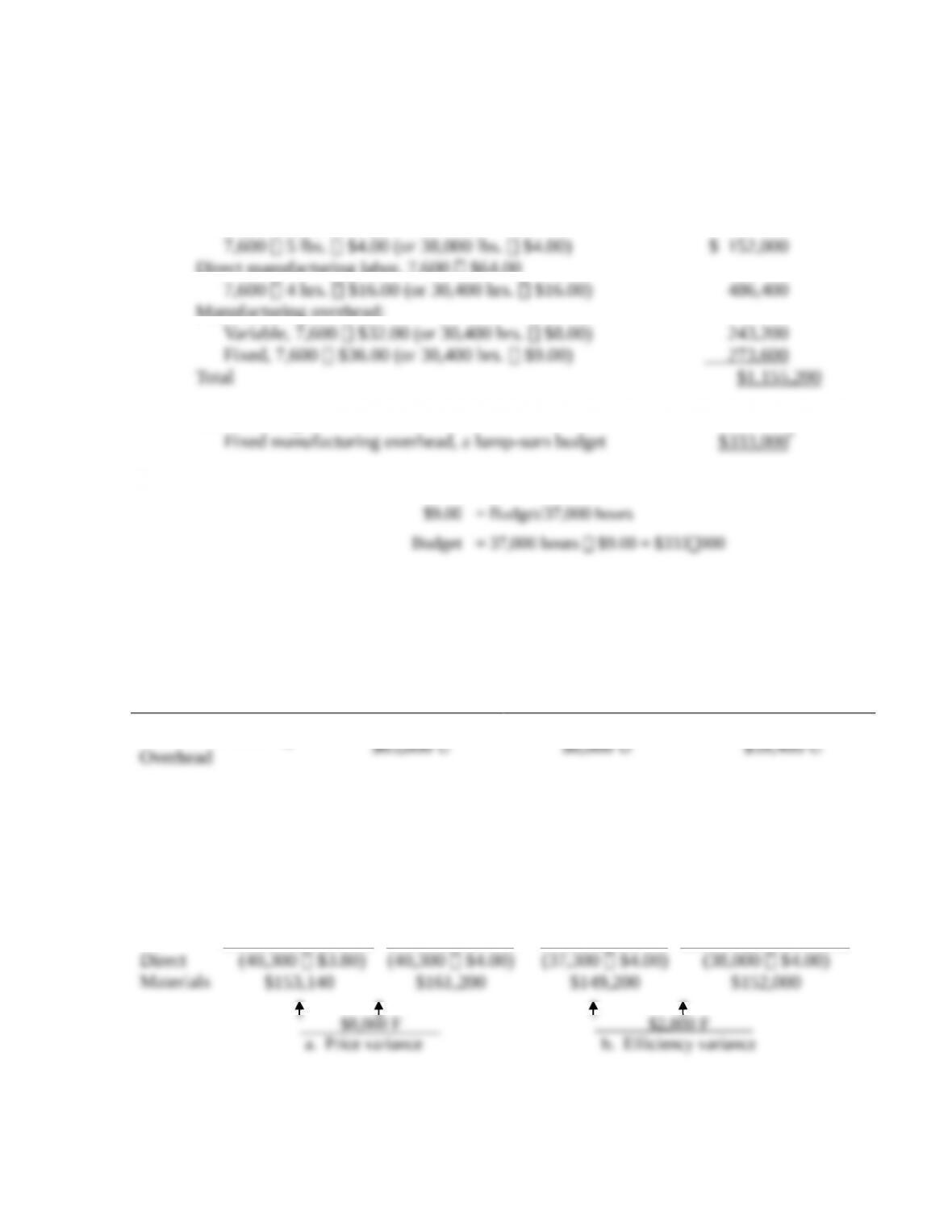

1. Total standard production costs are based on 7,600 units of output.

Direct materials, 7,600 $20.00

Direct manufacturing labor, 7,600 $64.00

Manufacturing overhead:

The following is for later use:

*Fixed manufacturing overhead rate =

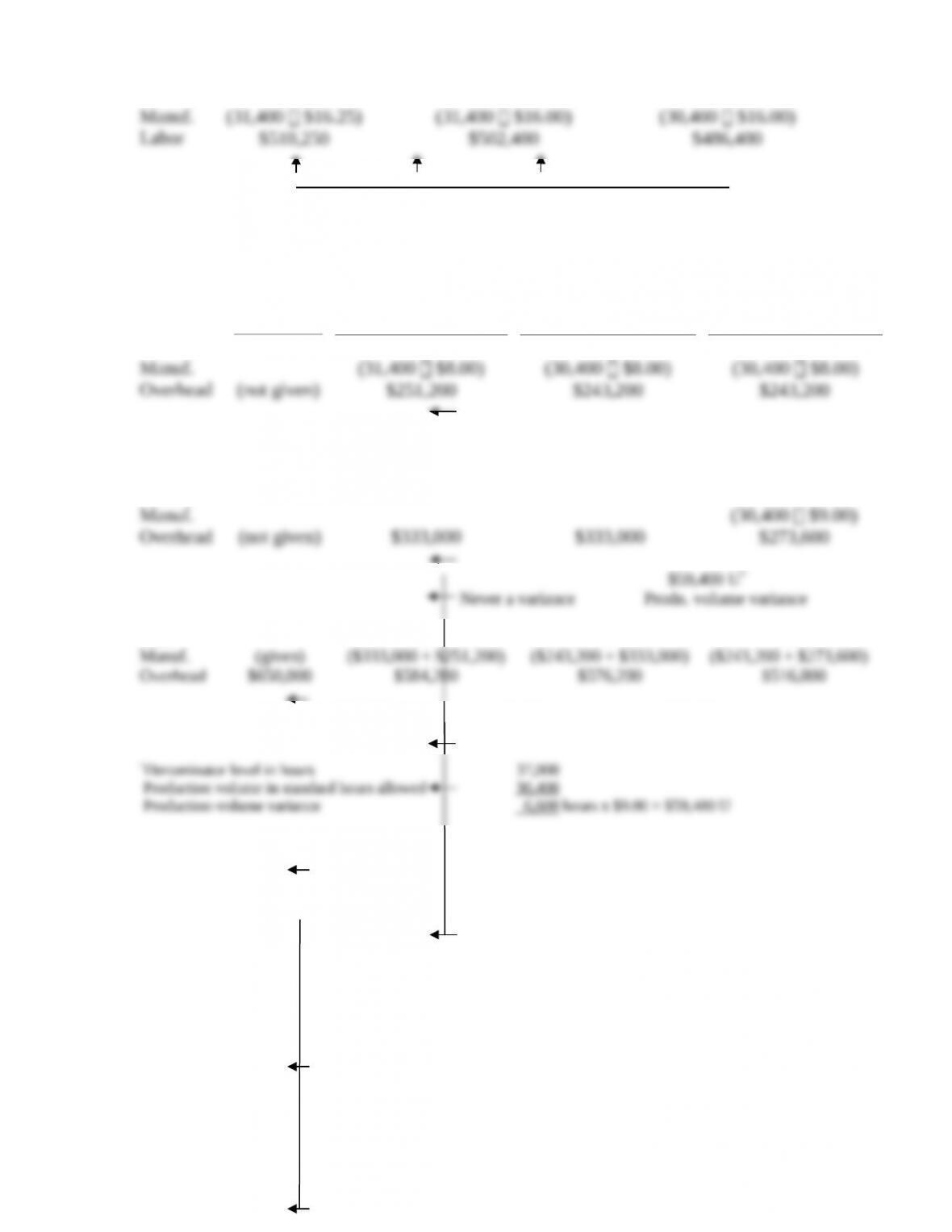

2. Solution Exhibit 8-44 presents a columnar presentation of the variances for Beal. An

overview of the 3-variance analysis using the block format of the text is:

3-Variance

Analysis

Spending

Variance

Efficiency

Variance

Production

Volume Variance

Total Manufacturing

SOLUTION EXHIBIT 8-44

Actual Costs

Incurred:

Actual Input Qty.

Actual Input Qty.

´

Budgeted Price

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

× Actual Rate Purchases Usage × Budgeted Price

Direct

$7,850 U $16,000 U

c. Price variance d. Efficiency variance

Actual

Costs

Incurred

Actual Input Qty.

Budgeted Rate

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

Budgeted Rate

Allocated:

(Budgeted Input Qty.

Allowed for

Actual Output

Budgeted Rate)

Variable

$8,000 U

Efficiency variance Never a variance

Fixed

Manuf.

(30,400 $9.00)

Total

Manuf.

(given)

($333,000 + $251,200)

($243,200 + $333,000)

($243,200 + $273,600)

$65,800 U $8,000 U $59,400 U

e. Spending variance f. Efficiency variance g. Prodn. volume variance

8-45 Nonfinancial variances. Kathy’s Kettle Potato Chips produces gourmet chips distributed

to chain sub shops throughout California. To ensure that their chips are of the highest quality and

have taste appeal, Kathy has a rigorous inspection process. For quality control purposes, Kathy

has a standard based on the number of pounds of chips inspected per hour and the number of

pounds that pass or fail the inspection.

Kathy expects that for every 1,000 pounds of chips produced, 200 pounds of chips will be

inspected. Inspection of 200 pounds of chips should take 1 hour. Kathy also expects that 1% of

the chips inspected will fail the inspection. During the month of May, Kathy produced 113,000

pounds of chips and inspected 22,300 pounds of chips in 120 hours. Of the 22,300 pounds of

chips inspected, 215 pounds of chips failed to pass the inspection.

Required:

1. Compute two variances that help determine whether the time spent on inspections was more

or less than expected. (Follow a format similar to the one used for the variable overhead

spending and efficiency variances, but without prices.)

2. Compute two variances that can be used to evaluate the percentage of the chips that fails the

inspection.

SOLUTION

(20 minutes) Non-financial variances

1. Variance Analysis of Inspection Hours for Kathy’s Kettle Potato Chips for May

Actual Pounds Standard Pounds Inspected

Actual Hours Inspected/Budgeted for Actual Output /Budgeted

For Inspections Pounds per hour Pounds per hour

2. Variance Analysis of Pounds Failing Inspection for Kathy’s Kettle Potato Chips for May

Actual pounds Standard Pounds Inspected

Actual Pounds Inspected × Budgeted for Actual Output × Budgeted

Failing Inspections Inspection Failure Rate Inspection Failure Rate

8-46 Overhead variances, service sector. Cavio is a cloud service provider that offers

computing resources to handle enterprise-wide applications. For March 2017, Cavio estimates

that it will provide 18,000 RAM hours of services to clients. The budgeted variable overhead rate

is $6 per RAM hour.

At the end of March, there is a $500 favorable spending variance for variable overhead and a

$1,575 unfavorable spending variance for fixed overhead. For the services actually provided

during the month, 14,850 RAM hours are budgeted and 15,000 RAM hours are actually used.

Total actual overhead costs are $119,875.

Required:

1. Compute efficiency and flexible-budget variances for Cavio’s variable overhead in March

2017. Will variable overhead be over- or underallocated? By how much?

2. Compute production-volume and flexible-budget variances for Cavio’s fixed overhead in

March 2017. Will fixed overhead be over- or underallocated? By how much?

SOLUTION

(30 minutes) Overhead variances, service sector

1. In the columnar presentation of variable overhead variance analysis, all numbers shown in

bold are calculated from the given information, in the order (a) – (e).

VARIABLE MANUFACTURING OVERHEAD

Flexible Budget:

Budgeted Input Qty.

Actual Costs

Incurred

Actual Input Qty.

´

Budgeted Rate

Allowed for Budgeted

Actual Output

´

Rate

(b) (a) (c)

15,000

´

$6.00 14,850

´

$6.00

RAM hrs. per RAM hr. RAM hrs. per RAM hr.

a. 15,000 RAM hours

´

$6 per RAM hour = $90,000

´

2. In the columnar presentation of fixed overhead variance analysis, all numbers shown in

bold are calculated from the given information, in the order (a) – (e).

FIXED MANUFACTURING OVERHEAD

Flexible Budget: Allocated:

Actual Costs

Static Budget Lump Sum

Regardless of Output

Budgeted Input Qty.

Allowed for Budgeted

Incurred Level

Actual Output

´

Rate

(a) (b)

14,850

´

$1.60* (c)

$1,575 U (e)

Flexible-budget variance

a. Actual FOH costs = $119,875 total overhead costs – $89,500 VOH costs = $30,375

¸

´

e. FOH flexible budget variance = FOH spending variance = $1,575 U

8-47 Direct-cost and overhead variances, income statement. The Greenspace Company

started business on January 1, 2017. The company adopted a standard costing system for the

production of ergonomic backpacks. Greenspace chose direct labor as the application base for

overhead and decided to use the proration method to account for variances at year-end.

In 2017, Greenspace expected to make and sell 160,000 backpacks; each was budgeted to use

2 yards of fabric and require 0.5 hours of direct labor work. The company expected to pay $2 per

yard for fabric and compensate workers at an hourly wage of $12. Greenspace has no variable

overhead costs, but budgeted $800,000 for fixed manufacturing overhead in 2017.

In 2017, Greenspace actually made 180,000 backpacks and sold 144,000 of them for a total

revenue of $2,592,000.

The costs incurred were as follows:

Fixed manufacturing costs $ 875,000

Fabric costs (370,000 yards bought and used) $ 758,500

Direct manufacturing labor costs (100,000 hours) $1,260,000

Required:

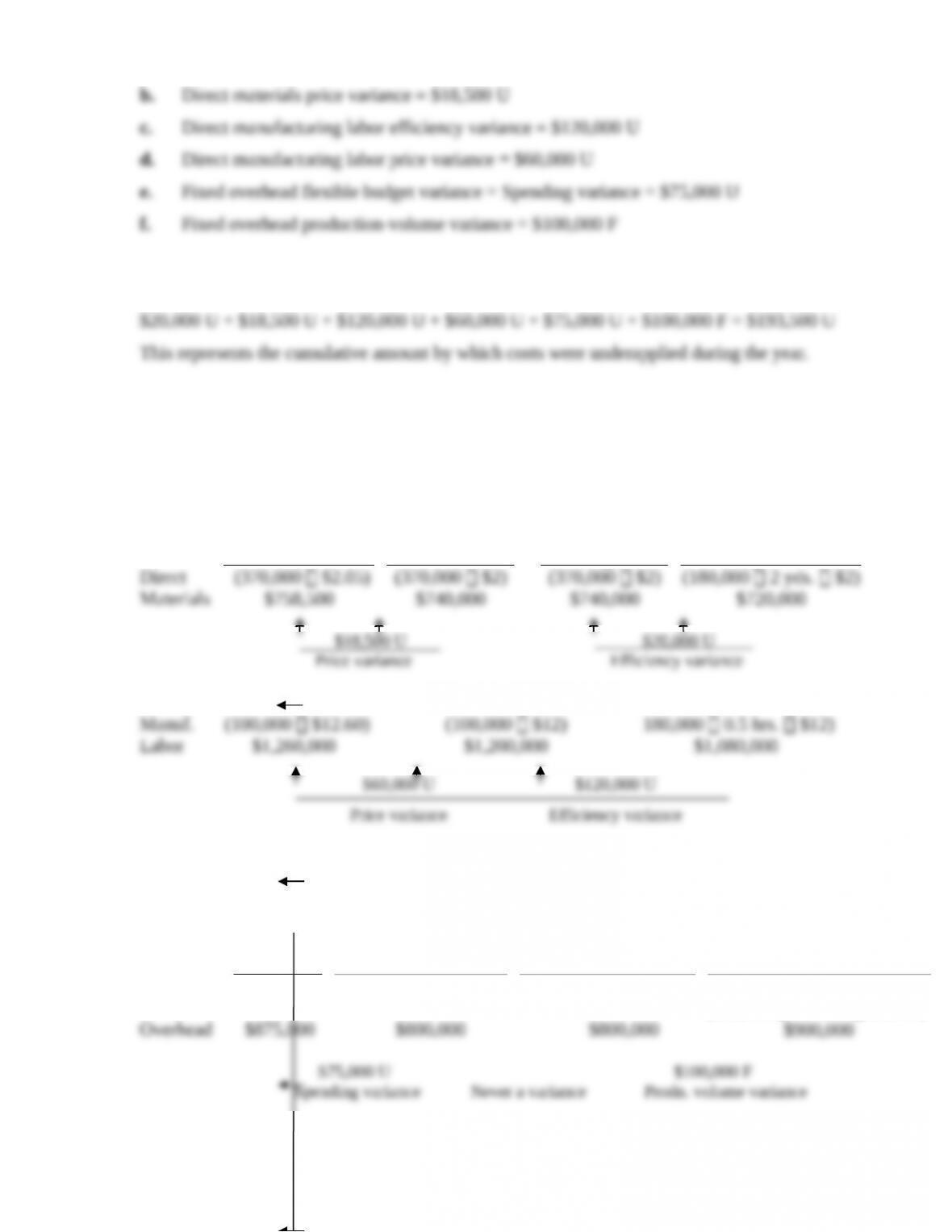

1. Compute the following variances for 2017, and indicate whether each is favorable (F) or

unfavorable (U):

a. Direct materials efficiency variance

b. Direct materials price variance

c. Direct manufacturing labor efficiency variance

d. Direct manufacturing labor price variance

e. Fixed overhead flexible-budget variance

f. Fixed overhead production-volume variance

2. Compute Greenspace Company’s gross margin for its first year of operation.

SOLUTION

(30 min.) Direct-cost and overhead variances, income statement.

Total standard production costs are based on 160,000 units of output.

Direct materials,

Direct manufacturing labor

Fixed manufacturing overhead

Fixed manufacturing overhead rate =

1. Solution Exhibit 8-47 presents a columnar presentation of the variances. Based on the

exhibit, the variances are as follows:

a. Direct materials efficiency variance = $20,000 U

Note that the total variances for the period equal:

SOLUTION EXHIBIT 8-47

Actual Costs

Incurred:

Actual Input Qty.

Actual Input Qty.

´

Budgeted Price

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

× Actual Rate Purchases Usage × Budgeted Price

Direct

Actual

Costs

Incurred

Actual Input Qty.

Budgeted Rate

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

Budgeted Rate

Allocated:

(Budgeted Input Qty.

Allowed for

Actual Output

Budgeted Rate)

Fixed

Manuf.

(180,000 0.5 hrs. $10.00)

2. Sales Revenue = 144,000 units sold × $18 = $2,592,000

Cost of Goods sold:

(+) Prorated share of underapplied cost:

= $277,200

8-48 Overhead variances, ethics. Carpenter Company uses standard costing. The company has

a manufacturing plant in Georgia. Standard labor-hours per unit are 0.50, and the variable

overhead rate for the Georgia plant is $3.50 per direct labor-hour. Fixed overhead for the Georgia

plant is budgeted at $1,800,000 for the year. Firm management has always used variance analysis

as a performance measure for the plant.

Tom Saban has just been hired as a new controller for Carpenter Company. Tom is good

friends with the Georgia plant manager and wants him to get a favorable review. Tom decides to

underestimate production, and budgets annual output of 1,200,000 units. His explanation for this

is that the economy is slowing and sales are likely to decrease.

At the end of the year, the plant reported the following actual results: output of 1,500,000

using 760,000 labor-hours in total, at a cost of $2,700,000 in variable overhead and $1,850,000

in fixed overhead.

Required:

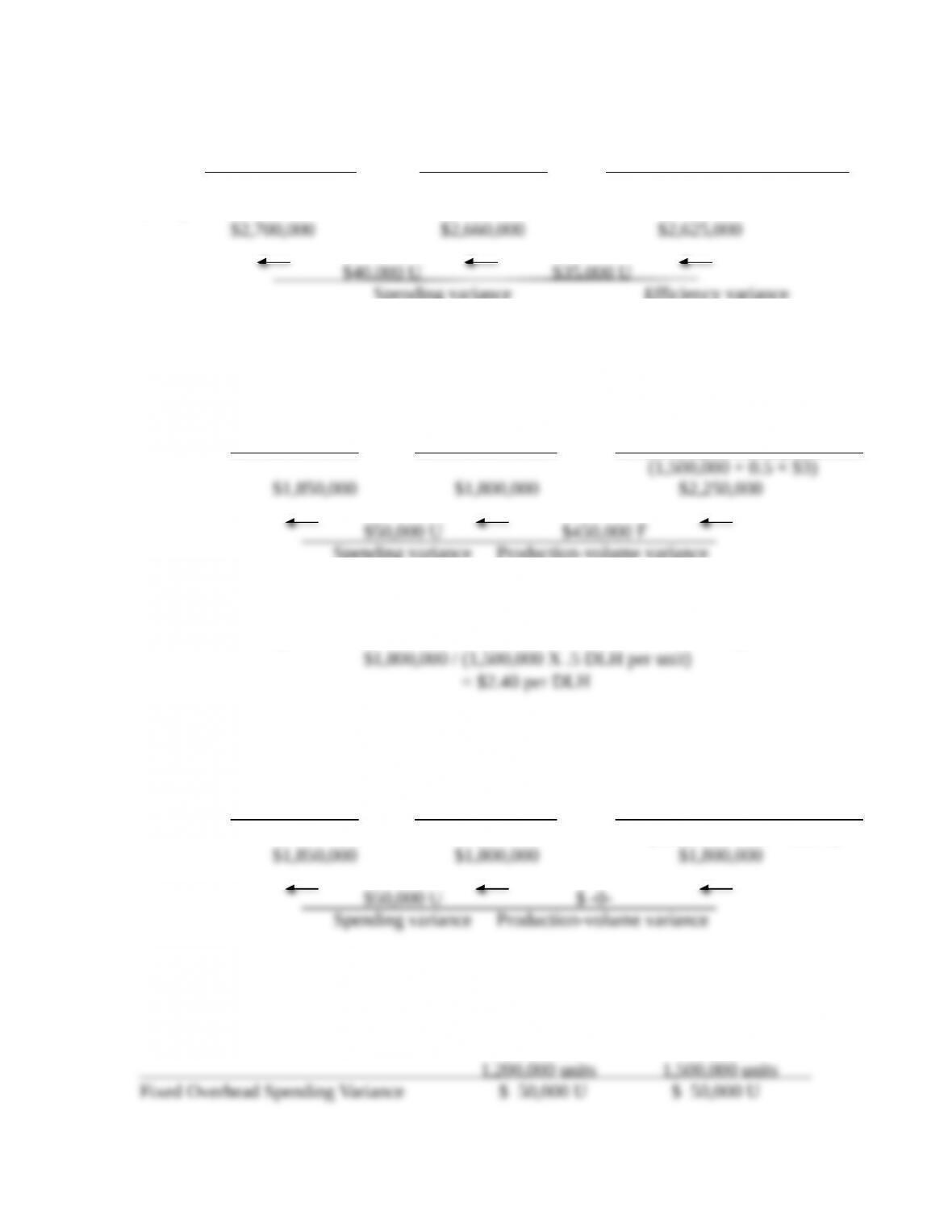

1. Compute the budgeted fixed cost per labor-hour for the fixed overhead.

2. Compute the variable overhead spending variance and the variable overhead efficiency

variance.

3. Compute the fixed overhead spending and volume variances.

4. Compute the budgeted fixed cost per labor-hour for the fixed overhead if Tom Saban had

estimated production more realistically at the expected sales level of 1,500,000 units.

5. Summarize the fixed overhead variance based on both the projected level of production of

1,200,000 units and 1,500,000 units.

6. Did Tom Saban’s attempt to make his friend, the plant manager, look better work? Why or

why not?

7. What do you think of Tom Saban’s behavior overall?

SOLUTION

(40 minutes) Overhead variances, ethics

1. Budget Fixed Overhead per Labor Hour =

2. Variable overhead variances:

Actual Actual hours Budgeted input allowed for

Variable Overhead × Budgeted rate Actual output × Budgeted rate

(760,000 × $3.50) (1,500,000 × 0.5 ×

$3.50)

Spending variance Efficiency variance

3. Fixed overhead variances:

Actual Static Budget Budgeted input allowed for

Fixed Overhead Fixed Overhead Actual output × Budgeted Rate

Spending variance Production-volume variance

4. Budget Fixed Overhead per Labor Hour =

Budgeted Fixed Overhead / Standard Direct Labor Hours for Budgeted Production

5. Fixed overhead variances with realistic budget:

Actual Static Budget Budgeted input allowed for

Fixed Overhead Fixed Overhead Actual output × Budgeted Rate

(1,500,000 × 0.5 × $2.40)

Fixed Manufacturing Overhead Variances:

Manipulated Realistic Expected

Production Production

6. Tom Saban made it appear as though his friend, the plant manager, did better than the level

at which he actually performed. The fixed overhead spending variance was unaffected by

the manipulation of expected production since it relies on a comparison of the budgeted to

actual cost realizations. However, the fixed overhead product-volume variance was

7. Tom Saban’s behavior is not ethical. He attempted to make his friend better off by

Try It! 8-1

a. Budgeted variable overhead = $25 per hour × (25,000 × 0.75) machine-hours

b. Variable overhead spending variance = ($25 − $23) × 19,050

c. Variable overhead efficiency variance = [19,050 − (27,000 × 0.75)] × $25

Try It! 8-2

a. Fixed overhead rate = (Expected overhead ÷ Expected labor hours)

b. Budgeted fixed overhead per month = $648,000/12

c. Budgeted labor hours per unit = 21,600/540,000

Try It! 8-3

a. Both (A) and (B) are zero. There is never a production-volume variance for variable

manufacturing overhead or an efficiency variance for fixed manufacturing overhead.

Try It! 8-4

a. Spending variance = $12,000 – $9,975

b. Normal setup hours = (11,250/225 units per batch) × 5.25 hours per batch

Fixed setup overhead rate = $9,975/262.5

c. Fixed setup overhead allocation = [(15,000/225) × 5.25 × $38]